Key Insights

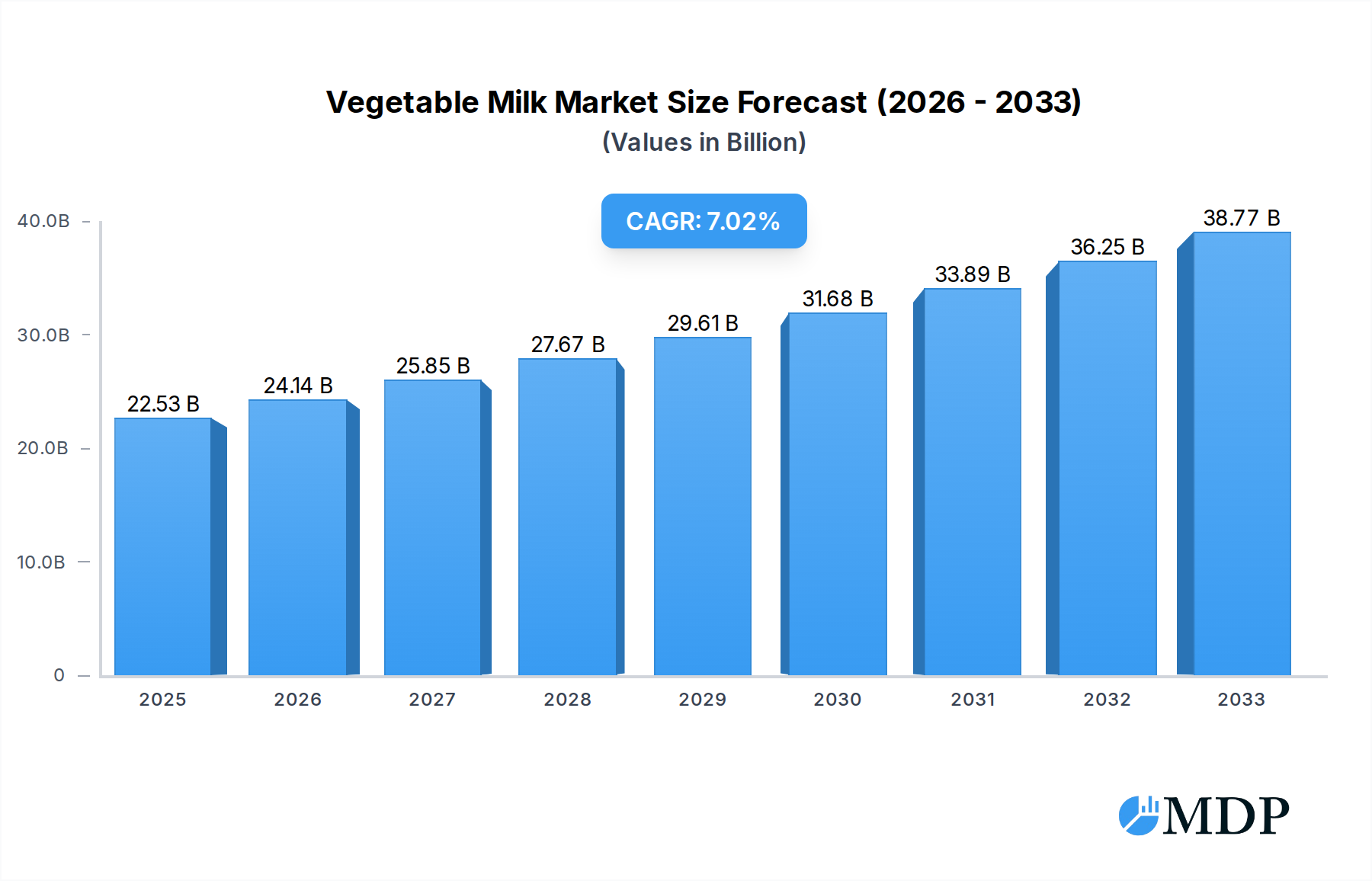

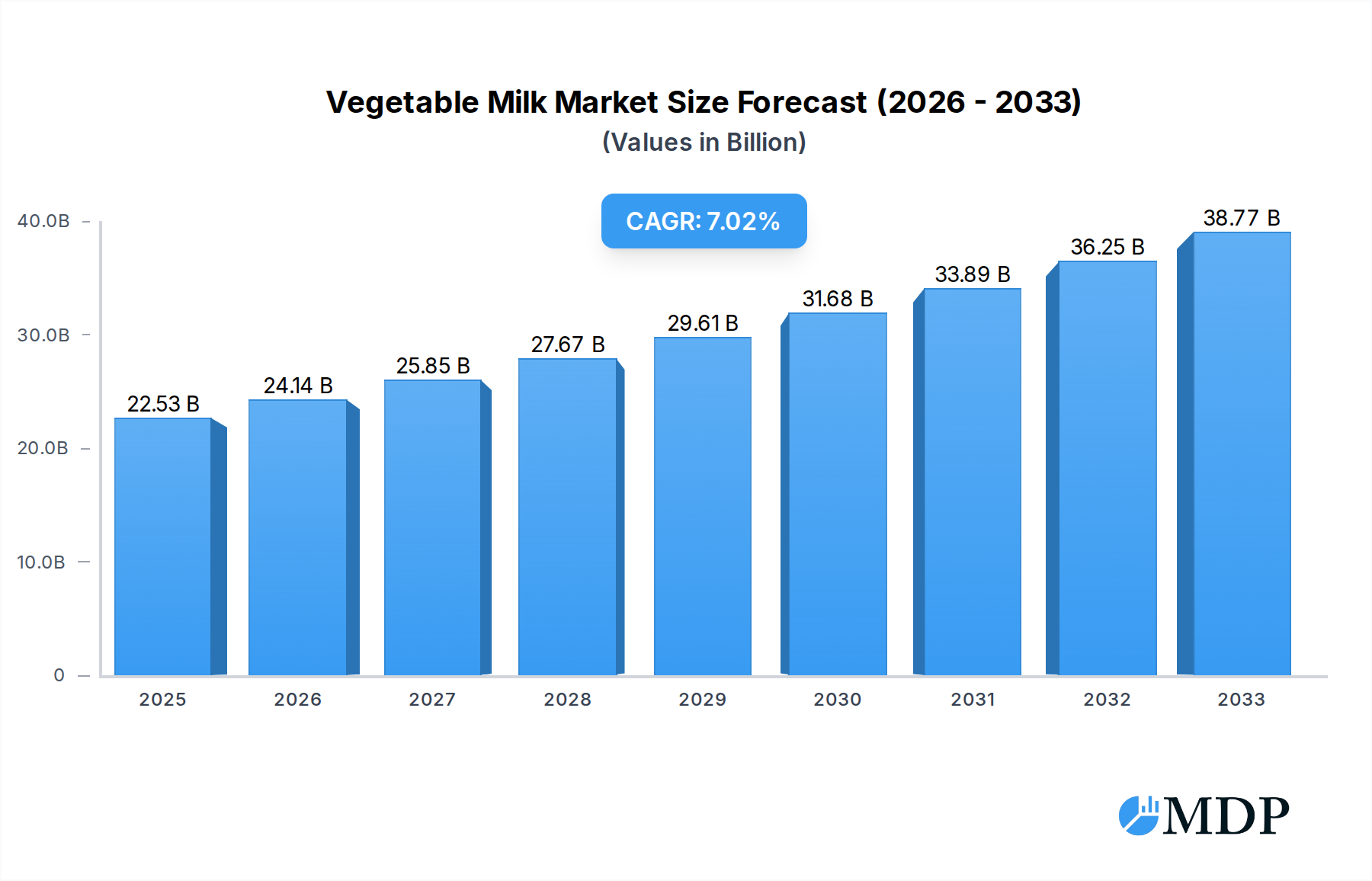

The global Vegetable Milk market is projected for robust expansion, reaching an estimated $22.53 billion by 2025. This growth is fueled by a compelling CAGR of 7.53% over the forecast period of 2025-2033. A significant surge in consumer awareness regarding the health benefits associated with plant-based diets, coupled with a rising incidence of lactose intolerance and dairy allergies, are primary market accelerators. Consumers are actively seeking alternatives to traditional dairy products, driven by both nutritional and ethical considerations. Furthermore, the increasing availability and diversification of vegetable milk options, encompassing a wider array of ingredients beyond traditional soy and almond, are attracting a broader consumer base. The market's dynamism is further evidenced by continuous innovation in product formulations, aiming to improve taste, texture, and nutritional profiles, thereby enhancing consumer appeal and driving demand across various market segments.

Vegetable Milk Market Size (In Billion)

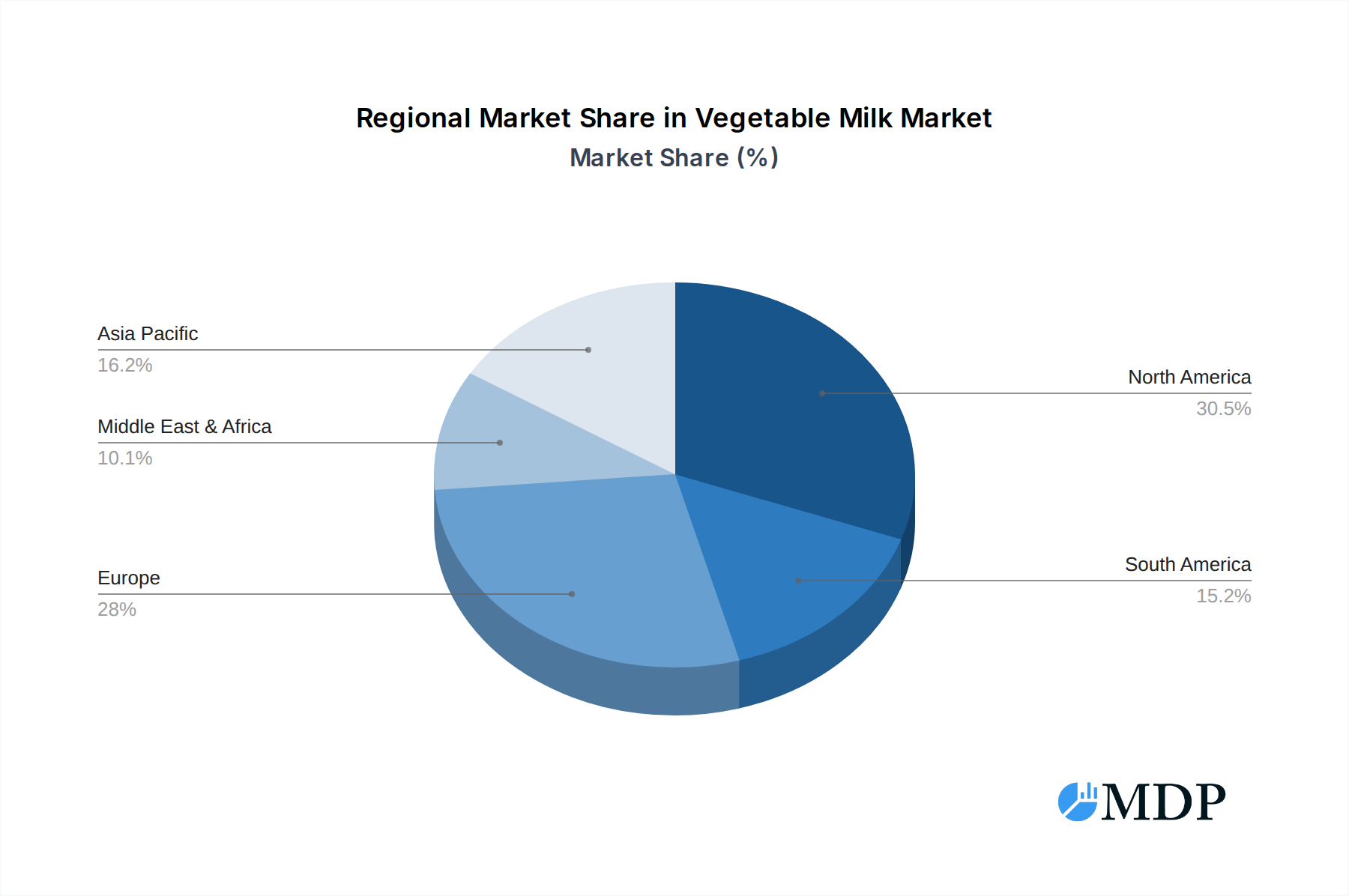

The market's expansion is anticipated to be driven by several key factors. Growing health consciousness among consumers, an increasing demand for lactose-free and vegan options, and environmental concerns related to conventional dairy farming are significant drivers. The burgeoning trend of flexitarian and plant-based diets worldwide is a major contributor to this market's upward trajectory. From a segmentation perspective, Supermarkets and Hypermarkets are expected to dominate sales channels due to their widespread reach and product variety, while Online Retailers are set to witness substantial growth, reflecting changing consumer shopping habits. In terms of product type, Legumes and Nuts are likely to remain the most popular bases for vegetable milk, appealing to a wide range of dietary preferences and nutritional needs. The market is witnessing active participation from key companies like Danone, WhiteWave Foods, and Ripple Foods, who are instrumental in product innovation and market penetration across major regions including North America, Europe, and Asia Pacific, with the latter showing immense potential for future growth.

Vegetable Milk Company Market Share

Unlocking the Billion-Dollar Vegetable Milk Market: A Comprehensive Growth & Innovation Report (2019-2033)

Dive into the booming vegetable milk market, a sector projected to reach over one billion dollars in valuation by 2025. This in-depth report, covering the historical period of 2019-2024 and a forecast period through 2033, provides unparalleled insights for industry stakeholders, investors, and manufacturers. With a base year of 2025 and an estimated year also in 2025, this analysis offers a granular view of market dynamics, trends, and future opportunities. Our research meticulously covers key players such as Ripple Foods, Danone, WhiteWave Foods, Archer-Daniels-Midland, Hain Celestial Group, Califia Farms, Daiya Foods, and Freedom Foods, along with emerging innovators.

Vegetable Milk Market Dynamics & Concentration

The vegetable milk market is experiencing dynamic shifts, characterized by robust innovation and increasing consumer adoption. Market concentration is gradually diversifying, moving from a few dominant players to a more fragmented landscape with the emergence of niche brands and private labels. Key drivers of innovation include the pursuit of enhanced nutritional profiles, improved taste and texture, and the development of sustainable sourcing and production methods. Regulatory frameworks, while generally supportive of plant-based alternatives, are evolving to address labeling standards and ingredient transparency, influencing product development and market entry strategies. Product substitutes, ranging from traditional dairy milk to other beverages, continue to exert competitive pressure, necessitating continuous product differentiation. End-user trends are overwhelmingly shifting towards health-conscious and environmentally aware consumers, fueling demand for plant-based options. Merger and acquisition (M&A) activities within the sector, though currently at a modest level with an estimated ten billion dollars in deal value and fifty M&A deals throughout the historical period, are anticipated to accelerate as larger corporations seek to expand their plant-based portfolios and smaller innovative companies seek capital for growth. The market share of leading players like Danone and WhiteWave Foods remains significant, but the growth of companies like Ripple Foods and Califia Farms indicates a healthy competitive environment.

Vegetable Milk Industry Trends & Analysis

The vegetable milk industry is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of fifteen percent from 2025 to 2033. This impressive trajectory is driven by a confluence of factors, including escalating consumer awareness of the health benefits associated with plant-based diets and a growing concern for environmental sustainability. Technological disruptions are at the forefront of this evolution, with advancements in ingredient processing, flavor enhancement, and the development of novel plant-based sources contributing to the creation of more palatable and nutritionally equivalent alternatives to dairy. Consumer preferences are undeniably leaning towards plant-based milk, fueled by the demand for lactose-free options, reduced saturated fat intake, and ethical considerations surrounding animal welfare. The market penetration of vegetable milk is rapidly increasing, moving beyond early adopters to mainstream consumers. Competitive dynamics are intensifying, with established food giants and agile startups alike vying for market share. This has led to aggressive product development, innovative marketing campaigns, and strategic partnerships aimed at capturing consumer attention. The global market size, estimated at fifty billion dollars in 2025, is expected to surpass one hundred billion dollars by the end of the forecast period, reflecting the strong underlying growth drivers and the enduring appeal of these dairy alternatives. The integration of advanced processing techniques, such as ultra-high temperature (UHT) processing and enzyme hydrolysis, is enhancing shelf-life and sensory qualities, further propelling market acceptance and expansion.

Leading Markets & Segments in Vegetable Milk

The vegetable milk market exhibits significant dominance in North America, with the United States leading the charge due to strong consumer demand for plant-based alternatives and a well-established retail infrastructure. Within this leading region, Supermarkets and Hypermarkets represent the most dominant application segment, accounting for an estimated sixty percent of total sales. This is driven by the convenience and accessibility offered to a broad consumer base. However, Online Retailers are experiencing rapid growth, projected to capture an additional twenty-five percent of the market share by 2033, fueled by the increasing preference for e-commerce for grocery purchases.

Dominant Type Segments:

- Legumes: Soy milk continues to hold a significant market share, driven by its long history, affordability, and established nutritional profile. Its market share is projected to remain at thirty percent in 2025, with moderate growth.

- Nuts: Almond milk has seen explosive growth and is expected to maintain its position as a leading type, accounting for an estimated thirty-five percent of the market in 2025. Its popularity is attributed to its perceived health benefits and mild flavor.

- Cereals: Oat milk has emerged as a significant contender, experiencing rapid expansion due to its creamy texture and versatility. Its market share is projected to grow to twenty-five percent by 2033.

- Seeds: Seed-based milks, such as those made from hemp and sunflower seeds, represent a smaller but growing segment, offering unique nutritional benefits and catering to allergen-conscious consumers.

Key Drivers of Dominance:

- Economic Policies: Favorable government initiatives and subsidies supporting plant-based agriculture contribute to cost competitiveness.

- Infrastructure: A well-developed cold chain and distribution network in key regions ensures efficient product availability.

- Consumer Awareness: Widespread media coverage and health campaigns highlighting the benefits of plant-based diets are crucial.

- Product Innovation: Continuous development of new flavors, fortified options, and allergen-free varieties caters to diverse consumer needs.

Vegetable Milk Product Developments

Product innovation in the vegetable milk sector is characterized by a focus on enhanced nutritional profiles, improved taste, and diverse applications. Manufacturers are actively developing fortified varieties with added vitamins and minerals, such as calcium and vitamin D, to better mimic the nutritional composition of dairy milk. Advances in processing technologies are leading to smoother textures and more neutral flavors, making them suitable for direct consumption, coffee, baking, and cooking. Competitive advantages are being built through unique ingredient sourcing, such as organic or sustainably grown legumes and nuts, and through the creation of specialized products targeting specific dietary needs, like low-sugar or high-protein options. The market is witnessing an influx of novel plant-based milk alternatives, expanding beyond traditional options to include those derived from ancient grains and exotic fruits.

Key Drivers of Vegetable Milk Growth

The growth of the vegetable milk market is propelled by several interconnected factors. Technologically, advancements in extraction and processing methods are improving taste, texture, and nutritional value, making plant-based options more appealing. Economically, the declining cost of raw materials for plant-based milks, coupled with increasing consumer purchasing power for premium health products, is a significant driver. Regulatory support for plant-based food industries and clear labeling guidelines are also fostering market expansion. Furthermore, the rising awareness of the environmental impact of traditional dairy farming is pushing consumers towards sustainable alternatives, directly fueling the demand for vegetable milk.

Challenges in the Vegetable Milk Market

Despite its robust growth, the vegetable milk market faces several challenges. Regulatory hurdles, particularly concerning naming conventions and fortification standards that align with dairy milk, can create confusion for consumers and manufacturers alike. Supply chain issues, including the availability and consistent quality of raw ingredients for certain plant-based milks, can impact production costs and scalability. Competitive pressures from both established dairy brands launching their own plant-based lines and the sheer volume of new entrants necessitate continuous innovation and effective marketing strategies. The perceived price premium for some vegetable milk varieties compared to conventional dairy milk can also be a barrier to mass adoption in price-sensitive markets.

Emerging Opportunities in Vegetable Milk

Emerging opportunities in the vegetable milk market are vast and varied. Technological breakthroughs in precision fermentation are paving the way for the creation of animal-free dairy proteins, which can be incorporated into plant-based milks to achieve unparalleled taste and functionality. Strategic partnerships between ingredient suppliers and beverage manufacturers are crucial for developing novel formulations and expanding production capacities. Market expansion into untapped geographical regions, particularly in emerging economies where interest in health and wellness is growing, presents significant potential. Furthermore, the development of plant-based milk derivatives, such as yogurts, cheeses, and ice creams, leverages existing consumer familiarity and infrastructure to drive further category growth.

Leading Players in the Vegetable Milk Sector

- Ripple Foods

- Danone

- WhiteWave Foods

- Archer-Daniels-Midland

- Hain Celestial Group

- Califia Farms

- Daiya Foods

- Freedom Foods

Key Milestones in Vegetable Milk Industry

- 2019: Increased investment in oat milk production by key players, leading to broader market availability.

- 2020: Launch of innovative, allergen-free seed-based milk alternatives, expanding consumer choice.

- 2021: Significant advancements in UHT processing technology for plant-based milks, enhancing shelf-life and distribution reach.

- 2022: Growing consumer demand for fortified vegetable milks, driving product development with added vitamins and minerals.

- 2023: Strategic acquisitions and partnerships aimed at consolidating market share and expanding product portfolios.

- 2024: Increased focus on sustainable packaging solutions and ethical sourcing practices within the industry.

Strategic Outlook for Vegetable Milk Market

The strategic outlook for the vegetable milk market is exceptionally bright, driven by sustained consumer demand for healthier, more sustainable, and ethically produced food options. Growth accelerators include the continuous innovation in product formulations to meet diverse dietary needs and taste preferences, alongside expansion into new product categories derived from plant-based milk bases. Strategic partnerships with technology providers for advanced processing and ingredient development will be key. Furthermore, market penetration in emerging economies, supported by targeted marketing campaigns and accessible distribution channels, will fuel substantial long-term growth, solidifying vegetable milk's position as a dominant force in the global beverage industry.

Vegetable Milk Segmentation

-

1. Application

- 1.1. Supermarkets and Hypermarkets

- 1.2. Specialist Retailers

- 1.3. Online Retailers

- 1.4. Others

-

2. Type

- 2.1. Legumes

- 2.2. Cereals

- 2.3. Nuts

- 2.4. Seeds

- 2.5. Others

Vegetable Milk Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Vegetable Milk Regional Market Share

Geographic Coverage of Vegetable Milk

Vegetable Milk REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.53% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Vegetable Milk Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Supermarkets and Hypermarkets

- 5.1.2. Specialist Retailers

- 5.1.3. Online Retailers

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Legumes

- 5.2.2. Cereals

- 5.2.3. Nuts

- 5.2.4. Seeds

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Vegetable Milk Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Supermarkets and Hypermarkets

- 6.1.2. Specialist Retailers

- 6.1.3. Online Retailers

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Legumes

- 6.2.2. Cereals

- 6.2.3. Nuts

- 6.2.4. Seeds

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Vegetable Milk Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Supermarkets and Hypermarkets

- 7.1.2. Specialist Retailers

- 7.1.3. Online Retailers

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Legumes

- 7.2.2. Cereals

- 7.2.3. Nuts

- 7.2.4. Seeds

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Vegetable Milk Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Supermarkets and Hypermarkets

- 8.1.2. Specialist Retailers

- 8.1.3. Online Retailers

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Legumes

- 8.2.2. Cereals

- 8.2.3. Nuts

- 8.2.4. Seeds

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Vegetable Milk Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Supermarkets and Hypermarkets

- 9.1.2. Specialist Retailers

- 9.1.3. Online Retailers

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Legumes

- 9.2.2. Cereals

- 9.2.3. Nuts

- 9.2.4. Seeds

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Vegetable Milk Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Supermarkets and Hypermarkets

- 10.1.2. Specialist Retailers

- 10.1.3. Online Retailers

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Legumes

- 10.2.2. Cereals

- 10.2.3. Nuts

- 10.2.4. Seeds

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Ripple Foods

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Danone

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 WhiteWave Foods

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Archer-Daniels-Midland

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Hain Celestial Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Califia Farms

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Daiya Foods

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Freedom Foods

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Ripple Foods

List of Figures

- Figure 1: Global Vegetable Milk Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Vegetable Milk Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Vegetable Milk Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Vegetable Milk Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Vegetable Milk Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Vegetable Milk Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Vegetable Milk Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Vegetable Milk Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Vegetable Milk Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Vegetable Milk Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Vegetable Milk Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Vegetable Milk Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Vegetable Milk Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Vegetable Milk Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Vegetable Milk Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Vegetable Milk Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Vegetable Milk Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Vegetable Milk Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Vegetable Milk Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Vegetable Milk Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Vegetable Milk Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Vegetable Milk Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Vegetable Milk Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Vegetable Milk Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Vegetable Milk Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Vegetable Milk Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Vegetable Milk Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Vegetable Milk Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Vegetable Milk Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Vegetable Milk Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Vegetable Milk Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Vegetable Milk Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Vegetable Milk Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Vegetable Milk Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Vegetable Milk Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Vegetable Milk Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Vegetable Milk Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Vegetable Milk Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Vegetable Milk Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Vegetable Milk Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Vegetable Milk Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Vegetable Milk Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Vegetable Milk Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Vegetable Milk Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Vegetable Milk Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Vegetable Milk Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Vegetable Milk Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Vegetable Milk Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Vegetable Milk Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Vegetable Milk Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vegetable Milk?

The projected CAGR is approximately 7.53%.

2. Which companies are prominent players in the Vegetable Milk?

Key companies in the market include Ripple Foods, Danone, WhiteWave Foods, Archer-Daniels-Midland, Hain Celestial Group, Califia Farms, Daiya Foods, Freedom Foods.

3. What are the main segments of the Vegetable Milk?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vegetable Milk," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vegetable Milk report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vegetable Milk?

To stay informed about further developments, trends, and reports in the Vegetable Milk, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence