Key Insights

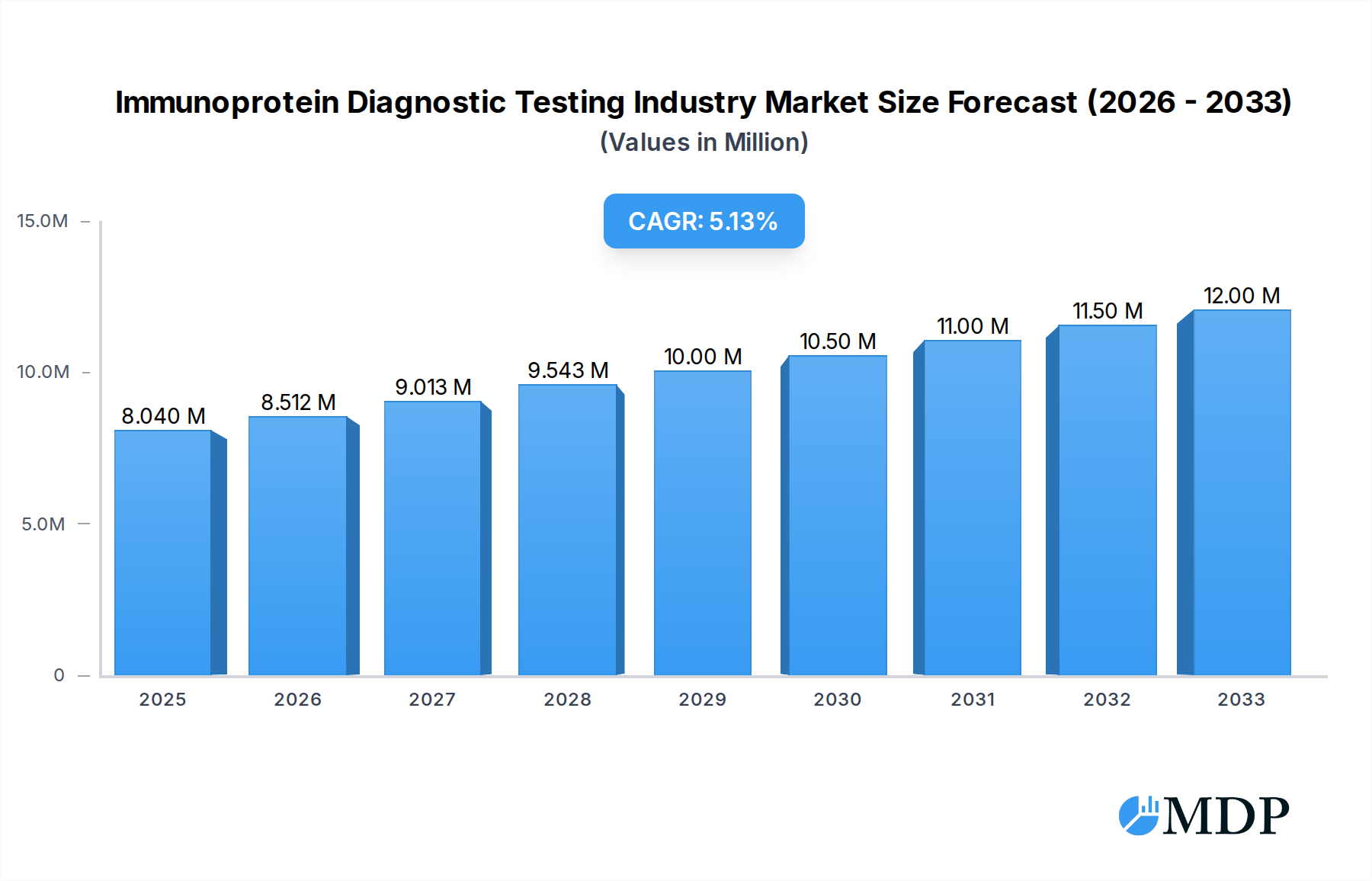

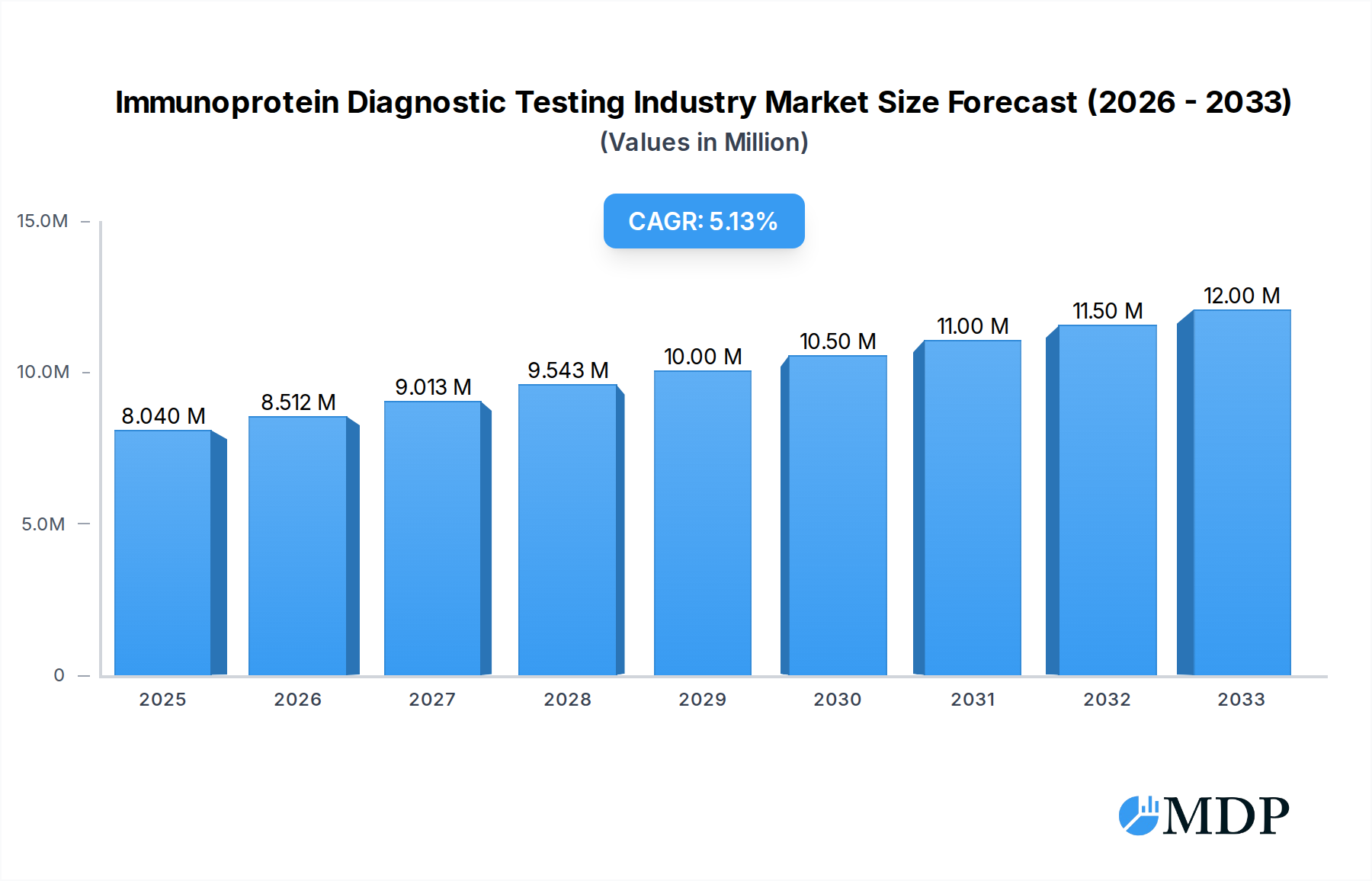

The Immunoprotein Diagnostic Testing market is poised for significant expansion, projected to reach 8.04 Million in value by 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 5.88%, indicating a sustained upward trajectory throughout the forecast period. The market's dynamism is fueled by escalating healthcare expenditures globally, a growing emphasis on early disease detection and personalized medicine, and the continuous development of advanced diagnostic technologies. The increasing prevalence of chronic and infectious diseases, coupled with an aging global population, further amplifies the demand for accurate and reliable immunoprotein diagnostic tests. Innovations in areas like chemiluminescence and immunofluorescence assays are enhancing sensitivity and specificity, enabling earlier and more precise diagnoses, which are crucial for effective treatment and improved patient outcomes.

Immunoprotein Diagnostic Testing Industry Market Size (In Million)

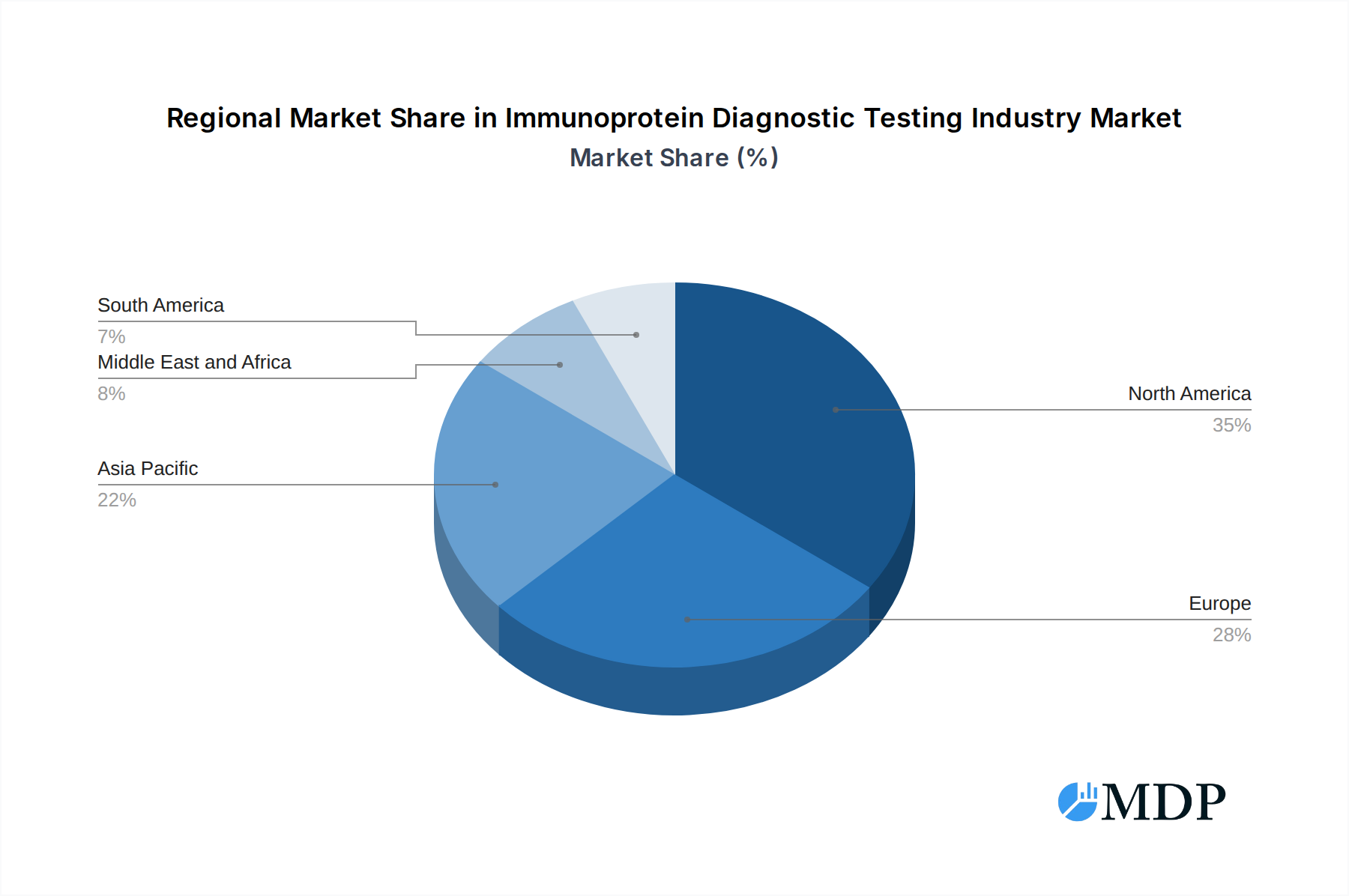

Key market drivers include the rising incidence of endocrine disorders, infectious diseases, and the increasing demand for toxicology screening in various settings. The market is segmented by product type into Instruments, Kits and Reagents, and Other Product Types, with Kits and Reagents likely to witness substantial growth due to their widespread use and disposable nature. Technological advancements are central to this market's evolution, with Chemiluminescence Assay, Immunofluorescence Assay, and Immunoturbidity Assay technologies at the forefront, driving innovation and adoption. Geographically, North America is expected to maintain a dominant position, driven by its advanced healthcare infrastructure and high adoption rates of new diagnostic technologies. However, the Asia Pacific region is anticipated to exhibit the fastest growth, propelled by improving healthcare access, a burgeoning middle class, and increasing government initiatives to bolster diagnostic capabilities. Key players like Thermo Fisher Scientific, Roche Diagnostics, and Abbott are actively investing in research and development, strategic partnerships, and market expansion to capitalize on these growth opportunities.

Immunoprotein Diagnostic Testing Industry Company Market Share

Gain unparalleled insights into the rapidly evolving Immunoprotein Diagnostic Testing Industry with our in-depth market research report. Spanning the comprehensive study period of 2019–2033, with a detailed analysis of the Base Year 2025 and Forecast Period 2025–2033, this report offers critical intelligence for stakeholders seeking to capitalize on this multi-billion dollar market. Discover key trends, emerging opportunities, and competitive landscapes impacting immunodiagnostics, protein assays, biomarker detection, and disease diagnostics. This report meticulously analyzes major players like Bio-Rad Laboratories Inc, Thermofisher Scientific Inc, F Hoffmann-La Roche Ltd, DiaSys Diagnostic Systems GmbH, Randox Laboratories, Diazyme Laboratories Inc, SERVA Electrophoresis GmbH, Abbott, Enzo Lifesciences Inc, and Calbiotech Inc, providing actionable insights for strategic decision-making in clinical chemistry, in vitro diagnostics (IVD), and point-of-care testing (POCT). We cover product types including Instruments, Kits and Reagents, and Other Product Types, alongside technologies such as Chemiluminescence Assay, Immunofluorescence Assay, Immunoturbidity Assay, Immunoprotein Electrophoresis, and Other Technologies. Applications are explored across Infectious Disease, Endocrine, Toxicology, and Other Applications.

Immunoprotein Diagnostic Testing Industry Market Dynamics & Concentration

The Immunoprotein Diagnostic Testing Industry is characterized by a moderate to high level of market concentration, with a few dominant players like Thermo Fisher Scientific Inc. and F Hoffmann-La Roche Ltd. holding significant market share, estimated to be approximately 35% combined. This concentration is driven by substantial R&D investments, extensive product portfolios, and established distribution networks. Innovation remains a primary driver, fueled by the increasing demand for early and accurate disease diagnosis, the development of novel biomarkers, and advancements in assay technologies like chemiluminescence and immunofluorescence. Regulatory frameworks, such as those established by the FDA and EMA, play a crucial role in market access and product development, with stringent approval processes for new diagnostic tests. Product substitutes, while present in broader diagnostic categories, are less impactful within the specialized realm of immunoprotein testing due to its unique ability to detect specific protein analytes. End-user trends highlight a growing preference for high-throughput, automated systems in clinical laboratories, alongside a rising interest in multiplexed assays for simultaneous detection of multiple immunoproteins. Merger and acquisition (M&A) activities are moderately active, with an estimated 15-20 significant deals occurring within the historical period 2019-2024, driven by companies seeking to expand their technological capabilities, product offerings, or geographical reach. For instance, strategic acquisitions often focus on companies with patented novel immunoassay technologies or specialized reagent development.

Immunoprotein Diagnostic Testing Industry Trends & Analysis

The Immunoprotein Diagnostic Testing Industry is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033. This expansion is significantly propelled by the increasing global prevalence of chronic diseases, such as autoimmune disorders and endocrine imbalances, which necessitate sophisticated diagnostic tools. Furthermore, the growing awareness of personalized medicine and the demand for early disease detection are acting as powerful catalysts for market penetration. Technological disruptions are at the forefront of this evolution, with advancements in assay sensitivity, specificity, and automation enhancing the diagnostic capabilities of immunoprotein tests. The integration of artificial intelligence (AI) and machine learning (ML) in data analysis and interpretation of assay results is also emerging as a transformative trend. Consumer preferences are increasingly shifting towards rapid and accurate diagnostic results, driving the demand for point-of-care (POC) testing solutions and user-friendly immunoassay platforms. The competitive dynamics within the industry are characterized by intense innovation, strategic partnerships, and ongoing product development to address unmet clinical needs. Companies are investing heavily in R&D to develop novel antibodies, optimize assay chemistries, and miniaturize instrumentation. The expanding use of immunoprotein diagnostics in infectious disease surveillance, particularly in the wake of global health crises, has further amplified market growth. Moreover, the development of highly sensitive tests for early detection of cancers and neurodegenerative diseases is expected to be a significant growth driver. The market penetration of advanced immunoprotein testing solutions is projected to exceed 65% by 2033, up from an estimated 40% in 2025, reflecting the increasing adoption across diverse healthcare settings.

Leading Markets & Segments in Immunoprotein Diagnostic Testing Industry

North America currently holds the dominant position in the global Immunoprotein Diagnostic Testing Industry, driven by robust healthcare infrastructure, high healthcare expenditure, and a strong emphasis on early disease detection and personalized medicine. The United States, in particular, is a key market, supported by a well-established regulatory framework, significant investments in research and development, and the presence of major industry players.

Product Type Dominance:

- Kits and Reagents: This segment is expected to exhibit the highest growth rate, driven by the increasing demand for consumable diagnostic components and the expansion of laboratory testing volumes. Key drivers include:

- Technological advancements leading to more sensitive and specific reagent formulations.

- The growing need for multiplexed assays capable of detecting multiple analytes simultaneously.

- The increasing outsourcing of diagnostic testing by healthcare providers.

- Instruments: While a mature segment, the demand for advanced automated immunoassay analyzers continues to grow, fueled by the need for higher throughput and improved efficiency in clinical laboratories. Drivers include:

- The development of compact and cost-effective instruments for point-of-care applications.

- Integration of sophisticated software for data management and analysis.

- Technological innovations in detection methods like enhanced chemiluminescence.

Technology Dominance:

- Chemiluminescence Assay: This technology leads the market due to its high sensitivity, broad dynamic range, and cost-effectiveness. Key drivers include:

- Continued innovation in luminescence substrates and enzyme-conjugate technologies.

- Suitability for high-throughput screening and a wide range of analytes.

- Integration into automated immunoassay platforms.

- Immunofluorescence Assay: This technology is gaining traction, particularly for autoimmune disease diagnostics and cell-based assays, due to its ability to visualize cellular localization of antigens. Drivers include:

- Advancements in fluorescent dyes and detection instrumentation.

- Growing applications in research and specialized clinical diagnostics.

Application Dominance:

- Infectious Disease: This segment is experiencing significant growth, amplified by the ongoing need for rapid and accurate detection of viral, bacterial, and fungal infections. Drivers include:

- The emergence of novel infectious agents and the need for rapid pandemic response diagnostics.

- The development of serological tests for monitoring immune status and vaccine efficacy.

- Increased screening for infectious diseases in pre-operative patients and blood donors.

- Endocrine: The rising incidence of endocrine disorders such as diabetes, thyroid disorders, and hormonal imbalances fuels sustained demand for immunoprotein testing in this application area. Drivers include:

- The need for precise monitoring of hormone levels and therapeutic effectiveness.

- Advancements in assays for detecting complex endocrine panels.

Immunoprotein Diagnostic Testing Industry Product Developments

The Immunoprotein Diagnostic Testing Industry is witnessing a surge in innovative product developments, primarily focused on enhancing assay sensitivity, specificity, and multiplexing capabilities. Companies are launching advanced immunoassay instruments designed for higher throughput and automation, alongside novel kits and reagents that enable the detection of a wider array of biomarkers with greater precision. Recent product innovations include the development of more rapid and user-friendly tests for infectious diseases and autoimmune disorders. These developments are crucial for improving diagnostic accuracy, enabling earlier disease intervention, and offering better patient outcomes. The competitive advantage lies in the ability to provide comprehensive diagnostic solutions that are cost-effective and seamlessly integrate into existing laboratory workflows, thereby capturing significant market share.

Key Drivers of Immunoprotein Diagnostic Testing Industry Growth

The Immunoprotein Diagnostic Testing Industry is propelled by several key growth drivers. The increasing global burden of chronic diseases, including autoimmune disorders and endocrine imbalances, necessitates precise diagnostic tools. Technological advancements, particularly in assay sensitivity and automation, are expanding the diagnostic capabilities and applications of immunoprotein tests. For example, the development of highly sensitive chemiluminescent assays allows for the detection of low-concentration biomarkers, crucial for early disease detection. Regulatory bodies worldwide are also encouraging the development and adoption of advanced diagnostic technologies to improve public health outcomes. Furthermore, the growing emphasis on personalized medicine and companion diagnostics is driving demand for targeted immunoprotein assays, enabling tailored treatment strategies for patients.

Challenges in the Immunoprotein Diagnostic Testing Industry Market

Despite its strong growth trajectory, the Immunoprotein Diagnostic Testing Industry faces several challenges. Stringent and evolving regulatory approval processes for new diagnostic tests can be time-consuming and costly, potentially delaying market entry for innovative products. The high cost of developing and manufacturing advanced immunoprotein assays and instruments can also pose a barrier to market accessibility, particularly in resource-limited settings. Intense competition among established players and emerging entrants leads to pricing pressures, impacting profit margins. Furthermore, the need for specialized training to operate complex instruments and interpret results can create a skilled workforce bottleneck, hindering widespread adoption. Ensuring consistent quality and supply chain reliability for critical reagents is also an ongoing concern.

Emerging Opportunities in Immunoprotein Diagnostic Testing Industry

The Immunoprotein Diagnostic Testing Industry is ripe with emerging opportunities, driven by significant technological breakthroughs and evolving healthcare paradigms. The increasing integration of artificial intelligence and machine learning with immunoassay platforms presents a substantial opportunity for enhanced data interpretation, predictive diagnostics, and improved workflow efficiency. The growing demand for point-of-care (POC) diagnostics opens avenues for developing miniaturized, user-friendly immunoprotein testing devices that can be used in diverse clinical settings, including remote areas. Strategic partnerships between diagnostic companies, pharmaceutical firms, and academic research institutions are poised to accelerate the development of novel biomarkers and companion diagnostics for targeted therapies. Furthermore, the expansion of emerging economies and the growing focus on public health initiatives offer significant market penetration opportunities for cost-effective and high-throughput immunoprotein diagnostic solutions.

Leading Players in the Immunoprotein Diagnostic Testing Industry Sector

- Bio-Rad Laboratories Inc

- Thermofisher Scientific Inc

- F Hoffmann-La Roche Ltd

- DiaSys Diagnostic Systems GmbH

- Randox Laboratories

- Diazyme Laboratories Inc

- SERVA Electrophoresis GmbH

- Abbott

- Enzo Lifesciences Inc

- Calbiotech Inc

Key Milestones in Immunoprotein Diagnostic Testing Industry Industry

- July 2022: KSL Beutner Laboratories launched a first-to-market Indirect Immunofluorescence (IIF) serum blood test in the US that positively identifies laminin 332, an antigen associated with the chronic, debilitating autoimmune disease mucous membrane pemphigoid (MMP). This innovation offers a significant advancement in the diagnosis of rare autoimmune conditions.

- April 2022: KSL Diagnostics, Inc launched a first-of-its-kind antibody test that detects an individual's immune response to COVID-19 and assesses the risk of infection when exposed. The COVID-19 Immune Index can help monitor the effectiveness of COVID-19 virus protection through a simple blood test, marking a crucial development in public health monitoring and vaccine efficacy assessment.

Strategic Outlook for Immunoprotein Diagnostic Testing Industry Market

The strategic outlook for the Immunoprotein Diagnostic Testing Industry is exceptionally promising, driven by continuous innovation and expanding applications. Future growth will likely be fueled by the development of more sophisticated multiplexing assays, enabling the simultaneous detection of numerous biomarkers from a single sample, thereby enhancing diagnostic efficiency and reducing costs. The increasing adoption of automation and artificial intelligence in laboratory diagnostics will further streamline workflows and improve accuracy. Furthermore, the growing demand for point-of-care immunoprotein testing solutions presents a significant opportunity for companies to expand their reach into underserved markets and decentralized healthcare settings. Strategic collaborations and partnerships will remain crucial for accelerating product development and market penetration, particularly in areas like oncology and neurodegenerative disease diagnostics.

Immunoprotein Diagnostic Testing Industry Segmentation

-

1. Product Type

- 1.1. Instruments

- 1.2. Kits and Reagents

- 1.3. Other Product Types

-

2. Technology

- 2.1. Chemiluminescence Assay

- 2.2. Immunofluorescence Assay

- 2.3. Immunoturbidity Assay

- 2.4. Immunoprotein Electrophoresis

- 2.5. Other Technologies

-

3. Application

- 3.1. Infectious Disease

- 3.2. Endocrine

- 3.3. Toxicology

- 3.4. Other Applications

Immunoprotein Diagnostic Testing Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Immunoprotein Diagnostic Testing Industry Regional Market Share

Geographic Coverage of Immunoprotein Diagnostic Testing Industry

Immunoprotein Diagnostic Testing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.88% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Instruments

- 5.1.2. Kits and Reagents

- 5.1.3. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Chemiluminescence Assay

- 5.2.2. Immunofluorescence Assay

- 5.2.3. Immunoturbidity Assay

- 5.2.4. Immunoprotein Electrophoresis

- 5.2.5. Other Technologies

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Infectious Disease

- 5.3.2. Endocrine

- 5.3.3. Toxicology

- 5.3.4. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Immunoprotein Diagnostic Testing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Instruments

- 6.1.2. Kits and Reagents

- 6.1.3. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Chemiluminescence Assay

- 6.2.2. Immunofluorescence Assay

- 6.2.3. Immunoturbidity Assay

- 6.2.4. Immunoprotein Electrophoresis

- 6.2.5. Other Technologies

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Infectious Disease

- 6.3.2. Endocrine

- 6.3.3. Toxicology

- 6.3.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Immunoprotein Diagnostic Testing Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Instruments

- 7.1.2. Kits and Reagents

- 7.1.3. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Chemiluminescence Assay

- 7.2.2. Immunofluorescence Assay

- 7.2.3. Immunoturbidity Assay

- 7.2.4. Immunoprotein Electrophoresis

- 7.2.5. Other Technologies

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Infectious Disease

- 7.3.2. Endocrine

- 7.3.3. Toxicology

- 7.3.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Immunoprotein Diagnostic Testing Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Instruments

- 8.1.2. Kits and Reagents

- 8.1.3. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Chemiluminescence Assay

- 8.2.2. Immunofluorescence Assay

- 8.2.3. Immunoturbidity Assay

- 8.2.4. Immunoprotein Electrophoresis

- 8.2.5. Other Technologies

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Infectious Disease

- 8.3.2. Endocrine

- 8.3.3. Toxicology

- 8.3.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Immunoprotein Diagnostic Testing Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Instruments

- 9.1.2. Kits and Reagents

- 9.1.3. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Chemiluminescence Assay

- 9.2.2. Immunofluorescence Assay

- 9.2.3. Immunoturbidity Assay

- 9.2.4. Immunoprotein Electrophoresis

- 9.2.5. Other Technologies

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Infectious Disease

- 9.3.2. Endocrine

- 9.3.3. Toxicology

- 9.3.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Middle East and Africa Immunoprotein Diagnostic Testing Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Instruments

- 10.1.2. Kits and Reagents

- 10.1.3. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. Chemiluminescence Assay

- 10.2.2. Immunofluorescence Assay

- 10.2.3. Immunoturbidity Assay

- 10.2.4. Immunoprotein Electrophoresis

- 10.2.5. Other Technologies

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Infectious Disease

- 10.3.2. Endocrine

- 10.3.3. Toxicology

- 10.3.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. South America Immunoprotein Diagnostic Testing Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Instruments

- 11.1.2. Kits and Reagents

- 11.1.3. Other Product Types

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. Chemiluminescence Assay

- 11.2.2. Immunofluorescence Assay

- 11.2.3. Immunoturbidity Assay

- 11.2.4. Immunoprotein Electrophoresis

- 11.2.5. Other Technologies

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Infectious Disease

- 11.3.2. Endocrine

- 11.3.3. Toxicology

- 11.3.4. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bio-Rad Laboratories Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Thermofisher Scientific Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 F Hoffmann-La Roche Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DiaSys Diagnostic Systems GmbH

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Randox Laboratories

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Diazyme Laboratories Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 SERVA Electrophoresis GmbH

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Abbott

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Enzo Lifesciences Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Calbiotech Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Bio-Rad Laboratories Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Immunoprotein Diagnostic Testing Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Immunoprotein Diagnostic Testing Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Immunoprotein Diagnostic Testing Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 4: North America Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 5: North America Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Immunoprotein Diagnostic Testing Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 7: North America Immunoprotein Diagnostic Testing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 8: North America Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 9: North America Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: North America Immunoprotein Diagnostic Testing Industry Volume Share (%), by Technology 2025 & 2033

- Figure 11: North America Immunoprotein Diagnostic Testing Industry Revenue (Million), by Application 2025 & 2033

- Figure 12: North America Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Application 2025 & 2033

- Figure 13: North America Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: North America Immunoprotein Diagnostic Testing Industry Volume Share (%), by Application 2025 & 2033

- Figure 15: North America Immunoprotein Diagnostic Testing Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Immunoprotein Diagnostic Testing Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Immunoprotein Diagnostic Testing Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 20: Europe Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 21: Europe Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: Europe Immunoprotein Diagnostic Testing Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 23: Europe Immunoprotein Diagnostic Testing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 24: Europe Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 25: Europe Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 26: Europe Immunoprotein Diagnostic Testing Industry Volume Share (%), by Technology 2025 & 2033

- Figure 27: Europe Immunoprotein Diagnostic Testing Industry Revenue (Million), by Application 2025 & 2033

- Figure 28: Europe Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Application 2025 & 2033

- Figure 29: Europe Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Immunoprotein Diagnostic Testing Industry Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Immunoprotein Diagnostic Testing Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Immunoprotein Diagnostic Testing Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Immunoprotein Diagnostic Testing Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 36: Asia Pacific Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 37: Asia Pacific Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: Asia Pacific Immunoprotein Diagnostic Testing Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 39: Asia Pacific Immunoprotein Diagnostic Testing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 40: Asia Pacific Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 41: Asia Pacific Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 42: Asia Pacific Immunoprotein Diagnostic Testing Industry Volume Share (%), by Technology 2025 & 2033

- Figure 43: Asia Pacific Immunoprotein Diagnostic Testing Industry Revenue (Million), by Application 2025 & 2033

- Figure 44: Asia Pacific Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Application 2025 & 2033

- Figure 45: Asia Pacific Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: Asia Pacific Immunoprotein Diagnostic Testing Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: Asia Pacific Immunoprotein Diagnostic Testing Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Immunoprotein Diagnostic Testing Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Immunoprotein Diagnostic Testing Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 52: Middle East and Africa Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 53: Middle East and Africa Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 54: Middle East and Africa Immunoprotein Diagnostic Testing Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 55: Middle East and Africa Immunoprotein Diagnostic Testing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 56: Middle East and Africa Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 57: Middle East and Africa Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 58: Middle East and Africa Immunoprotein Diagnostic Testing Industry Volume Share (%), by Technology 2025 & 2033

- Figure 59: Middle East and Africa Immunoprotein Diagnostic Testing Industry Revenue (Million), by Application 2025 & 2033

- Figure 60: Middle East and Africa Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Application 2025 & 2033

- Figure 61: Middle East and Africa Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 62: Middle East and Africa Immunoprotein Diagnostic Testing Industry Volume Share (%), by Application 2025 & 2033

- Figure 63: Middle East and Africa Immunoprotein Diagnostic Testing Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Middle East and Africa Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Immunoprotein Diagnostic Testing Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Immunoprotein Diagnostic Testing Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 68: South America Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Product Type 2025 & 2033

- Figure 69: South America Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 70: South America Immunoprotein Diagnostic Testing Industry Volume Share (%), by Product Type 2025 & 2033

- Figure 71: South America Immunoprotein Diagnostic Testing Industry Revenue (Million), by Technology 2025 & 2033

- Figure 72: South America Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 73: South America Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 74: South America Immunoprotein Diagnostic Testing Industry Volume Share (%), by Technology 2025 & 2033

- Figure 75: South America Immunoprotein Diagnostic Testing Industry Revenue (Million), by Application 2025 & 2033

- Figure 76: South America Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Application 2025 & 2033

- Figure 77: South America Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Application 2025 & 2033

- Figure 78: South America Immunoprotein Diagnostic Testing Industry Volume Share (%), by Application 2025 & 2033

- Figure 79: South America Immunoprotein Diagnostic Testing Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: South America Immunoprotein Diagnostic Testing Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Immunoprotein Diagnostic Testing Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Immunoprotein Diagnostic Testing Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 3: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 4: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 5: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 7: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 10: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 11: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 12: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 13: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 14: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 15: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 24: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 25: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 26: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 27: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 29: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: France Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Italy Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Spain Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 44: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 45: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 46: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 47: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 48: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 49: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: China Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Japan Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: India Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Australia Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: South Korea Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 64: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 65: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 66: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 67: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 68: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 69: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: GCC Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: South Africa Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 78: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Product Type 2020 & 2033

- Table 79: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 80: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 81: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 82: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 83: Global Immunoprotein Diagnostic Testing Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 84: Global Immunoprotein Diagnostic Testing Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: Brazil Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: Argentina Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Immunoprotein Diagnostic Testing Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Immunoprotein Diagnostic Testing Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Immunoprotein Diagnostic Testing Industry?

The projected CAGR is approximately 5.88%.

2. Which companies are prominent players in the Immunoprotein Diagnostic Testing Industry?

Key companies in the market include Bio-Rad Laboratories Inc, Thermofisher Scientific Inc , F Hoffmann-La Roche Ltd, DiaSys Diagnostic Systems GmbH, Randox Laboratories, Diazyme Laboratories Inc, SERVA Electrophoresis GmbH, Abbott, Enzo Lifesciences Inc, Calbiotech Inc.

3. What are the main segments of the Immunoprotein Diagnostic Testing Industry?

The market segments include Product Type, Technology, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.04 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Prevalence of Chronic Diseases; Technological Advancements of Products.

6. What are the notable trends driving market growth?

Endocrine Segment is Expected to Hold a Significant Share in the Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

Expenisive Techniques.

8. Can you provide examples of recent developments in the market?

July 2022: KSL Beutner Laboratories launched a first-to-market Indirect Immunofluorescence (IIF) serum blood test in the US that positively identifies laminin 332, an antigen associated with the chronic, debilitating autoimmune disease mucous membrane pemphigoid (MMP).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Immunoprotein Diagnostic Testing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Immunoprotein Diagnostic Testing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Immunoprotein Diagnostic Testing Industry?

To stay informed about further developments, trends, and reports in the Immunoprotein Diagnostic Testing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence