Key Insights

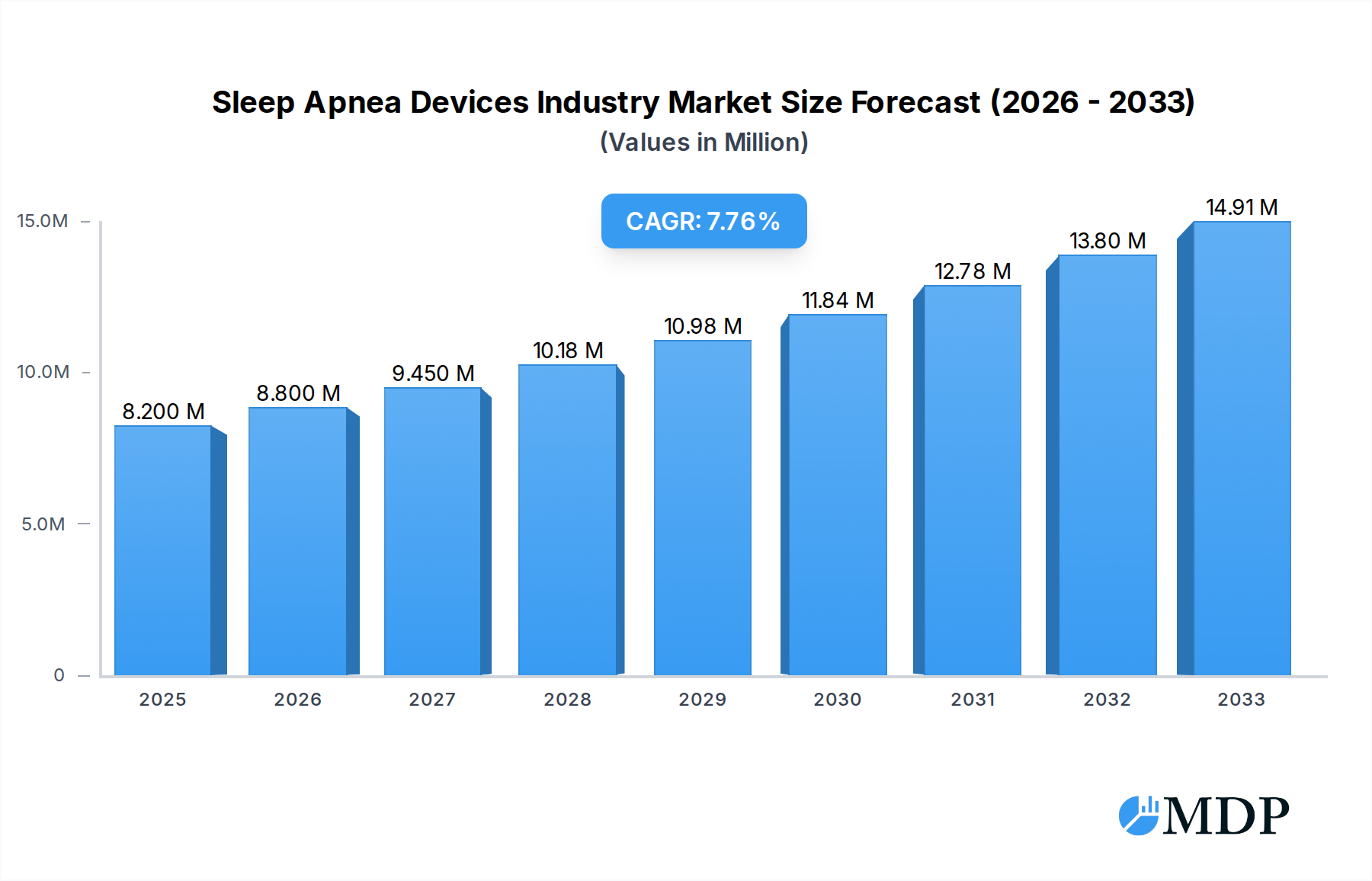

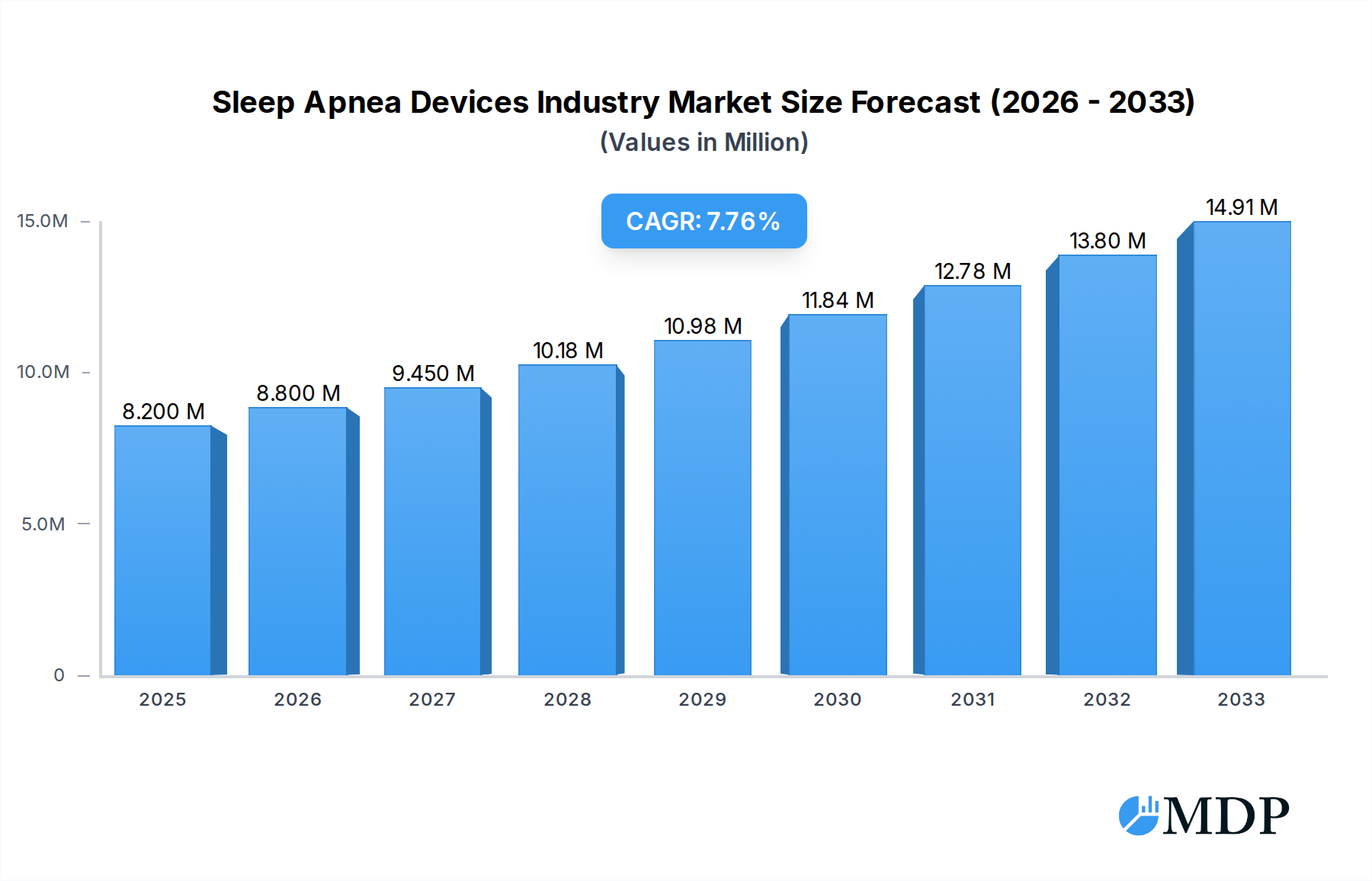

The global Sleep Apnea Devices market is poised for substantial expansion, projected to reach $8.20 Million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 7.33% between 2025 and 2033. This upward trajectory is fueled by several key drivers, including the increasing prevalence of sleep apnea globally, driven by rising obesity rates and an aging population, both significant risk factors for the disorder. Advancements in diagnostic technologies are also playing a crucial role, enabling earlier and more accurate detection. Furthermore, growing awareness among patients and healthcare professionals about the long-term health consequences of untreated sleep apnea, such as cardiovascular disease and stroke, is leading to a higher demand for effective treatment solutions. The market is segmented into Diagnostic Devices, encompassing polysomnography (PSG) devices, pulse oximeters, and actigraphy devices, and Therapeutic Devices, which include Positive Airway Pressure (PAP) devices (CPAP and BiPAP), oxygen devices, oral appliances, adaptive servo-ventilation (ASV) devices, and masks and accessories. The therapeutic segment, particularly PAP devices, is expected to dominate the market due to their widespread adoption and efficacy.

Sleep Apnea Devices Industry Market Size (In Million)

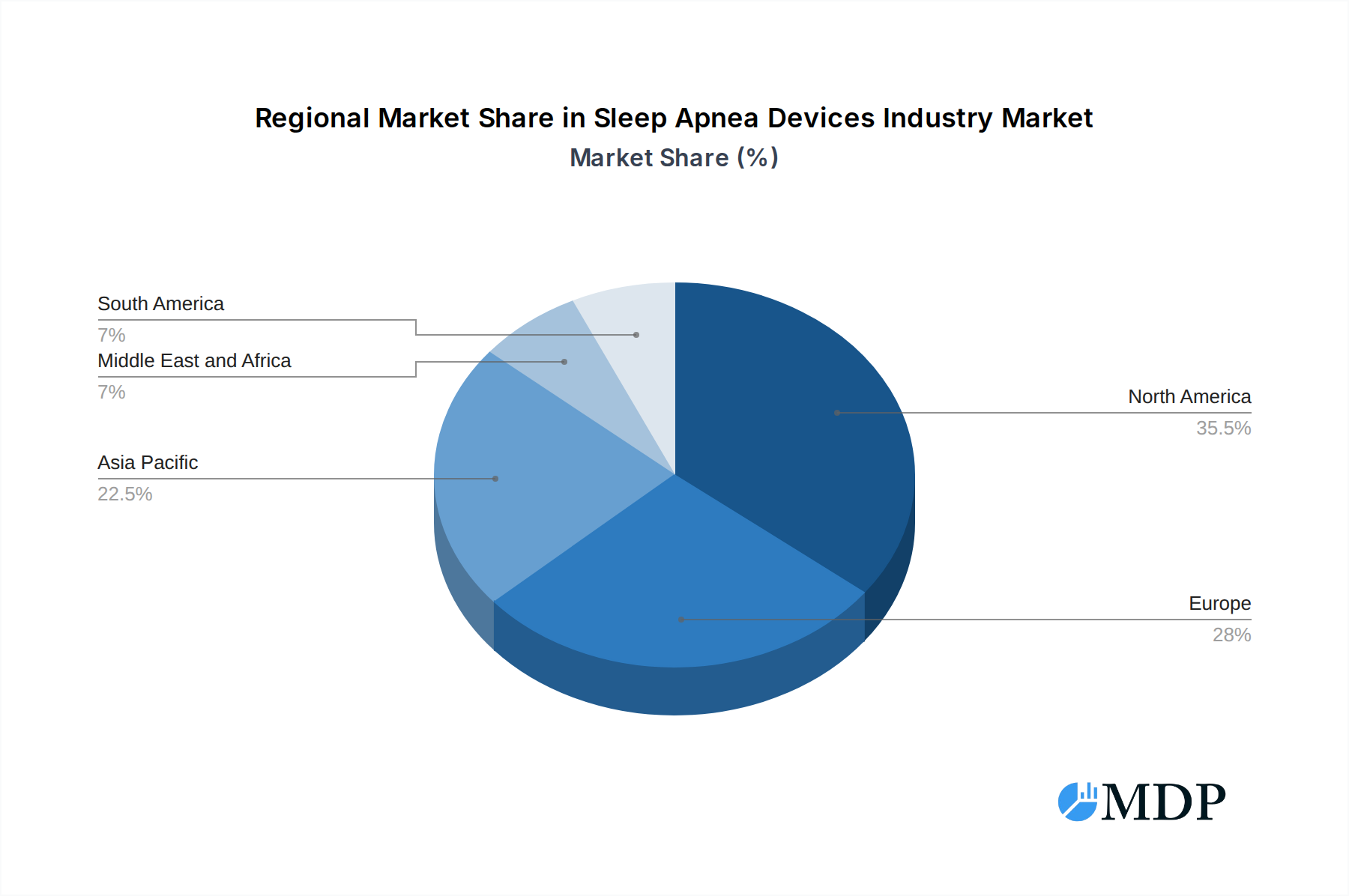

Several emerging trends are shaping the sleep apnea devices landscape. The integration of artificial intelligence (AI) and machine learning (ML) in diagnostic devices is enhancing data analysis and predictive capabilities. The development of more comfortable, user-friendly, and portable therapeutic devices, including miniaturized PAP machines and advanced mask designs, is improving patient compliance and adherence. Telehealth and remote monitoring solutions are also gaining traction, allowing for continuous patient management and support, which is particularly beneficial for individuals in remote areas. Geographically, North America currently leads the market, owing to high healthcare expenditure and early adoption of advanced medical technologies. However, the Asia Pacific region is anticipated to witness the fastest growth, driven by increasing healthcare infrastructure development, rising disposable incomes, and growing awareness of sleep disorders. Despite the positive outlook, market restraints such as the high cost of some advanced devices and potential reimbursement challenges in certain regions could pose hurdles. Nonetheless, the continuous innovation and increasing focus on sleep health are expected to drive sustained market growth.

Sleep Apnea Devices Industry Company Market Share

Unlock Profitable Growth in the Booming Sleep Apnea Devices Market: Comprehensive 2025-2033 Industry Report

Gain a critical edge in the rapidly expanding sleep apnea devices market with our in-depth, SEO-optimized industry report. Spanning the historical period of 2019-2024 and projecting to 2033, with a base year and estimated year of 2025, this comprehensive analysis delves into the intricate dynamics, key drivers, emerging opportunities, and challenges shaping this multi-billion dollar sector. Discover the latest product developments, leading players, and market trends impacting CPAP machines, BiPAP devices, oral appliances, and more. This report is your essential guide to navigating the global sleep apnea diagnosis and treatment landscape, essential for medical device manufacturers, healthcare providers, investors, and industry stakeholders seeking to capitalize on surging demand for sleep disorder solutions.

Sleep Apnea Devices Industry Market Dynamics & Concentration

The sleep apnea devices industry exhibits a moderate to high level of market concentration, driven by the significant R&D investments and stringent regulatory approvals required for therapeutic and diagnostic devices. Innovation remains a primary driver, fueled by advancements in AI-driven diagnostics, miniaturization of devices, and the development of more patient-friendly therapeutic solutions. Regulatory frameworks, such as FDA approvals in the US and CE marking in Europe, play a crucial role in market entry and product validation, acting as both a barrier to new entrants and a quality assurance mechanism for established players. Product substitutes, while present, are often limited in efficacy for severe cases, with lifestyle modifications and surgical interventions offering alternative but distinct treatment pathways. End-user trends are increasingly leaning towards home-based diagnostics and treatment, driven by convenience, cost-effectiveness, and growing awareness. Mergers and acquisitions (M&A) activities are a significant aspect of market concentration, with larger players acquiring innovative startups to expand their product portfolios and market reach. For instance, recent M&A deals have focused on companies developing advanced oral appliances and connected diagnostic tools. The market share distribution is characterized by a few dominant players holding substantial portions, while a growing number of niche players cater to specific segments or technological advancements. M&A deal counts in the past five years have shown a consistent upward trend, indicating strategic consolidation within the industry.

Sleep Apnea Devices Industry Industry Trends & Analysis

The sleep apnea devices industry is poised for robust growth, projected at a Compound Annual Growth Rate (CAGR) of approximately 8-10% during the forecast period of 2025–2033. This expansion is primarily fueled by a confluence of escalating awareness surrounding the adverse health consequences of untreated sleep apnea, including cardiovascular diseases, diabetes, and cognitive impairment, and the increasing prevalence of obesity, a significant risk factor. Technological disruptions are rapidly transforming the market, with a strong emphasis on connectivity and data analytics. Smart CPAP devices, equipped with wireless capabilities, allow for remote monitoring of patient adherence and treatment efficacy, enabling personalized therapy adjustments and improved patient outcomes. The integration of Artificial Intelligence (AI) in diagnostic tools, such as polysomnography (PSG) analysis, promises more accurate and faster diagnoses. Consumer preferences are shifting towards user-friendly, portable, and less intrusive solutions. This is driving demand for compact diagnostic devices like actigraphy and pulse oximeters for at-home monitoring, and quieter, more comfortable therapeutic devices. Furthermore, the growing acceptance of telehealth services is facilitating remote consultations and prescriptions, further boosting the adoption of home-use sleep apnea devices. Competitive dynamics are intensifying, with established giants like Philips, ResMed, and Fisher & Paykel Healthcare investing heavily in innovation and market expansion. The entry of new players, particularly those focusing on niche segments like oral appliances or innovative portable oxygen solutions, adds to the competitive landscape. Market penetration for sleep apnea devices, while growing, still has significant room for expansion, especially in emerging economies where awareness and healthcare infrastructure are rapidly developing. The increasing digitalization of healthcare and the focus on preventative medicine are also key market growth drivers, encouraging earlier diagnosis and intervention for sleep disorders.

Leading Markets & Segments in Sleep Apnea Devices Industry

The Therapeutic Devices segment commands the largest market share within the sleep apnea devices industry, predominantly driven by the Positive Airway Pressure (PAP) Devices, which include Continuous Positive Airway Pressure (CPAP) Devices and Bi-level Positive Airway Pressure (BiPAP) Devices. The dominance of PAP devices is attributed to their established efficacy in treating Obstructive Sleep Apnea (OSA), the most common form of the disorder. The growing incidence of OSA, coupled with increasing patient awareness and physician recommendation, fuels the demand for these devices. Within the therapeutic segment, CPAP devices represent the largest sub-segment due to their widespread adoption for mild to moderate OSA. BiPAP devices, offering varied pressure levels, cater to more complex cases and patients intolerant to CPAP.

The Diagnostic Devices segment is also experiencing substantial growth, with Polysomnography (PSG) Devices being the cornerstone for comprehensive sleep studies. However, the trend towards home-based diagnostics is elevating the importance of Actigraphy Devices and Pulse Oximeters for preliminary screening and continuous monitoring, offering convenience and cost-effectiveness.

Oxygen Devices, including Oxygen Concentrators and Portable Oxygen Concentrators, form another crucial segment, particularly for patients with co-existing respiratory conditions or severe sleep apnea requiring supplemental oxygen. The increasing preference for portable solutions enhances market penetration for Portable Oxygen Concentrators.

Oral Appliances are gaining traction as a viable alternative for patients with snoring and mild to moderate OSA who are CPAP-intolerant or prefer a non-invasive option. The innovation in this segment, such as the flexTAP appliance, highlights its growing appeal.

Adaptive Servo Ventilation (ASV) Devices address complex sleep breathing disorders, including central sleep apnea, and represent a niche but growing segment with advanced technological integration.

Masks and Accessories form an indispensable sub-segment, directly impacting patient comfort and adherence to PAP therapy. Innovations in mask design, materials, and fit are critical for user satisfaction.

Geographically, North America currently leads the market, driven by high awareness, advanced healthcare infrastructure, favorable reimbursement policies, and a high prevalence of obesity. The United States is the dominant country within this region. Europe follows closely, with countries like Germany, the UK, and France exhibiting strong market performance. The Asia-Pacific region is emerging as the fastest-growing market, fueled by increasing disposable incomes, rising healthcare expenditure, growing awareness of sleep disorders, and a large, underserved population. Economic policies promoting healthcare access and infrastructure development in these regions are key drivers of market expansion across all segments.

Sleep Apnea Devices Industry Product Developments

Product development in the sleep apnea devices industry is intensely focused on enhancing patient comfort, improving diagnostic accuracy, and leveraging connectivity. Innovations in PAP devices include quieter operation, integrated humidification systems, and advanced algorithms for pressure titration. Smart masks with integrated sensors are emerging to provide real-time data on mask fit and leakage. Diagnostic devices are becoming more compact and user-friendly, facilitating home-based sleep testing. The integration of AI for automated sleep stage scoring and anomaly detection in PSG data is a significant technological trend. Furthermore, the development of personalized oral appliances through 3D printing and advanced material science offers improved efficacy and comfort. These advancements not only improve patient outcomes but also address adherence challenges, a critical factor in managing sleep apnea effectively.

Key Drivers of Sleep Apnea Devices Industry Growth

Several key drivers are propelling the growth of the sleep apnea devices industry. Firstly, the escalating prevalence of sleep apnea, largely attributed to rising obesity rates and an aging global population, is a primary catalyst. Secondly, increasing patient and physician awareness regarding the severe health implications of untreated sleep apnea, such as cardiovascular disease and stroke, is driving demand for diagnosis and treatment. Thirdly, technological advancements, including the development of more comfortable and user-friendly PAP devices, sophisticated diagnostic tools, and connected health solutions, are enhancing patient adherence and treatment effectiveness. Favorable reimbursement policies in developed economies also play a crucial role in facilitating access to these devices. Lastly, the growing emphasis on preventative healthcare and the integration of telehealth are further accelerating market expansion.

Challenges in the Sleep Apnea Devices Industry Market

Despite its robust growth, the sleep apnea devices industry faces several challenges. High upfront costs of advanced diagnostic and therapeutic devices can be a barrier to adoption, particularly in emerging markets with limited healthcare budgets. Stringent regulatory approval processes, while ensuring product quality, can lead to extended time-to-market for new innovations. Reimbursement complexities and variations across different healthcare systems can also impact market access and affordability. Furthermore, patient adherence to therapy, especially with PAP devices, remains a significant challenge due to issues like mask discomfort, claustrophobia, and perceived inconvenience. Competitive pressures from both established players and emerging technologies also necessitate continuous innovation and cost optimization. Supply chain disruptions, as seen in recent global events, can also impact the availability and pricing of critical components.

Emerging Opportunities in Sleep Apnea Devices Industry

The sleep apnea devices industry is ripe with emerging opportunities for long-term growth. The increasing demand for home-based sleep diagnostics presents a significant avenue, driven by the convenience and cost-effectiveness of devices like actigraphy and portable PSG. The growing adoption of telehealth and remote patient monitoring solutions offers immense potential for connected sleep apnea devices, enabling continuous data tracking and personalized treatment adjustments. The development of AI-powered diagnostic tools promises to revolutionize sleep disorder detection, leading to earlier and more accurate diagnoses. Furthermore, the underserved markets in developing economies represent a vast untapped potential, as awareness and healthcare infrastructure improve. Strategic partnerships between device manufacturers, healthcare providers, and technology companies can accelerate innovation and market penetration, creating new integrated solutions for sleep disorder management.

Leading Players in the Sleep Apnea Devices Industry Sector

- Resmed

- Koninklijke Philips NV

- Fisher & Paykel Healthcare Limited

- GE Healthcare

- Invacare Corporation

- Vyaire Medical Inc

- Natus Medical Incorporated

- Somnomed

- Teleflex Incorporated

- Cadwell Laboratories Inc

- Nihon Kohden Corporation

- Oventus Medical

Key Milestones in Sleep Apnea Devices Industry Industry

- November 2022: ResMed and Alphabet's life science offshoot Verily announced the formation of Primasun, an end-to-end solution to help employers and healthcare providers identify populations at risk for complex sleep disorders.

- October 2022: Airway Management, manufacturer of the most globally researched custom oral appliances, announced the launch of flexTAP, a premium lab-made oral appliance designed to treat patients with snoring and mild to moderate obstructive sleep apnea.

Strategic Outlook for Sleep Apnea Devices Industry Market

The strategic outlook for the sleep apnea devices industry is overwhelmingly positive, driven by sustained demand and continuous innovation. Key growth accelerators include the increasing integration of artificial intelligence and machine learning in diagnostic and therapeutic devices, promising more personalized and effective treatments. The expansion of telehealth and remote patient monitoring platforms will further enhance patient engagement and adherence, particularly for CPAP therapy. A significant opportunity lies in addressing the large undiagnosed and undertreated sleep apnea population globally, especially in emerging markets. Strategic partnerships and collaborations, such as the one between ResMed and Verily, will be crucial for developing comprehensive sleep disorder management solutions. Investment in user-friendly, compact, and data-driven devices will remain paramount for capturing market share and meeting evolving consumer preferences. The industry is poised for a future characterized by greater accessibility, improved patient outcomes, and significant market expansion.

Sleep Apnea Devices Industry Segmentation

-

1. Diagnostic Devices

- 1.1. Polysomnography Devices (PSG)

- 1.2. Pulse Oximeters

- 1.3. Actigraphy Devices

-

2. Therapeutic Devices

-

2.1. Positive Airway Pressure (PAP) Devices

- 2.1.1. Continuous Positive Airway Pressure (CPAP) Devices

- 2.1.2. Bi-level Positive Airway Pressure (BiPAP) Devices

-

2.2. Oxygen Devices

- 2.2.1. Oxygen Concentrators

- 2.2.2. Portable Oxygen Concentrators

- 2.2.3. Liquid Portable Oxygen

- 2.3. Oral Appliances

- 2.4. Adaptive Servo Ventilation (ASV) Devices

- 2.5. Masks and Accessories

-

2.1. Positive Airway Pressure (PAP) Devices

Sleep Apnea Devices Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Sleep Apnea Devices Industry Regional Market Share

Geographic Coverage of Sleep Apnea Devices Industry

Sleep Apnea Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.33% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 5.1.1. Polysomnography Devices (PSG)

- 5.1.2. Pulse Oximeters

- 5.1.3. Actigraphy Devices

- 5.2. Market Analysis, Insights and Forecast - by Therapeutic Devices

- 5.2.1. Positive Airway Pressure (PAP) Devices

- 5.2.1.1. Continuous Positive Airway Pressure (CPAP) Devices

- 5.2.1.2. Bi-level Positive Airway Pressure (BiPAP) Devices

- 5.2.2. Oxygen Devices

- 5.2.2.1. Oxygen Concentrators

- 5.2.2.2. Portable Oxygen Concentrators

- 5.2.2.3. Liquid Portable Oxygen

- 5.2.3. Oral Appliances

- 5.2.4. Adaptive Servo Ventilation (ASV) Devices

- 5.2.5. Masks and Accessories

- 5.2.1. Positive Airway Pressure (PAP) Devices

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 6. Global Sleep Apnea Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 6.1.1. Polysomnography Devices (PSG)

- 6.1.2. Pulse Oximeters

- 6.1.3. Actigraphy Devices

- 6.2. Market Analysis, Insights and Forecast - by Therapeutic Devices

- 6.2.1. Positive Airway Pressure (PAP) Devices

- 6.2.1.1. Continuous Positive Airway Pressure (CPAP) Devices

- 6.2.1.2. Bi-level Positive Airway Pressure (BiPAP) Devices

- 6.2.2. Oxygen Devices

- 6.2.2.1. Oxygen Concentrators

- 6.2.2.2. Portable Oxygen Concentrators

- 6.2.2.3. Liquid Portable Oxygen

- 6.2.3. Oral Appliances

- 6.2.4. Adaptive Servo Ventilation (ASV) Devices

- 6.2.5. Masks and Accessories

- 6.2.1. Positive Airway Pressure (PAP) Devices

- 6.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 7. North America Sleep Apnea Devices Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 7.1.1. Polysomnography Devices (PSG)

- 7.1.2. Pulse Oximeters

- 7.1.3. Actigraphy Devices

- 7.2. Market Analysis, Insights and Forecast - by Therapeutic Devices

- 7.2.1. Positive Airway Pressure (PAP) Devices

- 7.2.1.1. Continuous Positive Airway Pressure (CPAP) Devices

- 7.2.1.2. Bi-level Positive Airway Pressure (BiPAP) Devices

- 7.2.2. Oxygen Devices

- 7.2.2.1. Oxygen Concentrators

- 7.2.2.2. Portable Oxygen Concentrators

- 7.2.2.3. Liquid Portable Oxygen

- 7.2.3. Oral Appliances

- 7.2.4. Adaptive Servo Ventilation (ASV) Devices

- 7.2.5. Masks and Accessories

- 7.2.1. Positive Airway Pressure (PAP) Devices

- 7.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 8. Europe Sleep Apnea Devices Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 8.1.1. Polysomnography Devices (PSG)

- 8.1.2. Pulse Oximeters

- 8.1.3. Actigraphy Devices

- 8.2. Market Analysis, Insights and Forecast - by Therapeutic Devices

- 8.2.1. Positive Airway Pressure (PAP) Devices

- 8.2.1.1. Continuous Positive Airway Pressure (CPAP) Devices

- 8.2.1.2. Bi-level Positive Airway Pressure (BiPAP) Devices

- 8.2.2. Oxygen Devices

- 8.2.2.1. Oxygen Concentrators

- 8.2.2.2. Portable Oxygen Concentrators

- 8.2.2.3. Liquid Portable Oxygen

- 8.2.3. Oral Appliances

- 8.2.4. Adaptive Servo Ventilation (ASV) Devices

- 8.2.5. Masks and Accessories

- 8.2.1. Positive Airway Pressure (PAP) Devices

- 8.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 9. Asia Pacific Sleep Apnea Devices Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 9.1.1. Polysomnography Devices (PSG)

- 9.1.2. Pulse Oximeters

- 9.1.3. Actigraphy Devices

- 9.2. Market Analysis, Insights and Forecast - by Therapeutic Devices

- 9.2.1. Positive Airway Pressure (PAP) Devices

- 9.2.1.1. Continuous Positive Airway Pressure (CPAP) Devices

- 9.2.1.2. Bi-level Positive Airway Pressure (BiPAP) Devices

- 9.2.2. Oxygen Devices

- 9.2.2.1. Oxygen Concentrators

- 9.2.2.2. Portable Oxygen Concentrators

- 9.2.2.3. Liquid Portable Oxygen

- 9.2.3. Oral Appliances

- 9.2.4. Adaptive Servo Ventilation (ASV) Devices

- 9.2.5. Masks and Accessories

- 9.2.1. Positive Airway Pressure (PAP) Devices

- 9.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 10. Middle East and Africa Sleep Apnea Devices Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 10.1.1. Polysomnography Devices (PSG)

- 10.1.2. Pulse Oximeters

- 10.1.3. Actigraphy Devices

- 10.2. Market Analysis, Insights and Forecast - by Therapeutic Devices

- 10.2.1. Positive Airway Pressure (PAP) Devices

- 10.2.1.1. Continuous Positive Airway Pressure (CPAP) Devices

- 10.2.1.2. Bi-level Positive Airway Pressure (BiPAP) Devices

- 10.2.2. Oxygen Devices

- 10.2.2.1. Oxygen Concentrators

- 10.2.2.2. Portable Oxygen Concentrators

- 10.2.2.3. Liquid Portable Oxygen

- 10.2.3. Oral Appliances

- 10.2.4. Adaptive Servo Ventilation (ASV) Devices

- 10.2.5. Masks and Accessories

- 10.2.1. Positive Airway Pressure (PAP) Devices

- 10.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 11. South America Sleep Apnea Devices Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 11.1.1. Polysomnography Devices (PSG)

- 11.1.2. Pulse Oximeters

- 11.1.3. Actigraphy Devices

- 11.2. Market Analysis, Insights and Forecast - by Therapeutic Devices

- 11.2.1. Positive Airway Pressure (PAP) Devices

- 11.2.1.1. Continuous Positive Airway Pressure (CPAP) Devices

- 11.2.1.2. Bi-level Positive Airway Pressure (BiPAP) Devices

- 11.2.2. Oxygen Devices

- 11.2.2.1. Oxygen Concentrators

- 11.2.2.2. Portable Oxygen Concentrators

- 11.2.2.3. Liquid Portable Oxygen

- 11.2.3. Oral Appliances

- 11.2.4. Adaptive Servo Ventilation (ASV) Devices

- 11.2.5. Masks and Accessories

- 11.2.1. Positive Airway Pressure (PAP) Devices

- 11.1. Market Analysis, Insights and Forecast - by Diagnostic Devices

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Natus Medical Incorporated

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Invacare Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Cadwell Laboratories Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 GE Healthcare

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Vyaire Medical Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Resmed

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Oventus Medical

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Fisher & Paykel Healthcare Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Koninklijke Philips NV

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Somnomed

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Teleflex Incorporated

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Nihon Kohden Corporation

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Natus Medical Incorporated

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Sleep Apnea Devices Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Sleep Apnea Devices Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Sleep Apnea Devices Industry Revenue (Million), by Diagnostic Devices 2025 & 2033

- Figure 4: North America Sleep Apnea Devices Industry Volume (K Unit), by Diagnostic Devices 2025 & 2033

- Figure 5: North America Sleep Apnea Devices Industry Revenue Share (%), by Diagnostic Devices 2025 & 2033

- Figure 6: North America Sleep Apnea Devices Industry Volume Share (%), by Diagnostic Devices 2025 & 2033

- Figure 7: North America Sleep Apnea Devices Industry Revenue (Million), by Therapeutic Devices 2025 & 2033

- Figure 8: North America Sleep Apnea Devices Industry Volume (K Unit), by Therapeutic Devices 2025 & 2033

- Figure 9: North America Sleep Apnea Devices Industry Revenue Share (%), by Therapeutic Devices 2025 & 2033

- Figure 10: North America Sleep Apnea Devices Industry Volume Share (%), by Therapeutic Devices 2025 & 2033

- Figure 11: North America Sleep Apnea Devices Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Sleep Apnea Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Sleep Apnea Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Sleep Apnea Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Sleep Apnea Devices Industry Revenue (Million), by Diagnostic Devices 2025 & 2033

- Figure 16: Europe Sleep Apnea Devices Industry Volume (K Unit), by Diagnostic Devices 2025 & 2033

- Figure 17: Europe Sleep Apnea Devices Industry Revenue Share (%), by Diagnostic Devices 2025 & 2033

- Figure 18: Europe Sleep Apnea Devices Industry Volume Share (%), by Diagnostic Devices 2025 & 2033

- Figure 19: Europe Sleep Apnea Devices Industry Revenue (Million), by Therapeutic Devices 2025 & 2033

- Figure 20: Europe Sleep Apnea Devices Industry Volume (K Unit), by Therapeutic Devices 2025 & 2033

- Figure 21: Europe Sleep Apnea Devices Industry Revenue Share (%), by Therapeutic Devices 2025 & 2033

- Figure 22: Europe Sleep Apnea Devices Industry Volume Share (%), by Therapeutic Devices 2025 & 2033

- Figure 23: Europe Sleep Apnea Devices Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Sleep Apnea Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Sleep Apnea Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Sleep Apnea Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Sleep Apnea Devices Industry Revenue (Million), by Diagnostic Devices 2025 & 2033

- Figure 28: Asia Pacific Sleep Apnea Devices Industry Volume (K Unit), by Diagnostic Devices 2025 & 2033

- Figure 29: Asia Pacific Sleep Apnea Devices Industry Revenue Share (%), by Diagnostic Devices 2025 & 2033

- Figure 30: Asia Pacific Sleep Apnea Devices Industry Volume Share (%), by Diagnostic Devices 2025 & 2033

- Figure 31: Asia Pacific Sleep Apnea Devices Industry Revenue (Million), by Therapeutic Devices 2025 & 2033

- Figure 32: Asia Pacific Sleep Apnea Devices Industry Volume (K Unit), by Therapeutic Devices 2025 & 2033

- Figure 33: Asia Pacific Sleep Apnea Devices Industry Revenue Share (%), by Therapeutic Devices 2025 & 2033

- Figure 34: Asia Pacific Sleep Apnea Devices Industry Volume Share (%), by Therapeutic Devices 2025 & 2033

- Figure 35: Asia Pacific Sleep Apnea Devices Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Pacific Sleep Apnea Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Sleep Apnea Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Sleep Apnea Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East and Africa Sleep Apnea Devices Industry Revenue (Million), by Diagnostic Devices 2025 & 2033

- Figure 40: Middle East and Africa Sleep Apnea Devices Industry Volume (K Unit), by Diagnostic Devices 2025 & 2033

- Figure 41: Middle East and Africa Sleep Apnea Devices Industry Revenue Share (%), by Diagnostic Devices 2025 & 2033

- Figure 42: Middle East and Africa Sleep Apnea Devices Industry Volume Share (%), by Diagnostic Devices 2025 & 2033

- Figure 43: Middle East and Africa Sleep Apnea Devices Industry Revenue (Million), by Therapeutic Devices 2025 & 2033

- Figure 44: Middle East and Africa Sleep Apnea Devices Industry Volume (K Unit), by Therapeutic Devices 2025 & 2033

- Figure 45: Middle East and Africa Sleep Apnea Devices Industry Revenue Share (%), by Therapeutic Devices 2025 & 2033

- Figure 46: Middle East and Africa Sleep Apnea Devices Industry Volume Share (%), by Therapeutic Devices 2025 & 2033

- Figure 47: Middle East and Africa Sleep Apnea Devices Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Middle East and Africa Sleep Apnea Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Middle East and Africa Sleep Apnea Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa Sleep Apnea Devices Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America Sleep Apnea Devices Industry Revenue (Million), by Diagnostic Devices 2025 & 2033

- Figure 52: South America Sleep Apnea Devices Industry Volume (K Unit), by Diagnostic Devices 2025 & 2033

- Figure 53: South America Sleep Apnea Devices Industry Revenue Share (%), by Diagnostic Devices 2025 & 2033

- Figure 54: South America Sleep Apnea Devices Industry Volume Share (%), by Diagnostic Devices 2025 & 2033

- Figure 55: South America Sleep Apnea Devices Industry Revenue (Million), by Therapeutic Devices 2025 & 2033

- Figure 56: South America Sleep Apnea Devices Industry Volume (K Unit), by Therapeutic Devices 2025 & 2033

- Figure 57: South America Sleep Apnea Devices Industry Revenue Share (%), by Therapeutic Devices 2025 & 2033

- Figure 58: South America Sleep Apnea Devices Industry Volume Share (%), by Therapeutic Devices 2025 & 2033

- Figure 59: South America Sleep Apnea Devices Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: South America Sleep Apnea Devices Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: South America Sleep Apnea Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: South America Sleep Apnea Devices Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Diagnostic Devices 2020 & 2033

- Table 2: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Diagnostic Devices 2020 & 2033

- Table 3: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Therapeutic Devices 2020 & 2033

- Table 4: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Therapeutic Devices 2020 & 2033

- Table 5: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Diagnostic Devices 2020 & 2033

- Table 8: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Diagnostic Devices 2020 & 2033

- Table 9: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Therapeutic Devices 2020 & 2033

- Table 10: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Therapeutic Devices 2020 & 2033

- Table 11: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Mexico Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Diagnostic Devices 2020 & 2033

- Table 20: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Diagnostic Devices 2020 & 2033

- Table 21: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Therapeutic Devices 2020 & 2033

- Table 22: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Therapeutic Devices 2020 & 2033

- Table 23: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Germany Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Germany Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: France Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: France Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Italy Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Italy Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Spain Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Spain Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Europe Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Diagnostic Devices 2020 & 2033

- Table 38: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Diagnostic Devices 2020 & 2033

- Table 39: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Therapeutic Devices 2020 & 2033

- Table 40: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Therapeutic Devices 2020 & 2033

- Table 41: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: China Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: China Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Japan Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Japan Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: India Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: India Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Australia Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Australia Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: South Korea Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: South Korea Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Rest of Asia Pacific Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Asia Pacific Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Diagnostic Devices 2020 & 2033

- Table 56: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Diagnostic Devices 2020 & 2033

- Table 57: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Therapeutic Devices 2020 & 2033

- Table 58: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Therapeutic Devices 2020 & 2033

- Table 59: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: GCC Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: GCC Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: South Africa Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: South Africa Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of Middle East and Africa Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: Rest of Middle East and Africa Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 67: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Diagnostic Devices 2020 & 2033

- Table 68: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Diagnostic Devices 2020 & 2033

- Table 69: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Therapeutic Devices 2020 & 2033

- Table 70: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Therapeutic Devices 2020 & 2033

- Table 71: Global Sleep Apnea Devices Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 72: Global Sleep Apnea Devices Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 73: Brazil Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: Brazil Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Argentina Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Argentina Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Rest of South America Sleep Apnea Devices Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 78: Rest of South America Sleep Apnea Devices Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sleep Apnea Devices Industry?

The projected CAGR is approximately 7.33%.

2. Which companies are prominent players in the Sleep Apnea Devices Industry?

Key companies in the market include Natus Medical Incorporated, Invacare Corporation, Cadwell Laboratories Inc, GE Healthcare, Vyaire Medical Inc, Resmed, Oventus Medical, Fisher & Paykel Healthcare Limited, Koninklijke Philips NV, Somnomed, Teleflex Incorporated, Nihon Kohden Corporation.

3. What are the main segments of the Sleep Apnea Devices Industry?

The market segments include Diagnostic Devices, Therapeutic Devices.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.20 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Awareness Among the Patient Population in the Developing Countries; Increase in Prevalence of Obesity and Hypertension; Upcoming Technological Advancements.

6. What are the notable trends driving market growth?

Pulse Oximeters are Expected to Register the Highest CAGR in the Diagnostic Devices Category.

7. Are there any restraints impacting market growth?

High Cost of Cpap Machines.

8. Can you provide examples of recent developments in the market?

In November 2022, ResMed and Alphabet's life science offshoot Verily announced the formation of Primasun, an end-to-end solution to help employers and healthcare providers identify populations at risk for complex sleep disorders.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sleep Apnea Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sleep Apnea Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sleep Apnea Devices Industry?

To stay informed about further developments, trends, and reports in the Sleep Apnea Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence