Key Insights

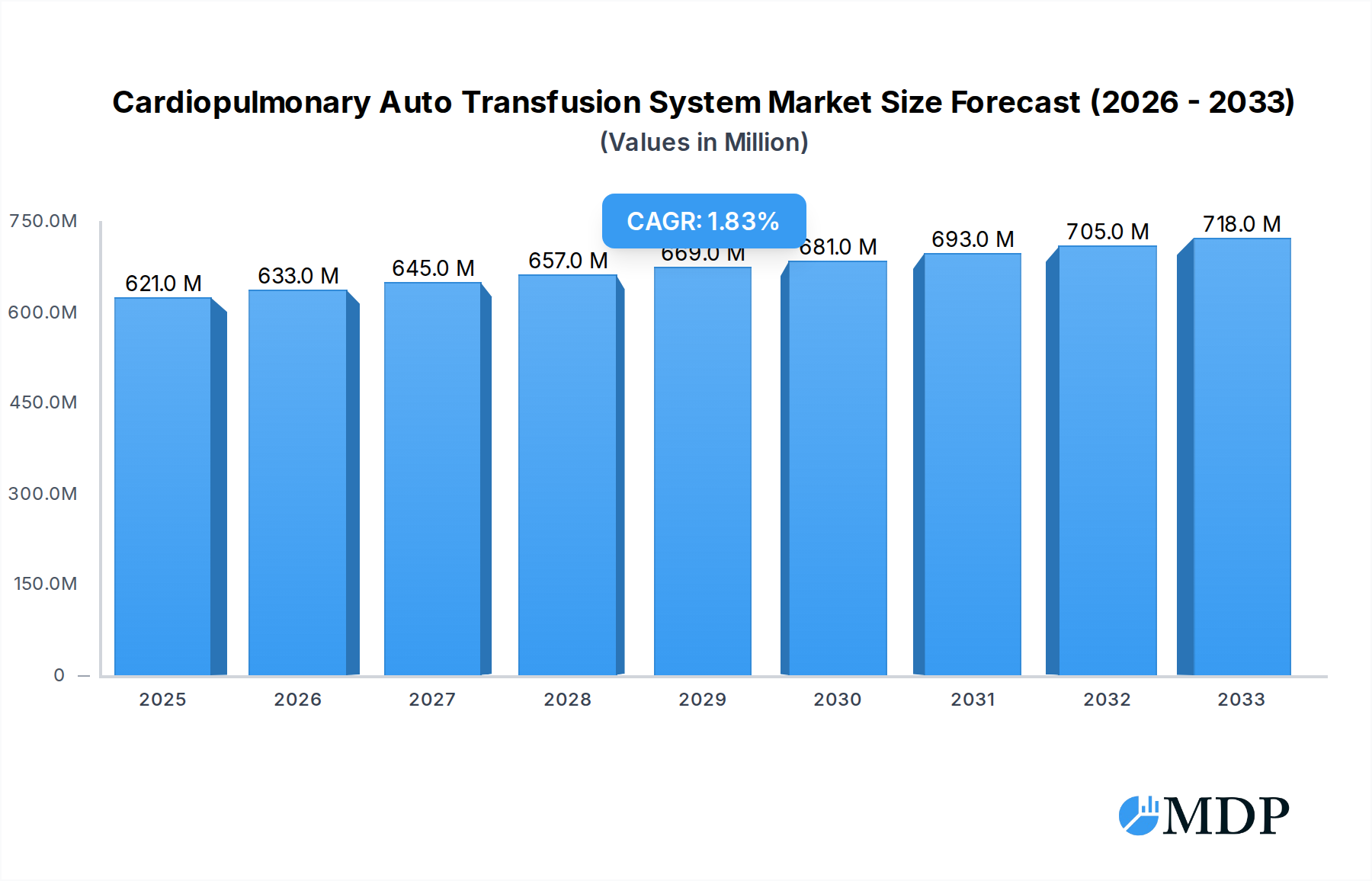

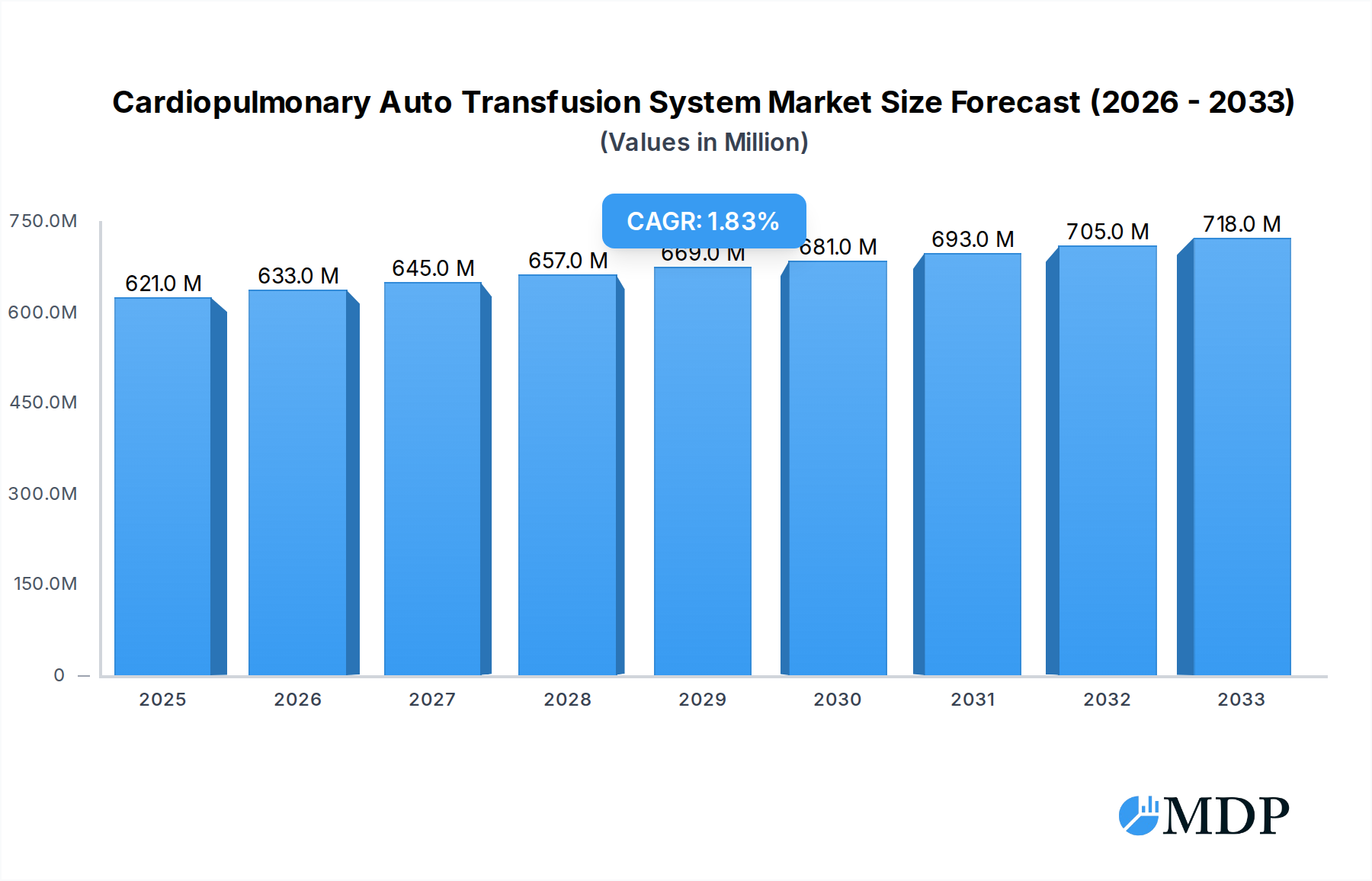

The global Cardiopulmonary Auto Transfusion System market is projected to reach $621 million by 2025, exhibiting a modest Compound Annual Growth Rate (CAGR) of 1.9% during the forecast period of 2025-2033. This steady growth is underpinned by increasing cardiovascular surgical procedures worldwide, a rising prevalence of cardiac diseases, and a growing awareness of the benefits of intraoperative blood salvage. Auto-transfusion systems play a crucial role in minimizing allogeneic blood transfusions, thereby reducing risks such as transfusion-transmitted infections and alloimmunization, which are significant concerns in complex surgeries. The demand for these systems is further bolstered by advancements in technology, leading to more efficient and user-friendly devices that enhance patient safety and optimize blood management strategies in critical care settings.

Cardiopulmonary Auto Transfusion System Market Size (In Million)

The market is segmented into On-Pump and Off-Pump Transfusion Devices, with the On-Pump Transfusion Device segment currently holding a larger share due to its integration with cardiopulmonary bypass procedures. Key applications include Hospitals and Ambulatory Surgical Centers, with hospitals accounting for the majority of the market due to the concentration of complex cardiac surgeries. While the market's growth is steady, potential restraints such as the high initial cost of sophisticated auto-transfusion systems and the availability of alternative blood management techniques could pose challenges. However, the increasing focus on patient blood management programs and the pursuit of cost-effectiveness in healthcare are expected to drive sustained adoption and innovation in this vital medical device sector, particularly in regions with advanced healthcare infrastructure like North America and Europe.

Cardiopulmonary Auto Transfusion System Company Market Share

Unveiling the Future: Cardiopulmonary Auto Transfusion System Market Analysis 2019-2033

[Report Title]: Cardiopulmonary Auto Transfusion System Market: Dynamics, Trends, and Strategic Outlook (2019–2033)

[Report Description]: This comprehensive report provides an in-depth analysis of the global Cardiopulmonary Auto Transfusion System market, a critical component in modern cardiac surgery. Covering the historical period of 2019-2024, the base year of 2025, and an extensive forecast period through 2033, this study offers invaluable insights into market dynamics, technological advancements, regional dominance, and key player strategies. With an estimated market size projected to reach several hundred million dollars in the coming years, this report is an essential resource for medical device manufacturers, healthcare providers, investors, and industry stakeholders seeking to navigate and capitalize on this growing sector. Discover market concentration, innovation drivers, evolving end-user trends, and the impact of regulatory frameworks on this vital medical technology. Gain a deep understanding of industry-wide trends, including market penetration, CAGR, and the influence of technological disruptions on consumer preferences. Identify leading markets and segments, with a focus on the dominance of Hospitals and On-Pump Transfusion Devices, and explore the strategic advantages and product developments shaping the competitive landscape. This report details key growth drivers, challenges, and emerging opportunities, providing a strategic outlook for sustained market growth.

Cardiopulmonary Auto Transfusion System Market Dynamics & Concentration

The Cardiopulmonary Auto Transfusion System market exhibits a moderate level of concentration, with a few prominent players holding significant market share. Haemonetics and Medtronic are recognized leaders, followed by LivaNova and Fresenius, each contributing substantially to the global market value, estimated to be in the hundreds of millions of dollars annually. Innovation drivers are primarily fueled by the increasing demand for minimally invasive cardiac procedures, a growing preference for autologous blood transfusion to mitigate risks associated with allogeneic transfusions, and advancements in device technology leading to enhanced efficiency and patient safety. Regulatory frameworks, particularly those enforced by the FDA and EMA, play a crucial role in shaping product development and market access, ensuring stringent quality and safety standards. While direct product substitutes are limited, advancements in blood management strategies and alternative hemostasis techniques present indirect competitive pressures. End-user trends highlight a growing adoption in large hospitals performing a high volume of cardiac surgeries, as well as increasing interest from specialized Ambulatory Surgical Centers. Mergers and Acquisitions (M&A) activities are infrequent but strategic, aimed at consolidating market presence, acquiring innovative technologies, or expanding product portfolios. The M&A deal count remains low, typically in the single digits annually, reflecting the specialized nature of the market.

Cardiopulmonary Auto Transfusion System Industry Trends & Analysis

The Cardiopulmonary Auto Transfusion System market is poised for robust growth, driven by a confluence of factors that underscore its increasing importance in cardiovascular surgery. The market is expected to witness a healthy Compound Annual Growth Rate (CAGR) of approximately 5-7% over the forecast period. This upward trajectory is primarily fueled by the escalating prevalence of cardiovascular diseases globally, necessitating more frequent and complex cardiac surgical interventions. As the aging population grows, so does the incidence of conditions requiring procedures like coronary artery bypass grafting and valve replacements, thereby amplifying the demand for cardiopulmonary bypass and autotransfusion systems.

Technological disruptions are a significant trend, with manufacturers continuously innovating to enhance the efficacy and safety of these systems. Key developments include the integration of advanced sensors for real-time blood parameter monitoring, improved filtration technologies for higher quality blood recovery, and more user-friendly interfaces for surgical teams. The shift towards minimally invasive surgical techniques, while reducing blood loss, still necessitates efficient blood management solutions, and autotransfusion systems are crucial in this regard.

Consumer preferences are increasingly leaning towards solutions that minimize patient risks and optimize recovery times. Autologous blood transfusions, facilitated by these systems, are favored due to the reduced risk of transfusion reactions, disease transmission, and alloimmunization compared to allogeneic blood. This preference directly translates into higher demand for cardiopulmonary auto transfusion systems. Furthermore, a growing awareness among healthcare providers and patients about the benefits of blood conservation strategies is a significant market penetrator. The market penetration of these systems is steadily increasing, especially in developed economies, but there is substantial room for growth in emerging markets.

Competitive dynamics are characterized by a focus on product differentiation, technological innovation, and strategic partnerships. Companies are investing heavily in research and development to offer systems with superior performance, cost-effectiveness, and ease of use. The market landscape, while having dominant players, also sees emerging companies striving to carve out niches through specialized product offerings or advanced technological capabilities. The ongoing quest for improved patient outcomes and reduced healthcare costs continues to shape the competitive strategies, pushing for more integrated and intelligent cardiopulmonary auto transfusion solutions. The overall market size is projected to reach several hundred million dollars by the end of the forecast period, reflecting sustained demand and technological advancements.

Leading Markets & Segments in Cardiopulmonary Auto Transfusion System

The global Cardiopulmonary Auto Transfusion System market is segmented by application and device type, with distinct regional influences driving demand. Hospitals represent the largest and most dominant application segment, accounting for an estimated 70-75% of the market share. This dominance is attributable to the concentration of complex cardiac surgeries, specialized surgical teams, and advanced infrastructure required for these procedures. Major cardiac surgery centers within leading economies consistently drive the demand for these sophisticated systems.

Within the hospital segment, the On-Pump Transfusion Device category is the primary revenue generator, representing approximately 60-65% of the market. This is directly linked to the prevalence of traditional open-heart surgeries that necessitate cardiopulmonary bypass. The efficiency and established protocols surrounding on-pump procedures ensure a steady demand for associated autotransfusion systems.

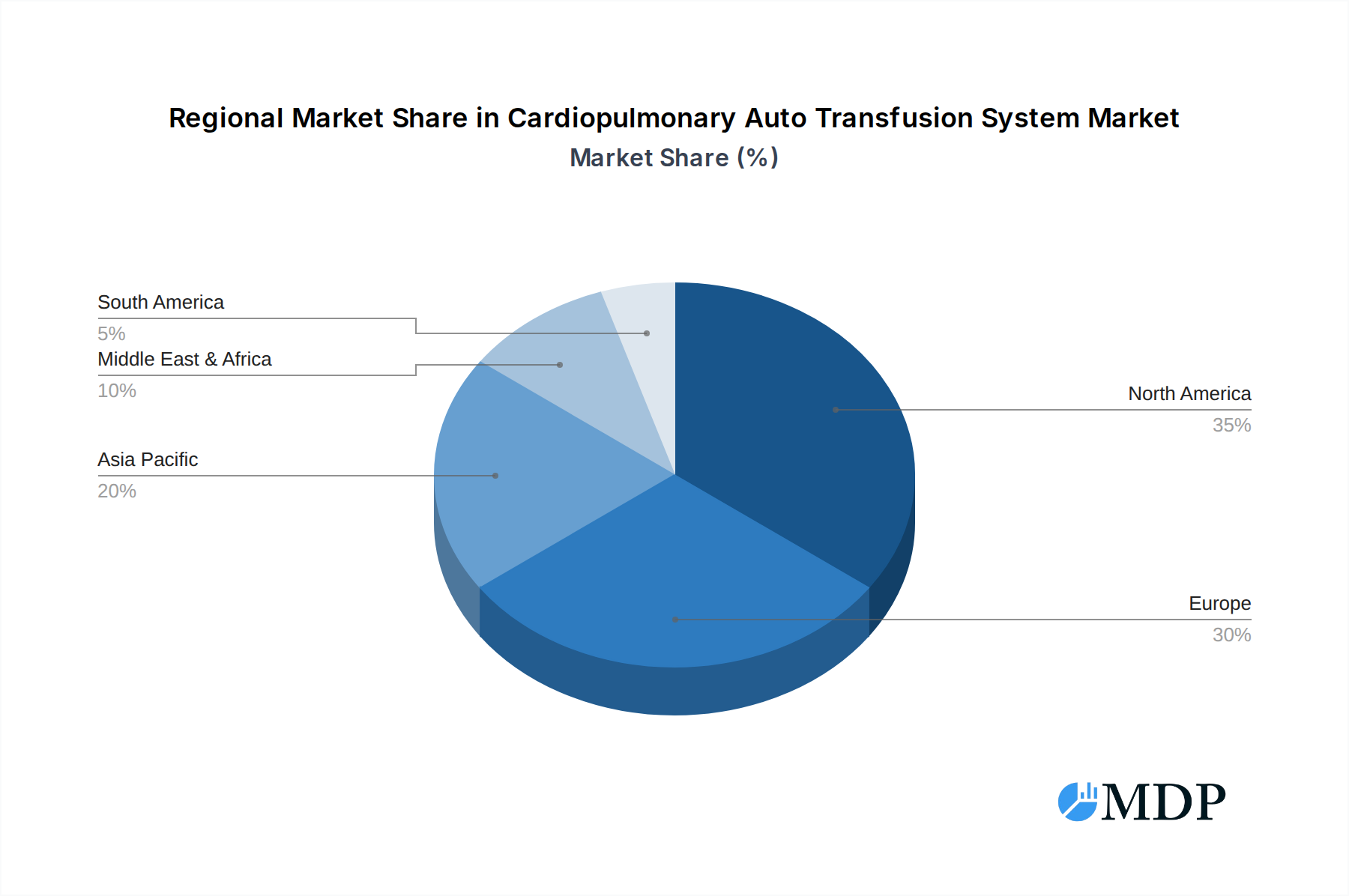

Geographically, North America is the leading market, contributing an estimated 35-40% to the global market revenue. This leadership is propelled by several factors:

- High prevalence of cardiovascular diseases: The region has one of the highest rates of heart disease globally, leading to a substantial volume of cardiac surgeries.

- Advanced healthcare infrastructure: Robust hospital networks, availability of skilled cardiac surgeons and perfusionists, and widespread adoption of cutting-edge medical technologies contribute to market leadership.

- Favorable reimbursement policies: Supportive insurance and reimbursement frameworks for complex surgical procedures and blood management techniques encourage the use of advanced autotransfusion systems.

- Significant R&D investment: Strong investment in medical research and development by both public and private entities drives innovation and the adoption of new technologies.

The United States is the single largest country market within North America, spearheading adoption and technological advancements. Other significant contributors to the global market include Europe (particularly Germany, the UK, and France) and, increasingly, Asia-Pacific, driven by a growing middle class, expanding healthcare access, and rising incidence of lifestyle-related diseases.

The Ambulatory Surgical Centers segment, while smaller, is experiencing a notable growth rate, estimated at 8-10% CAGR. This segment is expected to capture 15-20% of the market share by 2033, driven by the increasing trend of performing certain cardiac procedures in outpatient settings, offering cost-effectiveness and convenience for select patient populations. The adoption of Off-Pump Transfusion Device technology is also projected to witness significant growth within this segment, reflecting the increasing preference for less invasive surgical approaches.

The "Others" application segment, encompassing specialized cardiac clinics and research institutions, constitutes the remaining market share but plays a crucial role in early adoption and validation of new technologies. The interplay of these segments and regions, coupled with evolving surgical techniques, will continue to shape the market landscape for cardiopulmonary auto transfusion systems.

Cardiopulmonary Auto Transfusion System Product Developments

Product development in the Cardiopulmonary Auto Transfusion System sector is intensely focused on enhancing blood recovery efficiency, improving blood quality post-processing, and ensuring seamless integration with existing surgical workflows. Innovations include the development of more sophisticated filtration membranes to remove micro-aggregates and inflammatory mediators, as well as advanced anticoagulation management systems that optimize circuit performance while minimizing bleeding risks. Companies are also introducing more compact and ergonomic designs for easier handling in the operating room. Competitive advantages are being carved out through enhanced automation, real-time data analytics for better decision-making, and a stronger emphasis on disposables with improved biocompatibility and reduced allergenic potential, aiming for a total market value of several hundred million dollars.

Key Drivers of Cardiopulmonary Auto Transfusion System Growth

Several pivotal factors are driving the growth of the Cardiopulmonary Auto Transfusion System market. Firstly, the increasing global burden of cardiovascular diseases, leading to a rise in complex cardiac surgeries, is a primary demand generator. Secondly, technological advancements in device design, including improved filtration and automation, are enhancing product efficacy and patient safety, encouraging wider adoption. Thirdly, a growing emphasis on blood conservation strategies and the inherent benefits of autologous blood transfusion over allogeneic transfusions – such as reduced risks of transfusion reactions and disease transmission – are compelling factors for healthcare providers. Furthermore, supportive regulatory environments in key markets and increasing healthcare expenditure globally are facilitating market expansion.

Challenges in the Cardiopulmonary Auto Transfusion System Market

Despite its growth potential, the Cardiopulmonary Auto Transfusion System market faces several challenges. Stringent regulatory approval processes in various countries can lead to extended product launch timelines and increased development costs, estimated to be in the millions of dollars per approval. The high initial investment cost for sophisticated autotransfusion systems can be a barrier for smaller healthcare facilities in resource-limited regions, impacting market penetration. Supply chain complexities and the need for specialized training for operating room personnel to effectively utilize these systems also pose ongoing challenges. Moreover, the development and increasing adoption of alternative hemostasis techniques and advanced blood management protocols may present indirect competitive pressures.

Emerging Opportunities in Cardiopulmonary Auto Transfusion System

The Cardiopulmonary Auto Transfusion System market is ripe with emerging opportunities driven by technological innovation and evolving healthcare paradigms. The growing trend towards minimally invasive cardiac surgery presents an opportunity for the development of more compact and integrated autotransfusion systems that complement these approaches. Expansion into emerging economies, where the incidence of cardiovascular diseases is rising and healthcare infrastructure is developing, offers significant untapped market potential, estimated to contribute hundreds of millions of dollars in future revenue. Strategic partnerships between device manufacturers and academic institutions for advanced research in blood recovery and processing techniques can lead to groundbreaking innovations. Furthermore, the increasing focus on patient blood management programs within hospitals creates a demand for comprehensive autotransfusion solutions, fostering opportunities for bundled offerings and value-added services.

Leading Players in the Cardiopulmonary Auto Transfusion System Sector

- Haemonetics

- Medtronic

- LivaNova

- Fresenius

- Terumo Interventional Systems

- Wandong Health Sources

Key Milestones in Cardiopulmonary Auto Transfusion System Industry

- 2019: Introduction of next-generation autotransfusion devices with enhanced filtration capabilities, improving blood product quality.

- 2020: Increased focus on automation and digital integration within cardiopulmonary bypass circuits, leading to more efficient autotransfusion processes.

- 2021: Launch of advanced disposable kits with improved biocompatibility and reduced allergenic potential.

- 2022: Significant regulatory approvals for novel autotransfusion technologies in key European markets.

- 2023: Strategic collaborations for expanding autotransfusion system adoption in emerging markets, projected to add millions of dollars in revenue.

- 2024: Emergence of AI-driven analytics for real-time blood parameter monitoring and optimization during cardiac surgery.

Strategic Outlook for Cardiopulmonary Auto Transfusion System Market

The strategic outlook for the Cardiopulmonary Auto Transfusion System market remains exceptionally positive, driven by sustained demand for cardiac surgeries and continuous technological advancements. Key growth accelerators include the expansion of minimally invasive procedures, which will necessitate streamlined and integrated blood management solutions. Future market development will likely witness a greater emphasis on smart devices with advanced data analytics for real-time decision support and personalized patient care. Strategic opportunities lie in penetrating emerging markets by offering cost-effective and user-friendly autotransfusion systems, alongside robust training and support programs. Furthermore, fostering collaborations for research and development into next-generation blood recovery and processing technologies will be crucial for maintaining a competitive edge and capturing a larger share of the projected hundreds of millions of dollars global market.

Cardiopulmonary Auto Transfusion System Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Ambulatory Surgical Centers

- 1.3. Others

-

2. Type

- 2.1. On-Pump Transfusion Device

- 2.2. Off-Pump Transfusion Device

Cardiopulmonary Auto Transfusion System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cardiopulmonary Auto Transfusion System Regional Market Share

Geographic Coverage of Cardiopulmonary Auto Transfusion System

Cardiopulmonary Auto Transfusion System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cardiopulmonary Auto Transfusion System Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Ambulatory Surgical Centers

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. On-Pump Transfusion Device

- 5.2.2. Off-Pump Transfusion Device

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Cardiopulmonary Auto Transfusion System Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Ambulatory Surgical Centers

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. On-Pump Transfusion Device

- 6.2.2. Off-Pump Transfusion Device

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Cardiopulmonary Auto Transfusion System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Ambulatory Surgical Centers

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. On-Pump Transfusion Device

- 7.2.2. Off-Pump Transfusion Device

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Cardiopulmonary Auto Transfusion System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Ambulatory Surgical Centers

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. On-Pump Transfusion Device

- 8.2.2. Off-Pump Transfusion Device

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Cardiopulmonary Auto Transfusion System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Ambulatory Surgical Centers

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. On-Pump Transfusion Device

- 9.2.2. Off-Pump Transfusion Device

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Cardiopulmonary Auto Transfusion System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Ambulatory Surgical Centers

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. On-Pump Transfusion Device

- 10.2.2. Off-Pump Transfusion Device

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Haemonetics

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Medtronic

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 LivaNova

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Fresenius

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Terumo Interventional Systems

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Wandong Health Sources

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.1 Haemonetics

List of Figures

- Figure 1: Global Cardiopulmonary Auto Transfusion System Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Cardiopulmonary Auto Transfusion System Revenue (million), by Application 2025 & 2033

- Figure 3: North America Cardiopulmonary Auto Transfusion System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cardiopulmonary Auto Transfusion System Revenue (million), by Type 2025 & 2033

- Figure 5: North America Cardiopulmonary Auto Transfusion System Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Cardiopulmonary Auto Transfusion System Revenue (million), by Country 2025 & 2033

- Figure 7: North America Cardiopulmonary Auto Transfusion System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cardiopulmonary Auto Transfusion System Revenue (million), by Application 2025 & 2033

- Figure 9: South America Cardiopulmonary Auto Transfusion System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cardiopulmonary Auto Transfusion System Revenue (million), by Type 2025 & 2033

- Figure 11: South America Cardiopulmonary Auto Transfusion System Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Cardiopulmonary Auto Transfusion System Revenue (million), by Country 2025 & 2033

- Figure 13: South America Cardiopulmonary Auto Transfusion System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cardiopulmonary Auto Transfusion System Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Cardiopulmonary Auto Transfusion System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cardiopulmonary Auto Transfusion System Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Cardiopulmonary Auto Transfusion System Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Cardiopulmonary Auto Transfusion System Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Cardiopulmonary Auto Transfusion System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cardiopulmonary Auto Transfusion System Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cardiopulmonary Auto Transfusion System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cardiopulmonary Auto Transfusion System Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Cardiopulmonary Auto Transfusion System Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Cardiopulmonary Auto Transfusion System Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cardiopulmonary Auto Transfusion System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cardiopulmonary Auto Transfusion System Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Cardiopulmonary Auto Transfusion System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cardiopulmonary Auto Transfusion System Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Cardiopulmonary Auto Transfusion System Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Cardiopulmonary Auto Transfusion System Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Cardiopulmonary Auto Transfusion System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Cardiopulmonary Auto Transfusion System Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cardiopulmonary Auto Transfusion System Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cardiopulmonary Auto Transfusion System?

The projected CAGR is approximately 1.9%.

2. Which companies are prominent players in the Cardiopulmonary Auto Transfusion System?

Key companies in the market include Haemonetics, Medtronic, LivaNova, Fresenius, Terumo Interventional Systems, Wandong Health Sources.

3. What are the main segments of the Cardiopulmonary Auto Transfusion System?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 621 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cardiopulmonary Auto Transfusion System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cardiopulmonary Auto Transfusion System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cardiopulmonary Auto Transfusion System?

To stay informed about further developments, trends, and reports in the Cardiopulmonary Auto Transfusion System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence