Key Insights

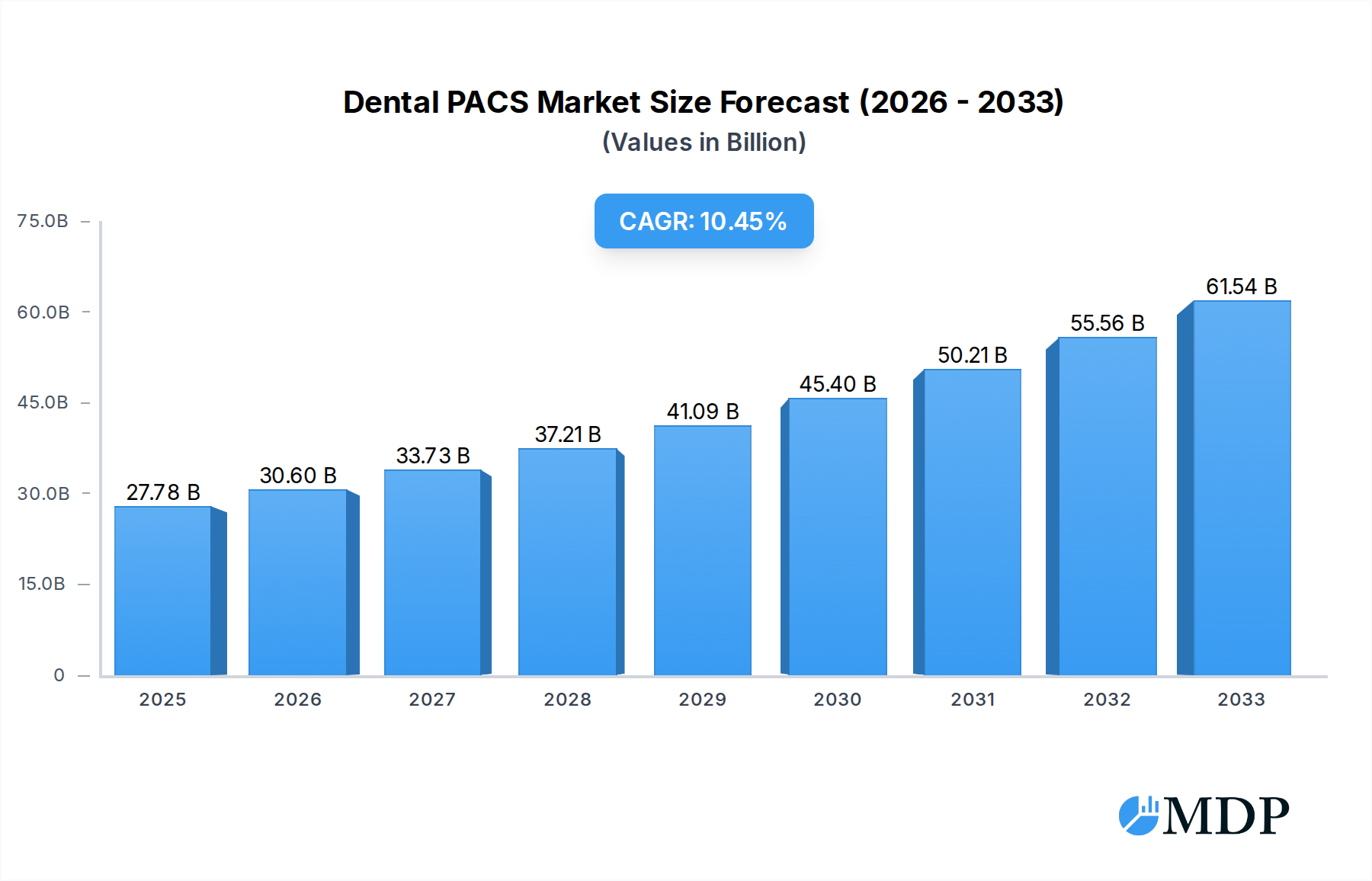

The global Dental PACS market is poised for substantial growth, projected to reach an estimated USD 27.78 billion in 2025. This expansion is driven by a CAGR of 10.2%, indicating a robust and sustained upward trajectory over the forecast period of 2025-2033. The increasing adoption of digital imaging technologies in dentistry, coupled with rising awareness about the benefits of PACS for efficient data management and improved diagnostic accuracy, are key catalysts. Furthermore, advancements in AI-powered diagnostic tools integrated with PACS solutions are expected to significantly enhance treatment planning and patient outcomes, thereby fueling market demand. The continuous innovation in imaging hardware, leading to higher resolution and faster acquisition times, also contributes to the overall market dynamism.

Dental PACS Market Size (In Billion)

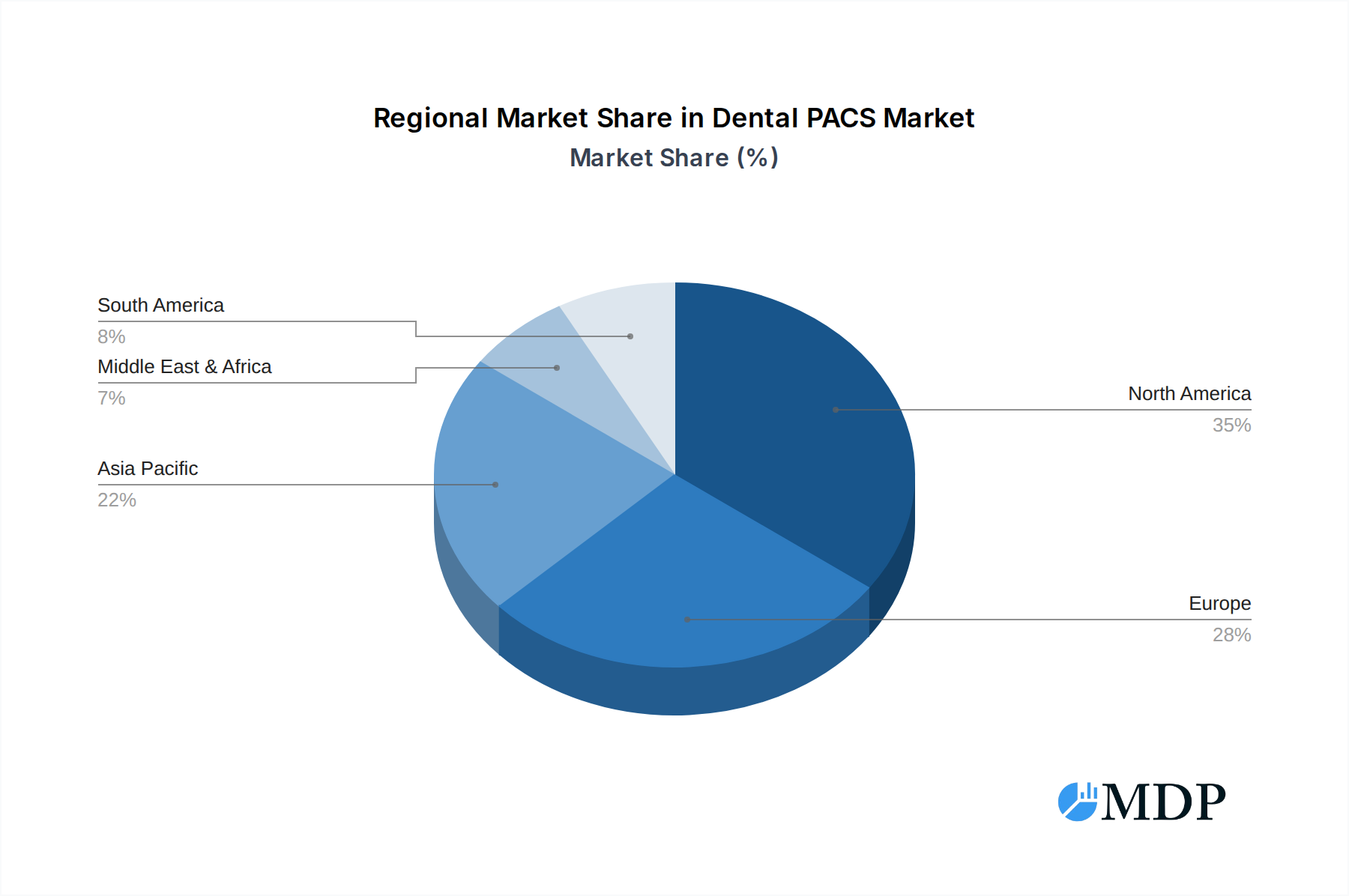

The market is segmented into various applications, including Dental X-rays, Intraoral Imaging, Extraoral Imaging, Panoramic Imaging, and Cephalometric Imaging. Within these applications, both 2D and 3D dental imaging, including Cone Beam CT (CBCT) imaging, are experiencing significant adoption. The growing prevalence of dental conditions and the increasing number of dental practitioners worldwide are contributing factors to the market's robust performance. Key industry players like DEXIS, LLC, Carestream Dental, and Vatech America are actively investing in research and development, launching innovative PACS solutions that cater to the evolving needs of dental professionals. North America currently leads the market share due to early adoption of advanced dental technologies and a strong healthcare infrastructure, with Asia Pacific anticipated to witness the fastest growth owing to increasing healthcare expenditure and a burgeoning dental tourism sector.

Dental PACS Company Market Share

Here is an SEO-optimized, engaging report description for Dental PACS, designed for maximum search visibility and to attract industry stakeholders.

This in-depth report, "Dental PACS Market Dynamics & Concentration 2019–2033," offers an unparalleled analysis of the global Dental Picture Archiving and Communication Systems (PACS) market. Covering a comprehensive study period from 2019 to 2033, with a base and estimated year of 2025, this report provides critical insights into market growth drivers, technological advancements, competitive landscapes, and future opportunities. Essential for dental practitioners, imaging equipment manufacturers, software developers, investors, and industry analysts, this report equips you with the actionable intelligence needed to navigate and capitalize on the evolving dental imaging sector.

With a projected market size reaching billions, this analysis delves into the core of Dental PACS, exploring applications such as Dental X-rays, Intraoral Imaging, Extraoral Imaging, Panoramic Imaging, and Cephalometric Imaging. It further dissects the market by types, including 2D Dental Imaging, 3D Dental Imaging, and Cone Beam CT (CBCT) Imaging. Gain a profound understanding of market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and significant M&A activities, with detailed metrics and actionable takeaways.

Key companies meticulously analyzed include: DEXIS, LLC, Carestream Dental, Vatech America, Apteryx Imaging Inc., SOTA Imaging, ImageWorks Corporation, Dürr Dental SE, Owandy Radiology, Planmeca Oy, Dentimax LLC, Mediadent. The report meticulously details key industry developments, market penetration rates, CAGR projections, and strategic outlooks, ensuring you have a holistic view of this dynamic and expanding market.

Dental PACS Market Dynamics & Concentration

The global Dental PACS market, projected to reach billions in value by 2033, exhibits a moderate to high concentration, with a few key players dominating significant market share. This concentration is driven by substantial R&D investments, the need for robust regulatory compliance, and the high cost of developing and deploying advanced imaging solutions. Innovation remains a primary driver, fueled by the constant demand for improved diagnostic accuracy, reduced radiation exposure, and seamless workflow integration within dental practices. Regulatory frameworks, particularly concerning data privacy (e.g., HIPAA, GDPR) and medical device certifications, play a crucial role in shaping market entry and product development, ensuring patient safety and data integrity. Product substitutes, though emerging in the form of AI-powered diagnostic tools and cloud-based image sharing platforms, are currently complementary rather than direct replacements for comprehensive PACS solutions. End-user trends indicate a strong preference for user-friendly interfaces, interoperability with existing practice management software, and cost-effective solutions, especially among small to medium-sized dental practices. Mergers and acquisitions (M&A) activities are strategically shaping the market landscape, with an estimated xx M&A deal count historically, as larger companies acquire innovative startups to expand their product portfolios and market reach. This dynamic environment necessitates continuous adaptation and strategic planning for sustained growth.

Dental PACS Industry Trends & Analysis

The Dental PACS market is poised for robust growth, driven by a confluence of technological advancements, increasing adoption of digital dentistry, and a growing awareness of the benefits of advanced imaging for early disease detection and treatment planning. The projected Compound Annual Growth Rate (CAGR) for the forecast period is an impressive xx%, indicating a sustained upward trajectory. Technological disruptions, such as the integration of Artificial Intelligence (AI) for automated image analysis, the advancement of Cone Beam CT (CBCT) technology for higher resolution and reduced scan times, and the increasing use of cloud-based PACS for enhanced accessibility and collaboration, are fundamentally reshaping the industry. Consumer preferences are evolving, with dental patients increasingly seeking minimally invasive procedures and precise diagnoses, which directly translates to a demand for sophisticated imaging solutions. Dental professionals are recognizing that effective PACS implementation leads to improved diagnostic capabilities, enhanced patient communication through clear visualization of dental conditions, and streamlined operational workflows. This leads to increased practice efficiency and potentially higher revenue streams. Competitive dynamics are intensifying, with established players and emerging innovators vying for market share by offering comprehensive solutions that encompass hardware, software, and ongoing support. Market penetration for digital dental imaging, a precursor to PACS adoption, continues to rise globally, creating a fertile ground for PACS implementation. The shift from film-based radiography to digital imaging has been a fundamental enabler, and the subsequent need for efficient storage, retrieval, and sharing of these digital images has propelled the Dental PACS market forward. Furthermore, the increasing prevalence of dental conditions requiring detailed 3D visualization, such as implantology, orthodontics, and endodontics, further amplifies the demand for advanced imaging modalities and the PACS systems to manage them.

Leading Markets & Segments in Dental PACS

The North America region currently holds a dominant position in the global Dental PACS market, driven by strong economic policies favoring healthcare technology adoption, a highly developed healthcare infrastructure, and a high rate of adoption of advanced dental technologies. Within North America, the United States spearheads this dominance due to significant investments in dental research and development, a large patient population seeking advanced dental care, and a well-established network of dental practices and imaging centers.

Key Drivers for Regional Dominance:

- Economic Policies: Favorable reimbursement policies for advanced diagnostic procedures and tax incentives for technology upgrades encourage widespread adoption of Dental PACS.

- Infrastructure Development: The robust presence of high-speed internet connectivity, advanced IT infrastructure, and a skilled workforce are crucial for seamless PACS implementation and operation.

- Technological Advancements: Early and rapid adoption of innovations like CBCT and AI-driven analytics by dental professionals in the region.

- Healthcare Spending: High per capita healthcare expenditure translates to greater willingness among dental practices and patients to invest in advanced imaging solutions.

- Regulatory Landscape: A clear and supportive regulatory environment for medical devices facilitates market entry and growth for PACS providers.

In terms of Applications, Dental X-rays and Intraoral Imaging represent the largest segments, due to their fundamental role in routine dental examinations and diagnostics. However, the 3D Dental Imaging segment, particularly Cone Beam CT (CBCT) Imaging, is experiencing the fastest growth. This surge is propelled by its indispensable role in complex procedures like dental implantology, orthodontics, and maxillofacial surgery, where detailed three-dimensional anatomical information is paramount for precise treatment planning and execution. The increasing availability of more affordable and compact CBCT units is further democratizing access to this advanced technology across a wider range of dental practices.

Dental PACS Product Developments

The Dental PACS market is characterized by continuous product innovation focused on enhancing diagnostic accuracy, improving workflow efficiency, and ensuring data security. Recent developments include the integration of AI algorithms for automated image analysis, lesion detection, and treatment outcome prediction. Enhanced 3D visualization tools, real-time image processing capabilities, and seamless integration with intraoral scanners and practice management software are also key trends. These innovations provide dental professionals with unparalleled diagnostic precision and streamline practice operations, offering a significant competitive advantage and catering to the growing demand for advanced, patient-centric dental care. The market fit for these products is exceptionally strong as they directly address the evolving needs of modern dentistry.

Key Drivers of Dental PACS Growth

The significant growth of the Dental PACS market is propelled by several interconnected factors. Technologically, the continuous evolution of imaging hardware, such as higher resolution sensors and more compact CBCT units, fuels the demand for sophisticated PACS to manage this rich data. The increasing sophistication of AI and machine learning algorithms for image analysis and diagnostic assistance further enhances the value proposition of PACS. Economically, rising global healthcare expenditure, particularly in emerging economies, and the increasing affordability of digital imaging technology are making PACS more accessible. The growing understanding among dental professionals of the long-term cost savings and improved patient outcomes associated with digital imaging and PACS implementation also drives adoption. Regulatory drivers, such as stringent mandates for digital record-keeping and data security, implicitly encourage the adoption of PACS solutions that comply with these standards.

Challenges in the Dental PACS Market

Despite its robust growth trajectory, the Dental PACS market faces several significant challenges. High initial investment costs for both hardware and software can be a barrier, particularly for smaller dental practices or those in developing regions. The complexity of integrating new PACS systems with existing IT infrastructure and legacy software can lead to workflow disruptions and require substantial technical expertise. Cybersecurity threats and the need for stringent data privacy compliance (e.g., HIPAA, GDPR) represent ongoing concerns, demanding robust security measures and continuous vigilance. Furthermore, the fragmented nature of the market and the presence of numerous vendors offering a wide range of solutions can lead to decision paralysis for buyers. Fierce competition can also put pressure on profit margins, requiring companies to constantly innovate and optimize their offerings to remain competitive.

Emerging Opportunities in Dental PACS

Emerging opportunities in the Dental PACS market are primarily driven by technological breakthroughs and strategic market expansion. The increasing integration of Artificial Intelligence (AI) for enhanced diagnostic capabilities, such as automated caries detection and periodontal disease assessment, presents a significant growth catalyst. Cloud-based PACS solutions are gaining traction, offering enhanced accessibility, scalability, and collaboration features, particularly attractive for multi-location dental practices and dental schools. The growing demand for integrated workflows, where PACS seamlessly connect with practice management software, digital impression systems, and 3D printers, creates opportunities for comprehensive solution providers. Furthermore, expansion into emerging markets in Asia-Pacific and Latin America, where the adoption of digital dentistry is rapidly increasing, offers substantial untapped potential. Strategic partnerships between PACS vendors, dental equipment manufacturers, and dental software developers are also crucial for creating bundled solutions and expanding market reach.

Leading Players in the Dental PACS Sector

- DEXIS, LLC

- Carestream Dental

- Vatech America

- Apteryx Imaging Inc.

- SOTA Imaging

- ImageWorks Corporation

- Dürr Dental SE

- Owandy Radiology

- Planmeca Oy

- Dentimax LLC

- Mediadent

Key Milestones in Dental PACS Industry

- 2019: Introduction of advanced AI algorithms for dental image analysis, enhancing diagnostic accuracy.

- 2020: Increased adoption of cloud-based PACS solutions, offering greater flexibility and remote access.

- 2021: Significant advancements in CBCT technology, leading to higher resolution and reduced scan times.

- 2022: Key strategic partnerships formed to create integrated dental workflow solutions.

- 2023: Heightened focus on cybersecurity and data protection protocols in PACS development.

- 2024: Emergence of portable and more affordable CBCT units, driving wider market penetration.

- 2025: Continued innovation in AI-driven diagnostics and predictive analytics for dental treatment planning.

Strategic Outlook for Dental PACS Market

The strategic outlook for the Dental PACS market is overwhelmingly positive, with growth accelerators centered on technological innovation and market expansion. The continued development and integration of AI and machine learning algorithms will be paramount, offering enhanced diagnostic accuracy and predictive analytics that will redefine dental care. The shift towards cloud-based infrastructure will provide scalability and accessibility, catering to the evolving needs of dental practices worldwide. Focus on interoperability and seamless integration with other dental technologies will be crucial for creating holistic digital ecosystems. Furthermore, strategic expansion into underpenetrated emerging markets, coupled with strategic acquisitions to consolidate market share and acquire new technologies, will shape the competitive landscape. Dental PACS providers that prioritize user experience, data security, and demonstrable return on investment will be best positioned for sustained success and market leadership in the coming decade.

Dental PACS Segmentation

-

1. Application

- 1.1. Dental X-rays

- 1.2. Intraoral Imaging

- 1.3. Extraoral Imaging

- 1.4. Panoramic Imaging

- 1.5. Cephalometric Imaging

-

2. Types

- 2.1. 2D Dental Imaging

- 2.2. 3D Dental Imaging

- 2.3. Cone Beam CT (CBCT) Imaging

Dental PACS Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Dental PACS Regional Market Share

Geographic Coverage of Dental PACS

Dental PACS REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Dental PACS Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Dental X-rays

- 5.1.2. Intraoral Imaging

- 5.1.3. Extraoral Imaging

- 5.1.4. Panoramic Imaging

- 5.1.5. Cephalometric Imaging

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 2D Dental Imaging

- 5.2.2. 3D Dental Imaging

- 5.2.3. Cone Beam CT (CBCT) Imaging

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Dental PACS Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Dental X-rays

- 6.1.2. Intraoral Imaging

- 6.1.3. Extraoral Imaging

- 6.1.4. Panoramic Imaging

- 6.1.5. Cephalometric Imaging

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 2D Dental Imaging

- 6.2.2. 3D Dental Imaging

- 6.2.3. Cone Beam CT (CBCT) Imaging

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Dental PACS Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Dental X-rays

- 7.1.2. Intraoral Imaging

- 7.1.3. Extraoral Imaging

- 7.1.4. Panoramic Imaging

- 7.1.5. Cephalometric Imaging

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 2D Dental Imaging

- 7.2.2. 3D Dental Imaging

- 7.2.3. Cone Beam CT (CBCT) Imaging

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Dental PACS Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Dental X-rays

- 8.1.2. Intraoral Imaging

- 8.1.3. Extraoral Imaging

- 8.1.4. Panoramic Imaging

- 8.1.5. Cephalometric Imaging

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 2D Dental Imaging

- 8.2.2. 3D Dental Imaging

- 8.2.3. Cone Beam CT (CBCT) Imaging

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Dental PACS Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Dental X-rays

- 9.1.2. Intraoral Imaging

- 9.1.3. Extraoral Imaging

- 9.1.4. Panoramic Imaging

- 9.1.5. Cephalometric Imaging

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 2D Dental Imaging

- 9.2.2. 3D Dental Imaging

- 9.2.3. Cone Beam CT (CBCT) Imaging

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Dental PACS Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Dental X-rays

- 10.1.2. Intraoral Imaging

- 10.1.3. Extraoral Imaging

- 10.1.4. Panoramic Imaging

- 10.1.5. Cephalometric Imaging

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 2D Dental Imaging

- 10.2.2. 3D Dental Imaging

- 10.2.3. Cone Beam CT (CBCT) Imaging

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 DEXIS

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 LLC

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Carestream Dental

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Vatech America

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Apteryx Imaging Inc.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 SOTA Imaging

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ImageWorks Corporation

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Dürr Dental SE

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Owandy Radiology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Planmeca Oy

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Dentimax LLC

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Mediadent

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 DEXIS

List of Figures

- Figure 1: Global Dental PACS Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Dental PACS Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Dental PACS Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Dental PACS Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Dental PACS Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Dental PACS Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Dental PACS Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Dental PACS Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Dental PACS Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Dental PACS Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Dental PACS Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Dental PACS Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Dental PACS Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Dental PACS Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Dental PACS Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Dental PACS Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Dental PACS Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Dental PACS Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Dental PACS Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Dental PACS Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Dental PACS Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Dental PACS Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Dental PACS Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Dental PACS Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Dental PACS Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Dental PACS Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Dental PACS Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Dental PACS Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Dental PACS Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Dental PACS Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Dental PACS Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dental PACS Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Dental PACS Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Dental PACS Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Dental PACS Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Dental PACS Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Dental PACS Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Dental PACS Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Dental PACS Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Dental PACS Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Dental PACS Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Dental PACS Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Dental PACS Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Dental PACS Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Dental PACS Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Dental PACS Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Dental PACS Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Dental PACS Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Dental PACS Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Dental PACS Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dental PACS?

The projected CAGR is approximately 10.2%.

2. Which companies are prominent players in the Dental PACS?

Key companies in the market include DEXIS, LLC, Carestream Dental, Vatech America, Apteryx Imaging Inc., SOTA Imaging, ImageWorks Corporation, Dürr Dental SE, Owandy Radiology, Planmeca Oy, Dentimax LLC, Mediadent.

3. What are the main segments of the Dental PACS?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dental PACS," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dental PACS report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dental PACS?

To stay informed about further developments, trends, and reports in the Dental PACS, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence