Key Insights

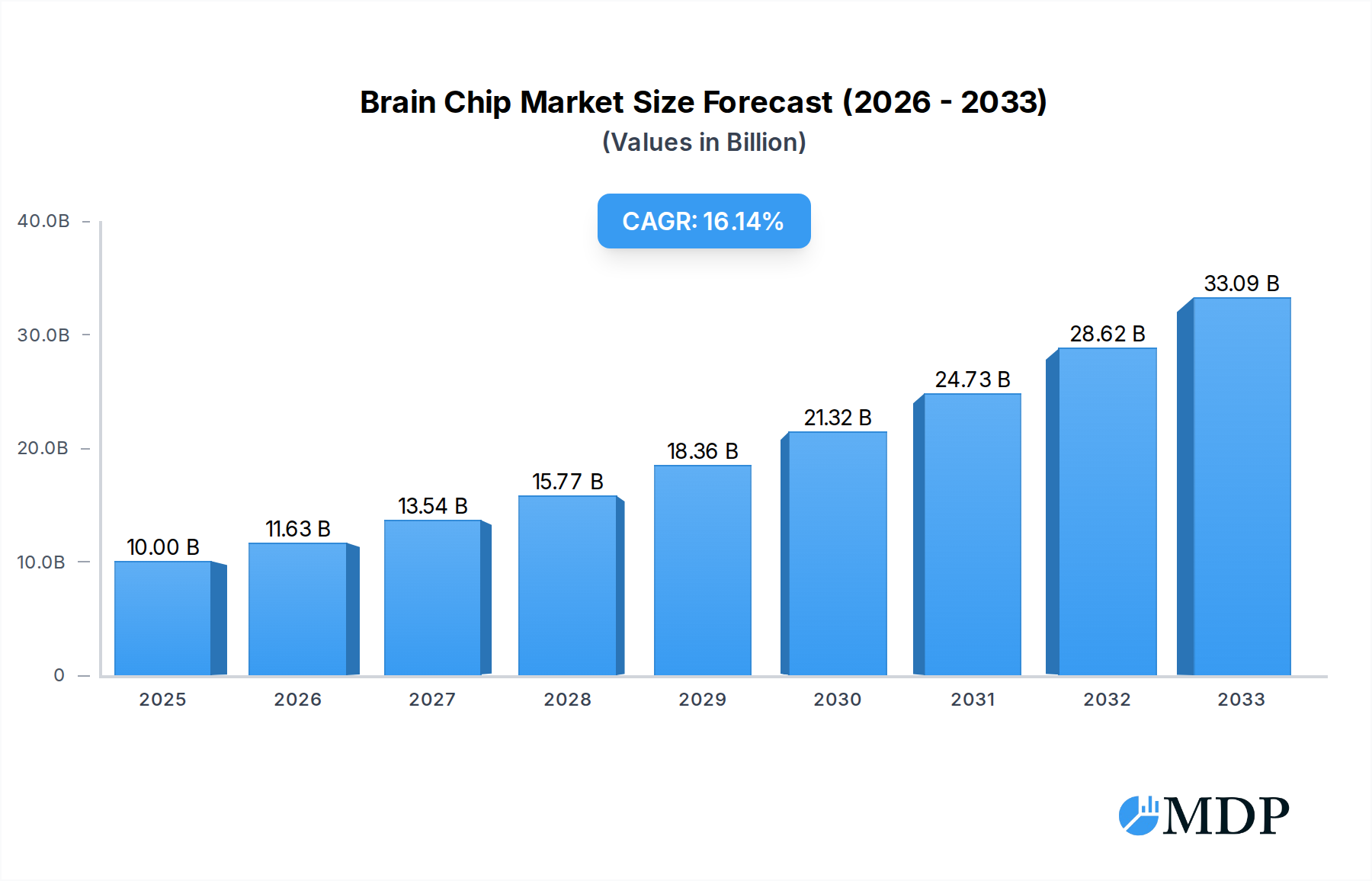

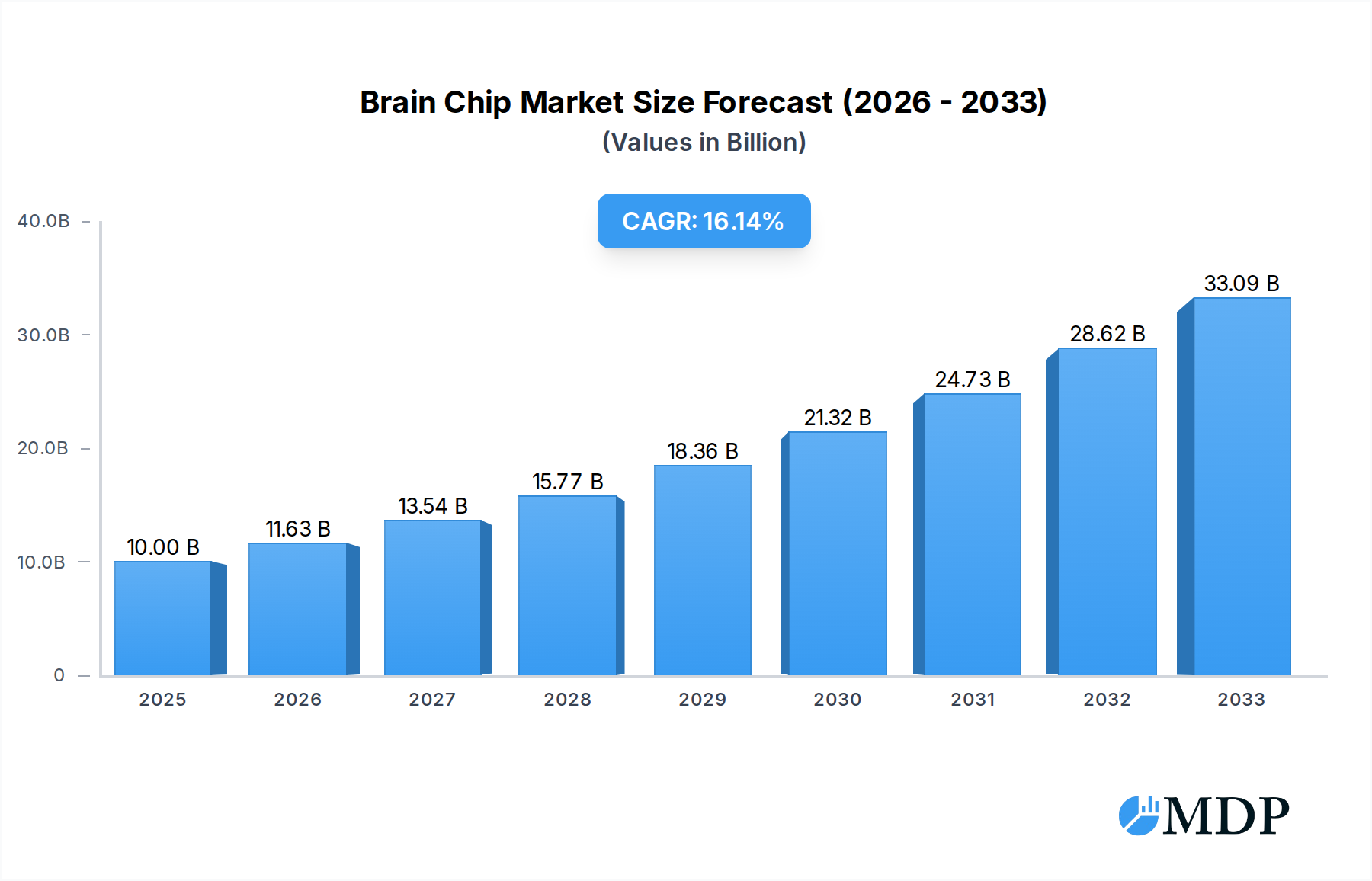

The global Brain Chip market is poised for significant expansion, projected to reach $10 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 16.32% through 2033. This impressive trajectory is primarily fueled by advancements in neural interface technology, increasing adoption by pharmaceutical and biotech companies for drug discovery and toxicity testing, and a growing demand from academic and research institutions for sophisticated in-vitro models. The market is experiencing a surge in innovation, with a clear trend towards developing sophisticated organ-on-a-chip models that accurately replicate the complex human brain environment. This allows for more reliable preclinical testing, reducing the need for animal models and accelerating the drug development process. Furthermore, the increasing prevalence of neurological disorders and brain injuries is driving the demand for advanced research tools and therapeutic development, further bolstering market growth.

Brain Chip Market Size (In Billion)

The market's growth is strategically segmented by application and patient type. Pharmaceutical and biotech companies represent a dominant segment, leveraging brain chip technology for high-throughput screening and personalized medicine initiatives. Academic and research institutions are also significant contributors, utilizing these advanced models for fundamental neuroscience research. While the market is largely driven by these key users, the ultimate impact will be seen in patients suffering from conditions such as paralysis, stroke, and brain injuries, for whom these technologies hold immense promise for future treatment strategies. Emerging applications and the continued refinement of these bio-engineered systems are expected to unlock new therapeutic avenues and diagnostic tools, solidifying the Brain Chip market's critical role in the future of healthcare and neuroscience research.

Brain Chip Company Market Share

Brain Chip Market Dynamics & Concentration

The global brain chip market is characterized by a moderate to high concentration driven by significant technological advancements and substantial research and development investments. Key innovation drivers include the increasing prevalence of neurological disorders, the pursuit of novel therapeutic solutions for paralysis, stroke, and brain injuries, and the relentless drive for enhanced human-computer interaction. Regulatory frameworks are evolving, with agencies like the FDA actively reviewing and approving innovative neurotechnology. However, the path to widespread adoption is influenced by stringent safety protocols and ethical considerations. Product substitutes, such as advanced rehabilitation therapies and traditional prosthetics, present ongoing competition, but brain chip technology offers a unique direct neural interface. End-user trends are increasingly focused on restoring lost function and improving quality of life, with a growing demand for personalized and minimally invasive solutions. Mergers and acquisitions (M&A) activity has been a significant feature, with XX M&A deals recorded between 2019 and 2024, reflecting consolidation and strategic integration of specialized expertise. Major players are actively seeking to acquire smaller, innovative startups to gain access to cutting-edge technologies and expand their intellectual property portfolios. The market share landscape is dynamic, with leading companies continually vying for dominance through technological breakthroughs and strategic partnerships.

Brain Chip Industry Trends & Analysis

The brain chip industry is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of XX% between 2025 and 2033. This impressive growth trajectory is fueled by a confluence of powerful market growth drivers, including the escalating global burden of neurological conditions such as Alzheimer's disease, Parkinson's disease, epilepsy, and the long-term effects of stroke and traumatic brain injury. The increasing incidence of these debilitating conditions necessitates advanced therapeutic interventions, positioning brain chip technology as a critical solution for restoring neural function and improving patient outcomes. Technological disruptions are at the forefront of this expansion, with continuous innovation in microelectronics, biocompatible materials, and sophisticated AI algorithms enabling more precise and effective neural interfaces. Miniaturization and wireless capabilities are key advancements, leading to less invasive procedures and enhanced user comfort. Consumer preferences are shifting towards solutions that offer a higher degree of autonomy and independence for individuals with disabilities. The demand for brain-computer interfaces (BCIs) that can facilitate communication, control external devices, and even restore motor functions is surging. Competitive dynamics within the industry are intense, marked by a race for patent protection, strategic collaborations between research institutions and commercial entities, and significant venture capital funding. The market penetration of brain chip solutions, while still nascent, is expected to accelerate as regulatory approvals broaden and clinical efficacy is further validated. The development of closed-loop systems, which can both monitor brain activity and deliver targeted stimulation, represents a significant frontier in therapeutic innovation. Furthermore, the application of brain chip technology in non-therapeutic areas, such as cognitive enhancement and advanced human-machine interfaces for augmented reality, is also contributing to the overall market dynamism, opening up new avenues for revenue generation and innovation.

Leading Markets & Segments in Brain Chip

The Pharmaceutical and Biotech Companies segment currently dominates the brain chip market, representing an estimated XX% of the total market value. This dominance is driven by substantial investment in research and development for novel neurological treatments and the increasing adoption of brain-computer interfaces (BCIs) as therapeutic tools. Academic and Research Institutions also play a pivotal role, constituting XX% of the market, by spearheading foundational research, developing new algorithms, and validating the efficacy of brain chip technologies.

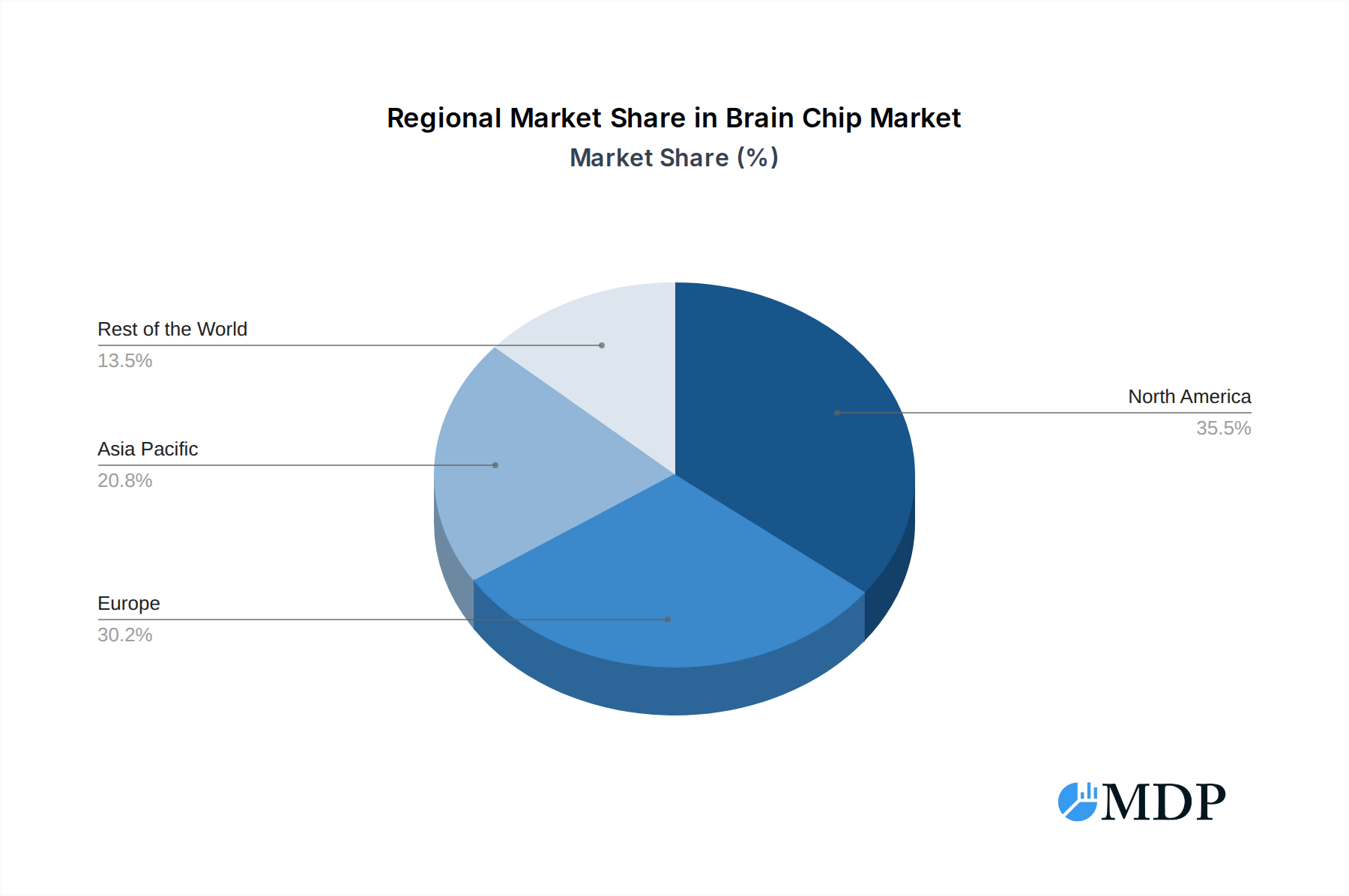

Dominant Region/Country: North America leads the global brain chip market, accounting for approximately XX% of the market share. This leadership is attributed to a robust healthcare infrastructure, significant government funding for neuroscience research, and the presence of leading research institutions and private companies actively engaged in brain chip development.

Key Drivers for Dominance:

- Economic Policies: Favorable government policies and grants supporting neurotechnology research and development.

- Infrastructure: Advanced healthcare systems and well-established clinical trial networks facilitate rapid product development and validation.

- Investment: High levels of private and public investment in R&D and venture capital funding for startups.

- Technological Advancements: A strong ecosystem of technological innovation, including microfabrication, AI, and neuroscience expertise.

Dominant Type Segment: The "for Paralyzed Patients" segment holds the largest share within the types category, estimated at XX%. This is due to the profound unmet need for restoring motor function and independence in individuals with spinal cord injuries and other forms of paralysis.

Key Drivers for Type Segment Dominance:

- Unmet Medical Needs: The critical need for solutions to restore mobility and communication for paralyzed individuals.

- Technological Maturity: Earlier advancements and more established research in BCIs for motor control.

- Clinical Validation: A growing body of clinical evidence demonstrating the efficacy of brain chip implants for paralysis.

The for Stroke Patients segment is a rapidly growing area, projected to see significant expansion due to the increasing global incidence of strokes and the potential for brain chips to aid in motor and cognitive rehabilitation. The for Brain Injury Patients segment also presents substantial growth opportunities as awareness and treatment options for traumatic brain injuries continue to advance.

Brain Chip Product Developments

The brain chip market is witnessing rapid product innovation characterized by advancements in biocompatibility, miniaturization, and signal processing. Companies are focusing on developing high-density electrode arrays for enhanced neural signal acquisition and targeted stimulation. Key applications include restoring motor function for paralyzed patients, facilitating communication for those with severe speech impairments, and aiding in the rehabilitation of stroke and brain injury survivors. Competitive advantages are being built on improved surgical implantation techniques, longer device longevity, and the integration of sophisticated AI algorithms for seamless brain-computer interaction. Emerging product trends point towards wireless and minimally invasive designs, aiming to reduce patient discomfort and increase accessibility.

Key Drivers of Brain Chip Growth

The brain chip market is propelled by several key growth drivers. Technologically, the rapid advancements in neuroscience, artificial intelligence, and microfabrication are enabling more sophisticated and effective brain-computer interfaces. Economically, increasing healthcare expenditure globally, particularly in neurodegenerative disease research and treatment, fuels investment in this sector. Regulatory bodies are becoming more receptive to innovative neurotechnologies, streamlining approval processes for promising brain chip applications. Furthermore, the rising global prevalence of neurological disorders such as Parkinson's, epilepsy, and stroke, alongside an aging population, creates a substantial and growing demand for solutions that can restore lost neurological function and improve quality of life. The push for personalized medicine also plays a crucial role, with brain chips offering the potential for highly tailored therapeutic interventions.

Challenges in the Brain Chip Market

Despite its promising growth, the brain chip market faces significant challenges. Regulatory hurdles remain a major concern, with stringent safety and efficacy requirements for implantable medical devices. The high cost of research, development, and manufacturing also presents a barrier to entry and affordability. Ethical considerations surrounding neural interfaces, including data privacy and potential misuse, require careful navigation. Supply chain complexities for specialized components and challenges in achieving long-term biocompatibility and preventing tissue rejection are also critical issues. Furthermore, public perception and acceptance of invasive brain implant technology can influence market penetration, alongside the need for extensive patient and clinician training.

Emerging Opportunities in Brain Chip

Emerging opportunities in the brain chip market are primarily driven by technological breakthroughs and strategic market expansion. The development of non-invasive or minimally invasive brain-computer interfaces presents a significant growth catalyst, broadening patient accessibility and reducing procedural risks. Advancements in AI and machine learning are enabling more sophisticated decoding of neural signals, leading to improved prosthetic control and communication capabilities. Strategic partnerships between neurotechnology companies, pharmaceutical firms, and academic institutions are accelerating research and clinical trials, fostering faster innovation cycles. Furthermore, the expanding application of brain chip technology beyond therapeutic uses, into areas like cognitive enhancement and advanced human-machine interfaces, opens vast new market potential and revenue streams.

Leading Players in the Brain Chip Sector

- Emulate

- TissUse

- Hesperos

- CN Bio Innovations

- Tara Biosystems

- Draper Laboratory

- Mimetas

- Nortis

- Micronit Microtechnologies B.V.

- Kirkstall

- Cherry Biotech SAS

- Else Kooi Laboratory

Key Milestones in Brain Chip Industry

- 2019: Launch of new advanced electrode materials with enhanced biocompatibility.

- 2020: Significant breakthroughs in AI algorithms for real-time neural signal interpretation.

- 2021: First successful clinical trials demonstrating restoration of complex motor functions in paralyzed patients.

- 2022: Approval of novel, minimally invasive brain chip implantation techniques by regulatory bodies.

- 2023: Increased venture capital funding rounds for several key brain chip startups.

- 2024: Introduction of wireless and rechargeable brain chip systems enhancing user convenience.

Strategic Outlook for Brain Chip Market

The strategic outlook for the brain chip market is exceptionally promising, driven by the convergence of technological innovation and a growing global demand for advanced neurological solutions. Future growth will be accelerated by continued investment in research and development, focusing on creating more sophisticated, less invasive, and highly personalized brain-computer interfaces. Strategic alliances between industry leaders, academic institutions, and healthcare providers will be crucial for speeding up clinical translation and market adoption. The expansion into new therapeutic areas, such as treating chronic pain, mental health disorders, and accelerating cognitive rehabilitation, presents significant untapped potential. Furthermore, the increasing integration of brain chip technology with other emerging fields like robotics and virtual reality will unlock novel applications and revenue streams, solidifying its position as a transformative technology in healthcare and beyond.

Brain Chip Segmentation

-

1. Application

- 1.1. Pharmaceutical and Biotech Companies

- 1.2. Academic and Research Institutions

- 1.3. End Users

-

2. Types

- 2.1. for Paralyzed Patients

- 2.2. for Stroke Patients

- 2.3. for Brain Injury Patients

- 2.4. Others

Brain Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Brain Chip Regional Market Share

Geographic Coverage of Brain Chip

Brain Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.32% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Brain Chip Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pharmaceutical and Biotech Companies

- 5.1.2. Academic and Research Institutions

- 5.1.3. End Users

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. for Paralyzed Patients

- 5.2.2. for Stroke Patients

- 5.2.3. for Brain Injury Patients

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Brain Chip Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pharmaceutical and Biotech Companies

- 6.1.2. Academic and Research Institutions

- 6.1.3. End Users

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. for Paralyzed Patients

- 6.2.2. for Stroke Patients

- 6.2.3. for Brain Injury Patients

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Brain Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pharmaceutical and Biotech Companies

- 7.1.2. Academic and Research Institutions

- 7.1.3. End Users

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. for Paralyzed Patients

- 7.2.2. for Stroke Patients

- 7.2.3. for Brain Injury Patients

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Brain Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pharmaceutical and Biotech Companies

- 8.1.2. Academic and Research Institutions

- 8.1.3. End Users

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. for Paralyzed Patients

- 8.2.2. for Stroke Patients

- 8.2.3. for Brain Injury Patients

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Brain Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pharmaceutical and Biotech Companies

- 9.1.2. Academic and Research Institutions

- 9.1.3. End Users

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. for Paralyzed Patients

- 9.2.2. for Stroke Patients

- 9.2.3. for Brain Injury Patients

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Brain Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pharmaceutical and Biotech Companies

- 10.1.2. Academic and Research Institutions

- 10.1.3. End Users

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. for Paralyzed Patients

- 10.2.2. for Stroke Patients

- 10.2.3. for Brain Injury Patients

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Emulate

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 TissUse

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Hesperos

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 CN Bio Innovations

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Tara Biosystems

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Draper Laboratory

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Mimetas

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Nortis

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Micronit Microtechnologies B.V.

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Kirkstall

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Cherry Biotech SAS

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Else Kooi Laboratory

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Emulate

List of Figures

- Figure 1: Global Brain Chip Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Brain Chip Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Brain Chip Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Brain Chip Volume (K), by Application 2025 & 2033

- Figure 5: North America Brain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Brain Chip Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Brain Chip Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Brain Chip Volume (K), by Types 2025 & 2033

- Figure 9: North America Brain Chip Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Brain Chip Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Brain Chip Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Brain Chip Volume (K), by Country 2025 & 2033

- Figure 13: North America Brain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Brain Chip Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Brain Chip Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Brain Chip Volume (K), by Application 2025 & 2033

- Figure 17: South America Brain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Brain Chip Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Brain Chip Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Brain Chip Volume (K), by Types 2025 & 2033

- Figure 21: South America Brain Chip Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Brain Chip Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Brain Chip Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Brain Chip Volume (K), by Country 2025 & 2033

- Figure 25: South America Brain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Brain Chip Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Brain Chip Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Brain Chip Volume (K), by Application 2025 & 2033

- Figure 29: Europe Brain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Brain Chip Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Brain Chip Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Brain Chip Volume (K), by Types 2025 & 2033

- Figure 33: Europe Brain Chip Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Brain Chip Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Brain Chip Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Brain Chip Volume (K), by Country 2025 & 2033

- Figure 37: Europe Brain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Brain Chip Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Brain Chip Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Brain Chip Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Brain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Brain Chip Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Brain Chip Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Brain Chip Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Brain Chip Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Brain Chip Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Brain Chip Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Brain Chip Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Brain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Brain Chip Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Brain Chip Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Brain Chip Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Brain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Brain Chip Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Brain Chip Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Brain Chip Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Brain Chip Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Brain Chip Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Brain Chip Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Brain Chip Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Brain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Brain Chip Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Brain Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Brain Chip Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Brain Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Brain Chip Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Brain Chip Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Brain Chip Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Brain Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Brain Chip Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Brain Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Brain Chip Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Brain Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Brain Chip Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Brain Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Brain Chip Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Brain Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Brain Chip Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Brain Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Brain Chip Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Brain Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Brain Chip Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Brain Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Brain Chip Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Brain Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Brain Chip Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Brain Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Brain Chip Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Brain Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Brain Chip Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Brain Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Brain Chip Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Brain Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Brain Chip Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Brain Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Brain Chip Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Brain Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Brain Chip Volume K Forecast, by Country 2020 & 2033

- Table 79: China Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Brain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Brain Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Brain Chip Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Brain Chip?

The projected CAGR is approximately 16.32%.

2. Which companies are prominent players in the Brain Chip?

Key companies in the market include Emulate, TissUse, Hesperos, CN Bio Innovations, Tara Biosystems, Draper Laboratory, Mimetas, Nortis, Micronit Microtechnologies B.V., Kirkstall, Cherry Biotech SAS, Else Kooi Laboratory.

3. What are the main segments of the Brain Chip?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Brain Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Brain Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Brain Chip?

To stay informed about further developments, trends, and reports in the Brain Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence