Key Insights

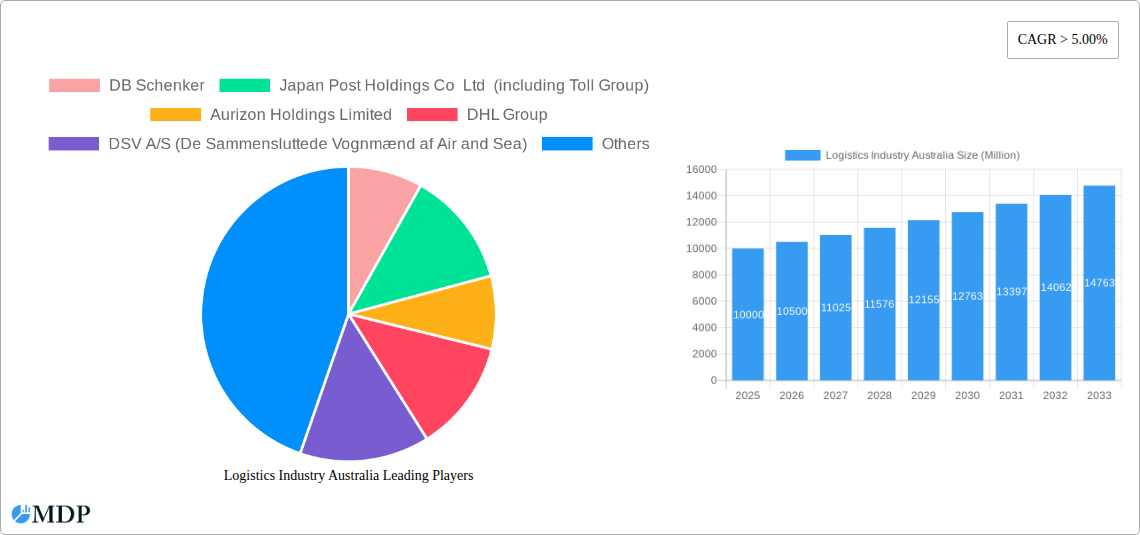

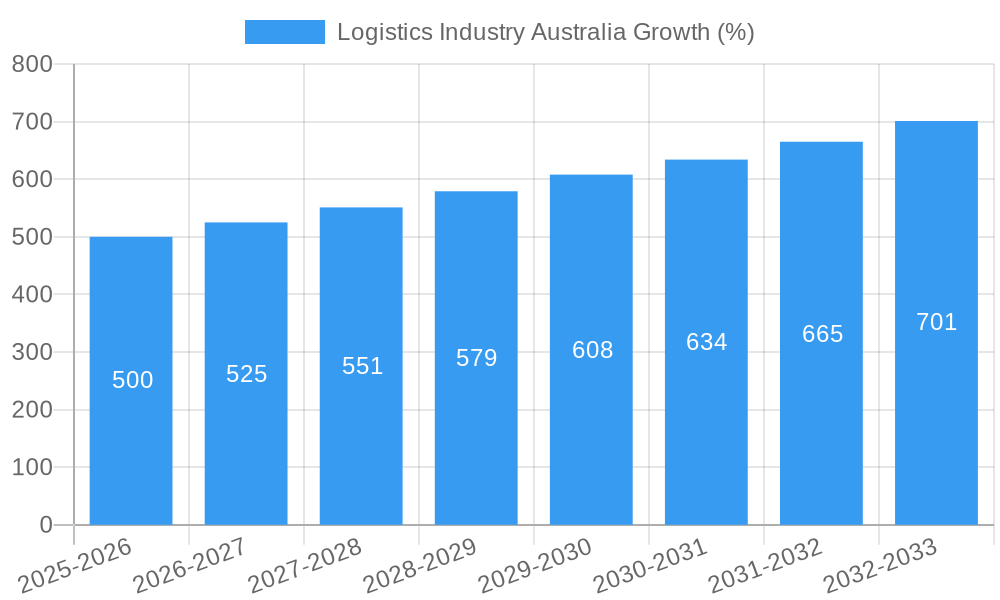

The Australian logistics industry, valued at approximately $XX million in 2025, is experiencing robust growth, exceeding a 5% compound annual growth rate (CAGR) between 2019 and 2033. This expansion is fueled by several key factors. Firstly, Australia's robust agricultural sector, coupled with burgeoning mining and construction activities, necessitates efficient and reliable logistics solutions for transporting raw materials and finished goods. Secondly, the growth of e-commerce is driving significant demand for express parcel delivery and temperature-controlled transportation. The increasing complexity of supply chains also necessitates specialized logistics services, including those catering to the oil and gas, and manufacturing sectors. Finally, government infrastructure investments, including improved road and rail networks, are improving connectivity and facilitating more efficient logistics operations. While factors such as fluctuating fuel prices and workforce shortages pose challenges, technological advancements, including automation and data analytics, offer opportunities for increased efficiency and cost optimization within the sector. The market is segmented by end-user industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, Others) and logistics function (Courier, Express, and Parcel (CEP), Temperature Controlled, Other Services), with significant growth expected across various segments. Major players such as DB Schenker, DHL, FedEx, and Toll Group are fiercely competing for market share, driving innovation and service improvements.

The forecast period (2025-2033) anticipates sustained market growth, primarily driven by the aforementioned factors. The Australian economy's continued expansion and increasing reliance on international trade will further stimulate demand for logistics services. While potential economic downturns or disruptions to global supply chains could pose risks, the long-term outlook remains positive for the Australian logistics sector. The industry’s adaptation to technological innovations and the ongoing focus on sustainability are expected to play significant roles in shaping the industry's trajectory in the coming years. The competitive landscape will continue to evolve, with consolidation and strategic partnerships potentially altering market dynamics.

Logistics Industry Australia: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Australian logistics industry, encompassing market dynamics, leading players, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry stakeholders, investors, and strategic decision-makers. The report leverages extensive data analysis to project a market size exceeding XX Million by 2033, driven by key trends and opportunities detailed within.

Logistics Industry Australia Market Dynamics & Concentration

The Australian logistics market, valued at approximately XX Million in 2024, is characterized by a moderately concentrated landscape dominated by a few major players. Market share is distributed amongst both global giants and established domestic firms. While exact figures are proprietary, DB Schenker, DHL Group, FedEx, and Kuehne + Nagel hold significant shares. The market’s competitive intensity is high, influenced by price competition, service differentiation, and technological advancements.

Innovation Drivers: Automation, data analytics, and sustainable practices are key innovation drivers. The adoption of autonomous vehicles, blockchain technology for enhanced supply chain transparency, and investments in green logistics solutions are reshaping the industry.

Regulatory Framework: Government regulations concerning safety, environmental sustainability, and fair competition directly impact market operations. Recent legislative changes focusing on carbon emission reduction are compelling businesses to adopt greener practices.

Product Substitutes: The availability of alternative transportation modes and logistics service providers exerts competitive pressure. The rise of e-commerce has also spurred the need for flexible and agile logistics solutions.

End-User Trends: The growth of e-commerce and the increasing demand for faster delivery times have significantly impacted the market. Specific end-user industries like manufacturing and wholesale & retail trade are major drivers of logistics demand.

M&A Activities: Consolidation through mergers and acquisitions has been a prominent feature in recent years. The number of M&A deals involving Australian logistics companies averaged approximately xx per year during the historical period (2019-2024), with a projected increase in the forecast period. These activities reflect the pursuit of scale, market share expansion, and diversification.

Logistics Industry Australia Industry Trends & Analysis

The Australian logistics industry exhibits robust growth potential, projected at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is underpinned by several significant factors:

- E-commerce Boom: The continued expansion of online retail fuels demand for efficient last-mile delivery and sophisticated supply chain management.

- Infrastructure Development: Government investments in transport infrastructure, such as port upgrades and road improvements, improve logistics efficiency and reduce costs.

- Technological Advancements: The adoption of advanced technologies like AI, IoT, and big data analytics optimizes operations, enhances visibility, and improves decision-making.

- Rising Demand for Specialized Services: The increasing need for temperature-controlled logistics and specialized handling solutions for various industries (e.g., pharmaceuticals, perishables) drives market segmentation.

- Focus on Sustainability: The growing emphasis on environmental responsibility is pushing logistics companies to adopt sustainable practices, including the use of electric vehicles and carbon-neutral solutions. Market penetration of these solutions is currently at approximately xx% but is projected to grow significantly.

The competitive landscape is characterized by intense rivalry, with companies focusing on service differentiation, technological innovation, and strategic partnerships to gain a competitive edge. Market penetration for key technologies like AI and blockchain varies, but adoption is progressively accelerating.

Leading Markets & Segments in Logistics Industry Australia

Dominant Segments:

- End-User Industry: Wholesale and Retail Trade and Manufacturing represent the largest segments, driven by the robust growth of e-commerce and domestic production. Mining and Quarrying also contributes significantly due to its reliance on efficient material transportation.

- Logistics Function: Courier, Express, and Parcel (CEP) services dominate the market, followed by temperature-controlled logistics, which is experiencing significant growth driven by the food and pharmaceutical industries. Other specialized services are also gaining traction.

Key Drivers:

- Economic Policies: Government initiatives promoting trade and infrastructure development are instrumental in driving market growth.

- Infrastructure: Investments in road, rail, and port infrastructure are vital in improving connectivity and efficiency.

- Technological advancements: Automation and digitization enhance efficiency and reduce costs.

- Consumer preferences: Growing demand for fast and reliable delivery services.

The dominance of Wholesale & Retail Trade and Manufacturing stems from their considerable reliance on efficient logistics solutions to manage their supply chains and meet customer demands.

Logistics Industry Australia Product Developments

Recent product innovations include the integration of advanced technologies such as AI, blockchain, and IoT into logistics operations. These technologies enhance visibility, improve efficiency, and optimize resource allocation. The focus on sustainable logistics has led to the development of electric vehicles and carbon-neutral transportation solutions, providing a competitive advantage by catering to environmentally conscious clients. The market fit for these innovations is strong, as companies increasingly prioritize sustainability and operational efficiency.

Key Drivers of Logistics Industry Australia Growth

The Australian logistics industry’s growth is propelled by several interconnected factors:

- Technological advancements: Automation, AI, and data analytics are streamlining operations and enhancing efficiency.

- E-commerce expansion: The surge in online shopping fuels demand for reliable and fast delivery services.

- Government investments: Infrastructure upgrades and supportive economic policies contribute to market expansion. Examples include recent investments in port infrastructure and national road networks.

Challenges in the Logistics Industry Australia Market

The industry faces significant challenges, including:

- Driver shortages: A persistent lack of skilled drivers impacts delivery efficiency and costs. This shortage currently affects approximately xx% of logistics companies.

- Rising fuel costs: Fluctuations in fuel prices directly influence operating expenses and profitability.

- Infrastructure limitations: Congestion in major cities and inadequate infrastructure in some regions create bottlenecks and delays.

- Increased competition: Intense rivalry among established players and new entrants necessitates ongoing innovation and cost optimization.

Emerging Opportunities in Logistics Industry Australia

The industry presents significant long-term growth opportunities:

- Last-mile delivery optimization: Innovations in drone delivery and autonomous vehicles offer potential efficiency gains.

- Supply chain digitization: Blockchain technology can enhance transparency and traceability throughout the supply chain.

- Sustainable logistics solutions: Growing demand for green logistics services presents opportunities for environmentally friendly solutions.

- Strategic partnerships: Collaboration between logistics providers and technology companies can drive innovation and improve service offerings.

Leading Players in the Logistics Industry Australia Sector

- DB Schenker

- Japan Post Holdings Co Ltd (including Toll Group)

- Aurizon Holdings Limited

- DHL Group

- DSV A/S (De Sammensluttede Vognmænd af Air and Sea)

- FedEx

- Qube Holdings Ltd

- LINX Cargo Care Group

- Kuehne + Nagel

- Linfox Pty Ltd

- K&S Corporation Limited

- Toll Grou

- Centurion Transport

Key Milestones in Logistics Industry Australia Industry

- January 2024: DHL Express expands its inter-continental connectivity with the deployment of a final Boeing 777 freighter in Singapore, significantly boosting payload capacity.

- January 2024: Kuehne + Nagel launches its Book & Claim insetting solution for electric vehicles, enhancing its decarbonization offerings and providing customers with carbon reduction claims.

- February 2024: DHL Supply Chain continues its fleet decarbonization efforts by adding electric yard tractors and light-duty trucks, supporting Australian electric vehicle manufacturing.

Strategic Outlook for Logistics Industry Australia Market

The Australian logistics market exhibits strong growth potential driven by e-commerce expansion, infrastructure improvements, and technological advancements. Strategic partnerships, investment in sustainable practices, and adoption of innovative technologies will be key to success. The focus on optimizing last-mile delivery and enhancing supply chain visibility will be pivotal in shaping future market dynamics and driving long-term profitability. The market’s continued evolution necessitates adaptability, innovation, and a commitment to sustainable practices to capitalize on emerging opportunities.

Logistics Industry Australia Segmentation

-

1. End User Industry

- 1.1. Agriculture, Fishing, and Forestry

- 1.2. Construction

- 1.3. Manufacturing

- 1.4. Oil and Gas, Mining and Quarrying

- 1.5. Wholesale and Retail Trade

- 1.6. Others

-

2. Logistics Function

-

2.1. Courier, Express, and Parcel (CEP)

-

2.1.1. By Destination Type

- 2.1.1.1. Domestic

- 2.1.1.2. International

-

2.1.1. By Destination Type

-

2.2. Freight Forwarding

-

2.2.1. By Mode Of Transport

- 2.2.1.1. Air

- 2.2.1.2. Sea and Inland Waterways

- 2.2.1.3. Others

-

2.2.1. By Mode Of Transport

-

2.3. Freight Transport

- 2.3.1. Pipelines

- 2.3.2. Rail

- 2.3.3. Road

-

2.4. Warehousing and Storage

-

2.4.1. By Temperature Control

- 2.4.1.1. Non-Temperature Controlled

-

2.4.1. By Temperature Control

- 2.5. Other Services

-

2.1. Courier, Express, and Parcel (CEP)

Logistics Industry Australia Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Logistics Industry Australia REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 5.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increase demand of Petrochemical is driving the market4.; Increase in Investments is driving the market

- 3.3. Market Restrains

- 3.3.1. 4.; High Cost of Operations

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Logistics Industry Australia Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 5.1.1. Agriculture, Fishing, and Forestry

- 5.1.2. Construction

- 5.1.3. Manufacturing

- 5.1.4. Oil and Gas, Mining and Quarrying

- 5.1.5. Wholesale and Retail Trade

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Logistics Function

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.2.1.1. By Destination Type

- 5.2.1.1.1. Domestic

- 5.2.1.1.2. International

- 5.2.1.1. By Destination Type

- 5.2.2. Freight Forwarding

- 5.2.2.1. By Mode Of Transport

- 5.2.2.1.1. Air

- 5.2.2.1.2. Sea and Inland Waterways

- 5.2.2.1.3. Others

- 5.2.2.1. By Mode Of Transport

- 5.2.3. Freight Transport

- 5.2.3.1. Pipelines

- 5.2.3.2. Rail

- 5.2.3.3. Road

- 5.2.4. Warehousing and Storage

- 5.2.4.1. By Temperature Control

- 5.2.4.1.1. Non-Temperature Controlled

- 5.2.4.1. By Temperature Control

- 5.2.5. Other Services

- 5.2.1. Courier, Express, and Parcel (CEP)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by End User Industry

- 6. North America Logistics Industry Australia Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 6.1.1. Agriculture, Fishing, and Forestry

- 6.1.2. Construction

- 6.1.3. Manufacturing

- 6.1.4. Oil and Gas, Mining and Quarrying

- 6.1.5. Wholesale and Retail Trade

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Logistics Function

- 6.2.1. Courier, Express, and Parcel (CEP)

- 6.2.1.1. By Destination Type

- 6.2.1.1.1. Domestic

- 6.2.1.1.2. International

- 6.2.1.1. By Destination Type

- 6.2.2. Freight Forwarding

- 6.2.2.1. By Mode Of Transport

- 6.2.2.1.1. Air

- 6.2.2.1.2. Sea and Inland Waterways

- 6.2.2.1.3. Others

- 6.2.2.1. By Mode Of Transport

- 6.2.3. Freight Transport

- 6.2.3.1. Pipelines

- 6.2.3.2. Rail

- 6.2.3.3. Road

- 6.2.4. Warehousing and Storage

- 6.2.4.1. By Temperature Control

- 6.2.4.1.1. Non-Temperature Controlled

- 6.2.4.1. By Temperature Control

- 6.2.5. Other Services

- 6.2.1. Courier, Express, and Parcel (CEP)

- 6.1. Market Analysis, Insights and Forecast - by End User Industry

- 7. South America Logistics Industry Australia Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by End User Industry

- 7.1.1. Agriculture, Fishing, and Forestry

- 7.1.2. Construction

- 7.1.3. Manufacturing

- 7.1.4. Oil and Gas, Mining and Quarrying

- 7.1.5. Wholesale and Retail Trade

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Logistics Function

- 7.2.1. Courier, Express, and Parcel (CEP)

- 7.2.1.1. By Destination Type

- 7.2.1.1.1. Domestic

- 7.2.1.1.2. International

- 7.2.1.1. By Destination Type

- 7.2.2. Freight Forwarding

- 7.2.2.1. By Mode Of Transport

- 7.2.2.1.1. Air

- 7.2.2.1.2. Sea and Inland Waterways

- 7.2.2.1.3. Others

- 7.2.2.1. By Mode Of Transport

- 7.2.3. Freight Transport

- 7.2.3.1. Pipelines

- 7.2.3.2. Rail

- 7.2.3.3. Road

- 7.2.4. Warehousing and Storage

- 7.2.4.1. By Temperature Control

- 7.2.4.1.1. Non-Temperature Controlled

- 7.2.4.1. By Temperature Control

- 7.2.5. Other Services

- 7.2.1. Courier, Express, and Parcel (CEP)

- 7.1. Market Analysis, Insights and Forecast - by End User Industry

- 8. Europe Logistics Industry Australia Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by End User Industry

- 8.1.1. Agriculture, Fishing, and Forestry

- 8.1.2. Construction

- 8.1.3. Manufacturing

- 8.1.4. Oil and Gas, Mining and Quarrying

- 8.1.5. Wholesale and Retail Trade

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Logistics Function

- 8.2.1. Courier, Express, and Parcel (CEP)

- 8.2.1.1. By Destination Type

- 8.2.1.1.1. Domestic

- 8.2.1.1.2. International

- 8.2.1.1. By Destination Type

- 8.2.2. Freight Forwarding

- 8.2.2.1. By Mode Of Transport

- 8.2.2.1.1. Air

- 8.2.2.1.2. Sea and Inland Waterways

- 8.2.2.1.3. Others

- 8.2.2.1. By Mode Of Transport

- 8.2.3. Freight Transport

- 8.2.3.1. Pipelines

- 8.2.3.2. Rail

- 8.2.3.3. Road

- 8.2.4. Warehousing and Storage

- 8.2.4.1. By Temperature Control

- 8.2.4.1.1. Non-Temperature Controlled

- 8.2.4.1. By Temperature Control

- 8.2.5. Other Services

- 8.2.1. Courier, Express, and Parcel (CEP)

- 8.1. Market Analysis, Insights and Forecast - by End User Industry

- 9. Middle East & Africa Logistics Industry Australia Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by End User Industry

- 9.1.1. Agriculture, Fishing, and Forestry

- 9.1.2. Construction

- 9.1.3. Manufacturing

- 9.1.4. Oil and Gas, Mining and Quarrying

- 9.1.5. Wholesale and Retail Trade

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Logistics Function

- 9.2.1. Courier, Express, and Parcel (CEP)

- 9.2.1.1. By Destination Type

- 9.2.1.1.1. Domestic

- 9.2.1.1.2. International

- 9.2.1.1. By Destination Type

- 9.2.2. Freight Forwarding

- 9.2.2.1. By Mode Of Transport

- 9.2.2.1.1. Air

- 9.2.2.1.2. Sea and Inland Waterways

- 9.2.2.1.3. Others

- 9.2.2.1. By Mode Of Transport

- 9.2.3. Freight Transport

- 9.2.3.1. Pipelines

- 9.2.3.2. Rail

- 9.2.3.3. Road

- 9.2.4. Warehousing and Storage

- 9.2.4.1. By Temperature Control

- 9.2.4.1.1. Non-Temperature Controlled

- 9.2.4.1. By Temperature Control

- 9.2.5. Other Services

- 9.2.1. Courier, Express, and Parcel (CEP)

- 9.1. Market Analysis, Insights and Forecast - by End User Industry

- 10. Asia Pacific Logistics Industry Australia Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by End User Industry

- 10.1.1. Agriculture, Fishing, and Forestry

- 10.1.2. Construction

- 10.1.3. Manufacturing

- 10.1.4. Oil and Gas, Mining and Quarrying

- 10.1.5. Wholesale and Retail Trade

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Logistics Function

- 10.2.1. Courier, Express, and Parcel (CEP)

- 10.2.1.1. By Destination Type

- 10.2.1.1.1. Domestic

- 10.2.1.1.2. International

- 10.2.1.1. By Destination Type

- 10.2.2. Freight Forwarding

- 10.2.2.1. By Mode Of Transport

- 10.2.2.1.1. Air

- 10.2.2.1.2. Sea and Inland Waterways

- 10.2.2.1.3. Others

- 10.2.2.1. By Mode Of Transport

- 10.2.3. Freight Transport

- 10.2.3.1. Pipelines

- 10.2.3.2. Rail

- 10.2.3.3. Road

- 10.2.4. Warehousing and Storage

- 10.2.4.1. By Temperature Control

- 10.2.4.1.1. Non-Temperature Controlled

- 10.2.4.1. By Temperature Control

- 10.2.5. Other Services

- 10.2.1. Courier, Express, and Parcel (CEP)

- 10.1. Market Analysis, Insights and Forecast - by End User Industry

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 DB Schenker

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Japan Post Holdings Co Ltd (including Toll Group)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Aurizon Holdings Limited

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 DHL Group

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 DSV A/S (De Sammensluttede Vognmænd af Air and Sea)

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 FedEx

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Qube Holdings Ltd

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 LINX Cargo Care Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Kuehne + Nagel

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Linfox Pty Ltd

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 K&S Corporation Limited

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Toll Grou

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Centurion Transport

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 DB Schenker

List of Figures

- Figure 1: Global Logistics Industry Australia Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: Australia Logistics Industry Australia Revenue (Million), by Country 2024 & 2032

- Figure 3: Australia Logistics Industry Australia Revenue Share (%), by Country 2024 & 2032

- Figure 4: North America Logistics Industry Australia Revenue (Million), by End User Industry 2024 & 2032

- Figure 5: North America Logistics Industry Australia Revenue Share (%), by End User Industry 2024 & 2032

- Figure 6: North America Logistics Industry Australia Revenue (Million), by Logistics Function 2024 & 2032

- Figure 7: North America Logistics Industry Australia Revenue Share (%), by Logistics Function 2024 & 2032

- Figure 8: North America Logistics Industry Australia Revenue (Million), by Country 2024 & 2032

- Figure 9: North America Logistics Industry Australia Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Logistics Industry Australia Revenue (Million), by End User Industry 2024 & 2032

- Figure 11: South America Logistics Industry Australia Revenue Share (%), by End User Industry 2024 & 2032

- Figure 12: South America Logistics Industry Australia Revenue (Million), by Logistics Function 2024 & 2032

- Figure 13: South America Logistics Industry Australia Revenue Share (%), by Logistics Function 2024 & 2032

- Figure 14: South America Logistics Industry Australia Revenue (Million), by Country 2024 & 2032

- Figure 15: South America Logistics Industry Australia Revenue Share (%), by Country 2024 & 2032

- Figure 16: Europe Logistics Industry Australia Revenue (Million), by End User Industry 2024 & 2032

- Figure 17: Europe Logistics Industry Australia Revenue Share (%), by End User Industry 2024 & 2032

- Figure 18: Europe Logistics Industry Australia Revenue (Million), by Logistics Function 2024 & 2032

- Figure 19: Europe Logistics Industry Australia Revenue Share (%), by Logistics Function 2024 & 2032

- Figure 20: Europe Logistics Industry Australia Revenue (Million), by Country 2024 & 2032

- Figure 21: Europe Logistics Industry Australia Revenue Share (%), by Country 2024 & 2032

- Figure 22: Middle East & Africa Logistics Industry Australia Revenue (Million), by End User Industry 2024 & 2032

- Figure 23: Middle East & Africa Logistics Industry Australia Revenue Share (%), by End User Industry 2024 & 2032

- Figure 24: Middle East & Africa Logistics Industry Australia Revenue (Million), by Logistics Function 2024 & 2032

- Figure 25: Middle East & Africa Logistics Industry Australia Revenue Share (%), by Logistics Function 2024 & 2032

- Figure 26: Middle East & Africa Logistics Industry Australia Revenue (Million), by Country 2024 & 2032

- Figure 27: Middle East & Africa Logistics Industry Australia Revenue Share (%), by Country 2024 & 2032

- Figure 28: Asia Pacific Logistics Industry Australia Revenue (Million), by End User Industry 2024 & 2032

- Figure 29: Asia Pacific Logistics Industry Australia Revenue Share (%), by End User Industry 2024 & 2032

- Figure 30: Asia Pacific Logistics Industry Australia Revenue (Million), by Logistics Function 2024 & 2032

- Figure 31: Asia Pacific Logistics Industry Australia Revenue Share (%), by Logistics Function 2024 & 2032

- Figure 32: Asia Pacific Logistics Industry Australia Revenue (Million), by Country 2024 & 2032

- Figure 33: Asia Pacific Logistics Industry Australia Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Logistics Industry Australia Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Logistics Industry Australia Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 3: Global Logistics Industry Australia Revenue Million Forecast, by Logistics Function 2019 & 2032

- Table 4: Global Logistics Industry Australia Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Logistics Industry Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Global Logistics Industry Australia Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 7: Global Logistics Industry Australia Revenue Million Forecast, by Logistics Function 2019 & 2032

- Table 8: Global Logistics Industry Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 9: United States Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Canada Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Mexico Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global Logistics Industry Australia Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 13: Global Logistics Industry Australia Revenue Million Forecast, by Logistics Function 2019 & 2032

- Table 14: Global Logistics Industry Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 15: Brazil Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Argentina Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Rest of South America Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Global Logistics Industry Australia Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 19: Global Logistics Industry Australia Revenue Million Forecast, by Logistics Function 2019 & 2032

- Table 20: Global Logistics Industry Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 21: United Kingdom Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Germany Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: France Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Italy Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Spain Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Russia Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Benelux Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Nordics Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Rest of Europe Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Global Logistics Industry Australia Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 31: Global Logistics Industry Australia Revenue Million Forecast, by Logistics Function 2019 & 2032

- Table 32: Global Logistics Industry Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 33: Turkey Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Israel Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: GCC Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: North Africa Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: South Africa Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Rest of Middle East & Africa Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Global Logistics Industry Australia Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 40: Global Logistics Industry Australia Revenue Million Forecast, by Logistics Function 2019 & 2032

- Table 41: Global Logistics Industry Australia Revenue Million Forecast, by Country 2019 & 2032

- Table 42: China Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: India Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Japan Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: South Korea Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: ASEAN Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Oceania Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Rest of Asia Pacific Logistics Industry Australia Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Logistics Industry Australia?

The projected CAGR is approximately > 5.00%.

2. Which companies are prominent players in the Logistics Industry Australia?

Key companies in the market include DB Schenker, Japan Post Holdings Co Ltd (including Toll Group), Aurizon Holdings Limited, DHL Group, DSV A/S (De Sammensluttede Vognmænd af Air and Sea), FedEx, Qube Holdings Ltd, LINX Cargo Care Group, Kuehne + Nagel, Linfox Pty Ltd, K&S Corporation Limited, Toll Grou, Centurion Transport.

3. What are the main segments of the Logistics Industry Australia?

The market segments include End User Industry, Logistics Function.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increase demand of Petrochemical is driving the market4.; Increase in Investments is driving the market.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

4.; High Cost of Operations.

8. Can you provide examples of recent developments in the market?

February 2024: DHL Supply Chain (DHL) is continuing the decarbonization of its Australian transport fleet by introducing additional new electric vehicles. The company has added two Terberg YT200EV electric yard tractors to its truck fleet and is supporting Australian electric vehicle manufacturing with the introduction of its first SEA Electric light duty truck to its last-mile fleet.January 2024: DHL Express has commenced services for the final Boeing 777 freighter deployed at the South Asia Hub in Singapore. With a payload capability of 102 tons, the aircraft joins the four other Boeing 777 freighters already deployed in Singapore to boost inter-continental connectivity between the Asia Pacific and the Americas. Sporting a dual DHL-Singapore Airlines (SIA) livery, these five freighters provide a total of 1,224 tons of payload capacity to meet growing customer demand for international express shipping services.January 2024: Kuehne + Nagel has announced its Book & Claim insetting solution for electric vehicles, to improve its decarbonization solutions. Developing Book & Claim insetting solutions for road freight was a strategic priority for Kuehne + Nagel. Customers who use Kuehne + Nagel's road transport services can now claim the carbon reductions of electric trucks when it is not possible to physically move their goods on these vehicles.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Logistics Industry Australia," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Logistics Industry Australia report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Logistics Industry Australia?

To stay informed about further developments, trends, and reports in the Logistics Industry Australia, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence