Key Insights

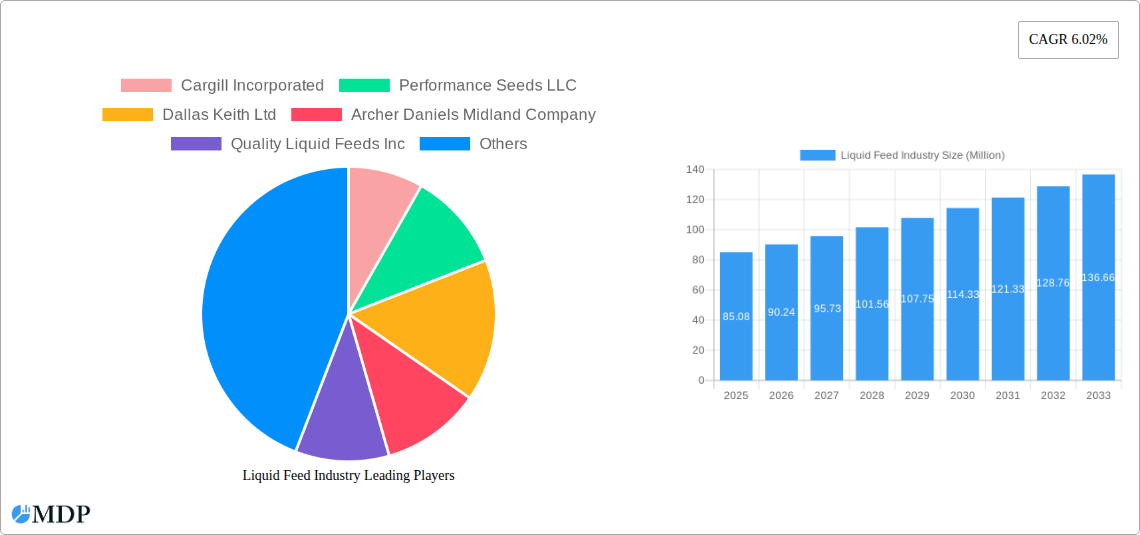

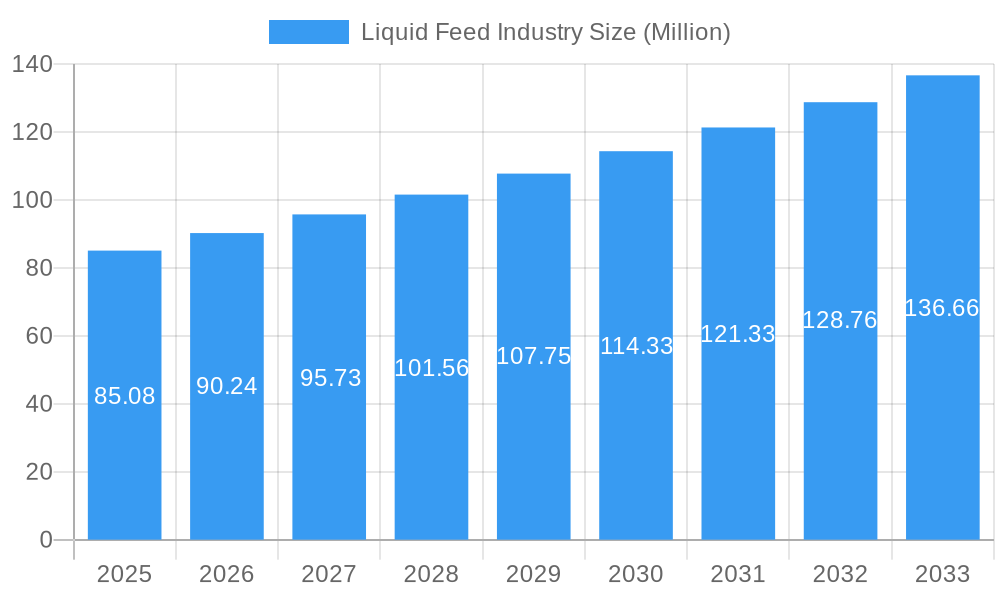

The global liquid feed market, valued at $85.08 million in 2025, is projected to experience robust growth, driven by several key factors. Increasing demand for efficient and cost-effective animal feed solutions, particularly within the intensive livestock farming sector, is a primary driver. The rising global population and the consequent surge in protein consumption are fueling this demand. Furthermore, the incorporation of liquid feeds offers advantages such as improved nutrient digestibility and reduced feed wastage, contributing to enhanced animal health and productivity. Technological advancements in feed formulation and delivery systems are also contributing to market expansion. Specific growth segments include those utilizing molasses and corn as key ingredients, catering to ruminant and poultry farming. However, the market faces challenges, including fluctuations in raw material prices (e.g., corn and molasses) and stringent regulatory frameworks related to feed safety and environmental concerns. Competitive pressures from established players like Cargill and ADM, alongside smaller regional producers, create a dynamic market landscape. Geographical expansion, particularly in developing economies with burgeoning livestock industries in regions like Asia-Pacific and South America, presents significant opportunities for growth. The market's continued expansion will likely depend on innovations focused on sustainable feed production, optimizing feed efficiency, and addressing regulatory compliance.

Liquid Feed Industry Market Size (In Million)

The forecast period (2025-2033) anticipates a compound annual growth rate (CAGR) of 6.02%. This growth is expected to be influenced by factors such as the increasing adoption of precision feeding techniques, leading to optimized nutrient delivery and reduced feed costs. Furthermore, the growing awareness among farmers regarding the benefits of liquid feeds in terms of improved animal health and performance will likely bolster market expansion. However, potential challenges include volatile energy prices impacting production costs, and the need for continual investment in research and development to create innovative and sustainable liquid feed solutions that meet the evolving needs of the livestock industry and address environmental concerns. Regional market growth will likely vary, with faster growth anticipated in regions experiencing rapid agricultural development and expanding livestock populations.

Liquid Feed Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global liquid feed industry, offering invaluable insights for stakeholders across the value chain. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report delivers actionable intelligence to navigate the dynamic landscape of this multi-billion dollar market. Key market segments including proteins, minerals, vitamins, and other types of liquid feed across various animal types (ruminant, poultry, swine, aquaculture, etc.) are thoroughly examined, alongside key players like Cargill, ADM, and BASF.

Liquid Feed Industry Market Dynamics & Concentration

The global liquid feed market, valued at xx Million in 2024, is characterized by moderate concentration with several major players commanding significant market share. Cargill Incorporated, Archer Daniels Midland Company, and BASF SE are among the leading companies, collectively holding an estimated xx% market share in 2024. The market’s dynamic nature is driven by several factors:

- Innovation: Continuous innovation in feed formulations, driven by advancements in enzyme technology and the development of novel additives, is a key growth driver. The recent launch of BASF's Natupulse TS exemplifies this trend.

- Regulatory Landscape: Stringent regulations concerning feed safety and environmental impact are shaping industry practices and driving the adoption of sustainable solutions.

- Product Substitutes: Competition from alternative feed sources and the rising popularity of organic and sustainable feed options are influencing market dynamics.

- End-User Trends: The growing demand for high-quality animal protein and the increasing adoption of intensive farming practices are major growth stimulants.

- M&A Activities: The market has witnessed a significant number of mergers and acquisitions (M&A) in recent years, with xx major deals recorded between 2019 and 2024, primarily aimed at expanding market reach and product portfolios. Eastman Chemical Company's acquisition of 3F Feed & Food in 2021 illustrates this trend. This consolidation is expected to continue, further impacting market concentration.

Liquid Feed Industry Industry Trends & Analysis

The global liquid feed market is experiencing robust growth, with a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Several factors contribute to this positive outlook:

The increasing demand for animal protein globally fuels the need for efficient and cost-effective feed solutions. Liquid feed's advantages in terms of nutrient delivery and ease of mixing are driving adoption. Technological advancements, including precision feeding technologies and data analytics, are optimizing feed formulation and improving the overall efficiency of animal production. Consumer preferences for sustainably produced animal products are also influencing the industry, leading to the development of environmentally friendly feed solutions. Furthermore, the competitive landscape is fostering innovation, with companies investing heavily in R&D to improve feed efficiency and enhance animal health. Market penetration of liquid feed is expected to increase from xx% in 2024 to xx% by 2033.

Leading Markets & Segments in Liquid Feed Industry

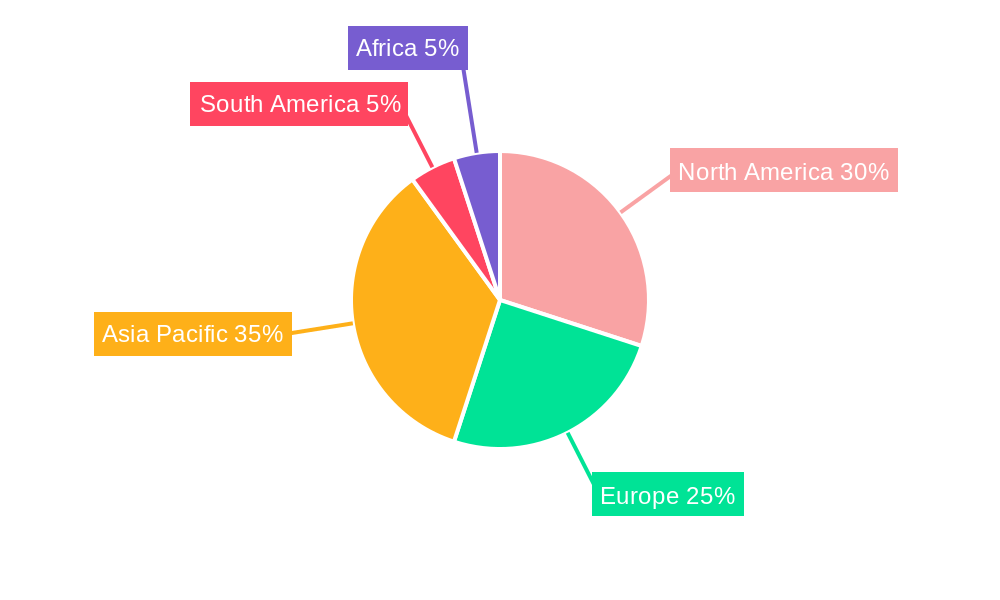

The North American region dominates the global liquid feed market, driven by factors such as the high density of livestock farming and robust infrastructure. Other regions with significant market share include Europe and Asia-Pacific, with growth varying by specific country and regional policies. Within the segment breakdown:

- By Type: The proteins segment holds the largest market share, followed by minerals and vitamins. The "other types" segment is expected to exhibit significant growth.

- By Ingredient: Molasses remains the dominant ingredient, followed by corn and urea. The "other ingredients" category is experiencing strong growth due to the rising popularity of functional additives and novel feed components.

- By Animal Type: Poultry and swine account for the largest market share, due to their high demand and relatively higher efficiency. However, the ruminant segment is showing considerable promise due to increased demand for dairy and beef.

Key Drivers:

- Economic Policies: Government support for agriculture and livestock farming incentivizes feed consumption and market growth.

- Infrastructure: Efficient transportation and logistics networks facilitate the distribution and delivery of liquid feed products.

- Technological Advancements: Innovation in feed processing and storage technologies enhance productivity and market efficiency.

Liquid Feed Industry Product Developments

Recent years have witnessed significant product innovations in the liquid feed industry, with a strong focus on enhancing feed efficiency, improving animal health, and promoting sustainable practices. New enzyme technologies, like BASF SE's Natupulse TS, are improving nutrient digestibility and reducing environmental impact. The industry also shows a growing emphasis on incorporating functional additives to enhance the overall health and performance of animals, reflecting both consumer and industry preferences. This focus on improved efficacy and sustainable methods drives growth and competitive advantage.

Key Drivers of Liquid Feed Industry Growth

Several factors are propelling the growth of the liquid feed industry. Technological advancements in feed formulation and delivery systems significantly improve efficiency and reduce costs. Growing global demand for animal protein, coupled with increasing urbanization and rising disposable incomes, is driving consumption. Favorable government policies and investments in agriculture further enhance market expansion. Finally, the development of innovative, sustainable feed solutions is attracting environmentally conscious consumers and investors.

Challenges in the Liquid Feed Industry Market

The liquid feed industry faces challenges, including volatile raw material prices, stringent regulations requiring compliance with ever-changing safety standards, and potential supply chain disruptions. These factors can impact production costs and profitability. Furthermore, intense competition among established players and the entry of new entrants create pressures on pricing and market share. Regulatory hurdles involving environmental concerns regarding animal waste pose another hurdle, with estimated xx Million lost annually in potential revenue due to compliance setbacks.

Emerging Opportunities in Liquid Feed Industry

Significant opportunities exist within the liquid feed industry. Technological advancements, such as precision feeding and the integration of data analytics, are enhancing efficiency and optimization. Strategic partnerships and collaborations across the value chain enhance production capabilities. Finally, market expansion into developing regions offers substantial growth potential. These factors promise significant long-term growth potential and enhanced market share.

Leading Players in the Liquid Feed Industry Sector

- Cargill Incorporated (Cargill)

- Performance Seeds LLC

- Dallas Keith Ltd

- Archer Daniels Midland Company (ADM)

- Quality Liquid Feeds Inc

- Bundaberg Molasses

- BASF SE (BASF)

- Land O'Lakes Inc (Land O'Lakes)

- Alliance Liquid Feeds Inc

- Masterfeeds LP

- Midwest Liquid Feeds LLC

- GrainCorp Limited (GrainCorp)

- Westway Feed Products LLC

- Ridley Corporation (Ridley)

Key Milestones in Liquid Feed Industry Industry

- December 2021: BASF SE launched Natupulse TS, a novel enzyme for animal feed, enhancing digestibility and sustainability.

- April 2021: Eastman Chemical Company acquired 3F Feed & Food, strengthening its position in the feed additive market.

- December 2020: Archer Daniels Midland (ADM) Company transitioned from dry to liquid lysine production, impacting the swine and poultry feed markets.

Strategic Outlook for Liquid Feed Industry Market

The future of the liquid feed industry is promising, driven by sustained demand for animal protein, technological innovation, and strategic partnerships. The focus on sustainable and efficient feed solutions presents significant growth opportunities. Companies that invest in R&D, embrace technological advancements, and adopt sustainable practices are well-positioned to capitalize on the market's potential and shape its future trajectory. The global market is poised for continued expansion, with substantial potential for market penetration and increased consumption.

Liquid Feed Industry Segmentation

-

1. Type

- 1.1. Proteins

- 1.2. Minerals

- 1.3. Vitamins

- 1.4. Other Types

-

2. Ingredients

- 2.1. Molasses

- 2.2. Corn

- 2.3. Urea

- 2.4. Other Ingredients

-

3. Animal Type

- 3.1. Ruminant

- 3.2. Poultry

- 3.3. Swine

- 3.4. Aquaculture

- 3.5. Other Animal Types

Liquid Feed Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Africa

- 5.1. South Africa

- 5.2. Rest of Africa

Liquid Feed Industry Regional Market Share

Geographic Coverage of Liquid Feed Industry

Liquid Feed Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.02% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Proteins

- 5.1.2. Minerals

- 5.1.3. Vitamins

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Ingredients

- 5.2.1. Molasses

- 5.2.2. Corn

- 5.2.3. Urea

- 5.2.4. Other Ingredients

- 5.3. Market Analysis, Insights and Forecast - by Animal Type

- 5.3.1. Ruminant

- 5.3.2. Poultry

- 5.3.3. Swine

- 5.3.4. Aquaculture

- 5.3.5. Other Animal Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. South America

- 5.4.5. Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Liquid Feed Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Proteins

- 6.1.2. Minerals

- 6.1.3. Vitamins

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Ingredients

- 6.2.1. Molasses

- 6.2.2. Corn

- 6.2.3. Urea

- 6.2.4. Other Ingredients

- 6.3. Market Analysis, Insights and Forecast - by Animal Type

- 6.3.1. Ruminant

- 6.3.2. Poultry

- 6.3.3. Swine

- 6.3.4. Aquaculture

- 6.3.5. Other Animal Types

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Liquid Feed Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Proteins

- 7.1.2. Minerals

- 7.1.3. Vitamins

- 7.1.4. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Ingredients

- 7.2.1. Molasses

- 7.2.2. Corn

- 7.2.3. Urea

- 7.2.4. Other Ingredients

- 7.3. Market Analysis, Insights and Forecast - by Animal Type

- 7.3.1. Ruminant

- 7.3.2. Poultry

- 7.3.3. Swine

- 7.3.4. Aquaculture

- 7.3.5. Other Animal Types

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Liquid Feed Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Proteins

- 8.1.2. Minerals

- 8.1.3. Vitamins

- 8.1.4. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Ingredients

- 8.2.1. Molasses

- 8.2.2. Corn

- 8.2.3. Urea

- 8.2.4. Other Ingredients

- 8.3. Market Analysis, Insights and Forecast - by Animal Type

- 8.3.1. Ruminant

- 8.3.2. Poultry

- 8.3.3. Swine

- 8.3.4. Aquaculture

- 8.3.5. Other Animal Types

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Liquid Feed Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Proteins

- 9.1.2. Minerals

- 9.1.3. Vitamins

- 9.1.4. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Ingredients

- 9.2.1. Molasses

- 9.2.2. Corn

- 9.2.3. Urea

- 9.2.4. Other Ingredients

- 9.3. Market Analysis, Insights and Forecast - by Animal Type

- 9.3.1. Ruminant

- 9.3.2. Poultry

- 9.3.3. Swine

- 9.3.4. Aquaculture

- 9.3.5. Other Animal Types

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Liquid Feed Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Proteins

- 10.1.2. Minerals

- 10.1.3. Vitamins

- 10.1.4. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Ingredients

- 10.2.1. Molasses

- 10.2.2. Corn

- 10.2.3. Urea

- 10.2.4. Other Ingredients

- 10.3. Market Analysis, Insights and Forecast - by Animal Type

- 10.3.1. Ruminant

- 10.3.2. Poultry

- 10.3.3. Swine

- 10.3.4. Aquaculture

- 10.3.5. Other Animal Types

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Africa Liquid Feed Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Proteins

- 11.1.2. Minerals

- 11.1.3. Vitamins

- 11.1.4. Other Types

- 11.2. Market Analysis, Insights and Forecast - by Ingredients

- 11.2.1. Molasses

- 11.2.2. Corn

- 11.2.3. Urea

- 11.2.4. Other Ingredients

- 11.3. Market Analysis, Insights and Forecast - by Animal Type

- 11.3.1. Ruminant

- 11.3.2. Poultry

- 11.3.3. Swine

- 11.3.4. Aquaculture

- 11.3.5. Other Animal Types

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Cargill Incorporated

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Performance Seeds LLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Dallas Keith Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Archer Daniels Midland Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Quality Liquid Feeds Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Bundaberg Molasses

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BASF SE

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Land O'lakes Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Alliance Liquid Feeds Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Masterfeeds LP

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Midwest Liquid Feeds LLC*List Not Exhaustive

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 GrainCorp Limited

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Westway Feed Products LLC

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Ridley Corporation

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Cargill Incorporated

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Liquid Feed Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Liquid Feed Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Liquid Feed Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Liquid Feed Industry Revenue (Million), by Ingredients 2025 & 2033

- Figure 5: North America Liquid Feed Industry Revenue Share (%), by Ingredients 2025 & 2033

- Figure 6: North America Liquid Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 7: North America Liquid Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 8: North America Liquid Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Liquid Feed Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Liquid Feed Industry Revenue (Million), by Type 2025 & 2033

- Figure 11: Europe Liquid Feed Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Liquid Feed Industry Revenue (Million), by Ingredients 2025 & 2033

- Figure 13: Europe Liquid Feed Industry Revenue Share (%), by Ingredients 2025 & 2033

- Figure 14: Europe Liquid Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 15: Europe Liquid Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 16: Europe Liquid Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Liquid Feed Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Liquid Feed Industry Revenue (Million), by Type 2025 & 2033

- Figure 19: Asia Pacific Liquid Feed Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Asia Pacific Liquid Feed Industry Revenue (Million), by Ingredients 2025 & 2033

- Figure 21: Asia Pacific Liquid Feed Industry Revenue Share (%), by Ingredients 2025 & 2033

- Figure 22: Asia Pacific Liquid Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 23: Asia Pacific Liquid Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 24: Asia Pacific Liquid Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Liquid Feed Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Liquid Feed Industry Revenue (Million), by Type 2025 & 2033

- Figure 27: South America Liquid Feed Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: South America Liquid Feed Industry Revenue (Million), by Ingredients 2025 & 2033

- Figure 29: South America Liquid Feed Industry Revenue Share (%), by Ingredients 2025 & 2033

- Figure 30: South America Liquid Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 31: South America Liquid Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 32: South America Liquid Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: South America Liquid Feed Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Africa Liquid Feed Industry Revenue (Million), by Type 2025 & 2033

- Figure 35: Africa Liquid Feed Industry Revenue Share (%), by Type 2025 & 2033

- Figure 36: Africa Liquid Feed Industry Revenue (Million), by Ingredients 2025 & 2033

- Figure 37: Africa Liquid Feed Industry Revenue Share (%), by Ingredients 2025 & 2033

- Figure 38: Africa Liquid Feed Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 39: Africa Liquid Feed Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 40: Africa Liquid Feed Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Africa Liquid Feed Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Liquid Feed Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Liquid Feed Industry Revenue Million Forecast, by Ingredients 2020 & 2033

- Table 3: Global Liquid Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 4: Global Liquid Feed Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Liquid Feed Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: Global Liquid Feed Industry Revenue Million Forecast, by Ingredients 2020 & 2033

- Table 7: Global Liquid Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 8: Global Liquid Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Rest of North America Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global Liquid Feed Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Global Liquid Feed Industry Revenue Million Forecast, by Ingredients 2020 & 2033

- Table 15: Global Liquid Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 16: Global Liquid Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Germany Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United Kingdom Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: France Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Liquid Feed Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 22: Global Liquid Feed Industry Revenue Million Forecast, by Ingredients 2020 & 2033

- Table 23: Global Liquid Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 24: Global Liquid Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: China Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Japan Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: India Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Australia Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Asia Pacific Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Liquid Feed Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 31: Global Liquid Feed Industry Revenue Million Forecast, by Ingredients 2020 & 2033

- Table 32: Global Liquid Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 33: Global Liquid Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: Brazil Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Argentina Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of South America Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Liquid Feed Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 38: Global Liquid Feed Industry Revenue Million Forecast, by Ingredients 2020 & 2033

- Table 39: Global Liquid Feed Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 40: Global Liquid Feed Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 41: South Africa Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Africa Liquid Feed Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Liquid Feed Industry?

The projected CAGR is approximately 6.02%.

2. Which companies are prominent players in the Liquid Feed Industry?

Key companies in the market include Cargill Incorporated, Performance Seeds LLC, Dallas Keith Ltd, Archer Daniels Midland Company, Quality Liquid Feeds Inc, Bundaberg Molasses, BASF SE, Land O'lakes Inc, Alliance Liquid Feeds Inc, Masterfeeds LP, Midwest Liquid Feeds LLC*List Not Exhaustive, GrainCorp Limited, Westway Feed Products LLC, Ridley Corporation.

3. What are the main segments of the Liquid Feed Industry?

The market segments include Type, Ingredients, Animal Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 85.08 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Meat; Initiatives By the Key Players; Focus on Animal nutrition and Health.

6. What are the notable trends driving market growth?

Increase in the Production of Meat and Aquaculture Products.

7. Are there any restraints impacting market growth?

Shift Toward Vegan- Based Diet; Changing Raw Material Prices and Strict Government Rules to Restrict Market Growth.

8. Can you provide examples of recent developments in the market?

December 2021: BASF SE launched the new enzyme product Natupulse TS for animal feed. Natupulse TS is a non-starch polysaccharide (NSP) enzyme. The addition of ß-mannanase to the feed decreases digesta viscosity, increases the digestibility of the feed, and ensures a more sustainable production. Natupulse TS is available in powder and liquid form. Both formulations deliver very good overall stability during storage, in premix, and under challenging conditions in the pelleting process.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Liquid Feed Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Liquid Feed Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Liquid Feed Industry?

To stay informed about further developments, trends, and reports in the Liquid Feed Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence