Key Insights

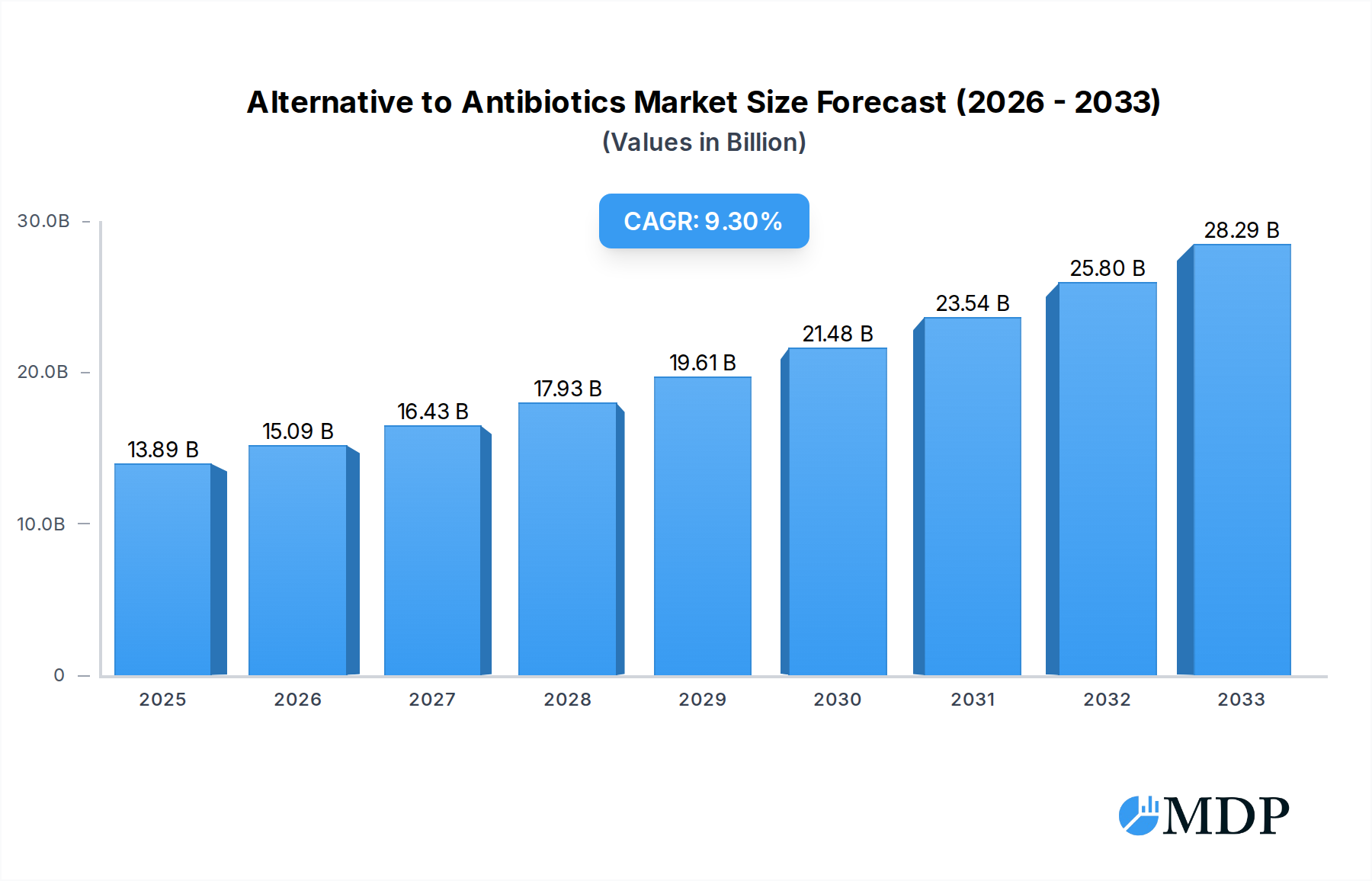

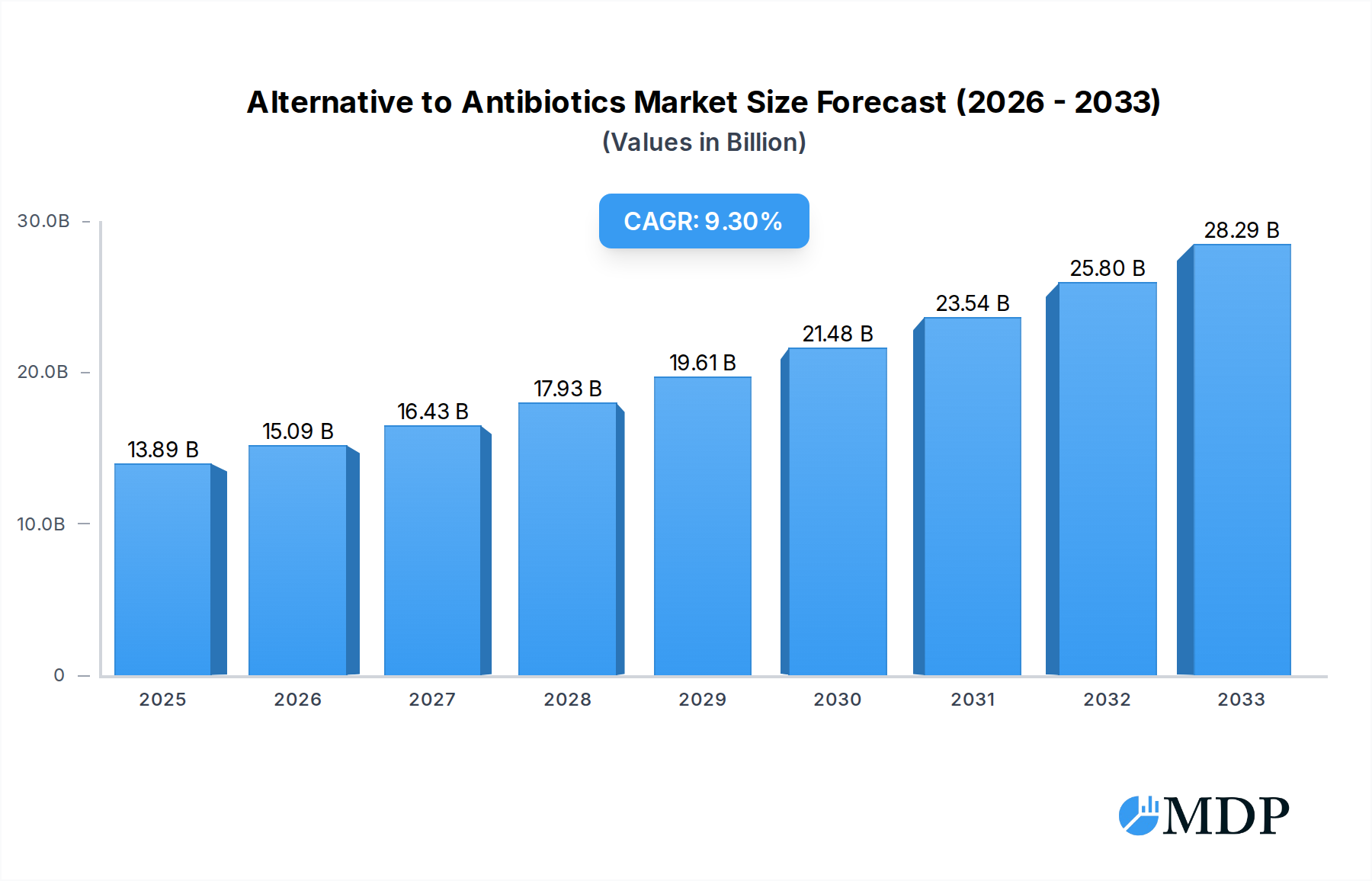

The global market for alternatives to antibiotics is experiencing robust expansion, driven by increasing consumer demand for healthier food products and growing concerns over antibiotic resistance. With a projected market size of USD 13.89 billion in 2025, this sector is poised for significant growth, exhibiting a compound annual growth rate (CAGR) of 8.72% during the forecast period of 2025-2033. This upward trajectory is fueled by several key factors. The food and beverage industry is a primary driver, actively seeking antimicrobial proteins, bacteriophages, and probiotics to enhance food safety and extend shelf life without relying on conventional antibiotics. Similarly, the pharmaceutical and dietary supplement sectors are heavily investing in these alternatives for therapeutic and preventative health applications, spurred by regulatory pressures and a growing understanding of the microbiome.

Alternative to Antibiotics Market Size (In Billion)

The market is segmented into various applications including food & beverage, drugs, and dietary supplements, with a notable presence in antimicrobial proteins, bacteriophages, and probiotics as primary types. Geographically, North America and Europe currently hold substantial market shares due to advanced research and development capabilities and strong regulatory frameworks supporting these innovations. However, the Asia Pacific region is expected to witness the fastest growth, driven by increasing disposable incomes, a rising prevalence of lifestyle diseases, and a growing awareness of the health benefits associated with probiotic and prebiotic-rich foods. Restraints include the high cost of research and development for novel alternatives and challenges in consumer education and acceptance. Nevertheless, ongoing technological advancements and strategic collaborations among key players like DSM, DuPont (Danisco), and Chr. Hansen are expected to overcome these hurdles and propel the market forward.

Alternative to Antibiotics Company Market Share

Unlock unprecedented insights into the rapidly expanding alternative to antibiotics market with this in-depth industry report. Spanning the historical period of 2019-2024, the base year of 2025, and a forecast period extending to 2033, this analysis offers a strategic roadmap for stakeholders navigating the burgeoning demand for antibiotic alternatives. Discover market dynamics, technological advancements, key players, and future growth trajectories in a market projected to reach multi-billion dollar valuations. This report is your essential guide to capitalizing on the shift away from traditional antibiotics across Food & Beverage, Drugs, and Dietary Supplements applications.

Alternative to Antibiotics Market Dynamics & Concentration

The alternative to antibiotics market is characterized by a dynamic blend of innovation and strategic maneuvering. Market concentration is moderately fragmented, with a few dominant players like DSM, DuPont (Danisco), and Chr. Hansen holding significant market share, estimated at over 50% collectively. However, the emergence of specialized companies such as BioGaia, Yakult, and Novozymes, alongside innovative startups, indicates a healthy competitive landscape. Key innovation drivers include the escalating global concern over antibiotic resistance, stringent government regulations restricting the use of traditional antibiotics in animal feed and human medicine, and a growing consumer preference for natural and sustainable health solutions. Product substitutes, while present, often lack the efficacy or broad applicability of established probiotics, antimicrobial proteins, and bacteriophages. End-user trends highlight a strong demand for effective and safe alternatives in animal husbandry, human health, and food preservation. Merger and acquisition (M&A) activities are on the rise, with an estimated 15-20 significant deals in the historical period, driven by the desire to consolidate intellectual property, expand product portfolios, and gain market access. The projected M&A deal count for the forecast period is expected to increase by 25% annually, further shaping market concentration.

Alternative to Antibiotics Industry Trends & Analysis

The alternative to antibiotics industry is experiencing robust growth, driven by a confluence of factors creating a compelling market narrative. The global market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 12.5% from 2025 to 2033, reaching an estimated market size of over one hundred billion dollars by the end of the forecast period. This expansion is primarily fueled by the escalating threat of antimicrobial resistance (AMR), a public health crisis demanding immediate and sustainable solutions. Governments worldwide are implementing stricter regulations on antibiotic use, particularly in agriculture, incentivizing the adoption of alternatives. Consumer awareness regarding the health benefits of probiotics and the risks associated with antibiotic residues in food products is a significant market penetration driver, especially within the Food & Beverage and Dietary Supplements segments.

Technological disruptions are at the forefront of this evolution. Advancements in genetic engineering, fermentation technologies, and the identification of novel antimicrobial proteins and bacteriophages are expanding the efficacy and application range of these alternatives. Companies are investing heavily in research and development to discover new strains of probiotics with targeted health benefits and to develop more potent bacteriophage therapies.

Competitive dynamics are intensifying, with established players like DSM, DuPont (Danisco), and Chr. Hansen leveraging their R&D capabilities and global distribution networks. Simultaneously, agile biotechnology firms and ingredient suppliers such as Lallemand, China-Biotics, and Novozymes are carving out niche markets and driving innovation. The increasing demand for natural and scientifically validated health solutions is pushing market penetration for well-researched probiotics and specialized antimicrobial proteins. The Drugs segment, though facing longer regulatory approval cycles, presents immense long-term potential for novel therapeutic applications of bacteriophages and antimicrobial proteins. The overall industry trajectory points towards a sustained period of growth and innovation.

Leading Markets & Segments in Alternative to Antibiotics

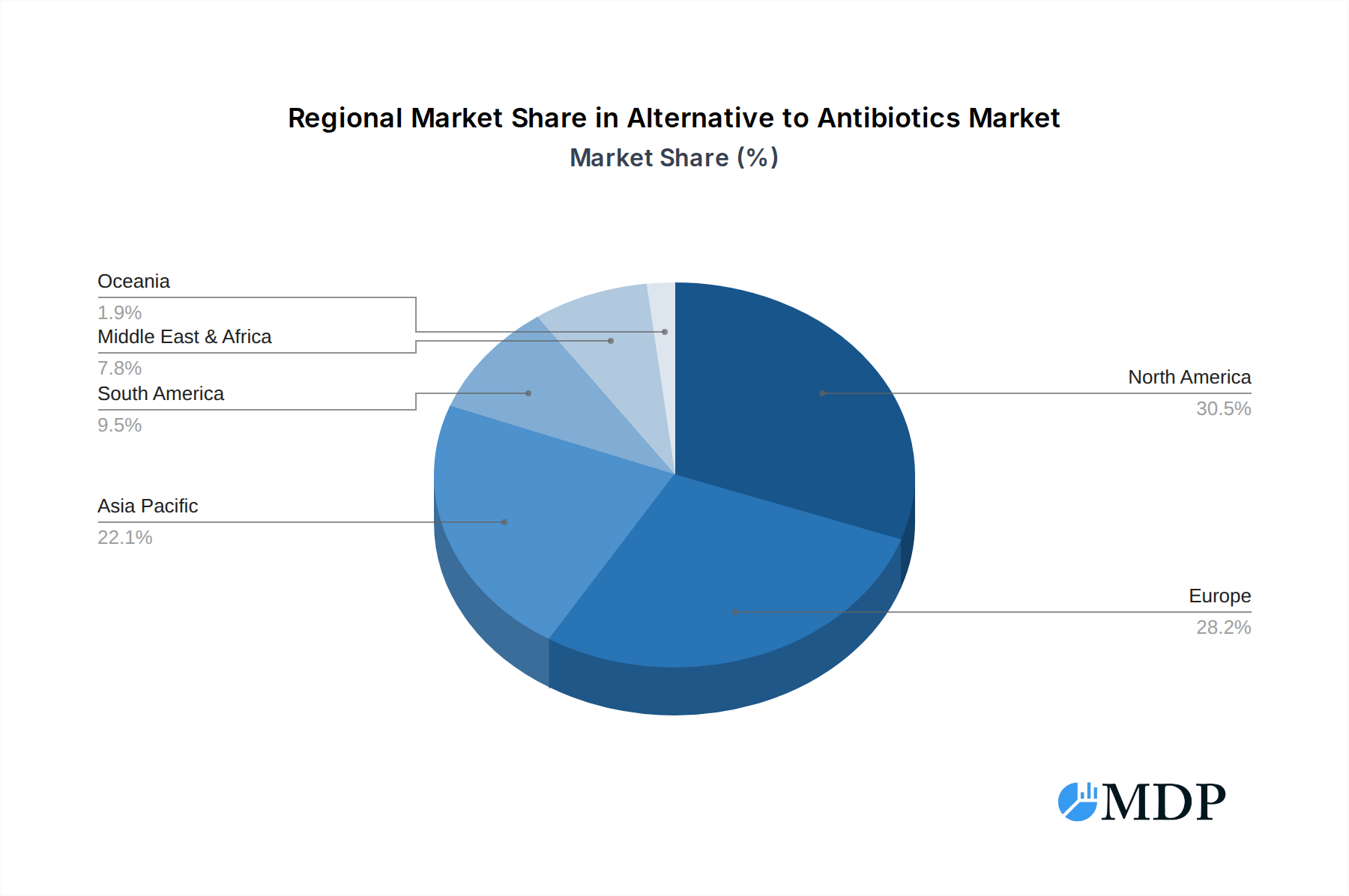

The alternative to antibiotics market exhibits distinct regional and segment dominance, driven by varying regulatory landscapes, consumer behaviors, and industrial needs. North America and Europe currently lead in market value, estimated to contribute over 60% of the global market share in 2025, owing to advanced research infrastructure, strong regulatory support for novel therapies, and high consumer awareness regarding health and wellness.

Application:

- Food & Beverage: This segment is projected to be the largest and fastest-growing, with an estimated market share of 40% in 2025, driven by the demand for natural food preservatives and functional ingredients that enhance gut health. Economic policies supporting sustainable agriculture and consumer demand for "clean label" products are key drivers.

- Dietary Supplements: Holding an estimated 35% market share, this segment benefits from the growing popularity of probiotics for digestive health, immune support, and overall well-being. The ease of market entry and direct-to-consumer accessibility contribute to its rapid expansion.

- Drugs: While currently representing a smaller but significant portion of the market (estimated 25%), the Drugs segment is poised for substantial long-term growth. Advancements in bacteriophage therapy for treating multidrug-resistant infections and the development of novel antimicrobial proteins as therapeutic agents are key drivers. Regulatory frameworks are evolving to accommodate these innovative treatments, with significant investment in clinical trials.

Types:

- Probiotics: This is the dominant type within the market, expected to command over 50% of the market share in 2025. Their widespread application in food, supplements, and animal feed, coupled with extensive scientific backing, fuels this dominance. Companies like BioGaia, Yakult, and Morinaga Milk Industry are key players.

- Antimicrobial Proteins: This category is experiencing rapid growth, estimated to capture 20% of the market share. Innovations in naturally occurring antimicrobial peptides and enzymes offer broad-spectrum activity and are gaining traction in food preservation and therapeutic applications.

- Bacteriophages: While currently a smaller segment (estimated 15%), bacteriophages are anticipated to witness the highest growth rate. Their targeted lytic activity against specific bacteria makes them a promising solution for combating resistant infections, with significant investment in research and development from entities like Novozymes and emerging biotech firms.

- Other: This category, encompassing prebiotics, organic acids, and plant extracts, accounts for the remaining market share but plays a supporting role in comprehensive alternative strategies.

The economic policies supporting R&D, robust infrastructure for manufacturing and distribution, and evolving consumer preferences for natural health solutions are pivotal in defining the dominance of these segments and regions.

Alternative to Antibiotics Product Developments

Product innovation in the alternative to antibiotics market is focused on enhancing efficacy, expanding application breadth, and improving delivery mechanisms. Companies are developing next-generation probiotics with enhanced survivability and targeted health benefits, as well as novel antimicrobial proteins derived from diverse natural sources. Significant progress is being made in the engineering and optimization of bacteriophages for precise therapeutic intervention against antibiotic-resistant bacteria. Competitive advantages are being built on superior scientific validation, cost-effectiveness, and regulatory compliance, attracting interest from food manufacturers, pharmaceutical companies, and dietary supplement brands seeking safe and sustainable alternatives to traditional antibiotics.

Key Drivers of Alternative to Antibiotics Growth

The alternative to antibiotics market is propelled by several key growth drivers. The escalating global crisis of antimicrobial resistance (AMR) is a primary catalyst, compelling industries to seek effective alternatives. Stringent regulatory frameworks worldwide, limiting the use of traditional antibiotics in animal agriculture and human medicine, create a favorable environment for these emerging solutions. Furthermore, a significant shift in consumer preferences towards natural, organic, and scientifically validated health products is fueling demand, particularly within the Food & Beverage and Dietary Supplements segments. Technological advancements in biotechnology, including genetic engineering and advanced fermentation processes, are enabling the development of more potent and diverse alternative products like enhanced probiotics and targeted bacteriophages.

Challenges in the Alternative to Antibiotics Market

Despite robust growth, the alternative to antibiotics market faces significant challenges. Regulatory hurdles remain a primary concern, particularly for novel therapeutic applications of bacteriophages and advanced antimicrobial proteins in the Drugs segment, requiring extensive and costly clinical trials. Supply chain complexities in sourcing and scaling up production of specific probiotic strains and bacteriophage cocktails can lead to price volatility and availability issues. Intense competition from established pharmaceutical companies and the perception of higher upfront costs compared to conventional antibiotics can also act as restraints. Furthermore, educating consumers and industry stakeholders about the efficacy and safety of these alternatives is an ongoing challenge. The estimated impact of these challenges on market growth could range from a 5-10% reduction in projected CAGR if not effectively addressed.

Emerging Opportunities in Alternative to Antibiotics

Emerging opportunities within the alternative to antibiotics market are abundant, driven by unmet medical needs and evolving industry demands. The development of personalized probiotic formulations tailored to individual gut microbiomes presents a significant avenue for growth. Advances in bacteriophage therapy, including the creation of "cocktails" to combat multi-drug resistant bacteria, offer revolutionary solutions for healthcare. Strategic partnerships between biotechnology firms and large Food & Beverage and pharmaceutical companies are accelerating product development and market penetration. Furthermore, the expansion into emerging economies, where awareness of AMR is growing and regulatory frameworks are becoming more supportive, represents a substantial market expansion strategy. The potential for novel applications in areas like wound healing and crop protection further diversifies growth prospects, estimated to contribute an additional fifty billion dollars in market value over the forecast period.

Leading Players in the Alternative to Antibiotics Sector

- DSM

- DuPont (Danisco)

- Chr. Hansen

- Lallemand

- China-Biotics

- Nestle

- Danone

- Probi

- BioGaia

- Yakult

- Novozymes

- Valio

- Glory Biotech

- Ganeden

- Morinaga Milk Industry

- Sabinsa

- Greentech

- Bioriginal

- Biosearch Life

- UAS Laboratories

- Synbiotech

Key Milestones in Alternative to Antibiotics Industry

- 2019: Increased regulatory focus on antibiotic reduction in animal feed globally, driving demand for alternatives.

- 2020: Launch of several new probiotic strains with enhanced digestive health benefits by leading supplement manufacturers.

- 2021: Significant investment rounds for bacteriophage therapy companies addressing antibiotic-resistant infections.

- 2022: Increased M&A activity, with major ingredient suppliers acquiring smaller biotechnology firms to expand their portfolios.

- 2023: Release of key clinical trial results demonstrating the efficacy of certain antimicrobial proteins in food preservation.

- 2024: Growing consumer awareness campaigns about the benefits of probiotics and the risks of antibiotic overuse.

- Ongoing: Continuous research and development in identifying novel strains of probiotics and engineering more effective bacteriophages.

Strategic Outlook for Alternative to Antibiotics Market

The alternative to antibiotics market is poised for sustained and accelerated growth, driven by ongoing scientific innovation and increasing global demand for healthier and more sustainable solutions. Key growth accelerators include the continued intensification of the AMR crisis, leading to further regulatory support for alternatives, and the relentless pursuit of novel applications for probiotics, antimicrobial proteins, and bacteriophages. Strategic opportunities lie in forging robust collaborations between research institutions, biotechnology firms, and end-user industries, alongside focused market penetration in developing economies. The market's future trajectory is strongly indicative of a multi-billion dollar industry consolidation and expansion, offering substantial returns for early adopters and strategic investors.

Alternative to Antibiotics Segmentation

-

1. Application

- 1.1. Food & Beverage

- 1.2. Drugs

- 1.3. Dietary Supplements

-

2. Types

- 2.1. Antimicrobial Proteins

- 2.2. Bacteriophages

- 2.3. Probiotics

- 2.4. Other

Alternative to Antibiotics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Alternative to Antibiotics Regional Market Share

Geographic Coverage of Alternative to Antibiotics

Alternative to Antibiotics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.72% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Alternative to Antibiotics Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food & Beverage

- 5.1.2. Drugs

- 5.1.3. Dietary Supplements

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Antimicrobial Proteins

- 5.2.2. Bacteriophages

- 5.2.3. Probiotics

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Alternative to Antibiotics Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food & Beverage

- 6.1.2. Drugs

- 6.1.3. Dietary Supplements

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Antimicrobial Proteins

- 6.2.2. Bacteriophages

- 6.2.3. Probiotics

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Alternative to Antibiotics Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food & Beverage

- 7.1.2. Drugs

- 7.1.3. Dietary Supplements

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Antimicrobial Proteins

- 7.2.2. Bacteriophages

- 7.2.3. Probiotics

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Alternative to Antibiotics Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food & Beverage

- 8.1.2. Drugs

- 8.1.3. Dietary Supplements

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Antimicrobial Proteins

- 8.2.2. Bacteriophages

- 8.2.3. Probiotics

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Alternative to Antibiotics Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food & Beverage

- 9.1.2. Drugs

- 9.1.3. Dietary Supplements

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Antimicrobial Proteins

- 9.2.2. Bacteriophages

- 9.2.3. Probiotics

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Alternative to Antibiotics Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food & Beverage

- 10.1.2. Drugs

- 10.1.3. Dietary Supplements

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Antimicrobial Proteins

- 10.2.2. Bacteriophages

- 10.2.3. Probiotics

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 DSM

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 DuPont(Danisco)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Chr. Hansen

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Lallemand

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 China-Biotics

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Nestle

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Danone

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Probi

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 BioGaia

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Yakult

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Novozymes

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Valio

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Glory Biotech

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Ganeden

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Morinaga Milk Industry

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Sabinsa

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Greentech

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Bioriginal

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Biosearch Life

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 UAS Laboratories

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Synbiotech

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 DSM

List of Figures

- Figure 1: Global Alternative to Antibiotics Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Alternative to Antibiotics Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Alternative to Antibiotics Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Alternative to Antibiotics Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Alternative to Antibiotics Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Alternative to Antibiotics Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Alternative to Antibiotics Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Alternative to Antibiotics Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Alternative to Antibiotics Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Alternative to Antibiotics Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Alternative to Antibiotics Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Alternative to Antibiotics Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Alternative to Antibiotics Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Alternative to Antibiotics Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Alternative to Antibiotics Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Alternative to Antibiotics Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Alternative to Antibiotics Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Alternative to Antibiotics Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Alternative to Antibiotics Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Alternative to Antibiotics Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Alternative to Antibiotics Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Alternative to Antibiotics Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Alternative to Antibiotics Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Alternative to Antibiotics Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Alternative to Antibiotics Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Alternative to Antibiotics Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Alternative to Antibiotics Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Alternative to Antibiotics Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Alternative to Antibiotics Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Alternative to Antibiotics Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Alternative to Antibiotics Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Alternative to Antibiotics Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Alternative to Antibiotics Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Alternative to Antibiotics Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Alternative to Antibiotics Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Alternative to Antibiotics Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Alternative to Antibiotics Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Alternative to Antibiotics Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Alternative to Antibiotics Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Alternative to Antibiotics Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Alternative to Antibiotics Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Alternative to Antibiotics Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Alternative to Antibiotics Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Alternative to Antibiotics Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Alternative to Antibiotics Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Alternative to Antibiotics Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Alternative to Antibiotics Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Alternative to Antibiotics Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Alternative to Antibiotics Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Alternative to Antibiotics Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Alternative to Antibiotics?

The projected CAGR is approximately 8.72%.

2. Which companies are prominent players in the Alternative to Antibiotics?

Key companies in the market include DSM, DuPont(Danisco), Chr. Hansen, Lallemand, China-Biotics, Nestle, Danone, Probi, BioGaia, Yakult, Novozymes, Valio, Glory Biotech, Ganeden, Morinaga Milk Industry, Sabinsa, Greentech, Bioriginal, Biosearch Life, UAS Laboratories, Synbiotech.

3. What are the main segments of the Alternative to Antibiotics?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.89 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Alternative to Antibiotics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Alternative to Antibiotics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Alternative to Antibiotics?

To stay informed about further developments, trends, and reports in the Alternative to Antibiotics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence