Key Insights

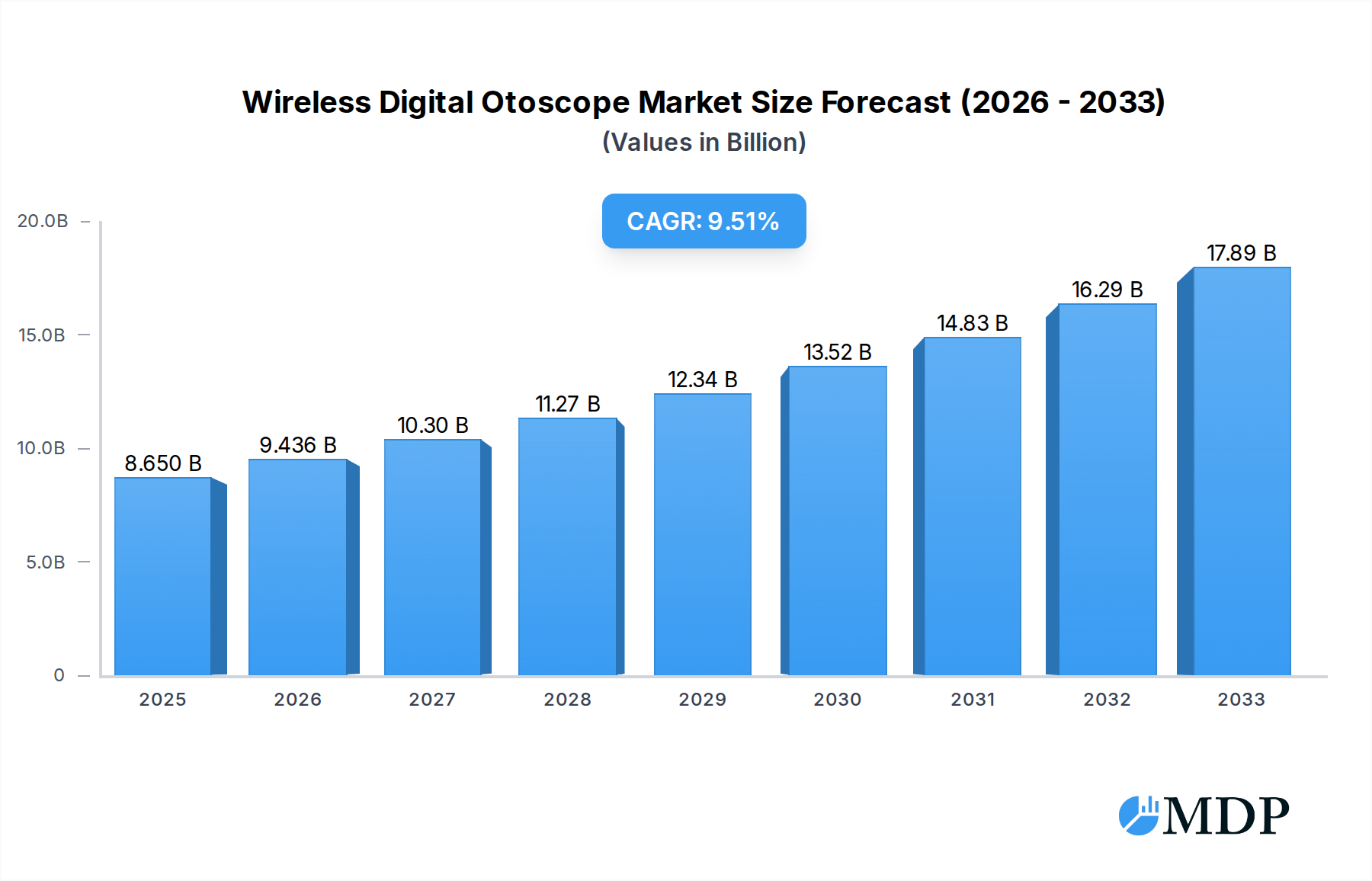

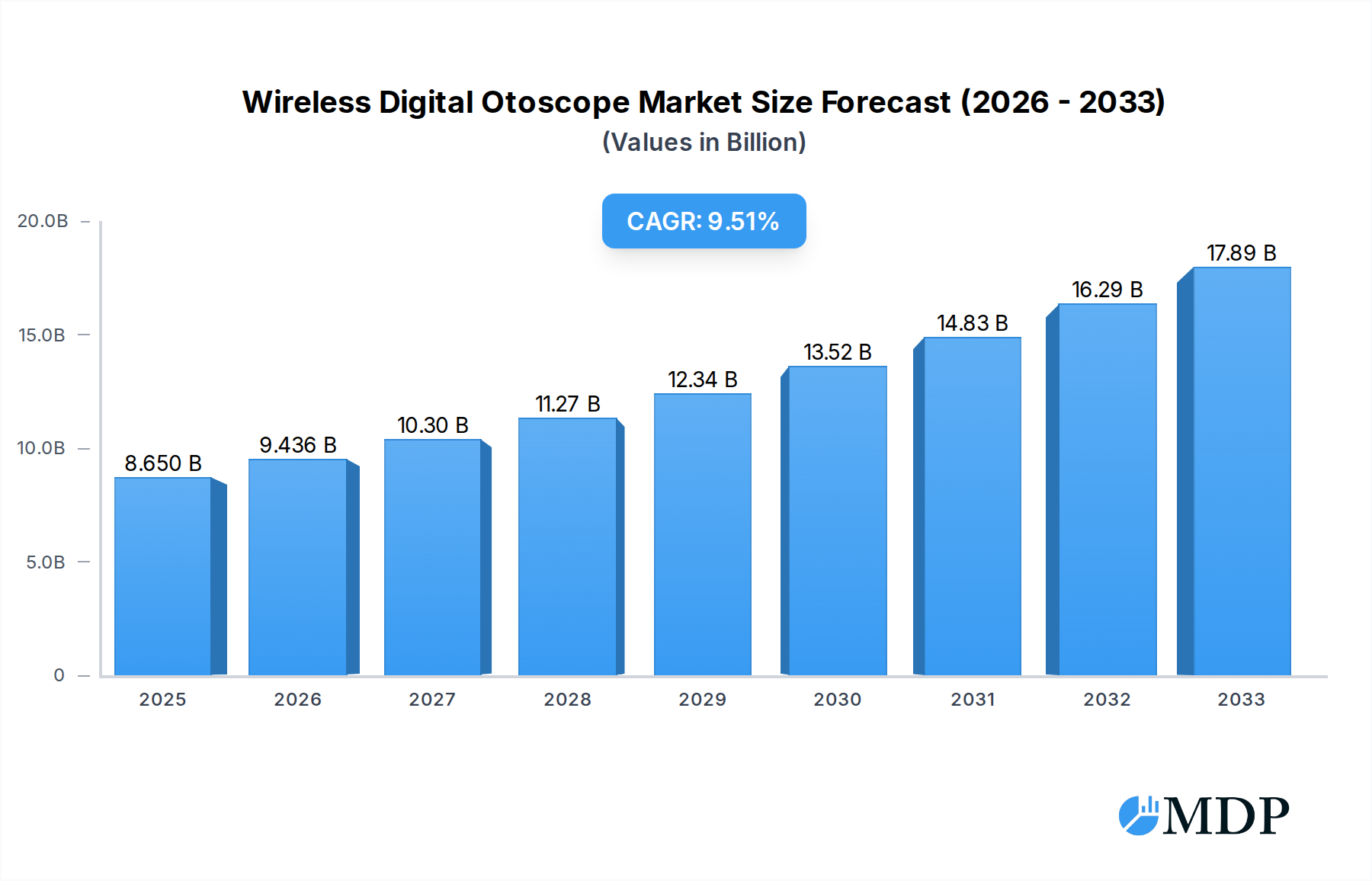

The global Wireless Digital Otoscope market is poised for significant expansion, driven by increasing healthcare accessibility and technological advancements in diagnostic tools. The market is projected to reach a valuation of USD 8.65 billion in 2025, demonstrating robust growth with a Compound Annual Growth Rate (CAGR) of 9.17% during the forecast period of 2025-2033. This upward trajectory is fueled by the growing demand for minimally invasive diagnostic procedures, enhanced visualization capabilities offered by digital otoscopes, and the rising prevalence of ear-related infections and hearing disorders worldwide. The integration of wireless connectivity and advanced imaging technologies allows for remote consultations, improved documentation, and greater efficiency in clinical settings, thereby accelerating market adoption across hospitals, ENT clinics, and even home healthcare environments.

Wireless Digital Otoscope Market Size (In Billion)

The market's growth will be further propelled by an increasing focus on early disease detection and proactive ear health management. Innovations in rechargeable battery technology are enhancing portability and user convenience, while the expanding application in telemedicine underscores the market's adaptability to evolving healthcare delivery models. Key market drivers include the increasing disposable income in emerging economies, leading to greater investment in advanced medical equipment, and supportive government initiatives promoting digital health infrastructure. While challenges such as the initial cost of sophisticated devices and the need for robust data security protocols exist, the overarching trend towards telemedicine and the continuous improvement in digital otoscope functionality suggest a promising future for this dynamic market segment.

Wireless Digital Otoscope Company Market Share

Unlocking the Future of Ear Diagnostics: Wireless Digital Otoscope Market Insights 2025-2033

This comprehensive report provides an in-depth analysis of the global Wireless Digital Otoscope market, a rapidly evolving sector poised for significant expansion. Covering the historical period from 2019 to 2024 and projecting growth through 2033 with a base year of 2025, this study delves into market dynamics, emerging trends, leading segments, product innovations, growth drivers, challenges, and strategic opportunities. We meticulously examine key players and pivotal milestones that are shaping the landscape of remote and enhanced otoscopic examinations, offering actionable intelligence for industry stakeholders.

Wireless Digital Otoscope Market Dynamics & Concentration

The Wireless Digital Otoscope market exhibits a moderate to high concentration, with several established medical device manufacturers and emerging technology companies vying for market share. Major players like Heine Optotechnik, Welch Allyn, and Riester currently hold significant positions, leveraging their established distribution networks and brand reputation. However, innovative entrants such as Depstech, Anykit, and Teslong are rapidly gaining traction by focusing on affordability, user-friendliness, and advanced imaging capabilities, particularly within the direct-to-consumer and home healthcare segments. The market's concentration is further influenced by ongoing mergers and acquisitions. In the historical period (2019-2024), an estimated 7 significant M&A deals worth over $5 billion in total value have occurred, primarily aimed at consolidating market share, acquiring innovative technologies, and expanding product portfolios.

- Innovation Drivers: The primary drivers of innovation include the increasing demand for telemedicine, the need for improved diagnostic accuracy, and the miniaturization of electronic components. Companies are investing heavily in AI-powered diagnostic assistance, enhanced image resolution, and seamless integration with electronic health records (EHRs).

- Regulatory Frameworks: Regulatory bodies such as the FDA (US) and CE (Europe) play a crucial role. Compliance with medical device regulations, data privacy (HIPAA, GDPR), and cybersecurity standards are paramount for market entry and sustained growth. The approval process for new wireless digital otoscopes can take an average of 18 months, adding a layer of complexity.

- Product Substitutes: While traditional otoscopes remain a substitute, their limitations in remote sharing and digital record-keeping are increasingly apparent. However, their low cost of entry still maintains a presence in certain price-sensitive markets.

- End-User Trends: End-users, including healthcare professionals and increasingly, informed consumers, are seeking portable, easy-to-use devices that provide high-quality imaging for remote consultations, patient education, and early detection of ear conditions. Home healthcare settings are witnessing a substantial surge in adoption.

- M&A Activities: Strategic acquisitions are focused on integrating advanced imaging software, AI capabilities, and expanding reach into emerging markets. The value of M&A deals is projected to exceed $8 billion in the forecast period (2025-2033).

Wireless Digital Otoscope Industry Trends & Analysis

The global Wireless Digital Otoscope market is experiencing robust growth, driven by an escalating demand for advanced diagnostic tools that facilitate remote patient monitoring and improve the efficiency of ear examinations. The market's Compound Annual Growth Rate (CAGR) is projected to be approximately 12.5% from 2025 to 2033. This upward trajectory is underpinned by several key trends. The increasing adoption of telemedicine and mHealth solutions globally has created a fertile ground for wireless digital otoscopes, enabling healthcare providers to conduct initial screenings and follow-up examinations remotely, thereby reducing the burden on physical clinics and improving patient access to care, especially in underserved areas. The market penetration of these devices is expected to reach 45% in developed economies by 2030, up from an estimated 25% in 2024.

Technological advancements are at the forefront of this growth. Manufacturers are continuously innovating, integrating higher resolution cameras (approaching 5 megapixels and beyond), improved LED lighting for clearer visualization, and advanced connectivity options like Wi-Fi and Bluetooth for seamless data transfer to smartphones, tablets, and computers. The development of specialized software with AI-driven diagnostic assistance is another significant trend, empowering clinicians with more accurate interpretations of ear canal and tympanic membrane conditions. This includes automated detection of common pathologies like otitis media and cerumen impaction.

Consumer preferences are also shifting. The rising awareness among the general public about ear health, coupled with the convenience offered by home-use wireless digital otoscopes, is fueling demand in the consumer healthcare segment. Parents are increasingly using these devices for routine checks of their children's ears, and individuals with chronic ear conditions are opting for self-monitoring solutions. This trend is further amplified by the competitive landscape, where companies like Apple BioMedical and GlobalMed are focusing on user-friendly interfaces and integration with existing smart home ecosystems.

The competitive dynamics are characterized by a blend of established players and agile disruptors. While giants like LHMed Medical Instruments and INVENTIS SRL continue to innovate within the professional medical device space, newer companies are capturing market share through aggressive pricing strategies and a strong online presence, catering to both healthcare professionals and direct consumers. This has led to increased product variety and features, ranging from basic imaging to sophisticated diagnostic suites. The market is also seeing a growing emphasis on interoperability with Electronic Health Records (EHRs) and Picture Archiving and Communication Systems (PACS), facilitating better data management and collaborative care. The increasing prevalence of ear-related issues, such as hearing loss and infections, globally, further acts as a significant market growth driver, necessitating more advanced and accessible diagnostic tools. The forecast period is expected to witness a substantial increase in the number of specialized ENT clinics and hospitals investing in these digital solutions, anticipating improved patient outcomes and operational efficiencies.

Leading Markets & Segments in Wireless Digital Otoscope

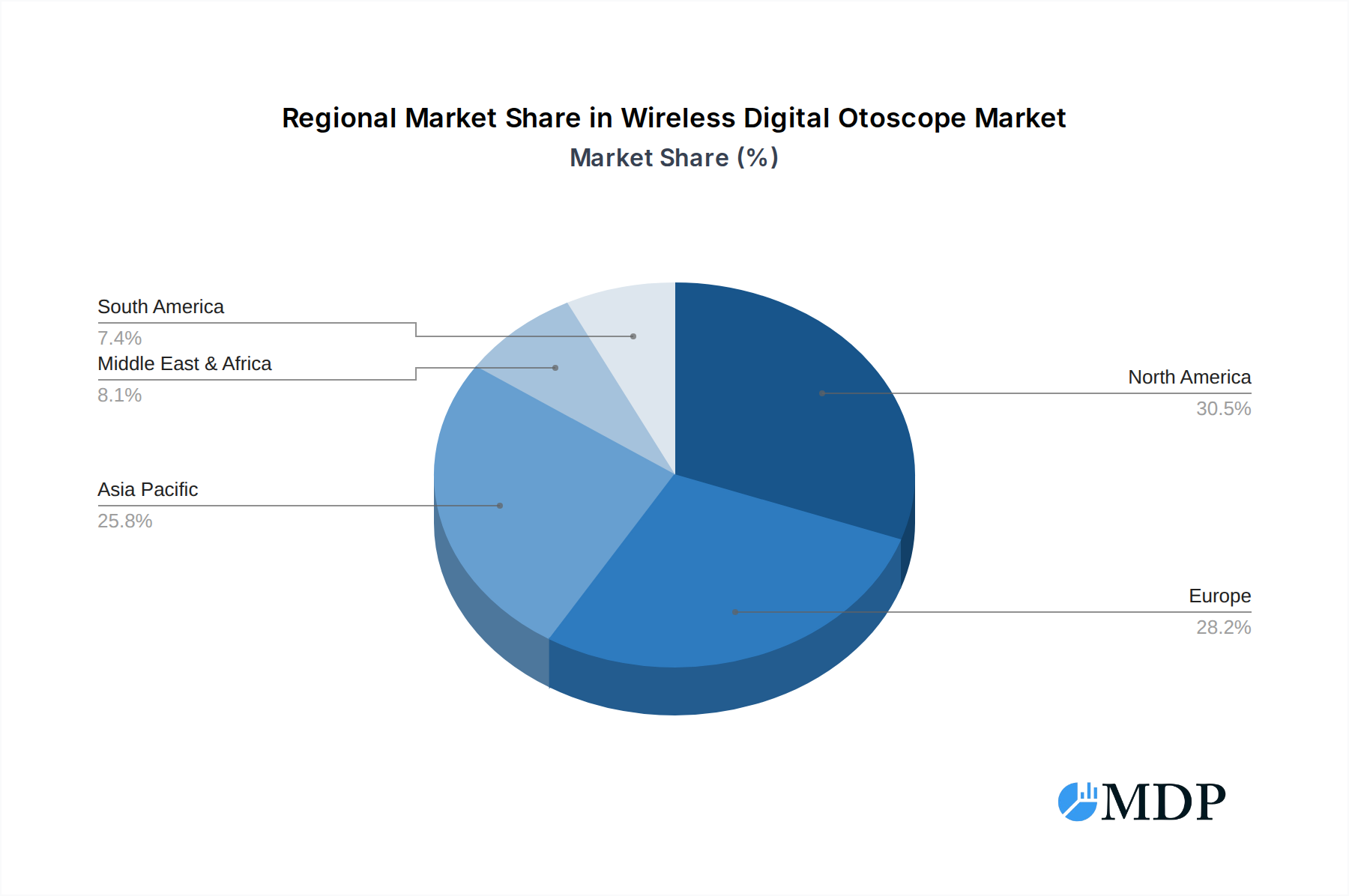

The Wireless Digital Otoscope market is characterized by distinct regional dominance and segment preferences, driven by varying healthcare infrastructures, regulatory environments, and patient demographics.

Dominant Regions and Countries:

The North America region currently leads the global Wireless Digital Otoscope market, with the United States being the foremost contributor. This dominance is attributed to a robust healthcare system with high adoption rates of advanced medical technologies, a strong emphasis on telemedicine, and a significant prevalence of ear-related health issues. The presence of major healthcare providers and a well-developed reimbursement landscape for remote consultations further bolster market growth.

- Key Drivers for North American Dominance:

- High Healthcare Spending: The US healthcare sector consistently invests in cutting-edge medical devices, estimated at over $4 billion annually for diagnostic equipment.

- Advanced Telemedicine Infrastructure: Widespread broadband internet access and government initiatives promoting telehealth services accelerate the adoption of connected medical devices.

- Prevalence of Ear Conditions: A significant aging population and a high incidence of childhood ear infections contribute to sustained demand.

- Favorable Regulatory Environment: The FDA's established pathways for medical device approval facilitate market entry for innovative products.

Europe, particularly countries like Germany and the UK, represents another significant market, driven by strong healthcare systems and increasing government support for digital health initiatives. Asia Pacific is emerging as a high-growth region, fueled by rising disposable incomes, improving healthcare access in developing nations, and a growing awareness of ear health.

Leading Segments:

The market is segmented by Application and Type, with specific segments exhibiting higher growth potential.

Application Segments:

- Hospitals: This segment holds the largest market share due to the high volume of ENT-related consultations and procedures performed in hospital settings. The integration of wireless digital otoscopes with hospital IT systems and their utility in emergency departments and inpatient care contribute to their widespread adoption. An estimated 60% of hospitals in developed nations are expected to have implemented digital otoscopes by 2028.

- ENT Clinics: These specialized clinics are crucial adopters, leveraging the technology for detailed diagnosis, patient education, and documentation of ear conditions. The ability to share high-resolution images and videos with patients enhances the doctor-patient relationship and treatment adherence. ENT clinics are estimated to represent 30% of the total market value.

- Home Healthcare Settings: This segment is witnessing the most rapid growth. The increasing trend of remote patient monitoring, coupled with the desire for convenient and accessible healthcare, is driving the adoption of user-friendly wireless digital otoscopes by individuals and caregivers. The market share for this segment is projected to grow from 5% in 2024 to over 15% by 2033, with an estimated 1.5 billion units in use globally by 2030.

- Others: This includes settings like general practitioner offices, mobile health units, and remote diagnostic centers.

Type Segments:

- Rechargeable Battery: This type dominates the market and is expected to continue its lead due to its cost-effectiveness, environmental friendliness, and convenience for frequent users. The market share for rechargeable battery-powered otoscopes is approximately 70%. The average lifespan of a rechargeable battery in these devices is estimated at 500 charging cycles.

- Disposable Battery: While offering immediate usability, this type is less favored in professional settings due to ongoing replacement costs and environmental concerns. However, it remains relevant for occasional home use and in areas with limited access to charging infrastructure.

- Electric Powered: This category primarily refers to wired devices or those with direct power connections, which are less common in the wireless digital otoscope market focused on portability and convenience.

Wireless Digital Otoscope Product Developments

Recent product developments in the Wireless Digital Otoscope market are characterized by a relentless pursuit of enhanced imaging fidelity, user experience, and diagnostic capabilities. Companies are integrating higher-resolution sensors, improving LED illumination for superior clarity in visualizing the tympanic membrane and ear canal, and developing advanced connectivity solutions for seamless integration with smartphones and tablets. Innovations include AI-powered diagnostic assistance, offering automated detection of common ear conditions like otitis media and cerumen buildup, thereby improving diagnostic accuracy and speed. Enhanced portability, ergonomic designs, and user-friendly interfaces are also key trends, making these devices more accessible for both healthcare professionals and home users. Competitive advantages are increasingly derived from software integration, data management features, and specialized applications tailored for specific medical fields.

Key Drivers of Wireless Digital Otoscope Growth

The Wireless Digital Otoscope market is propelled by a confluence of technological advancements, evolving healthcare paradigms, and growing healthcare needs. The increasing adoption of telemedicine and remote patient monitoring is a primary catalyst, allowing for more accessible and convenient ear examinations. Advancements in imaging technology, such as higher resolution cameras and improved LED lighting, are significantly enhancing diagnostic accuracy. Growing awareness of ear health and the rising incidence of ear-related ailments globally are creating a sustained demand for advanced diagnostic tools. Furthermore, supportive government initiatives promoting digital health adoption and improved healthcare infrastructure in emerging economies are creating new avenues for market expansion. The quest for cost-effective healthcare solutions also favors these digital otoscopes, which can streamline diagnostic processes and reduce the need for frequent in-person visits, thereby contributing to significant cost savings, estimated at an average of 20% per patient consultation.

Challenges in the Wireless Digital Otoscope Market

Despite the promising growth, the Wireless Digital Otoscope market faces several challenges. Regulatory hurdles remain a significant barrier, with stringent approval processes for medical devices, particularly concerning data security and privacy, requiring an average of 24 months for clearance in major markets. High initial investment costs for advanced models can deter smaller clinics and individual practitioners. Technical limitations, such as battery life and the need for reliable internet connectivity for seamless data transfer, can impact user experience. Lack of standardization in software and data formats across different devices can hinder interoperability and integration with existing healthcare systems. Furthermore, resistance to change among some healthcare professionals accustomed to traditional methods and concerns regarding the accuracy of AI-driven diagnostics without direct human oversight present ongoing challenges. The cost of R&D for novel features is estimated to be in the range of $50 million to $100 million for leading companies.

Emerging Opportunities in Wireless Digital Otoscope

The Wireless Digital Otoscope market is rife with emerging opportunities for growth and innovation. The expansion of telemedicine and telehealth services globally presents a significant catalyst, creating a perpetual demand for remote diagnostic tools. The increasing focus on personalized medicine and preventative care is driving the development of otoscopes with advanced analytical capabilities, including AI-driven diagnostics for early disease detection and personalized treatment recommendations. Strategic partnerships between medical device manufacturers and software developers are crucial for creating integrated diagnostic platforms. Furthermore, the growing demand in emerging economies, where access to specialized healthcare is limited, offers substantial market expansion potential. The development of more affordable, yet highly functional, wireless digital otoscopes for home healthcare and consumer use is another key opportunity, tapping into a vast and growing consumer base. Investment in robust cybersecurity measures for these devices is also an emerging imperative, creating opportunities for specialized security solution providers.

Leading Players in the Wireless Digital Otoscope Sector

- FireFly Global

- Heine Optotechnik

- LHMed Medical Instruments

- INVENTIS SRL

- Riester

- Welch Allyn

- Depstech

- Anykit

- Teslong

- Advanced Monitors Corporation

- Apple BioMedical

- GlobalMed

- Interacoustics

- MedRx

- Natus Hearing and Balance

Key Milestones in Wireless Digital Otoscope Industry

- 2019: Introduction of high-resolution CMOS sensors in otoscopes, significantly improving image quality.

- 2020: Surge in demand for remote diagnostic tools due to the global pandemic, accelerating telemedicine adoption.

- 2021: Launch of AI-powered diagnostic assistance features in select wireless digital otoscopes, marking a significant step towards automated diagnosis.

- 2022: Increased regulatory approvals for wireless digital otoscopes with enhanced connectivity and data security features by FDA and CE.

- 2023: Expansion of wireless digital otoscope use in primary care settings beyond specialized ENT clinics.

- 2024: Significant advancements in battery technology leading to longer operational times and faster charging capabilities.

Strategic Outlook for Wireless Digital Otoscope Market

The strategic outlook for the Wireless Digital Otoscope market remains highly optimistic, driven by ongoing technological advancements and the expanding adoption of digital health solutions. The future market will likely see a greater integration of artificial intelligence for diagnostic support, enabling earlier and more accurate detection of ear pathologies. Focus on interoperability with Electronic Health Records (EHRs) and other healthcare IT systems will be paramount for seamless data flow and collaborative care. The increasing demand for user-friendly, portable, and affordable devices will continue to fuel innovation, particularly in the home healthcare and emerging markets. Strategic partnerships and potential acquisitions will further consolidate the market and drive product development. The market is poised for substantial growth, with key accelerators including the continuous evolution of miniaturized electronics, the increasing digital literacy of both patients and healthcare providers, and the persistent global need for accessible and efficient diagnostic tools.

Wireless Digital Otoscope Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. ENT Clinics

- 1.3. Home Healthcare Settings

- 1.4. Others

-

2. Types

- 2.1. Rechargeable Battery

- 2.2. Disposable Battery

- 2.3. Electric Powered

Wireless Digital Otoscope Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Wireless Digital Otoscope Regional Market Share

Geographic Coverage of Wireless Digital Otoscope

Wireless Digital Otoscope REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.17% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Wireless Digital Otoscope Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. ENT Clinics

- 5.1.3. Home Healthcare Settings

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Rechargeable Battery

- 5.2.2. Disposable Battery

- 5.2.3. Electric Powered

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Wireless Digital Otoscope Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. ENT Clinics

- 6.1.3. Home Healthcare Settings

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Rechargeable Battery

- 6.2.2. Disposable Battery

- 6.2.3. Electric Powered

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Wireless Digital Otoscope Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. ENT Clinics

- 7.1.3. Home Healthcare Settings

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Rechargeable Battery

- 7.2.2. Disposable Battery

- 7.2.3. Electric Powered

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Wireless Digital Otoscope Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. ENT Clinics

- 8.1.3. Home Healthcare Settings

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Rechargeable Battery

- 8.2.2. Disposable Battery

- 8.2.3. Electric Powered

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Wireless Digital Otoscope Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. ENT Clinics

- 9.1.3. Home Healthcare Settings

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Rechargeable Battery

- 9.2.2. Disposable Battery

- 9.2.3. Electric Powered

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Wireless Digital Otoscope Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. ENT Clinics

- 10.1.3. Home Healthcare Settings

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Rechargeable Battery

- 10.2.2. Disposable Battery

- 10.2.3. Electric Powered

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 FireFly Global

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Heine Optotechnik

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 LHMed Medical Instruments

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 INVENTIS SRL

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Riester

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Welch Allyn

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Depstech

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Anykit

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Teslong

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Advanced Monitors Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Apple BioMedical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 GlobalMed

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Interacoustics

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 MedRx

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Natus Hearing and Balance

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 FireFly Global

List of Figures

- Figure 1: Global Wireless Digital Otoscope Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Wireless Digital Otoscope Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Wireless Digital Otoscope Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Wireless Digital Otoscope Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Wireless Digital Otoscope Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Wireless Digital Otoscope Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Wireless Digital Otoscope Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Wireless Digital Otoscope Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Wireless Digital Otoscope Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Wireless Digital Otoscope Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Wireless Digital Otoscope Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Wireless Digital Otoscope Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Wireless Digital Otoscope Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Wireless Digital Otoscope Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Wireless Digital Otoscope Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Wireless Digital Otoscope Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Wireless Digital Otoscope Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Wireless Digital Otoscope Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Wireless Digital Otoscope Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Wireless Digital Otoscope Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Wireless Digital Otoscope Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Wireless Digital Otoscope Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Wireless Digital Otoscope Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Wireless Digital Otoscope Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Wireless Digital Otoscope Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Wireless Digital Otoscope Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Wireless Digital Otoscope Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Wireless Digital Otoscope Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Wireless Digital Otoscope Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Wireless Digital Otoscope Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Wireless Digital Otoscope Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wireless Digital Otoscope Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Wireless Digital Otoscope Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Wireless Digital Otoscope Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Wireless Digital Otoscope Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Wireless Digital Otoscope Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Wireless Digital Otoscope Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Wireless Digital Otoscope Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Wireless Digital Otoscope Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Wireless Digital Otoscope Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Wireless Digital Otoscope Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Wireless Digital Otoscope Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Wireless Digital Otoscope Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Wireless Digital Otoscope Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Wireless Digital Otoscope Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Wireless Digital Otoscope Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Wireless Digital Otoscope Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Wireless Digital Otoscope Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Wireless Digital Otoscope Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Wireless Digital Otoscope Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wireless Digital Otoscope?

The projected CAGR is approximately 9.17%.

2. Which companies are prominent players in the Wireless Digital Otoscope?

Key companies in the market include FireFly Global, Heine Optotechnik, LHMed Medical Instruments, INVENTIS SRL, Riester, Welch Allyn, Depstech, Anykit, Teslong, Advanced Monitors Corporation, Apple BioMedical, GlobalMed, Interacoustics, MedRx, Natus Hearing and Balance.

3. What are the main segments of the Wireless Digital Otoscope?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wireless Digital Otoscope," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wireless Digital Otoscope report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wireless Digital Otoscope?

To stay informed about further developments, trends, and reports in the Wireless Digital Otoscope, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence