Key Insights

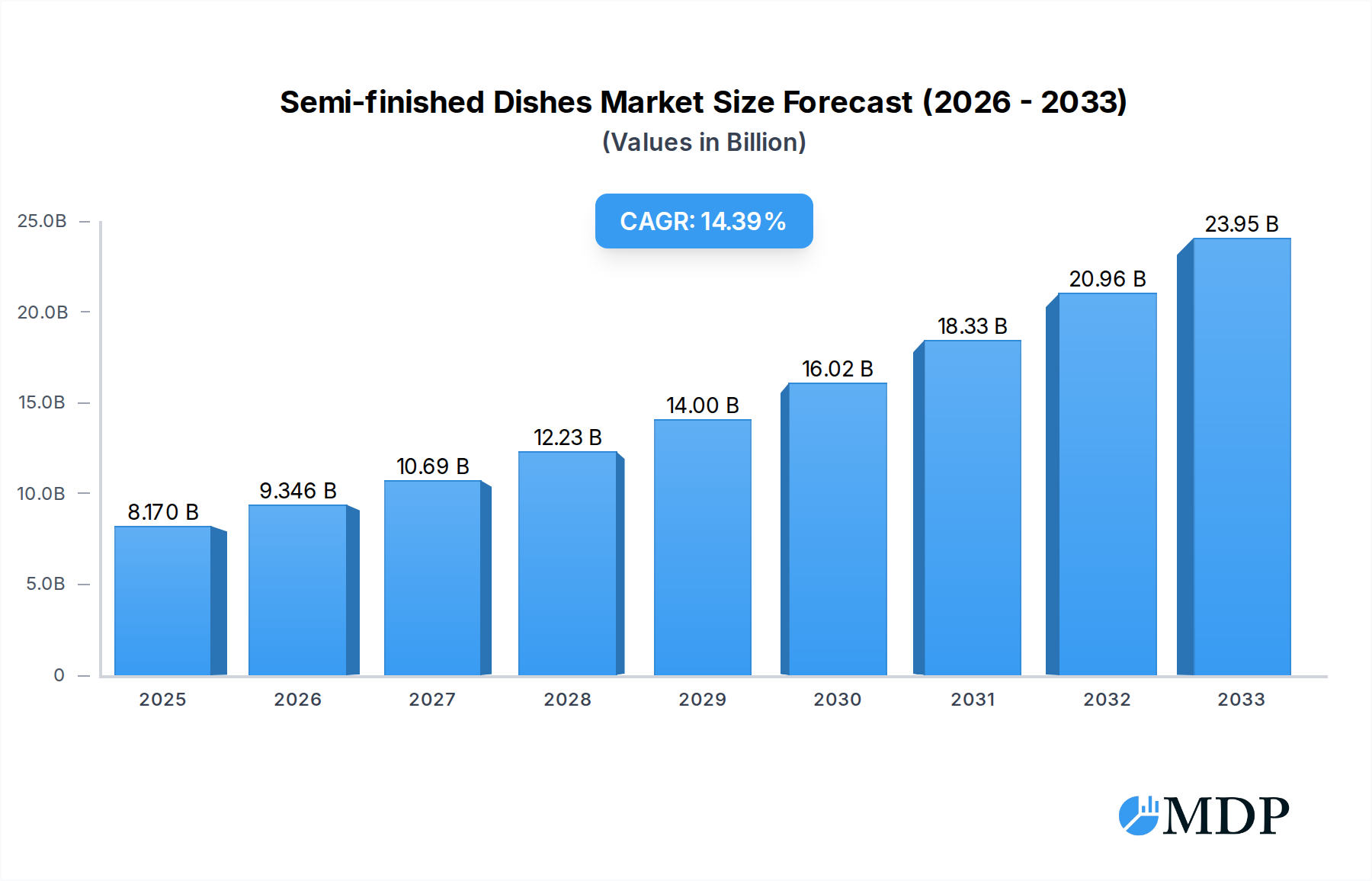

The global Semi-finished Dishes market is poised for substantial growth, projected to reach $8.17 billion by 2025. This robust expansion is driven by evolving consumer lifestyles, increasing demand for convenience, and a growing preference for ready-to-cook meals. The market is experiencing a significant CAGR of 14.44%, indicating a dynamic and rapidly expanding sector. Key drivers include the rise of dual-income households, busy urban lifestyles, and a heightened awareness of healthy eating habits, which are being met by the convenience offered by semi-finished dishes. Furthermore, advancements in food processing technology and expanding distribution channels, particularly through online sales platforms, are further fueling this growth trajectory. The convenience factor, coupled with the ability to provide diverse culinary experiences at home, makes semi-finished dishes an attractive option for a broad consumer base.

Semi-finished Dishes Market Size (In Billion)

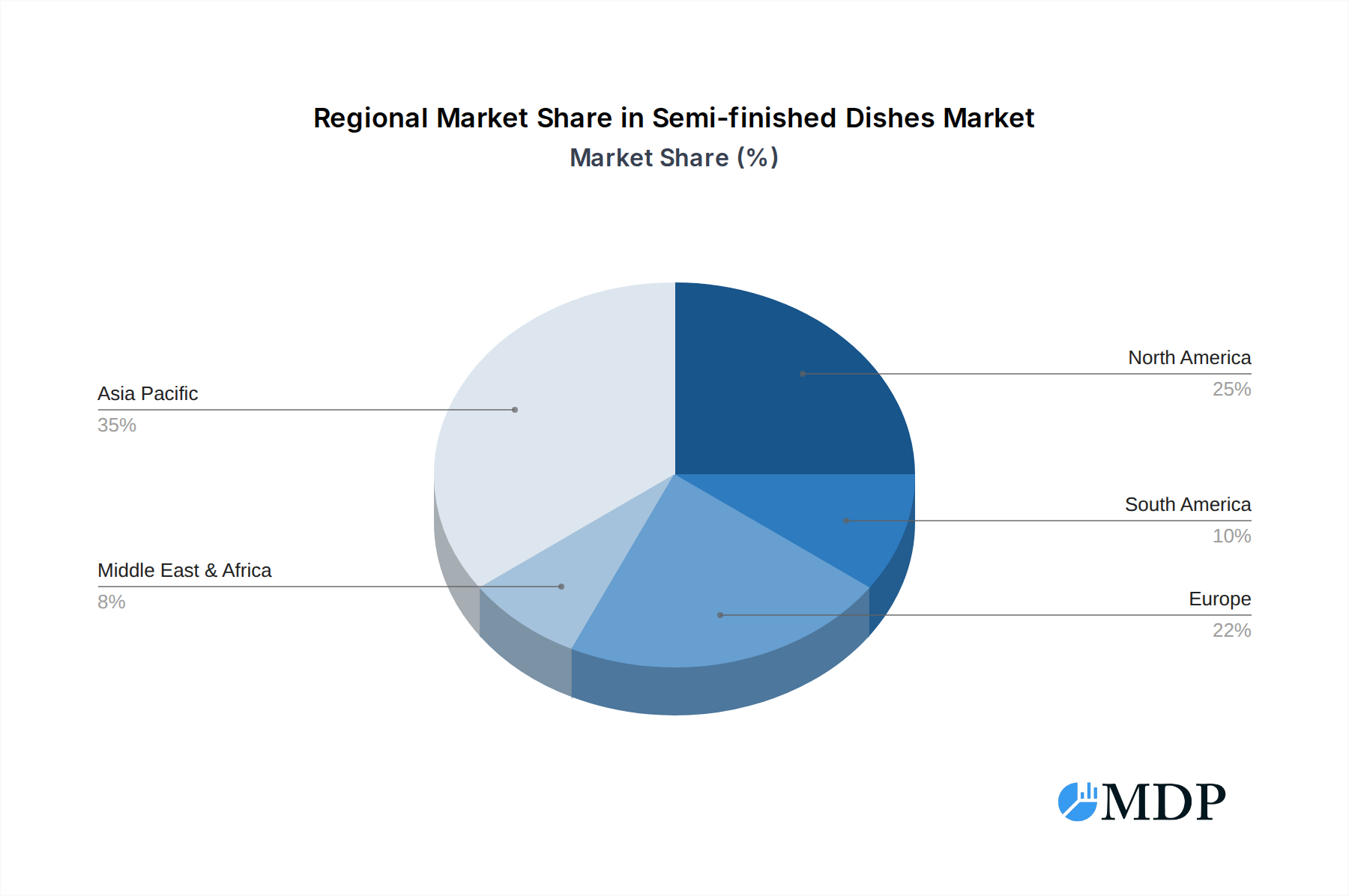

The market's segmentation reveals a strong inclination towards "Online Sales" as a primary distribution channel, reflecting the digital shift in consumer purchasing habits. In terms of product types, "Bagged" and "Boxed" formats are expected to dominate, offering consumer-friendly packaging and extended shelf life. Geographically, the Asia Pacific region, led by China, is anticipated to be a significant contributor to market expansion due to its large population and increasing disposable incomes. North America and Europe also present substantial opportunities, driven by the widespread adoption of convenience foods. While the market is characterized by strong growth, potential restraints could include intense competition, fluctuating raw material prices, and the need for continuous innovation to cater to evolving consumer tastes and dietary preferences. However, the overarching trend of convenience-seeking consumers and the increasing sophistication of product offerings are expected to outweigh these challenges, solidifying the positive market outlook.

Semi-finished Dishes Company Market Share

Semi-finished Dishes Market: Global Report 2025-2033 - Unlocking Opportunities in a Billion-Dollar Industry

This comprehensive report delves into the global semi-finished dishes market, a dynamic sector poised for significant expansion. With a study period from 2019 to 2033, including a base year of 2025 and a forecast period spanning 2025 to 2033, this analysis provides invaluable insights for industry stakeholders seeking to capitalize on emerging trends and drive sustainable growth. The report meticulously examines market dynamics, industry trends, leading markets, product innovations, growth drivers, challenges, emerging opportunities, key players, historical milestones, and strategic outlooks, all within a projected billion-dollar valuation. Leveraging high-traffic keywords such as "frozen ready meals," "meal kits," "convenience food," "foodservice solutions," and "private label frozen food," this report aims to maximize search visibility and attract a wide spectrum of industry professionals, from manufacturers and distributors to retailers and investors.

Semi-finished Dishes Market Dynamics & Concentration

The global semi-finished dishes market exhibits a moderate to high concentration, with key players like PFI Foods, JBS Foods, Tyson Foods, SYSCO, and Kobe Bussan holding substantial market shares. Innovation remains a primary driver, fueled by consumer demand for convenient, healthy, and diverse meal options. Technological advancements in food processing, preservation, and packaging are continuously shaping product offerings. Regulatory frameworks, particularly concerning food safety, labeling, and ingredient sourcing, play a crucial role in market accessibility and product development. The availability of readily accessible ingredients and the increasing adoption of advanced food processing technologies are contributing to market growth. Product substitutes, including fresh meal kits and restaurant takeaways, present a competitive landscape, yet the convenience and longer shelf-life of semi-finished dishes offer a distinct advantage. End-user trends are increasingly leaning towards healthier, plant-based, and globally inspired flavor profiles. Mergers and acquisitions (M&A) activities are observed as companies seek to expand their product portfolios, geographical reach, and market dominance. For instance, the M&A deal count is projected to be in the xx range during the forecast period. The market share of the top five players is estimated to be around xx billion in 2025.

Semi-finished Dishes Industry Trends & Analysis

The semi-finished dishes industry is experiencing robust growth, driven by a confluence of factors that are reshaping consumer habits and market dynamics. The increasing pace of modern life, coupled with a growing disposable income in many regions, has amplified the demand for convenient food solutions. Consumers are actively seeking ways to reduce time spent on meal preparation without compromising on taste or nutritional value. This fundamental shift in consumer preference serves as a primary catalyst for market expansion. The compound annual growth rate (CAGR) for the semi-finished dishes market is projected to be around xx% from 2025 to 2033, indicating a sustained upward trajectory.

Technological disruptions are also playing a pivotal role. Advancements in freezing technology, rapid chilling, and sophisticated packaging solutions are enhancing the quality, shelf-life, and variety of semi-finished dishes available. These innovations not only preserve the freshness and flavor of ingredients but also enable manufacturers to offer a wider array of culinary options, catering to diverse global palates. The integration of AI and automation in production processes is also contributing to increased efficiency and reduced costs, further stimulating market growth.

Consumer preferences are evolving rapidly. There's a discernible trend towards healthier options, with a growing demand for dishes that are low in sodium, sugar, and unhealthy fats. The rise of plant-based diets and flexitarianism has led to an increased interest in vegetarian and vegan semi-finished dishes, prompting manufacturers to expand their offerings in these categories. Furthermore, consumers are increasingly seeking transparency in ingredients and sourcing, pushing for cleaner labels and ethically produced food products. The desire for authentic global flavors and unique culinary experiences is also a significant trend, leading to the introduction of a wider range of ethnic and gourmet semi-finished dishes.

Competitive dynamics within the industry are intensifying. Established food manufacturers are investing heavily in research and development to create innovative products that meet evolving consumer demands. The rise of online grocery platforms and direct-to-consumer (DTC) models has created new distribution channels, allowing smaller players to gain market access. Private label brands are also gaining traction, offering consumers a more affordable alternative while maintaining good quality. The market penetration of semi-finished dishes is expected to reach xx% by 2033, showcasing its growing importance in the global food landscape.

Leading Markets & Segments in Semi-finished Dishes

The Online Sales segment is emerging as a dominant force in the global semi-finished dishes market, driven by the increasing adoption of e-commerce and the convenience it offers to consumers. With an estimated market size of xx billion in 2025, online platforms provide unparalleled accessibility, allowing consumers to browse, select, and order a wide variety of semi-finished dishes from the comfort of their homes. This channel is particularly popular among tech-savvy millennials and Gen Z consumers who prioritize convenience and instant gratification. The widespread availability of online grocery stores, dedicated meal kit delivery services, and the integration of semi-finished dish offerings by major e-commerce giants like Amazon and Alibaba have significantly boosted this segment's growth. Economic policies that support digital infrastructure development and e-commerce logistics further amplify online sales potential.

In terms of product types, Bagged semi-finished dishes are currently leading the market, accounting for an estimated xx billion in sales in 2025. This dominance is attributed to their cost-effectiveness, ease of storage, and suitability for a wide range of products, from vegetables and pasta dishes to curries and stir-fries. Bagged packaging often allows for portion control and can be designed for microwave or stovetop heating, further enhancing convenience for the end-user.

However, the Boxed segment, though currently smaller, is experiencing rapid growth, driven by premiumization and a focus on enhanced product presentation and ingredient integrity. Boxed packaging is often favored for more complex or delicate semi-finished dishes, such as lasagna, gratins, or gourmet meals, where presentation and the preservation of individual components are crucial. Retailers are increasingly leveraging attractive boxed packaging to showcase quality and appeal to consumers willing to pay a premium for a superior dining experience. The infrastructure supporting chilled and frozen logistics is crucial for both bagged and boxed segments, with investments in cold chain management playing a significant role in market expansion.

The Others category, which includes items like trays, pouches, and other innovative packaging formats, represents a significant area for future growth. As manufacturers explore new ways to enhance consumer experience and product shelf-life, the adoption of these diverse packaging solutions is expected to rise. The dominance of these segments is also influenced by regional economic policies that favor consumer spending on convenience foods, and robust retail infrastructure that facilitates efficient distribution.

Semi-finished Dishes Product Developments

Product innovation in the semi-finished dishes market is primarily focused on addressing the growing consumer demand for healthier, more diverse, and globally inspired meal options. Manufacturers are actively developing plant-based and vegetarian alternatives, catering to the rising flexitarian and vegan populations. Advances in sous-vide cooking technology and flash-freezing techniques are enabling the creation of semi-finished dishes that retain superior texture and flavor profiles, mimicking freshly prepared meals. Furthermore, there's a growing emphasis on clean label ingredients, with a reduction in artificial preservatives, colors, and flavors. Competitive advantages are being built around unique flavor combinations, convenient preparation methods (e.g., ready-to-heat pouches, microwave-safe containers), and extended shelf-life without compromising nutritional value or taste. The integration of dietary information and allergen transparency on packaging also enhances market appeal.

Key Drivers of Semi-finished Dishes Growth

The semi-finished dishes market is propelled by a synergistic interplay of several key drivers. Technological advancements in food processing, preservation, and packaging are continuously enhancing product quality, variety, and shelf-life. For instance, the adoption of advanced freezing techniques ensures minimal nutrient loss and optimal texture. Economic factors, such as rising disposable incomes and a growing middle class in emerging economies, are increasing consumer purchasing power and demand for convenient food solutions. Societal shifts, including busy lifestyles and a growing preference for home dining over eating out, further fuel the need for quick and easy meal preparation. Regulatory support for food safety standards and innovation in food technology also creates a favorable environment for market expansion. The growing awareness and demand for healthier food options are also pushing manufacturers to develop and promote nutritious semi-finished dishes.

Challenges in the Semi-finished Dishes Market

Despite the promising growth trajectory, the semi-finished dishes market faces several significant challenges. Stringent regulatory hurdles related to food safety, labeling, and ingredient sourcing can increase compliance costs and slow down product launches. Supply chain disruptions, exacerbated by global events, can impact the availability and cost of raw materials, leading to production delays and price volatility. Intense competitive pressures from both established brands and emerging players, as well as substitute products like fresh meal kits and restaurant delivery, necessitate continuous innovation and aggressive pricing strategies. Consumer perception regarding the healthiness and freshness of semi-finished dishes can also act as a restraint, requiring concerted marketing efforts to educate consumers and build trust. The logistical complexities of maintaining cold chains for frozen and chilled products across vast distribution networks also present an ongoing challenge.

Emerging Opportunities in Semi-finished Dishes

The semi-finished dishes market is ripe with emerging opportunities poised to drive long-term growth. Technological breakthroughs in areas like artificial intelligence for personalized meal recommendations, advanced preservation methods that further extend shelf-life while maintaining quality, and smart packaging with embedded sensors for real-time freshness monitoring, represent significant avenues for innovation. Strategic partnerships between food manufacturers, technology providers, and e-commerce platforms can unlock new distribution channels and enhance customer reach. The growing global demand for ethically sourced and sustainable food products presents an opportunity for companies to differentiate themselves by focusing on transparent sourcing and eco-friendly packaging. Furthermore, the expansion into under-served geographical markets with tailored product offerings and localized marketing strategies holds substantial untapped potential. The increasing demand for specialized dietary options, such as gluten-free, low-carb, and allergen-free semi-finished dishes, also offers a niche for focused product development.

Leading Players in the Semi-finished Dishes Sector

- PFI Foods

- JBS Foods

- Tyson Foods

- SYSCO

- Kobe Bussan

- Nichirei Corporation

- Anjoy Foods

- LongDa Foodstuff Group

- Springsnow Food Group

- Weizhixiang Food

- Zhanjiang Guolian Aquatic Products

- Huifa Foodstuff

- Haixin Foods

- Qianwei Central Kitchen Food

- Sanquan Food

- Fortune Ng Fung Food

- IMES

- Atenk

- Thai President Foods Plc

- UPG-INVEST LLC

- Primafonte Srl

- HSL Food

- HelloFresh

- Synear Food

- Haidilao

- Fresh Hema

Key Milestones in Semi-finished Dishes Industry

- 2019: Increased adoption of plant-based ingredients in semi-finished dishes, reflecting growing consumer interest.

- 2020: Surge in online sales of semi-finished dishes due to global pandemic-driven lockdowns and increased home cooking.

- 2021: Introduction of innovative packaging solutions aimed at enhancing convenience and sustainability in bagged and boxed offerings.

- 2022: Significant M&A activities as larger food corporations acquire niche players to expand their ready-meal portfolios.

- 2023: Growing emphasis on personalized nutrition and customization in semi-finished dishes, with some brands offering meal planning tools.

- 2024: Expansion of smart kitchen technologies integrating with semi-finished dish preparation, enhancing user experience.

Strategic Outlook for Semi-finished Dishes Market

The strategic outlook for the semi-finished dishes market is characterized by sustained innovation and aggressive market penetration. Growth accelerators will include the continued expansion of online sales channels, the development of premium and health-conscious product lines, and the exploration of emerging markets. Manufacturers will need to focus on building resilient supply chains, investing in advanced processing technologies, and leveraging data analytics to understand and cater to evolving consumer preferences. Strategic collaborations and mergers will likely continue to shape the competitive landscape, enabling companies to achieve economies of scale and broaden their market reach. The emphasis on sustainability and transparency in sourcing will become increasingly critical for brand loyalty and market differentiation. The market is poised for significant growth, driven by its ability to offer convenience without compromising on quality and variety.

Semi-finished Dishes Segmentation

-

1. Application

- 1.1. Online Sales

- 1.2. Offline Sales

-

2. Types

- 2.1. Bagged

- 2.2. Boxed

- 2.3. Others

Semi-finished Dishes Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Semi-finished Dishes Regional Market Share

Geographic Coverage of Semi-finished Dishes

Semi-finished Dishes REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.44% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Semi-finished Dishes Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Online Sales

- 5.1.2. Offline Sales

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Bagged

- 5.2.2. Boxed

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Semi-finished Dishes Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Online Sales

- 6.1.2. Offline Sales

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Bagged

- 6.2.2. Boxed

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Semi-finished Dishes Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Online Sales

- 7.1.2. Offline Sales

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Bagged

- 7.2.2. Boxed

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Semi-finished Dishes Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Online Sales

- 8.1.2. Offline Sales

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Bagged

- 8.2.2. Boxed

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Semi-finished Dishes Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Online Sales

- 9.1.2. Offline Sales

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Bagged

- 9.2.2. Boxed

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Semi-finished Dishes Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Online Sales

- 10.1.2. Offline Sales

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Bagged

- 10.2.2. Boxed

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 PFI Foods

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 JBS Foods

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Tyson Foods

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 SYSCO

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Kobe Bussan

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Nichirei Corporation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Anjoy Foods

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 LongDa Foodstuff Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Springsnow Food Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Weizhixiang Food

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Zhanjiang Guolian Aquatic Products

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Huifa Foodstuff

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Haixin Foods

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Qianwei Central Kitchen Food

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Sanquan Food

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Fortune Ng Fung Food

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 IMES

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Atenk

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Thai President Foods Plc

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 UPG-INVEST LLC

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Primafonte Srl

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 HSL Food

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 HelloFresh

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Synear Food

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Haidilao

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Fresh Hema

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.1 PFI Foods

List of Figures

- Figure 1: Global Semi-finished Dishes Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Semi-finished Dishes Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Semi-finished Dishes Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Semi-finished Dishes Volume (K), by Application 2025 & 2033

- Figure 5: North America Semi-finished Dishes Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Semi-finished Dishes Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Semi-finished Dishes Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Semi-finished Dishes Volume (K), by Types 2025 & 2033

- Figure 9: North America Semi-finished Dishes Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Semi-finished Dishes Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Semi-finished Dishes Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Semi-finished Dishes Volume (K), by Country 2025 & 2033

- Figure 13: North America Semi-finished Dishes Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Semi-finished Dishes Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Semi-finished Dishes Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Semi-finished Dishes Volume (K), by Application 2025 & 2033

- Figure 17: South America Semi-finished Dishes Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Semi-finished Dishes Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Semi-finished Dishes Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Semi-finished Dishes Volume (K), by Types 2025 & 2033

- Figure 21: South America Semi-finished Dishes Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Semi-finished Dishes Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Semi-finished Dishes Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Semi-finished Dishes Volume (K), by Country 2025 & 2033

- Figure 25: South America Semi-finished Dishes Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Semi-finished Dishes Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Semi-finished Dishes Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Semi-finished Dishes Volume (K), by Application 2025 & 2033

- Figure 29: Europe Semi-finished Dishes Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Semi-finished Dishes Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Semi-finished Dishes Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Semi-finished Dishes Volume (K), by Types 2025 & 2033

- Figure 33: Europe Semi-finished Dishes Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Semi-finished Dishes Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Semi-finished Dishes Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Semi-finished Dishes Volume (K), by Country 2025 & 2033

- Figure 37: Europe Semi-finished Dishes Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Semi-finished Dishes Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Semi-finished Dishes Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Semi-finished Dishes Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Semi-finished Dishes Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Semi-finished Dishes Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Semi-finished Dishes Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Semi-finished Dishes Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Semi-finished Dishes Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Semi-finished Dishes Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Semi-finished Dishes Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Semi-finished Dishes Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Semi-finished Dishes Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Semi-finished Dishes Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Semi-finished Dishes Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Semi-finished Dishes Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Semi-finished Dishes Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Semi-finished Dishes Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Semi-finished Dishes Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Semi-finished Dishes Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Semi-finished Dishes Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Semi-finished Dishes Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Semi-finished Dishes Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Semi-finished Dishes Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Semi-finished Dishes Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Semi-finished Dishes Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semi-finished Dishes Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Semi-finished Dishes Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Semi-finished Dishes Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Semi-finished Dishes Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Semi-finished Dishes Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Semi-finished Dishes Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Semi-finished Dishes Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Semi-finished Dishes Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Semi-finished Dishes Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Semi-finished Dishes Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Semi-finished Dishes Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Semi-finished Dishes Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Semi-finished Dishes Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Semi-finished Dishes Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Semi-finished Dishes Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Semi-finished Dishes Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Semi-finished Dishes Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Semi-finished Dishes Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Semi-finished Dishes Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Semi-finished Dishes Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Semi-finished Dishes Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Semi-finished Dishes Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Semi-finished Dishes Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Semi-finished Dishes Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Semi-finished Dishes Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Semi-finished Dishes Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Semi-finished Dishes Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Semi-finished Dishes Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Semi-finished Dishes Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Semi-finished Dishes Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Semi-finished Dishes Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Semi-finished Dishes Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Semi-finished Dishes Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Semi-finished Dishes Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Semi-finished Dishes Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Semi-finished Dishes Volume K Forecast, by Country 2020 & 2033

- Table 79: China Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Semi-finished Dishes Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Semi-finished Dishes Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semi-finished Dishes?

The projected CAGR is approximately 14.44%.

2. Which companies are prominent players in the Semi-finished Dishes?

Key companies in the market include PFI Foods, JBS Foods, Tyson Foods, SYSCO, Kobe Bussan, Nichirei Corporation, Anjoy Foods, LongDa Foodstuff Group, Springsnow Food Group, Weizhixiang Food, Zhanjiang Guolian Aquatic Products, Huifa Foodstuff, Haixin Foods, Qianwei Central Kitchen Food, Sanquan Food, Fortune Ng Fung Food, IMES, Atenk, Thai President Foods Plc, UPG-INVEST LLC, Primafonte Srl, HSL Food, HelloFresh, Synear Food, Haidilao, Fresh Hema.

3. What are the main segments of the Semi-finished Dishes?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.17 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semi-finished Dishes," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semi-finished Dishes report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semi-finished Dishes?

To stay informed about further developments, trends, and reports in the Semi-finished Dishes, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence