Key Insights

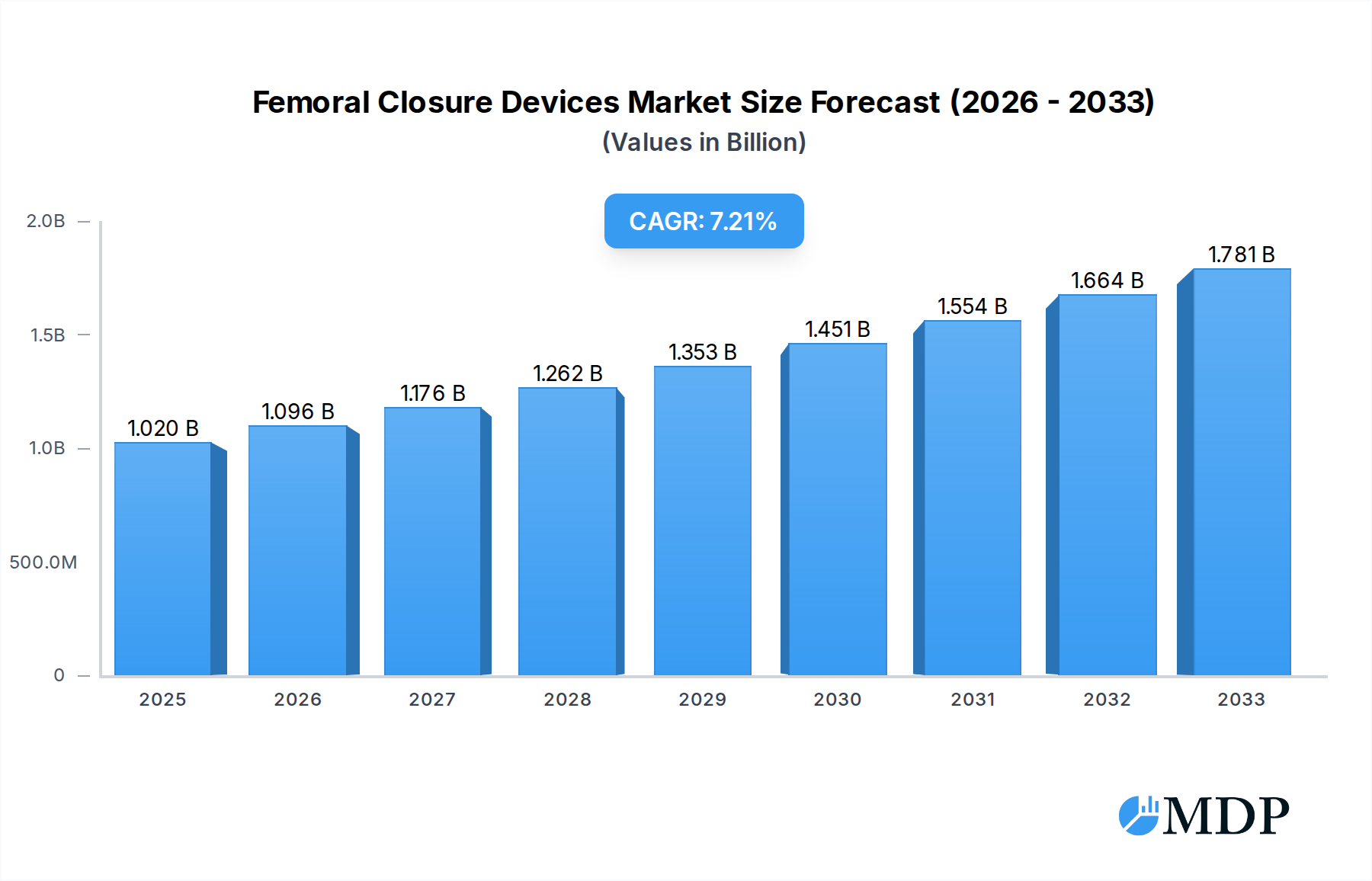

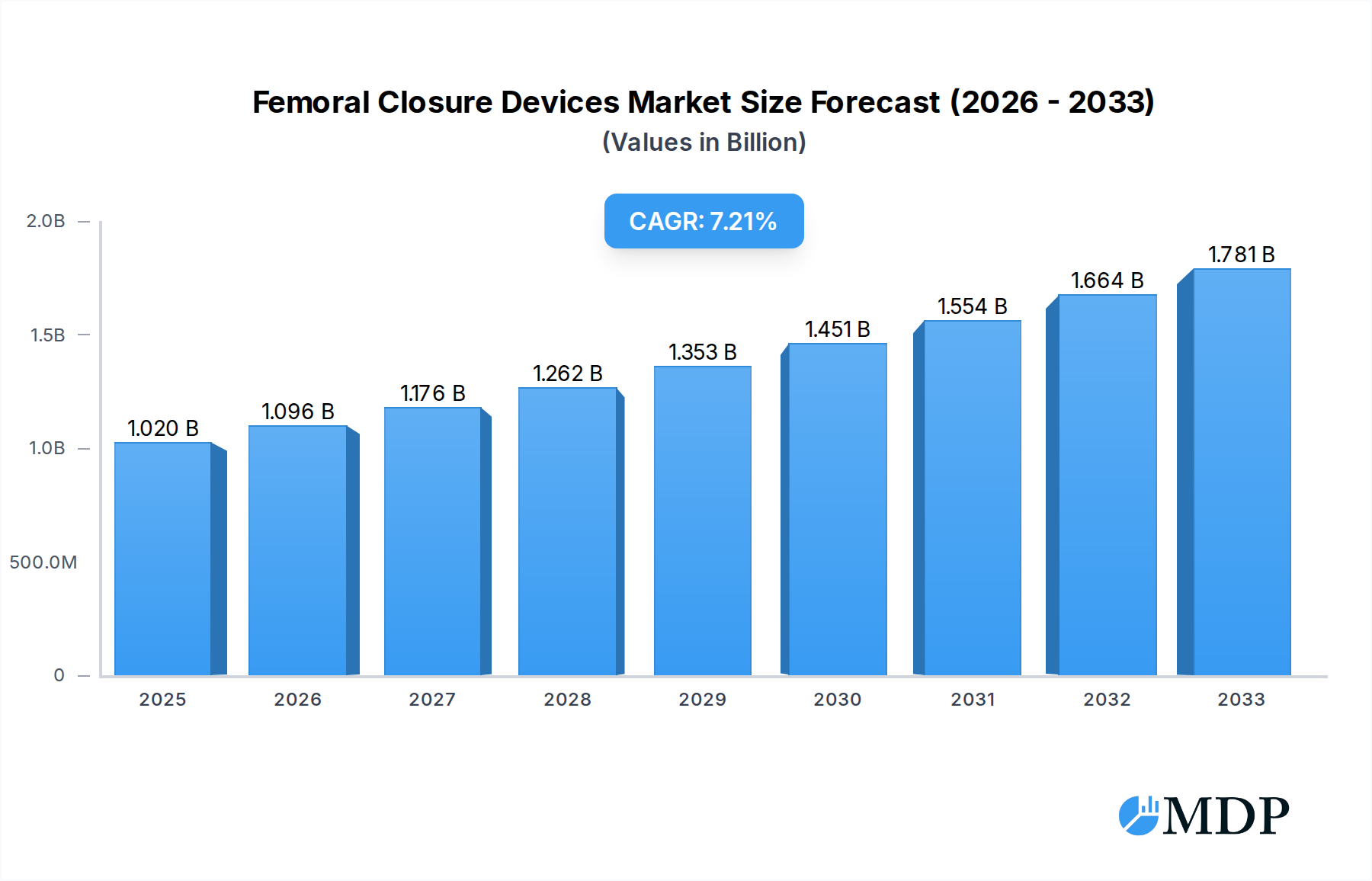

The global Femoral Closure Devices market is poised for significant expansion, projected to reach $1.02 billion in 2025 and grow at a robust CAGR of 7.3% through 2033. This growth is primarily fueled by the increasing prevalence of cardiovascular diseases, necessitating a higher volume of minimally invasive interventional procedures like angiography. The demand for efficient and safe closure of the femoral artery post-access is paramount, driving innovation in both passive and active closure device technologies. Passive closure devices, offering simplicity and cost-effectiveness, will continue to hold a substantial share. However, the market is witnessing a notable shift towards active closure devices due to their enhanced control, reduced complication rates, and faster patient ambulation capabilities. Technological advancements, coupled with a growing focus on patient outcomes and shorter hospital stays, are key enablers for this market's upward trajectory.

Femoral Closure Devices Market Size (In Billion)

The market's expansion is further propelled by an aging global population, which inherently contributes to a higher incidence of vascular conditions requiring intervention. Furthermore, the continuous development of new devices with improved hemostatic efficacy and user-friendliness by leading companies such as Abbott Laboratories, Terumo, and Cardiva is shaping the competitive landscape. While the market benefits from strong drivers, potential restraints such as stringent regulatory approvals and the high cost of advanced active closure devices could temper the pace of growth in certain segments. Nonetheless, the expanding healthcare infrastructure in emerging economies and the increasing adoption of percutaneous techniques across various interventional specialties are expected to offset these challenges, ensuring a dynamic and expanding Femoral Closure Devices market.

Femoral Closure Devices Company Market Share

Unlocking the Future of Vascular Access: Comprehensive Femoral Closure Devices Market Report 2019-2033

This in-depth report provides a critical analysis of the global Femoral Closure Devices Market, a vital segment within the interventional cardiology and vascular surgery landscape. Spanning the Study Period: 2019–2033, with a Base Year: 2025 and Forecast Period: 2025–2033, this comprehensive research offers unparalleled insights for industry stakeholders, including manufacturers, investors, researchers, and healthcare professionals. Our analysis is meticulously crafted to provide actionable intelligence, focusing on market dynamics, technological advancements, regulatory landscapes, and competitive strategies. Dive deep into market penetration, CAGR, and CAGR-driven growth projections, with all monetary values presented in billions. This report is designed for immediate use, requiring no further modifications.

Femoral Closure Devices Market Dynamics & Concentration

The Femoral Closure Devices Market exhibits a moderate to high concentration, with key players dominating significant market share. In 2025, the top five companies are estimated to hold over $3 billion in cumulative market share. Innovation drivers are primarily fueled by the demand for minimally invasive procedures, enhanced patient safety, and reduced complications. Regulatory frameworks, overseen by bodies like the FDA and EMA, are increasingly stringent, pushing for robust clinical evidence and product efficacy. Product substitutes, such as manual compression and suture-based closures, exist but are gradually being overshadowed by the efficiency and superiority of dedicated closure devices. End-user trends indicate a strong preference for devices offering faster ambulation times and reduced vascular access site issues, particularly in Interventional Procedures and Angiography Surgery. Merger and acquisition (M&A) activities are expected to remain a strategic tool for market expansion and consolidation, with an estimated XX M&A deals anticipated between 2025 and 2033, valued at over $500 million.

Femoral Closure Devices Industry Trends & Analysis

The global Femoral Closure Devices Market is poised for robust growth, projected to expand at a compound annual growth rate (CAGR) of approximately 7.5% from 2025 to 2033. This significant growth is propelled by several interconnected trends. The escalating prevalence of cardiovascular diseases, including peripheral artery disease and coronary artery disease, directly fuels the demand for interventional procedures like angioplasty and stenting, which inherently require reliable femoral artery access and subsequent closure. Technological disruptions are a constant force, with manufacturers continuously investing in research and development to create devices offering improved hemostasis, reduced complication rates, and enhanced ease of use for clinicians. The shift towards minimally invasive surgery remains a paramount trend, directly benefiting the adoption of femoral closure devices over traditional, more invasive closure methods. Consumer preferences are increasingly aligned with faster patient recovery and shorter hospital stays, making advanced closure techniques highly desirable. Competitive dynamics are characterized by fierce innovation, with companies vying for market leadership through product differentiation, strategic partnerships, and aggressive marketing campaigns. Market penetration is expected to reach over 80% for suitable procedures by 2033, driven by increasing awareness and reimbursement policies that favor advanced closure technologies. The estimated market size in 2025 is projected to be over $2.5 billion.

Leading Markets & Segments in Femoral Closure Devices

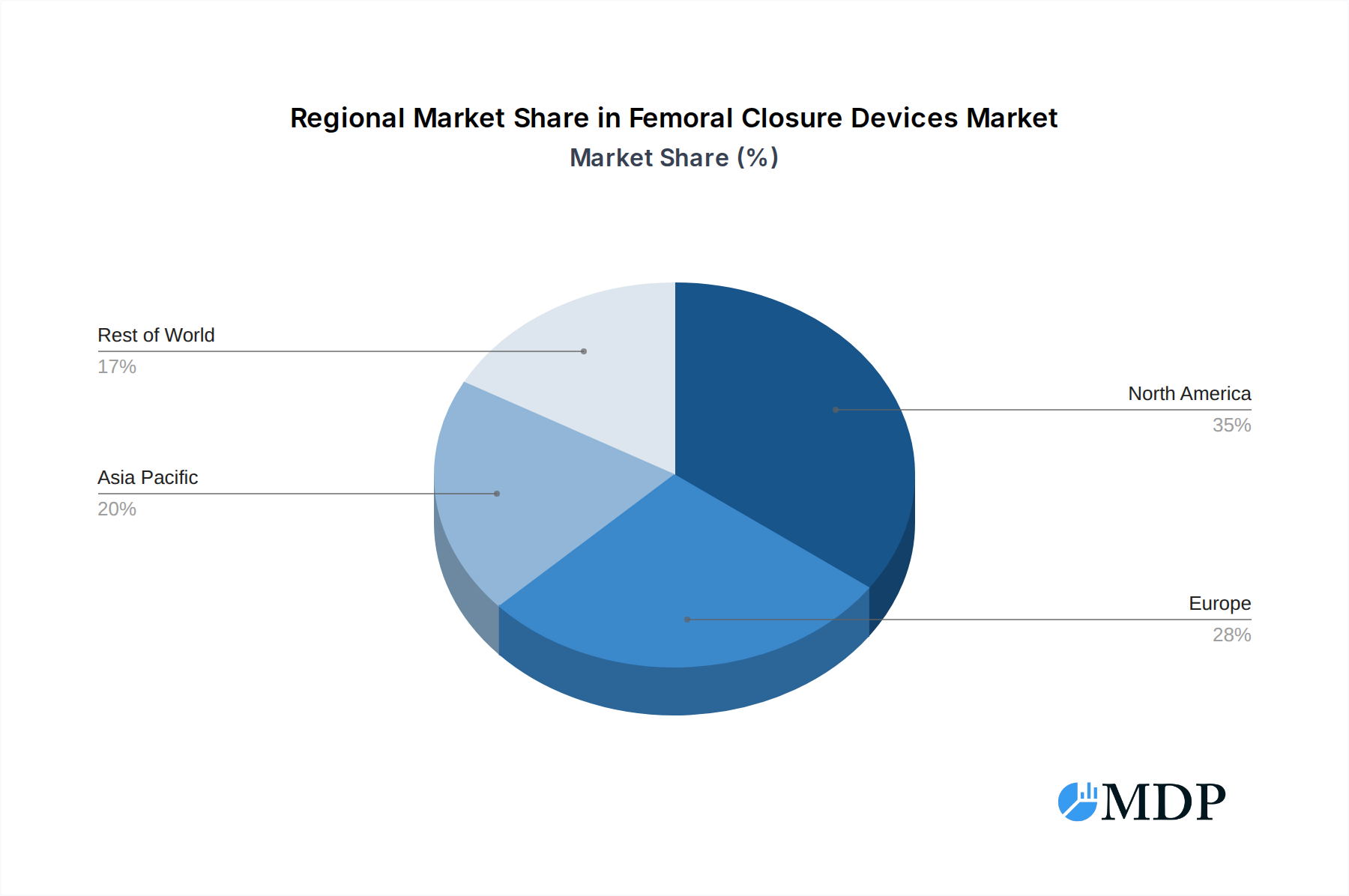

North America currently holds the dominant position in the Femoral Closure Devices Market, driven by a high incidence of cardiovascular diseases, advanced healthcare infrastructure, and a strong emphasis on adopting novel medical technologies. Within North America, the United States accounts for the largest share, a dominance attributed to favorable reimbursement policies for interventional procedures, substantial investment in medical R&D, and a high concentration of leading healthcare institutions.

Application Dominance:

- Interventional Procedures: This segment, encompassing a wide array of minimally invasive vascular interventions, represents the largest application area. The increasing volume of percutaneous coronary interventions (PCI), peripheral interventions, and electrophysiology procedures directly translates to a higher demand for effective femoral closure solutions. Key drivers include the growing elderly population undergoing these procedures and the continuous development of more complex interventional techniques.

- Angiography Surgery: While traditionally a significant application, the growth in angiography surgery closure devices is moderated by the increasing preference for purely interventional approaches. However, it remains a substantial segment, particularly in diagnostic procedures and complex surgical interventions.

Type Dominance:

- Active Closure Devices: This category is experiencing the most rapid growth. Active devices, which actively approximate the vessel walls through sutures, clips, or anchors, offer superior hemostasis and faster sealing compared to passive devices. The technological sophistication and proven efficacy of active closure devices are making them the preferred choice for many interventionalists, especially in high-flow arterial punctures. Their contribution to reducing complications like hematoma and pseudoaneurysm is a significant growth accelerator. The estimated market share for active closure devices in 2025 is over $1.8 billion.

- Passive Closure Devices: While still a significant market segment, passive closure devices, which rely on external pressure or internal collagen/gelatin plugs to achieve hemostasis, are witnessing slower growth compared to their active counterparts. They remain a viable and cost-effective option for certain procedures and patient profiles, but advancements in active closure technologies are gradually eroding their market dominance.

Femoral Closure Devices Product Developments

Recent product developments in the Femoral Closure Devices Market are characterized by a focus on enhanced biocompatibility, improved ease of use, and minimized patient trauma. Innovations include bioabsorbable materials for plugs, advanced anchor designs for more secure vessel approximation, and integrated imaging guidance systems for precise device deployment. These advancements aim to reduce closure time, lower complication rates such as bleeding and infection, and facilitate quicker patient ambulation, thereby offering a competitive edge to manufacturers and improved patient outcomes.

Key Drivers of Femoral Closure Devices Growth

The Femoral Closure Devices Market growth is primarily driven by the escalating incidence of cardiovascular diseases worldwide, necessitating a greater number of interventional procedures. Technological advancements in device design, leading to enhanced efficacy and reduced complications, are a significant catalyst. The growing preference for minimally invasive surgical techniques, coupled with favorable reimbursement policies for advanced closure solutions, further propels market expansion. The aging global population also contributes to the demand, as older individuals are more prone to vascular conditions requiring these interventions.

Challenges in the Femoral Closure Devices Market

Despite robust growth prospects, the Femoral Closure Devices Market faces several challenges. Stringent regulatory approvals for novel devices can lead to extended market entry timelines and significant development costs. The presence of established alternatives like manual compression, though less efficient, can pose a competitive restraint. Pricing pressures from healthcare systems seeking cost containment also impact market dynamics. Furthermore, the complexity of certain procedures may require specialized training for optimal device utilization, presenting an adoption barrier.

Emerging Opportunities in Femoral Closure Devices

Emerging opportunities in the Femoral Closure Devices Market lie in the development of highly specialized devices for complex vascular access scenarios, such as bariatric procedures or obese patient populations. The untapped potential in emerging economies, with their growing healthcare expenditures and increasing adoption of interventional cardiology, presents a significant expansion avenue. Strategic partnerships between device manufacturers and healthcare institutions can foster clinical validation and market penetration. Furthermore, advancements in biodegradable materials and smart closure technologies offer avenues for next-generation product innovation.

Leading Players in the Femoral Closure Devices Sector

- Abbott Laboratories

- Terumo

- Cardiva

- Cordis

- Morris Innovative

- Teleflex

- Vascular Solutions

- Essential Medical

- InSeal Medical

- Medeon Biodesign

- Transluminal Technologies

- Vasorum

- Cardinal Health

Key Milestones in Femoral Closure Devices Industry

- 2019: Launch of next-generation active closure devices with enhanced anchor technology.

- 2020: Significant increase in M&A activity as larger players acquire innovative startups.

- 2021: FDA approval of novel bioabsorbable plug technology for femoral closure.

- 2022: Growing adoption of dual-artery closure devices for complex procedures.

- 2023: Increased focus on robotic-assisted closure techniques.

- 2024: Expansion of product portfolios into pediatric vascular access.

- 2025: Projected surge in adoption of AI-guided closure device deployment systems.

- 2026-2033: Continued innovation in biomaterials and integration of smart device functionalities.

Strategic Outlook for Femoral Closure Devices Market

The strategic outlook for the Femoral Closure Devices Market is exceptionally positive, driven by an ongoing surge in demand for minimally invasive cardiovascular interventions. Key growth accelerators include relentless innovation in device technology, leading to improved patient outcomes and reduced healthcare costs. Market expansion into emerging economies and strategic collaborations will be crucial for sustained growth. The industry will likely witness further consolidation as companies seek to achieve economies of scale and broader market reach, solidifying the dominance of advanced closure solutions.

Femoral Closure Devices Segmentation

-

1. Application

- 1.1. Angiography Surgery

- 1.2. Interventional Procedures

-

2. Types

- 2.1. Passive Closure Devices

- 2.2. Active Closure Devices

Femoral Closure Devices Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Femoral Closure Devices Regional Market Share

Geographic Coverage of Femoral Closure Devices

Femoral Closure Devices REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Femoral Closure Devices Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Angiography Surgery

- 5.1.2. Interventional Procedures

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Passive Closure Devices

- 5.2.2. Active Closure Devices

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Femoral Closure Devices Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Angiography Surgery

- 6.1.2. Interventional Procedures

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Passive Closure Devices

- 6.2.2. Active Closure Devices

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Femoral Closure Devices Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Angiography Surgery

- 7.1.2. Interventional Procedures

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Passive Closure Devices

- 7.2.2. Active Closure Devices

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Femoral Closure Devices Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Angiography Surgery

- 8.1.2. Interventional Procedures

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Passive Closure Devices

- 8.2.2. Active Closure Devices

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Femoral Closure Devices Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Angiography Surgery

- 9.1.2. Interventional Procedures

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Passive Closure Devices

- 9.2.2. Active Closure Devices

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Femoral Closure Devices Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Angiography Surgery

- 10.1.2. Interventional Procedures

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Passive Closure Devices

- 10.2.2. Active Closure Devices

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Abbott Laboratories

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Terumo

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Cardiva

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Cordis

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Morris Innovative

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Teleflex

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Vascular Solutions

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Essential Medical

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 InSeal Medical

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Medeon Biodesign

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Transluminal Technologies

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Vasorum

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Cardinal Health

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Abbott Laboratories

List of Figures

- Figure 1: Global Femoral Closure Devices Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Femoral Closure Devices Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Femoral Closure Devices Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Femoral Closure Devices Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Femoral Closure Devices Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Femoral Closure Devices Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Femoral Closure Devices Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Femoral Closure Devices Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Femoral Closure Devices Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Femoral Closure Devices Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Femoral Closure Devices Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Femoral Closure Devices Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Femoral Closure Devices Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Femoral Closure Devices Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Femoral Closure Devices Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Femoral Closure Devices Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Femoral Closure Devices Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Femoral Closure Devices Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Femoral Closure Devices Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Femoral Closure Devices Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Femoral Closure Devices Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Femoral Closure Devices Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Femoral Closure Devices Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Femoral Closure Devices Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Femoral Closure Devices Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Femoral Closure Devices Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Femoral Closure Devices Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Femoral Closure Devices Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Femoral Closure Devices Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Femoral Closure Devices Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Femoral Closure Devices Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Femoral Closure Devices Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Femoral Closure Devices Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Femoral Closure Devices Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Femoral Closure Devices Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Femoral Closure Devices Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Femoral Closure Devices Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Femoral Closure Devices Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Femoral Closure Devices Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Femoral Closure Devices Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Femoral Closure Devices Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Femoral Closure Devices Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Femoral Closure Devices Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Femoral Closure Devices Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Femoral Closure Devices Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Femoral Closure Devices Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Femoral Closure Devices Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Femoral Closure Devices Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Femoral Closure Devices Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Femoral Closure Devices Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Femoral Closure Devices?

The projected CAGR is approximately 7.3%.

2. Which companies are prominent players in the Femoral Closure Devices?

Key companies in the market include Abbott Laboratories, Terumo, Cardiva, Cordis, Morris Innovative, Teleflex, Vascular Solutions, Essential Medical, InSeal Medical, Medeon Biodesign, Transluminal Technologies, Vasorum, Cardinal Health.

3. What are the main segments of the Femoral Closure Devices?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Femoral Closure Devices," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Femoral Closure Devices report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Femoral Closure Devices?

To stay informed about further developments, trends, and reports in the Femoral Closure Devices, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence