Key Insights

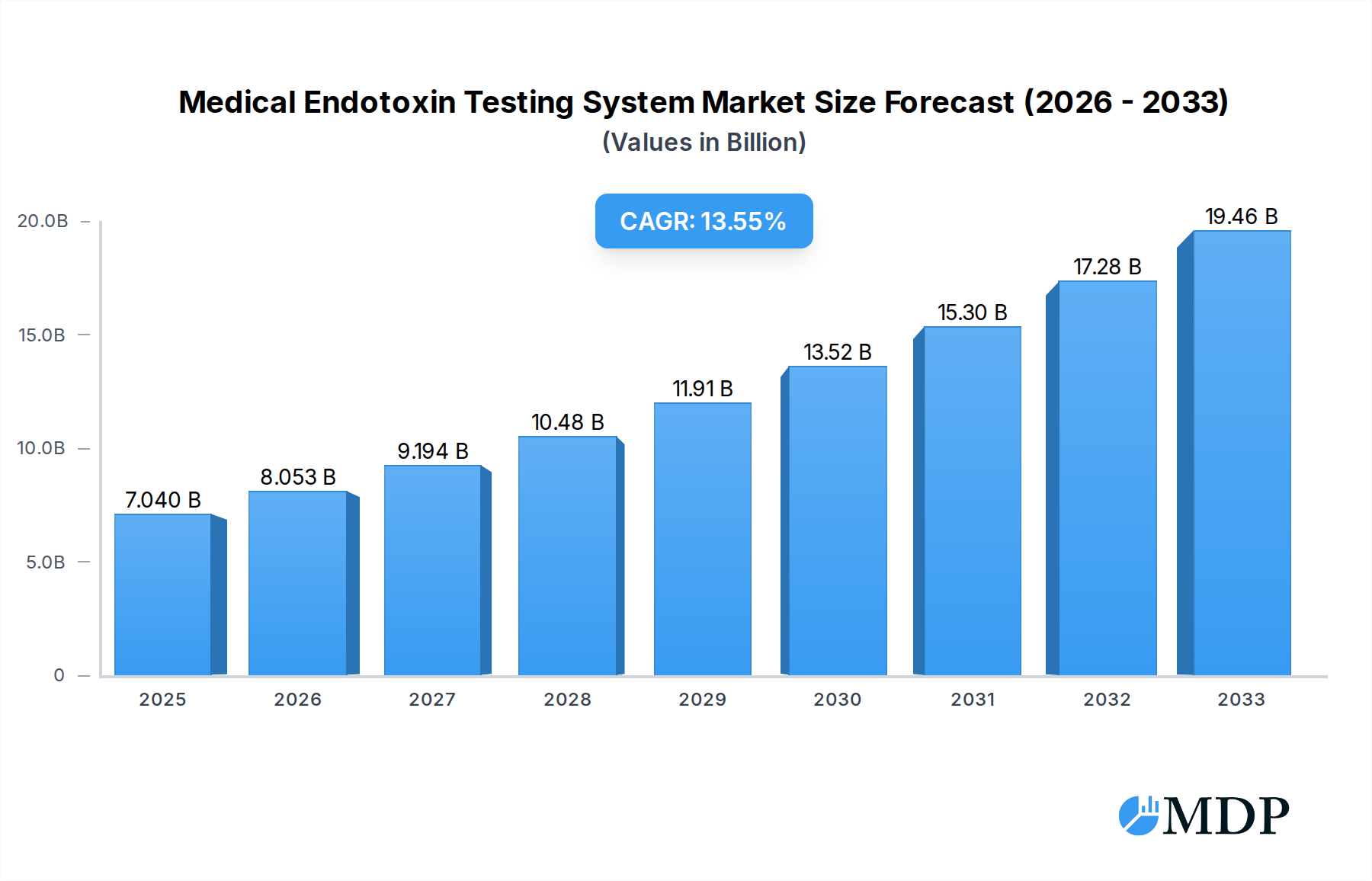

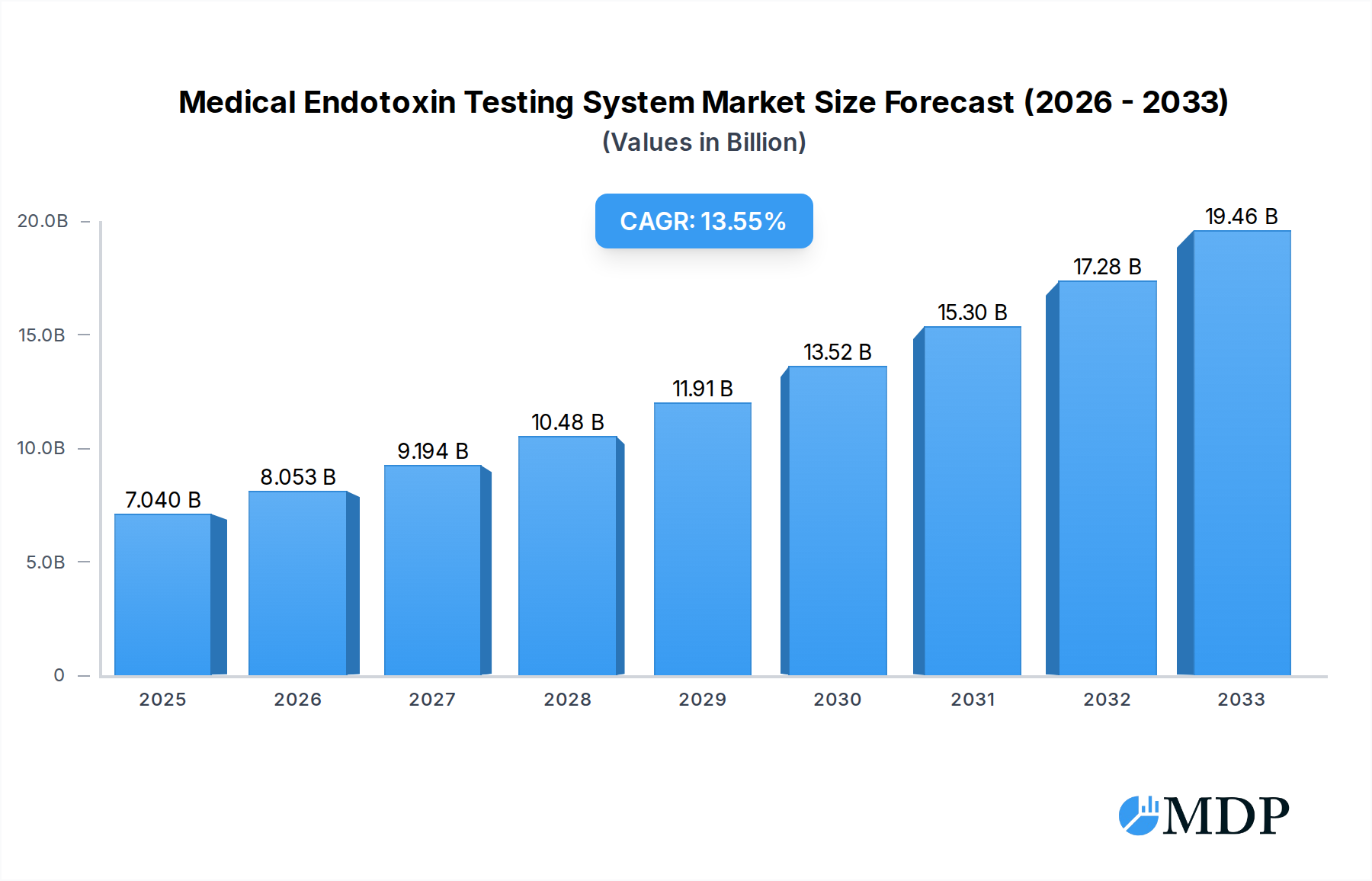

The Medical Endotoxin Testing System market is poised for significant expansion, projected to reach $7.04 billion by 2025, fueled by a robust CAGR of 14.39% throughout the forecast period. This impressive growth trajectory underscores the increasing critical importance of reliable endotoxin detection in safeguarding patient safety and ensuring the quality of pharmaceutical and biopharmaceutical products. The escalating demand for parenteral drugs, vaccines, and medical devices, coupled with stringent regulatory requirements from bodies like the FDA and EMA, are primary drivers. Furthermore, advancements in testing methodologies, leading to more sensitive, faster, and automated solutions, are also contributing to market adoption. The rise of biologics and advanced therapies, which are particularly sensitive to endotoxin contamination, further amplifies the need for sophisticated endotoxin testing systems.

Medical Endotoxin Testing System Market Size (In Billion)

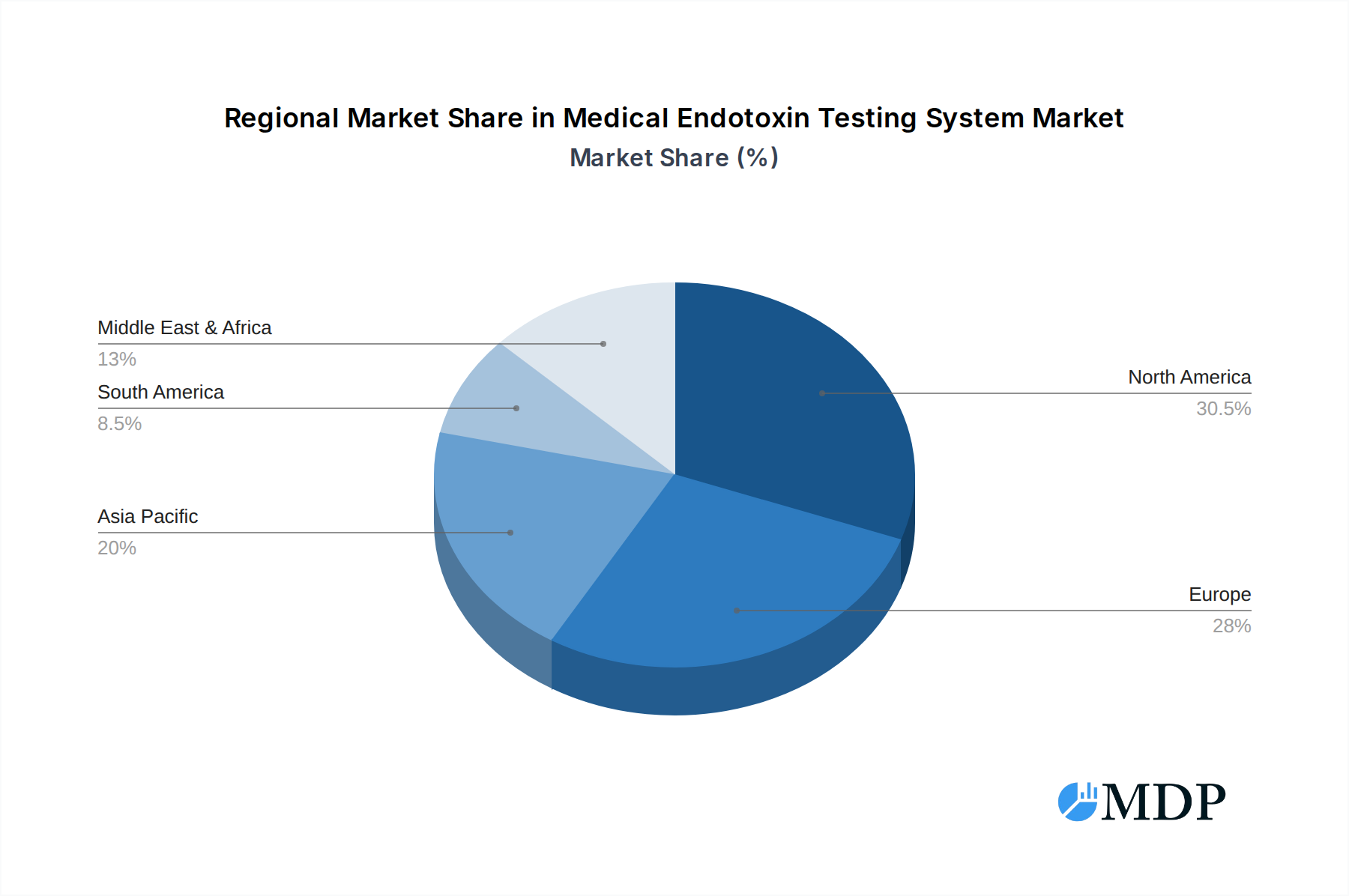

The market's dynamism is further shaped by key trends such as the increasing adoption of automated robotic equipment for high-throughput screening and the growing preference for handheld spectrophotometers for on-site testing in diverse settings. While the potential for market disruptions exists due to the complexity of regulatory landscapes and the cost associated with advanced testing technologies, the overarching demand for patient safety and product integrity will continue to propel market growth. The medical and biopharmaceutical sectors are anticipated to be the dominant application segments, with scientific research also playing a crucial role in driving innovation and demand. Geographically, North America and Europe are expected to lead market share, driven by established healthcare infrastructures and rigorous quality control standards, while the Asia Pacific region is projected for rapid growth due to its expanding pharmaceutical industry and increasing healthcare investments.

Medical Endotoxin Testing System Company Market Share

Here's your SEO-optimized, engaging report description for the Medical Endotoxin Testing System market, designed for maximum visibility and immediate use without modification:

Medical Endotoxin Testing System Market Dynamics & Concentration

The medical endotoxin testing system market is characterized by a moderate to high concentration, with key players like Agilent, Thermo Fisher, and Lonza holding significant market shares, estimated to be over 35 billion collectively. Innovation is a primary driver, propelled by the relentless pursuit of enhanced sensitivity, speed, and automation in endotoxin detection. Regulatory frameworks, particularly from the FDA and EMA, mandate stringent endotoxin limits for parenteral drugs and medical devices, creating a consistent demand for compliant testing solutions. Product substitutes, while existing in the form of less sensitive or slower methods, are increasingly being phased out due to regulatory pressure and the demand for robust quality control. End-user trends lean towards a preference for rapid, in-process testing to minimize batch failures and optimize production timelines, with biopharmaceutical manufacturers leading this adoption, investing billions in advanced systems. Mergers and acquisitions (M&A) activities, though not consistently high in volume, have been strategic, with approximately 7 significant deals valued in the billions occurring during the historical period (2019-2024), aimed at expanding product portfolios and geographic reach.

Medical Endotoxin Testing System Industry Trends & Analysis

The medical endotoxin testing system market is experiencing robust growth, driven by an increasing global demand for safe and effective pharmaceutical products and medical devices. The projected Compound Annual Growth Rate (CAGR) for the forecast period 2025-2033 is an impressive 8.5%, with the estimated market size in 2025 projected to reach a staggering 55 billion. Technological disruptions are at the forefront of market evolution. Advancements in limulus amebocyte lysate (LAL) reagent sensitivity, the development of recombinant factor C (rFC) assays offering a non-animal origin alternative, and the integration of automation and robotics are transforming testing efficiency. Consumer preferences are shifting towards faster, more accurate, and cost-effective solutions, leading to a surge in the adoption of automated benchtop systems and handheld spectrophotometers that enable real-time, in-process monitoring. Competitive dynamics are intense, with leading companies investing heavily in research and development to maintain their market leadership. Market penetration is high in developed regions like North America and Europe, exceeding 80% for advanced testing methods, while emerging economies are showing significant growth potential due to expanding healthcare infrastructure and increasing regulatory compliance. The total market value is projected to exceed 100 billion by 2033.

Leading Markets & Segments in Medical Endotoxin Testing System

The Biopharmaceuticals segment is the dominant force within the medical endotoxin testing system market, projected to account for over 40 billion of the total market value in 2025. This dominance is primarily driven by the stringent regulatory requirements for parenteral drugs, vaccines, and biologics, which necessitate highly sensitive and reliable endotoxin detection throughout the manufacturing process. Within this segment, applications in therapeutic protein production and cell and gene therapy manufacturing are experiencing particularly rapid expansion. The Medical application segment, encompassing medical devices and diagnostics, also holds significant market share, estimated at over 15 billion in 2025, driven by the growing prevalence of chronic diseases and the increasing use of implantable and invasive medical devices.

Dominant Application Segment Drivers (Biopharmaceuticals):

- Stringent Regulatory Mandates: Global regulatory bodies like the FDA and EMA impose strict endotoxin limits, driving consistent demand for advanced testing.

- Growth in Biologics and Biosimilars: The expanding pipeline of biologic drugs and the increasing adoption of biosimilars require rigorous quality control.

- Cell and Gene Therapy Advancements: The novel nature of these therapies necessitates highly sensitive and validated endotoxin testing protocols.

- Focus on Patient Safety: Endotoxin contamination poses a severe risk to patient health, making its detection paramount.

Dominant Type Segment (Automated Robotic Equipment):

- Efficiency and Throughput: Automated systems offer unparalleled speed and high throughput, crucial for large-scale biopharmaceutical production.

- Reduced Human Error: Automation minimizes variability and the risk of manual errors, ensuring data integrity.

- Cost-Effectiveness: Despite higher initial investment, automation leads to reduced labor costs and faster batch release, ultimately proving cost-effective.

- Integration Capabilities: Automated platforms can be seamlessly integrated into existing LIMS and manufacturing execution systems.

Leading Regions: North America and Europe currently represent the largest markets, with an estimated combined market value exceeding 50 billion in 2025, due to mature biopharmaceutical industries and established regulatory frameworks. However, the Asia-Pacific region is emerging as a high-growth market, with an estimated CAGR of 10% during the forecast period, driven by expanding pharmaceutical manufacturing capabilities and increasing investment in healthcare.

Medical Endotoxin Testing System Product Developments

Product developments in the medical endotoxin testing system market are focused on enhancing speed, sensitivity, and automation. Companies like Agilent and Thermo Fisher are leading the charge with innovations in LAL reagents and assay technologies, including advancements in recombinant factor C assays offering a reliable, animal-free alternative. The integration of automated robotic equipment and benchtop systems is transforming laboratory workflows, enabling faster, more accurate, and hands-free testing. Fujifilm's advancements in microfluidics are paving the way for point-of-care testing solutions, while Veolia is focusing on integrated water safety and endotoxin monitoring systems. These developments offer significant competitive advantages by reducing testing times, minimizing the risk of contamination, and improving overall laboratory efficiency, contributing to a market value exceeding 55 billion in 2025.

Key Drivers of Medical Endotoxin Testing System Growth

The medical endotoxin testing system market is propelled by several key drivers, significantly contributing to its projected growth to over 100 billion by 2033.

- Increasingly Stringent Regulatory Requirements: Global health authorities are continuously tightening endotoxin limits for pharmaceuticals and medical devices, mandating more sensitive and reliable testing methods.

- Growing Biopharmaceutical and Vaccine Production: The booming biopharmaceutical industry, coupled with the global demand for vaccines, directly correlates with the need for robust endotoxin testing throughout the manufacturing lifecycle.

- Technological Advancements in Assay Development: Innovations in LAL reagents and the development of recombinant factor C (rFC) assays offer improved specificity, reduced assay times, and the elimination of animal-derived components.

- Rising Incidence of Hospital-Acquired Infections: Endotoxin contamination is a major contributor to hospital-acquired infections, driving demand for effective endotoxin testing in healthcare settings and medical device manufacturing.

Challenges in the Medical Endotoxin Testing System Market

Despite its robust growth, the medical endotoxin testing system market faces several challenges that could temper its expansion, impacting the overall market value projected to exceed 100 billion by 2033.

- High Cost of Advanced Systems: The initial investment for highly automated and sophisticated endotoxin testing systems can be substantial, posing a barrier for smaller laboratories and research institutions.

- Complex Regulatory Compliance: Navigating the evolving and often region-specific regulatory landscapes for endotoxin testing can be challenging and time-consuming for manufacturers and end-users.

- Interference from Sample Matrix Components: Certain complex sample matrices in biopharmaceutical manufacturing can interfere with assay results, requiring extensive method validation and development.

- Supply Chain Volatility for Reagents: Dependence on specific reagents, particularly LAL, can lead to supply chain vulnerabilities and price fluctuations, impacting testing costs.

Emerging Opportunities in Medical Endotoxin Testing System

The medical endotoxin testing system market is ripe with emerging opportunities that are poised to drive long-term growth, contributing to a market value projected to exceed 100 billion by 2033.

- Point-of-Care (POC) and In-Process Testing: The development of portable, rapid endotoxin testing devices for use at the point of care or directly on the manufacturing floor presents a significant opportunity to reduce turnaround times and improve real-time quality control.

- Rise of Biosimilars and Novel Biologics: The expanding market for biosimilars and the continuous development of novel biologic drugs, including cell and gene therapies, create a sustained demand for advanced and validated endotoxin testing solutions.

- Adoption of Recombinant Factor C (rFC) Assays: The increasing preference for animal-free testing methods, driven by ethical concerns and regulatory guidance, fuels the adoption of rFC-based assays, creating opportunities for companies specializing in these technologies.

- Expansion in Emerging Markets: The growing pharmaceutical and healthcare sectors in Asia-Pacific, Latin America, and the Middle East offer substantial untapped potential for market penetration and expansion of endotoxin testing services and systems.

Leading Players in the Medical Endotoxin Testing System Sector

- Agilent

- Criver Microbial

- Thermo Fisher

- ACC (Associates of Cape Cod, Inc.)

- Fujifilm

- Veolia

- Lonza

Key Milestones in Medical Endotoxin Testing System Industry

- 2019: Increased adoption of recombinant factor C (rFC) assays in biopharmaceutical manufacturing, driven by regulatory endorsements.

- 2020: Surge in demand for rapid endotoxin testing solutions due to increased vaccine production and the global pandemic.

- 2021: Strategic acquisitions of smaller endotoxin testing technology companies by major players to expand portfolios.

- 2022: Introduction of advanced automated robotic equipment for high-throughput endotoxin testing in large biopharmaceutical facilities.

- 2023: Growing emphasis on sustainability and animal-free testing methods, leading to further innovation in rFC assay development.

- 2024: Enhanced integration of endotoxin testing systems with LIMS and data analytics platforms for improved quality control and compliance.

Strategic Outlook for Medical Endotoxin Testing System Market

The strategic outlook for the medical endotoxin testing system market is exceptionally positive, with growth accelerators pointing towards continued expansion and innovation, projecting a market value exceeding 100 billion by 2033. Key growth accelerants include the increasing regulatory scrutiny on endotoxin contamination in pharmaceuticals and medical devices, driving demand for highly sensitive and compliant testing solutions. The burgeoning biopharmaceutical sector, with its focus on biologics, vaccines, and novel therapies, will continue to be a primary engine of market growth. Strategic opportunities lie in the continued development and adoption of rapid, automated, and point-of-care testing solutions. Furthermore, the growing preference for animal-free testing methods, like recombinant factor C assays, presents a significant avenue for product development and market penetration. Expansion into emerging economies with developing healthcare infrastructure and increasing regulatory enforcement will also fuel long-term market potential.

Medical Endotoxin Testing System Segmentation

-

1. Application

- 1.1. Medical

- 1.2. Biopharmaceuticals

- 1.3. Scientific Research

- 1.4. Other

-

2. Types

- 2.1. Handheld Spectrophotometers

- 2.2. Benchtop Systems

- 2.3. Automated Robotic Equipment

- 2.4. Other

Medical Endotoxin Testing System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Endotoxin Testing System Regional Market Share

Geographic Coverage of Medical Endotoxin Testing System

Medical Endotoxin Testing System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Endotoxin Testing System Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Medical

- 5.1.2. Biopharmaceuticals

- 5.1.3. Scientific Research

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Handheld Spectrophotometers

- 5.2.2. Benchtop Systems

- 5.2.3. Automated Robotic Equipment

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical Endotoxin Testing System Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Medical

- 6.1.2. Biopharmaceuticals

- 6.1.3. Scientific Research

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Handheld Spectrophotometers

- 6.2.2. Benchtop Systems

- 6.2.3. Automated Robotic Equipment

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical Endotoxin Testing System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Medical

- 7.1.2. Biopharmaceuticals

- 7.1.3. Scientific Research

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Handheld Spectrophotometers

- 7.2.2. Benchtop Systems

- 7.2.3. Automated Robotic Equipment

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical Endotoxin Testing System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Medical

- 8.1.2. Biopharmaceuticals

- 8.1.3. Scientific Research

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Handheld Spectrophotometers

- 8.2.2. Benchtop Systems

- 8.2.3. Automated Robotic Equipment

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical Endotoxin Testing System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Medical

- 9.1.2. Biopharmaceuticals

- 9.1.3. Scientific Research

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Handheld Spectrophotometers

- 9.2.2. Benchtop Systems

- 9.2.3. Automated Robotic Equipment

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical Endotoxin Testing System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Medical

- 10.1.2. Biopharmaceuticals

- 10.1.3. Scientific Research

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Handheld Spectrophotometers

- 10.2.2. Benchtop Systems

- 10.2.3. Automated Robotic Equipment

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Agilent

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Criver Microbial

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Thermo Fisher

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ACC (Associates of Cape Cod

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Inc.)

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Fujifilm

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Veolia

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Lonza

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Agilent

List of Figures

- Figure 1: Global Medical Endotoxin Testing System Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Medical Endotoxin Testing System Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Medical Endotoxin Testing System Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Medical Endotoxin Testing System Volume (K), by Application 2025 & 2033

- Figure 5: North America Medical Endotoxin Testing System Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Medical Endotoxin Testing System Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Medical Endotoxin Testing System Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Medical Endotoxin Testing System Volume (K), by Types 2025 & 2033

- Figure 9: North America Medical Endotoxin Testing System Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Medical Endotoxin Testing System Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Medical Endotoxin Testing System Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Medical Endotoxin Testing System Volume (K), by Country 2025 & 2033

- Figure 13: North America Medical Endotoxin Testing System Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Medical Endotoxin Testing System Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Medical Endotoxin Testing System Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Medical Endotoxin Testing System Volume (K), by Application 2025 & 2033

- Figure 17: South America Medical Endotoxin Testing System Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Medical Endotoxin Testing System Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Medical Endotoxin Testing System Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Medical Endotoxin Testing System Volume (K), by Types 2025 & 2033

- Figure 21: South America Medical Endotoxin Testing System Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Medical Endotoxin Testing System Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Medical Endotoxin Testing System Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Medical Endotoxin Testing System Volume (K), by Country 2025 & 2033

- Figure 25: South America Medical Endotoxin Testing System Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Medical Endotoxin Testing System Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Medical Endotoxin Testing System Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Medical Endotoxin Testing System Volume (K), by Application 2025 & 2033

- Figure 29: Europe Medical Endotoxin Testing System Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Medical Endotoxin Testing System Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Medical Endotoxin Testing System Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Medical Endotoxin Testing System Volume (K), by Types 2025 & 2033

- Figure 33: Europe Medical Endotoxin Testing System Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Medical Endotoxin Testing System Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Medical Endotoxin Testing System Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Medical Endotoxin Testing System Volume (K), by Country 2025 & 2033

- Figure 37: Europe Medical Endotoxin Testing System Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Medical Endotoxin Testing System Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Medical Endotoxin Testing System Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Medical Endotoxin Testing System Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Medical Endotoxin Testing System Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Medical Endotoxin Testing System Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Medical Endotoxin Testing System Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Medical Endotoxin Testing System Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Medical Endotoxin Testing System Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Medical Endotoxin Testing System Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Medical Endotoxin Testing System Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Medical Endotoxin Testing System Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Medical Endotoxin Testing System Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Medical Endotoxin Testing System Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Medical Endotoxin Testing System Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Medical Endotoxin Testing System Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Medical Endotoxin Testing System Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Medical Endotoxin Testing System Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Medical Endotoxin Testing System Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Medical Endotoxin Testing System Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Medical Endotoxin Testing System Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Medical Endotoxin Testing System Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Medical Endotoxin Testing System Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Medical Endotoxin Testing System Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Medical Endotoxin Testing System Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Medical Endotoxin Testing System Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Medical Endotoxin Testing System Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Medical Endotoxin Testing System Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Medical Endotoxin Testing System Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Medical Endotoxin Testing System Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Medical Endotoxin Testing System Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Medical Endotoxin Testing System Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Medical Endotoxin Testing System Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Medical Endotoxin Testing System Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Medical Endotoxin Testing System Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Medical Endotoxin Testing System Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Medical Endotoxin Testing System Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Medical Endotoxin Testing System Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Medical Endotoxin Testing System Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Medical Endotoxin Testing System Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Medical Endotoxin Testing System Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Medical Endotoxin Testing System Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Medical Endotoxin Testing System Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Medical Endotoxin Testing System Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Medical Endotoxin Testing System Volume K Forecast, by Country 2020 & 2033

- Table 79: China Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Medical Endotoxin Testing System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Medical Endotoxin Testing System Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Endotoxin Testing System?

The projected CAGR is approximately 14.39%.

2. Which companies are prominent players in the Medical Endotoxin Testing System?

Key companies in the market include Agilent, Criver Microbial, Thermo Fisher, ACC (Associates of Cape Cod, Inc.), Fujifilm, Veolia, Lonza.

3. What are the main segments of the Medical Endotoxin Testing System?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Endotoxin Testing System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Endotoxin Testing System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Endotoxin Testing System?

To stay informed about further developments, trends, and reports in the Medical Endotoxin Testing System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence