Key Insights

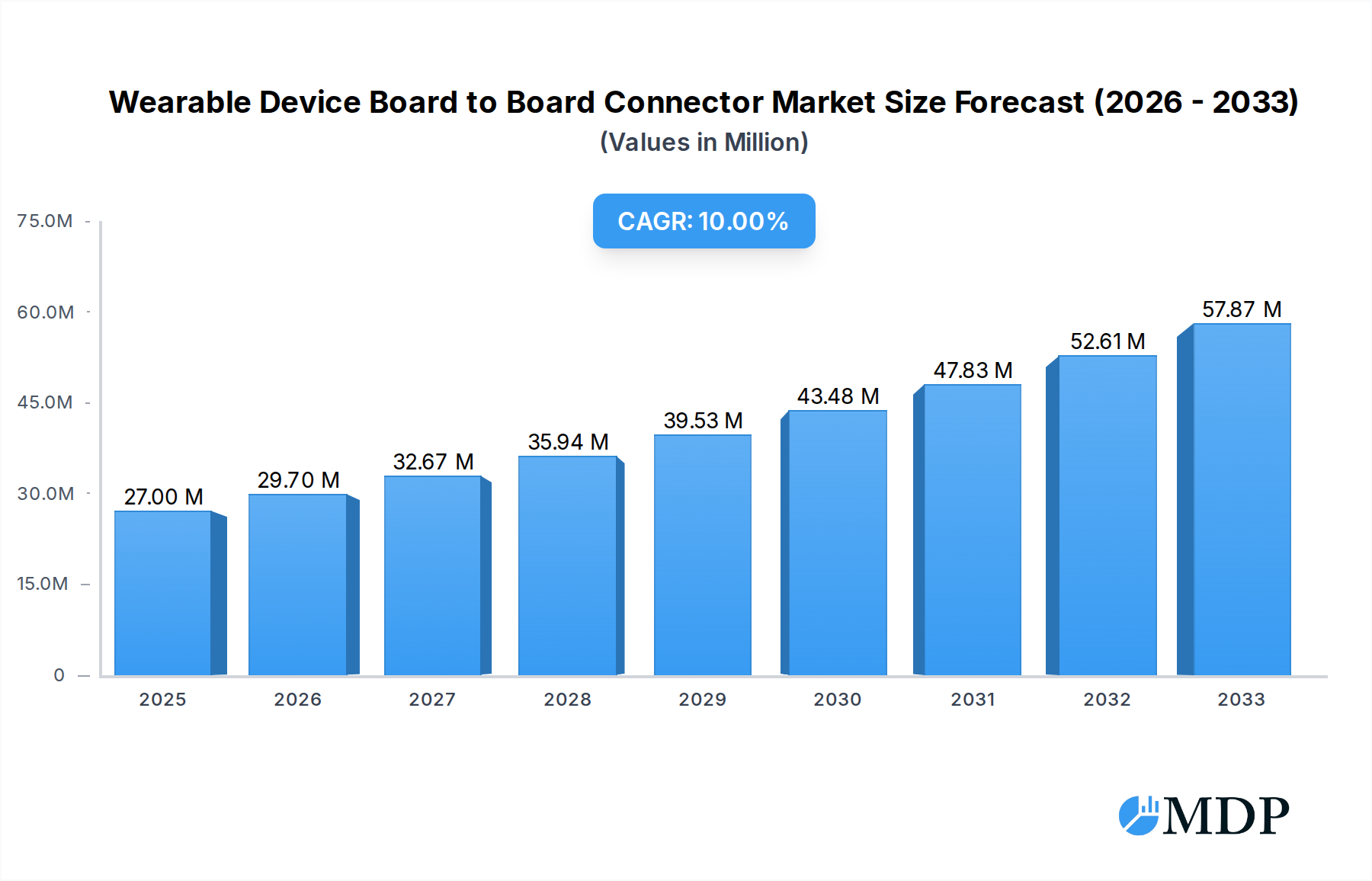

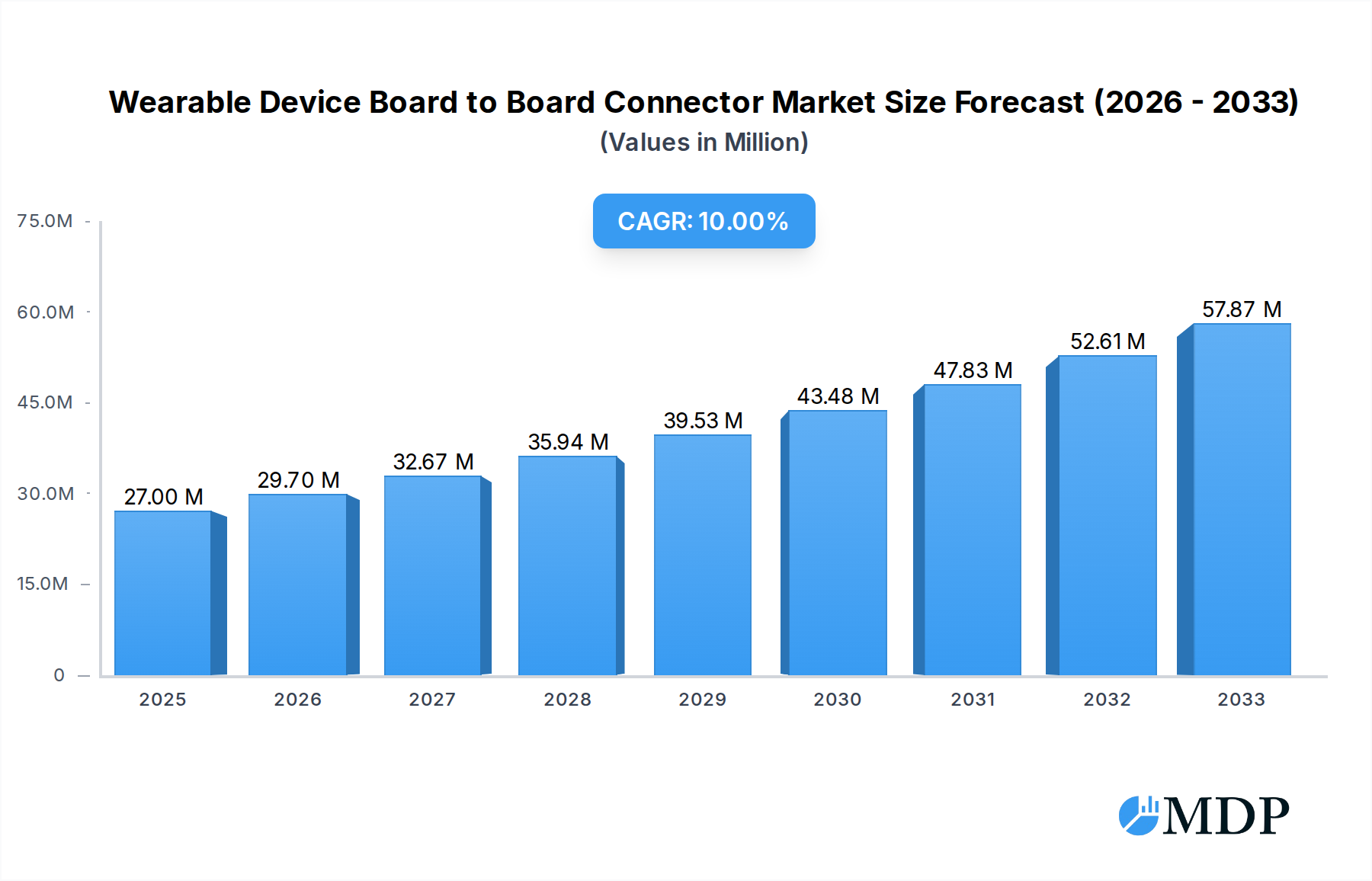

The global Wearable Device Board to Board Connector market is poised for substantial expansion, projected to reach $27 million in 2025 and surge at a Compound Annual Growth Rate (CAGR) of 10% through 2033. This robust growth is primarily fueled by the escalating demand for miniaturized and high-performance electronic components within the rapidly evolving wearable technology sector. Key market drivers include the relentless innovation in smartwatches, wireless headphones, and VR/AR glasses, each requiring increasingly sophisticated interconnect solutions. As these devices become more integral to daily life, offering enhanced functionalities and a seamless user experience, the need for reliable, compact, and efficient board-to-board connectors becomes paramount. Furthermore, advancements in connector technology, such as higher stacking densities and improved signal integrity, are enabling the development of even sleeker and more powerful wearable products, further propelling market demand.

Wearable Device Board to Board Connector Market Size (In Million)

The market is characterized by a significant trend towards miniaturization, with a notable emphasis on connectors with stacking heights below 0.7mm, catering to the design constraints of ultra-thin wearable devices. This segment is expected to witness the most vigorous growth, driven by consumer preference for lightweight and aesthetically pleasing gadgets. Conversely, while connectors with stacking heights between 0.7-0.8mm and above 0.8mm will continue to serve specific applications, their growth trajectory may be more moderate compared to their ultra-low profile counterparts. Emerging applications beyond traditional wearables, such as advanced medical monitoring devices and innovative personal communication gadgets, also present significant future growth opportunities. However, potential restraints such as supply chain disruptions, the high cost of advanced materials, and the need for stringent miniaturization could present challenges that manufacturers will need to navigate effectively to sustain this impressive growth.

Wearable Device Board to Board Connector Company Market Share

Wearable Device Board to Board Connector Market Dynamics & Concentration

The wearable device board-to-board connector market, a critical yet often unseen component in the rapidly evolving world of connected personal technology, is characterized by a dynamic interplay of innovation, market consolidation, and evolving end-user demands. This report delves into the intricate market dynamics, analyzing factors that shape its competitive landscape and future trajectory. The market exhibits a moderate to high concentration, with key players like TE Connectivity, Amphenol, and Molex holding significant market share, estimated to be in the hundreds of millions of dollars. These industry giants leverage extensive R&D capabilities, robust supply chains, and strategic acquisitions to maintain their leadership. Recent M&A activities, with an estimated 20-30 deals per year in the broader connector industry with wearable applications, indicate a trend towards consolidation as companies seek to expand their product portfolios and geographical reach. Innovation remains a primary driver, fueled by the relentless demand for smaller, more powerful, and more energy-efficient wearable devices. Regulatory frameworks, particularly those pertaining to miniaturization, electromagnetic interference (EMI) shielding, and material safety, are increasingly influencing product design and manufacturing processes. The emergence of advanced materials and manufacturing techniques, coupled with a growing acceptance of cutting-edge wearable technologies by consumers, further propels market growth. Product substitutes, while limited in direct board-to-board applications, can emerge in the form of flexible circuitry or advanced soldering techniques for highly integrated designs, posing a subtle challenge. End-user trends, driven by increasing consumer adoption of smartwatches, wireless headphones, and VR/AR glasses, directly translate into higher demand for sophisticated and miniaturized board-to-board connectors. The forecast anticipates a significant surge in demand, with market revenue projected to reach xx million by 2033.

Wearable Device Board to Board Connector Industry Trends & Analysis

The wearable device board-to-board connector industry is currently experiencing a period of accelerated growth and transformation, driven by a confluence of technological advancements, shifting consumer preferences, and burgeoning application areas. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 15-20% over the forecast period of 2025–2033, a testament to its robust expansion potential. This growth is underpinned by several key trends. Firstly, the relentless miniaturization of electronic components is a defining characteristic of the wearable sector. As devices become smaller and sleeker, the demand for equally compact and high-performance board-to-board connectors intensifies. This necessitates innovations in materials, design, and manufacturing processes to achieve ultra-low stacking heights, some below 0.7mm, and reduced pitch sizes without compromising signal integrity or power delivery.

Secondly, the increasing integration of advanced functionalities in wearables, such as sophisticated sensors for health monitoring, augmented reality capabilities in VR/AR glasses, and immersive audio experiences in wireless headphones, places a premium on connector reliability and performance. These applications require connectors that can handle high-speed data transfer, low power consumption, and robust environmental resistance, including resistance to moisture, dust, and temperature fluctuations. The market penetration of smartwatches, in particular, has been a significant catalyst, creating a substantial installed base and driving ongoing demand for replacement and upgrade components. Similarly, the burgeoning VR/AR market, though still in its nascent stages compared to smartwatches, holds immense future potential for board-to-board connector innovation, requiring specialized solutions for high-bandwidth data transmission and complex interconnectivity.

Technological disruptions, including the adoption of advanced plating technologies for improved conductivity and durability, and innovative locking mechanisms for enhanced mechanical stability, are continuously pushing the boundaries of connector design. Furthermore, the shift towards flexible printed circuit boards (FPC) and flexible hybrid electronics is influencing connector designs, demanding solutions that can accommodate the unique characteristics of these flexible substrates. Consumer preferences are increasingly leaning towards aesthetically pleasing, comfortable, and feature-rich wearable devices. This translates into a demand for connectors that are not only functional but also contribute to the overall design integrity and user experience, such as those enabling seamless integration within slim device profiles. Competitive dynamics are fierce, with established players and emerging innovators vying for market share through product differentiation, strategic partnerships, and aggressive pricing strategies. The industry is witnessing a significant investment in research and development to address the evolving needs of applications such as advanced health trackers, augmented reality headsets, and next-generation hearables. The market is projected to reach an estimated xx million by the base year 2025, with further substantial growth anticipated through the forecast period.

Leading Markets & Segments in Wearable Device Board to Board Connector

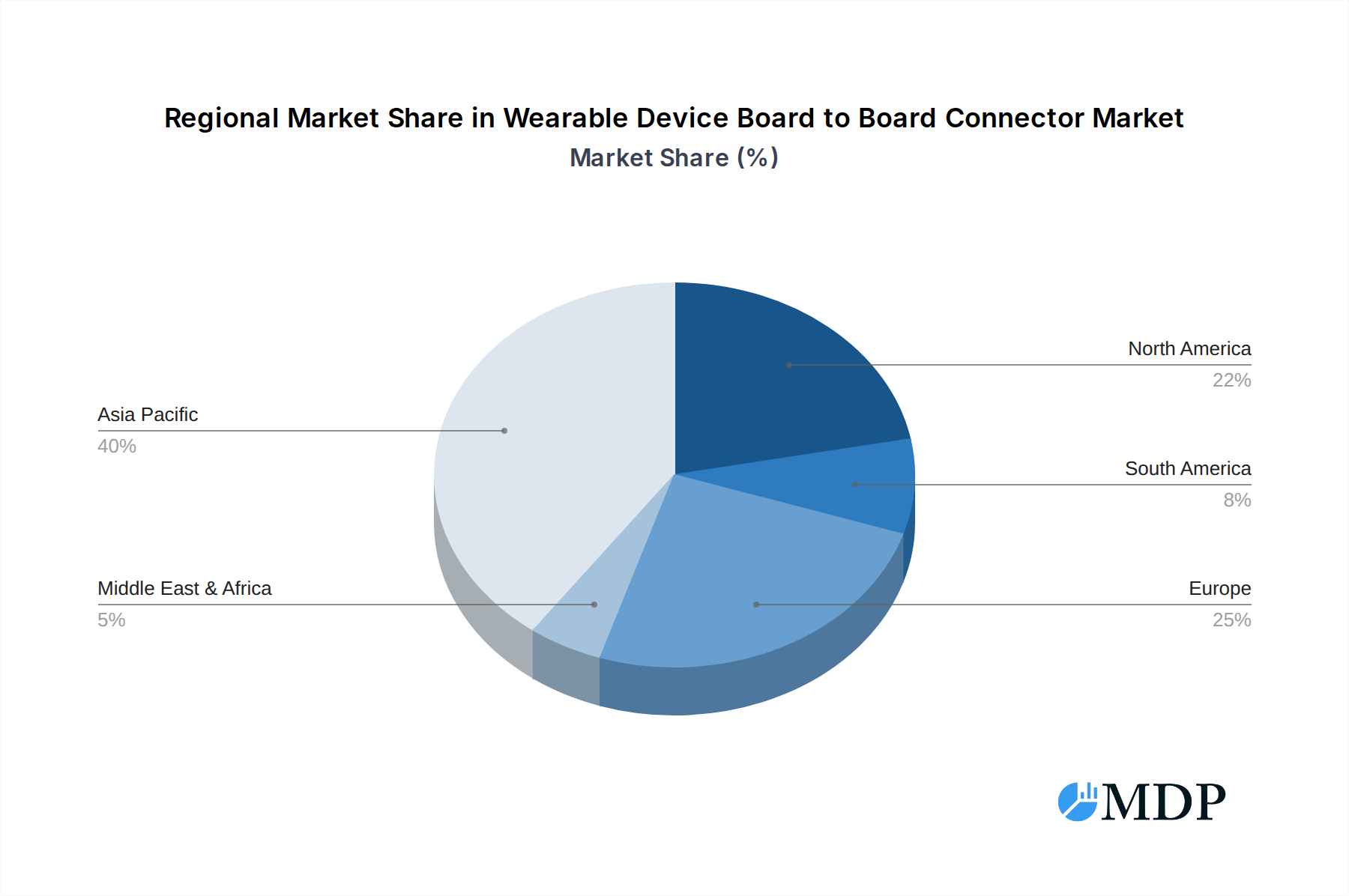

The global wearable device board-to-board connector market is dominated by Asia-Pacific, particularly China, South Korea, and Taiwan, driven by their established strength in consumer electronics manufacturing and the presence of leading wearable device brands. The region's economic policies that foster technological innovation and manufacturing excellence, coupled with a highly developed electronics infrastructure, create an unparalleled ecosystem for the production and adoption of wearable technologies. Within this dominant region, the Smart Watch segment is currently the largest and most influential application.

Application Dominance Analysis:

- Smart Watch: This segment benefits from widespread consumer adoption, rapid product iteration cycles, and an increasing demand for advanced health monitoring features. The miniaturization requirements for smartwatches are particularly stringent, driving innovation in connectors with stacking heights below 0.7mm. The market size for smartwatches is projected to be in the tens of millions of units annually.

- Wireless Headphones: The booming market for true wireless stereo (TWS) earbuds and premium audio devices is a significant growth driver. These devices require highly integrated and compact connectors to fit within small form factors while ensuring reliable audio transmission and battery charging.

- VR/AR Glasses: While still a developing market, VR/AR glasses represent a substantial future growth opportunity. These applications demand high-bandwidth connectors for immersive visual and auditory experiences, as well as robust interconnectivity for sensors and processing units. The growth in this segment is directly tied to advancements in display technology and processing power.

- Others: This segment encompasses a diverse range of emerging wearable devices, including fitness trackers, smart rings, smart glasses (beyond full VR/AR), and specialized medical wearables. The growth in these niche areas contributes to the overall market expansion.

Type Dominance Analysis:

- Stacking Height Below 0.7mm: This category is experiencing the most rapid growth due to the unceasing demand for ultra-slim and lightweight wearable devices. Innovations in dielectric materials, contact designs, and manufacturing precision are critical for success in this segment. The market share for this type is estimated to be over 40% and growing.

- Stacking Height 0.7-0.8mm: This segment caters to a broader range of wearables where ultra-low profiles are not the absolute priority but miniaturization remains key. These connectors offer a good balance of performance, cost, and form factor, making them popular in many mid-range smartwatches and wireless headphones.

- Stacking Height Above 0.8mm: While less prominent in the most advanced wearables, this category still finds application in certain industrial or more robust wearable devices where higher mechanical strength or ease of assembly might be prioritized over extreme miniaturization.

The market penetration of smartwatches, coupled with the increasing sophistication of their internal components, directly influences the demand for board-to-board connectors, especially those enabling ultra-low stacking heights. Economic policies supporting R&D and manufacturing in the Asia-Pacific region continue to bolster the dominance of this market. The overall market revenue in the wearable device board-to-board connector sector is projected to reach xx million by 2025.

Wearable Device Board to Board Connector Product Developments

Product development in the wearable device board-to-board connector market is aggressively focused on miniaturization and high performance. Innovations are centered on achieving ultra-low stacking heights, often below 0.7mm, and ultra-fine pitch designs to accommodate the ever-shrinking form factors of smartwatches, wireless headphones, and VR/AR glasses. Manufacturers are investing in advanced materials, such as high-performance plastics and specialized plating techniques, to enhance conductivity, durability, and signal integrity. Edge connectors and board-to-flex connectors are also gaining traction, offering greater design flexibility. These developments are crucial for enabling the integration of more sensors, processors, and battery capacity within smaller wearable devices, providing a distinct competitive advantage for companies that can deliver reliable and space-saving interconnect solutions.

Key Drivers of Wearable Device Board to Board Connector Growth

The growth of the wearable device board-to-board connector market is propelled by a synergistic combination of technological, economic, and consumer-driven factors. The insatiable demand for smaller, more feature-rich wearable devices, such as smartwatches and wireless headphones, is a primary catalyst. This is directly supported by continuous advancements in semiconductor technology, enabling smaller processors and sensors that necessitate equally miniaturized interconnect solutions. Economic prosperity in emerging markets fuels consumer spending on personal electronics, further expanding the wearable device user base. Furthermore, increasing government initiatives and investments in the Internet of Things (IoT) ecosystem and smart manufacturing indirectly boost the demand for essential components like board-to-board connectors.

Challenges in the Wearable Device Board to Board Connector Market

Despite its robust growth, the wearable device board-to-board connector market faces several significant challenges. The extreme miniaturization required often pushes the boundaries of manufacturing precision, leading to higher production costs and potential quality control issues, estimated to impact cost by up to 10-15%. Supply chain volatility, particularly for specialized raw materials, can disrupt production schedules and impact lead times. Intense competition from both established players and new entrants creates downward pressure on pricing, impacting profit margins for some manufacturers. Moreover, the rapid pace of technological evolution means that connector designs can quickly become obsolete, requiring continuous investment in R&D to stay competitive. Regulatory hurdles, though generally favorable, can also add complexity, especially concerning international standards for material compliance and electromagnetic interference.

Emerging Opportunities in Wearable Device Board to Board Connector

The future of the wearable device board-to-board connector market is ripe with emerging opportunities. The rapid advancement and adoption of augmented and virtual reality technologies present a significant avenue for growth, requiring high-speed, low-latency interconnect solutions. The burgeoning medical wearable segment, focused on remote patient monitoring and advanced diagnostics, will demand highly reliable, miniaturized, and often medical-grade connectors. Strategic partnerships between connector manufacturers and leading wearable device brands are crucial for co-development and early integration of next-generation interconnect solutions. Furthermore, the growing trend of customization and personalization in wearables opens doors for specialized connector designs tailored to specific niche applications, expanding market reach.

Leading Players in the Wearable Device Board to Board Connector Sector

- TE Connectivity

- Amphenol

- Molex

- Panasonic

- Kyosera

- HRS

- LCN

- JAE

- ECT

- OCN

- Sunway Communication

- YXT

- Acon

- CSCONN

Key Milestones in Wearable Device Board to Board Connector Industry

- 2019: Introduction of new ultra-low profile connectors (<0.5mm stacking height) for next-generation smartwatches.

- 2020: Increased demand for ruggedized and waterproof connectors driven by outdoor and sports-focused wearables.

- 2021: significant increase in R&D investment by major players focusing on high-speed data transfer for VR/AR applications.

- 2022: Emergence of novel locking mechanisms for enhanced vibration resistance in wearable devices.

- 2023: Growing adoption of FPC (Flexible Printed Circuit) connectors to facilitate highly flexible wearable designs.

- 2024: Key players announce strategic partnerships to develop specialized connectors for advanced health monitoring wearables.

Strategic Outlook for Wearable Device Board to Board Connector Market

The strategic outlook for the wearable device board-to-board connector market is exceptionally positive, driven by relentless innovation and expanding market penetration. Growth accelerators include the continued miniaturization of electronic components, the increasing integration of advanced functionalities into wearables, and the burgeoning adoption of AR/VR technologies. Companies that invest in ultra-low profile connectors, high-speed data transmission capabilities, and robust environmental resistance will be well-positioned to capture market share. Furthermore, fostering strategic collaborations with wearable device manufacturers and focusing on emerging applications such as medical wearables and advanced hearables will be crucial for long-term success and sustained revenue growth, projected to reach xx million by 2033.

Wearable Device Board to Board Connector Segmentation

-

1. Application

- 1.1. Wireless Headphones

- 1.2. Smart Watch

- 1.3. VR/AR Glasses

- 1.4. Others

-

2. Types

- 2.1. Stacking Height Below 0.7mm

- 2.2. Stacking Height 0.7-0.8mm

- 2.3. Stacking Height Above 0.8mm

Wearable Device Board to Board Connector Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Wearable Device Board to Board Connector Regional Market Share

Geographic Coverage of Wearable Device Board to Board Connector

Wearable Device Board to Board Connector REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Wearable Device Board to Board Connector Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Wireless Headphones

- 5.1.2. Smart Watch

- 5.1.3. VR/AR Glasses

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Stacking Height Below 0.7mm

- 5.2.2. Stacking Height 0.7-0.8mm

- 5.2.3. Stacking Height Above 0.8mm

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Wearable Device Board to Board Connector Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Wireless Headphones

- 6.1.2. Smart Watch

- 6.1.3. VR/AR Glasses

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Stacking Height Below 0.7mm

- 6.2.2. Stacking Height 0.7-0.8mm

- 6.2.3. Stacking Height Above 0.8mm

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Wearable Device Board to Board Connector Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Wireless Headphones

- 7.1.2. Smart Watch

- 7.1.3. VR/AR Glasses

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Stacking Height Below 0.7mm

- 7.2.2. Stacking Height 0.7-0.8mm

- 7.2.3. Stacking Height Above 0.8mm

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Wearable Device Board to Board Connector Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Wireless Headphones

- 8.1.2. Smart Watch

- 8.1.3. VR/AR Glasses

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Stacking Height Below 0.7mm

- 8.2.2. Stacking Height 0.7-0.8mm

- 8.2.3. Stacking Height Above 0.8mm

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Wearable Device Board to Board Connector Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Wireless Headphones

- 9.1.2. Smart Watch

- 9.1.3. VR/AR Glasses

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Stacking Height Below 0.7mm

- 9.2.2. Stacking Height 0.7-0.8mm

- 9.2.3. Stacking Height Above 0.8mm

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Wearable Device Board to Board Connector Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Wireless Headphones

- 10.1.2. Smart Watch

- 10.1.3. VR/AR Glasses

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Stacking Height Below 0.7mm

- 10.2.2. Stacking Height 0.7-0.8mm

- 10.2.3. Stacking Height Above 0.8mm

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 TE Connectivity

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Amphenol

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Molex

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Panasonic

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Kyosera

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 HRS

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 LCN

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 JAE

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 ECT

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 OCN

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Sunway Communication

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 YXT

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Acon

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 CSCONN

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 TE Connectivity

List of Figures

- Figure 1: Global Wearable Device Board to Board Connector Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Wearable Device Board to Board Connector Revenue (million), by Application 2025 & 2033

- Figure 3: North America Wearable Device Board to Board Connector Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Wearable Device Board to Board Connector Revenue (million), by Types 2025 & 2033

- Figure 5: North America Wearable Device Board to Board Connector Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Wearable Device Board to Board Connector Revenue (million), by Country 2025 & 2033

- Figure 7: North America Wearable Device Board to Board Connector Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Wearable Device Board to Board Connector Revenue (million), by Application 2025 & 2033

- Figure 9: South America Wearable Device Board to Board Connector Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Wearable Device Board to Board Connector Revenue (million), by Types 2025 & 2033

- Figure 11: South America Wearable Device Board to Board Connector Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Wearable Device Board to Board Connector Revenue (million), by Country 2025 & 2033

- Figure 13: South America Wearable Device Board to Board Connector Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Wearable Device Board to Board Connector Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Wearable Device Board to Board Connector Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Wearable Device Board to Board Connector Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Wearable Device Board to Board Connector Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Wearable Device Board to Board Connector Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Wearable Device Board to Board Connector Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Wearable Device Board to Board Connector Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Wearable Device Board to Board Connector Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Wearable Device Board to Board Connector Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Wearable Device Board to Board Connector Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Wearable Device Board to Board Connector Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Wearable Device Board to Board Connector Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Wearable Device Board to Board Connector Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Wearable Device Board to Board Connector Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Wearable Device Board to Board Connector Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Wearable Device Board to Board Connector Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Wearable Device Board to Board Connector Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Wearable Device Board to Board Connector Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wearable Device Board to Board Connector Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Wearable Device Board to Board Connector Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Wearable Device Board to Board Connector Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Wearable Device Board to Board Connector Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Wearable Device Board to Board Connector Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Wearable Device Board to Board Connector Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Wearable Device Board to Board Connector Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Wearable Device Board to Board Connector Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Wearable Device Board to Board Connector Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Wearable Device Board to Board Connector Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Wearable Device Board to Board Connector Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Wearable Device Board to Board Connector Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Wearable Device Board to Board Connector Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Wearable Device Board to Board Connector Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Wearable Device Board to Board Connector Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Wearable Device Board to Board Connector Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Wearable Device Board to Board Connector Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Wearable Device Board to Board Connector Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Wearable Device Board to Board Connector Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wearable Device Board to Board Connector?

The projected CAGR is approximately 10%.

2. Which companies are prominent players in the Wearable Device Board to Board Connector?

Key companies in the market include TE Connectivity, Amphenol, Molex, Panasonic, Kyosera, HRS, LCN, JAE, ECT, OCN, Sunway Communication, YXT, Acon, CSCONN.

3. What are the main segments of the Wearable Device Board to Board Connector?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 27 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wearable Device Board to Board Connector," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wearable Device Board to Board Connector report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wearable Device Board to Board Connector?

To stay informed about further developments, trends, and reports in the Wearable Device Board to Board Connector, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence