Key Insights

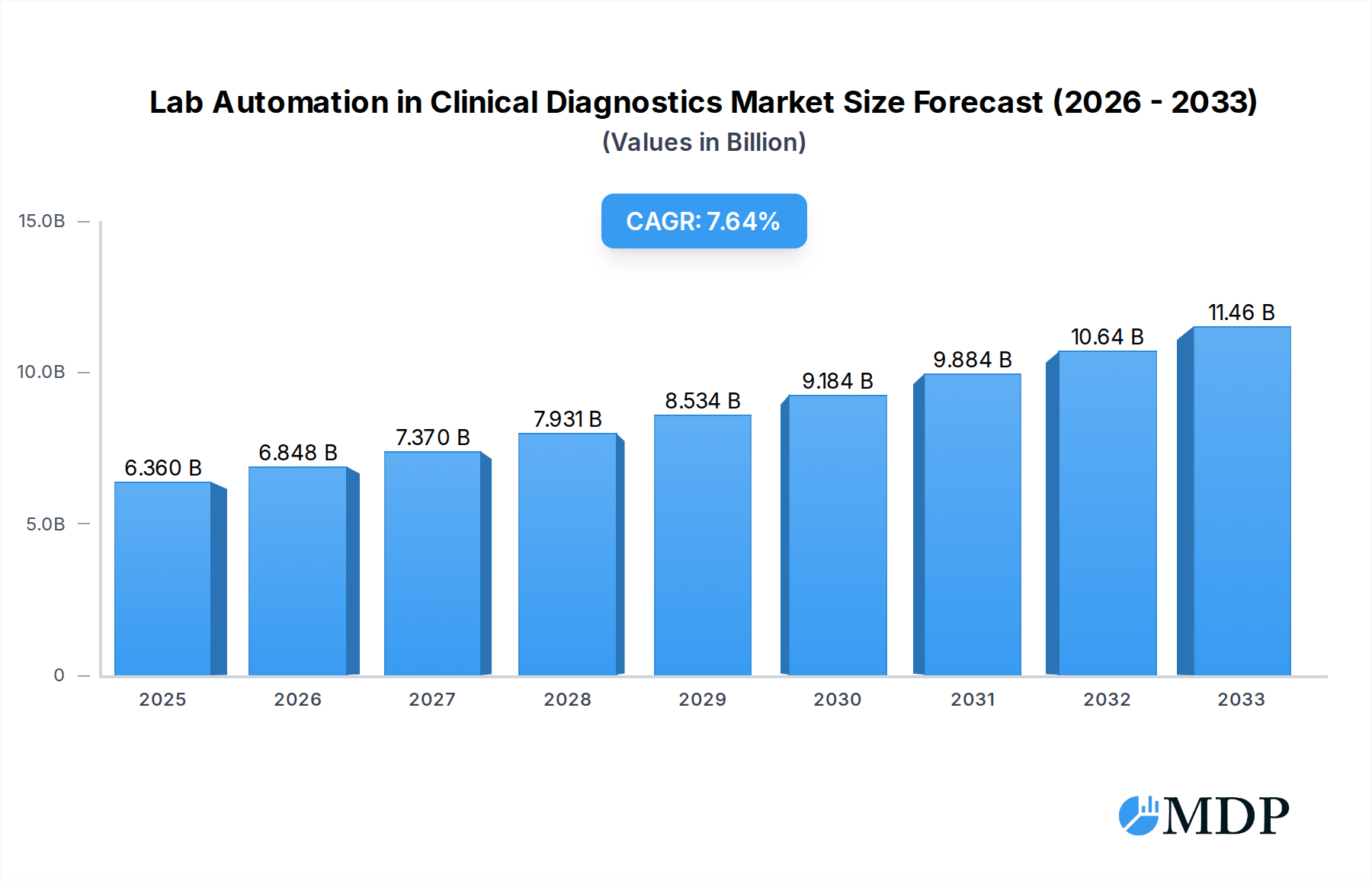

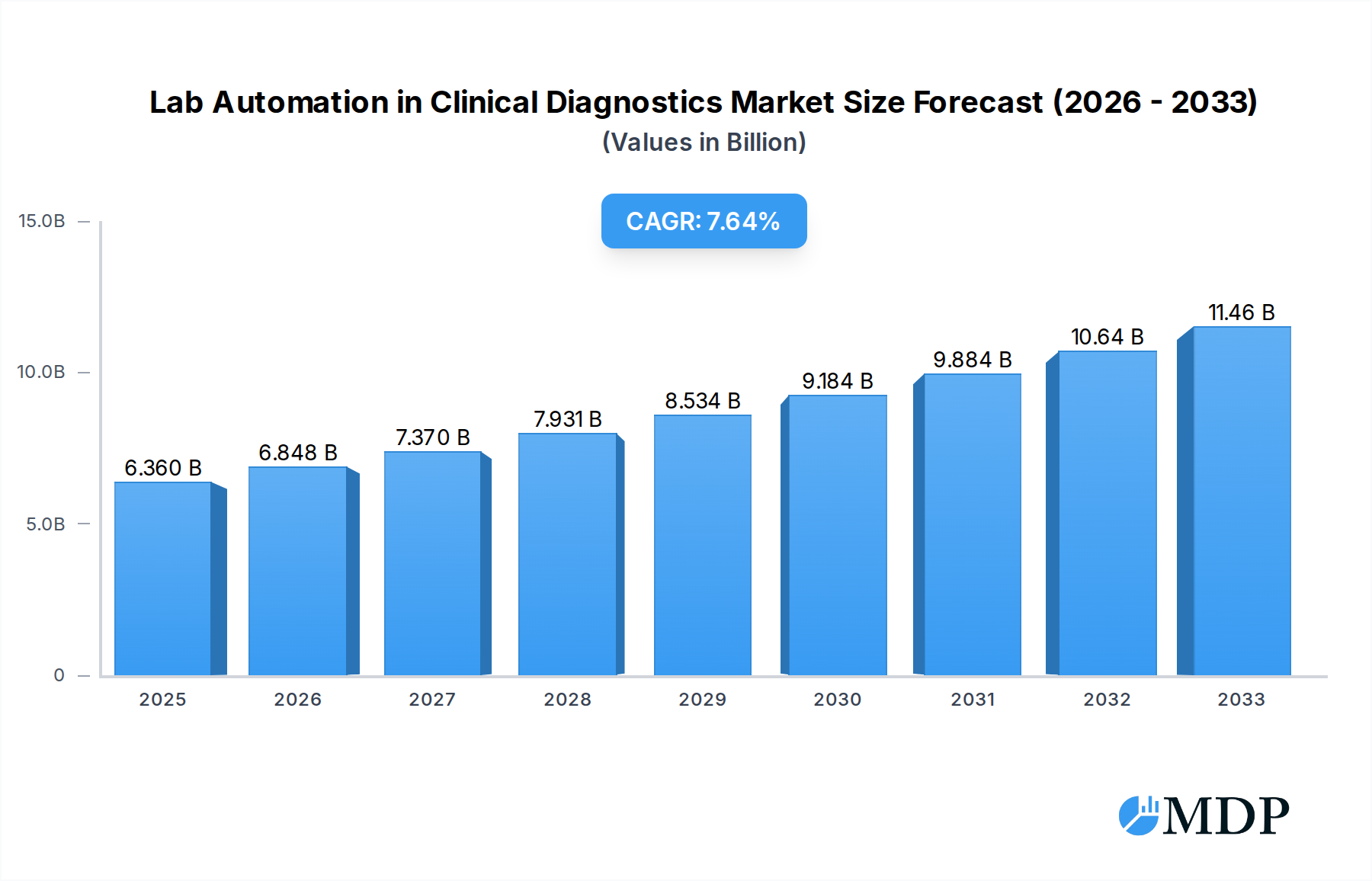

The global Lab Automation in Clinical Diagnostics Market is poised for robust growth, projected to reach USD 6.36 billion in 2025, and is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 7.2% through 2033. This significant expansion is driven by an increasing demand for faster, more accurate, and efficient diagnostic testing, fueled by the rising global burden of chronic diseases and infectious outbreaks. Advancements in robotics, artificial intelligence (AI), and machine learning are transforming clinical laboratories, enabling higher throughput, reduced human error, and improved turnaround times for critical patient results. The market's expansion is further bolstered by a growing emphasis on precision medicine and personalized healthcare, requiring sophisticated automation solutions for complex genomic and proteomic analyses. Investments in healthcare infrastructure, particularly in emerging economies, are also contributing to market penetration, as laboratories strive to meet growing testing volumes and improve diagnostic capabilities.

Lab Automation in Clinical Diagnostics Market Market Size (In Billion)

Key segments within the lab automation ecosystem are experiencing dynamic evolution. Automated Liquid Handlers are crucial for high-throughput screening and sample processing, while Automated Plate Handlers optimize workflow efficiency. Robotic Arms are increasingly employed for repetitive tasks, enhancing precision and safety. Automated Storage and Retrieval Systems (AS/RS) are vital for managing vast sample inventories, and Vision Systems play a critical role in quality control and data analysis. Prominent players like Thermo Fisher Scientific, Danaher Corporation, and Siemens Healthineers AG are at the forefront of innovation, driving advancements through strategic collaborations and research and development. The market is characterized by a continuous drive for integrated solutions that streamline the entire diagnostic workflow, from sample accessioning to result reporting, ultimately aiming to improve patient outcomes and reduce healthcare costs.

Lab Automation in Clinical Diagnostics Market Company Market Share

Report Description: Lab Automation in Clinical Diagnostics Market: Forecast to 2033

Unlock the Future of Healthcare Efficiency with the Comprehensive Lab Automation in Clinical Diagnostics Market Report

This in-depth analysis of the Lab Automation in Clinical Diagnostics market provides critical insights for stakeholders navigating this rapidly evolving sector. Covering the period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, this report offers a detailed examination of market dynamics, industry trends, leading segments, and key players. Discover the strategic imperative of laboratory automation in enhancing diagnostic accuracy, improving turnaround times, and driving cost efficiencies in clinical settings. With an estimated market value projected to reach over $15 billion by 2025, this report is an indispensable resource for understanding growth drivers, emerging opportunities, and competitive landscapes. Leverage actionable intelligence to inform your investment strategies and capitalize on the substantial growth potential within the clinical diagnostics automation space.

Lab Automation in Clinical Diagnostics Market Market Dynamics & Concentration

The Lab Automation in Clinical Diagnostics market is characterized by a moderate to high concentration, with a few dominant players holding significant market share. This concentration is driven by high research and development costs, stringent regulatory requirements, and the need for robust and reliable integrated solutions. Innovation drivers are primarily focused on enhancing assay throughput, improving precision and accuracy, miniaturizing systems, and developing intelligent software for data analysis and workflow optimization. Regulatory frameworks, such as those from the FDA and EMA, play a crucial role in market entry and product approval, emphasizing safety, efficacy, and data integrity.

Product substitutes, while limited for fully integrated automation systems, can include manual processing or semi-automated solutions for specific tasks, though these often lack the scalability and efficiency of fully automated platforms. End-user trends reveal a growing demand for faster and more accurate diagnostic results, driven by an aging global population, the increasing prevalence of chronic diseases, and the push for personalized medicine. Laboratories are increasingly seeking solutions that reduce human error, minimize operational costs, and free up skilled personnel for higher-value tasks. Merger and acquisition (M&A) activities are a significant aspect of market dynamics, with larger companies acquiring smaller innovators to expand their product portfolios, gain access to new technologies, and consolidate market presence. Recent M&A activities have focused on bolstering capabilities in areas like molecular diagnostics, artificial intelligence, and data analytics within the lab automation ecosystem.

Lab Automation in Clinical Diagnostics Market Industry Trends & Analysis

The Lab Automation in Clinical Diagnostics market is experiencing robust growth, fueled by a confluence of technological advancements, evolving healthcare demands, and strategic investments. The Compound Annual Growth Rate (CAGR) is projected to exceed 7.5% during the forecast period (2025-2033), indicating a sustained upward trajectory. Key growth drivers include the escalating need for faster and more accurate diagnostic testing to support timely clinical decision-making, particularly in the face of rising infectious disease outbreaks and the increasing burden of chronic illnesses. The drive for operational efficiency and cost reduction within healthcare systems globally also significantly propels the adoption of automated solutions, minimizing labor costs and improving laboratory throughput.

Technological disruptions are at the forefront of this market's evolution. The integration of artificial intelligence (AI) and machine learning (ML) into laboratory automation platforms is revolutionizing data analysis, predictive diagnostics, and workflow optimization. Advanced robotics, sophisticated liquid handling systems, and integrated vision systems are enhancing precision and minimizing human error. Consumer preferences, which translate to demand from healthcare providers and diagnostic laboratories, are shifting towards fully integrated, user-friendly, and scalable automation solutions that can adapt to varying laboratory volumes and specialized testing needs. The emphasis is on seamless workflows from sample accessioning to result reporting, reducing turnaround times and improving patient outcomes.

Competitive dynamics are intense, with established players continuously innovating and emerging companies introducing disruptive technologies. Strategies include product diversification, strategic partnerships for technology integration, and geographical expansion. Market penetration is steadily increasing, especially in developed regions, as laboratories recognize the long-term benefits of investing in automation. The increasing complexity of diagnostic assays, particularly in areas like genomics and proteomics, further necessitates automated solutions to handle the high-volume, intricate workflows involved. The ongoing digital transformation in healthcare, with a focus on data interoperability and connected laboratory environments, is also a significant trend shaping the future of lab automation.

Leading Markets & Segments in Lab Automation in Clinical Diagnostics Market

The global Lab Automation in Clinical Diagnostics market is segmented by equipment type, with Automated Liquid Handlers currently dominating the market share and expected to maintain its leadership position throughout the forecast period. These systems are fundamental to virtually all laboratory workflows, from sample preparation to assay execution, making them indispensable across various diagnostic disciplines. The significant demand for precise and high-throughput pipetting in molecular diagnostics, immunoassay, and clinical chemistry applications underpins their market dominance.

Automated Liquid Handlers: These are the cornerstone of lab automation, offering unparalleled precision and speed in dispensing and transferring liquids. Drivers for their dominance include the increasing volume of sample testing, the complexity of multi-step assays, and the critical need to minimize human error in sensitive diagnostic procedures. Their application spans across genomics, proteomics, drug discovery, and clinical diagnostics, ensuring broad market penetration.

Automated Plate Handlers: Essential for managing microplates, these systems automate the movement, incubation, and processing of plates, significantly accelerating throughput for high-volume screening and testing. Economic policies favoring laboratory efficiency and infrastructure development in emerging economies are key drivers for their increased adoption.

Robotic Arms: Increasingly sophisticated robotic arms are being integrated into laboratory workflows to perform complex manipulation tasks, sample tracking, and reagent management. Their flexibility and adaptability to diverse laboratory layouts and processes contribute to their growing market presence.

Automated Storage and Retrieval Systems (AS/RS): As laboratories generate and store vast amounts of samples and reagents, AS/RS solutions are becoming critical for efficient inventory management, sample tracking, and ensuring sample integrity. The need for secure and organized sample storage, especially for long-term archiving and research purposes, drives their adoption.

Vision Systems: Integrated vision systems enhance automation by enabling sample identification, quality control, and defect detection. Their role in ensuring the accuracy and reliability of automated processes is crucial, particularly in complex diagnostic workflows where sample integrity is paramount.

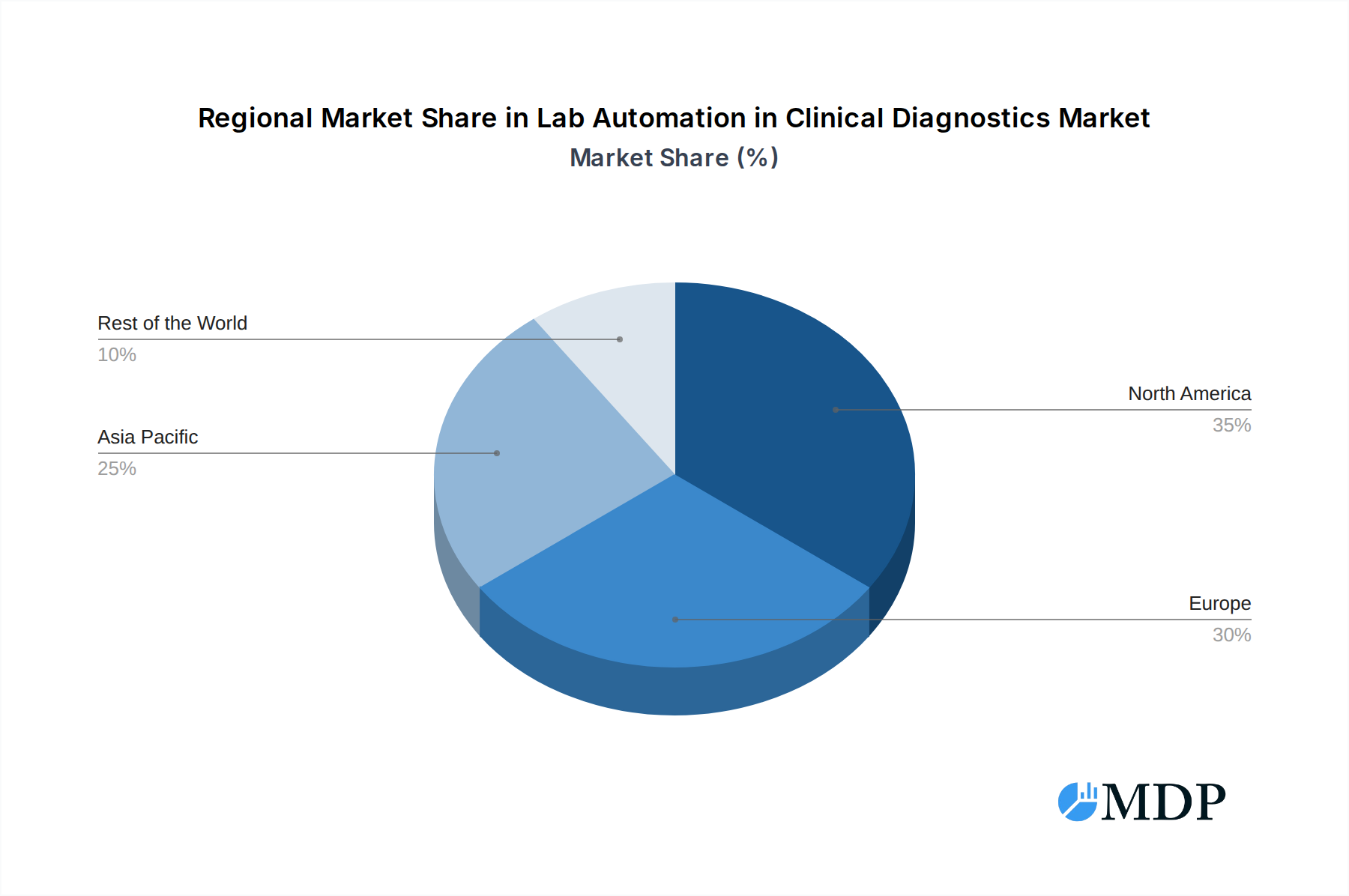

North America currently represents the leading market, driven by advanced healthcare infrastructure, high R&D spending, and a strong regulatory environment that encourages technological adoption. The United States, in particular, exhibits a high market penetration for lab automation due to the presence of major diagnostic companies and a significant volume of clinical testing.

Lab Automation in Clinical Diagnostics Market Product Developments

Product developments in the Lab Automation in Clinical Diagnostics market are continuously pushing the boundaries of efficiency and accuracy. Innovations are centered around modular designs for enhanced flexibility, AI-powered analytics for predictive insights, and miniaturized systems to address space constraints in laboratories. Companies are focusing on creating integrated platforms that automate entire workflows, from sample preparation to result interpretation, thereby reducing turnaround times and minimizing human intervention. Applications are expanding to include personalized medicine, infectious disease diagnostics, and advanced cancer screening, where high-throughput and precise automation are critical. The competitive advantage lies in offering robust, scalable, and user-friendly solutions that seamlessly integrate into existing laboratory infrastructures, delivering reliable data for critical clinical decisions.

Key Drivers of Lab Automation in Clinical Diagnostics Market Growth

The growth of the Lab Automation in Clinical Diagnostics market is propelled by several key factors. Technological advancements such as AI, robotics, and advanced sensor technologies are enabling more sophisticated and efficient automated systems. The increasing global burden of chronic diseases and infectious diseases necessitates higher throughput and accuracy in diagnostic testing, driving demand for automation. Regulatory bodies' emphasis on improving diagnostic accuracy and reducing errors further encourages the adoption of automated solutions. Economic factors, including the drive for healthcare cost containment, highlight the long-term cost-saving benefits of lab automation. Furthermore, the growing awareness among healthcare providers about the benefits of faster turnaround times and improved patient outcomes is a significant catalyst.

Challenges in the Lab Automation in Clinical Diagnostics Market Market

Despite the strong growth trajectory, the Lab Automation in Clinical Diagnostics market faces several challenges. High initial investment costs for advanced automation systems can be a barrier for smaller laboratories or those with limited budgets. Integration complexities with existing laboratory information systems (LIS) and other equipment can pose significant technical hurdles. The need for specialized skilled personnel to operate and maintain complex automated systems can also be a constraint. Stringent and evolving regulatory requirements demand continuous compliance and validation, adding to development and operational costs. Supply chain disruptions, as seen in recent global events, can impact the availability of critical components and finished products. Additionally, resistance to change within established laboratory workflows and a preference for traditional methods can slow down adoption rates.

Emerging Opportunities in Lab Automation in Clinical Diagnostics Market

Emerging opportunities in the Lab Automation in Clinical Diagnostics market are abundant, driven by ongoing technological innovation and evolving healthcare needs. The increasing demand for point-of-care diagnostics presents an opportunity for developing compact, automated, and user-friendly systems that can be deployed in decentralized settings. The expansion of genomic and proteomic testing creates a need for highly specialized and high-throughput automation solutions. The growing focus on personalized medicine and companion diagnostics requires precise and reproducible automation for complex assays. Strategic partnerships between automation providers, reagent manufacturers, and AI developers are fostering the creation of comprehensive, end-to-end solutions. Furthermore, the expansion of healthcare infrastructure in emerging economies presents a significant untapped market for lab automation solutions.

Leading Players in the Lab Automation in Clinical Diagnostics Market Sector

- Thermo Fisher Scientific

- Danaher Corporation

- Hudson Robotics

- Becton Dickinson

- Synchron Lab Automation

- Agilent Technologies Inc

- Siemens Healthineers AG

- Tecan Group Ltd

- Perkinelmer Inc

- Honeywell International Inc

- Bio-Rad Laboratories Inc

- Roche Holding AG

- Shimadzu Corporation

- Aurora Biomed

Key Milestones in Lab Automation in Clinical Diagnostics Market Industry

- March 2021: Roche announced the launch of cobas pure integrated solutions in countries accepting the CE mark. This new compact analyzer combines three technologies on a single platform, simplifying daily operations for labs with limited space and resources.

- March 2020: Thermo Fisher announced its intent to acquire QIAGEN N.V., aiming to expand its specialty diagnostics portfolio with attractive molecular diagnostics capabilities, including infectious disease testing. QIAGEN's instruments can automate these workflows, while its bioinformatics systems provide actionable insights.

Strategic Outlook for Lab Automation in Clinical Diagnostics Market Market

The strategic outlook for the Lab Automation in Clinical Diagnostics market is overwhelmingly positive, driven by an increasing recognition of its critical role in modern healthcare. Future growth will be accelerated by the continued integration of AI and machine learning, enabling smarter and more predictive diagnostic capabilities. The development of modular and scalable automation platforms will cater to a wider range of laboratory sizes and needs, from high-throughput research facilities to smaller clinical settings. Strategic partnerships and collaborations will be key in developing comprehensive solutions that address the entire diagnostic workflow, fostering greater interoperability and data management. The focus on miniaturization and the development of user-friendly interfaces will further democratize access to advanced automation. As the demand for rapid, accurate, and cost-effective diagnostics continues to rise globally, the market for lab automation is poised for sustained expansion, presenting significant opportunities for innovation and investment.

Lab Automation in Clinical Diagnostics Market Segmentation

-

1. Equipment

- 1.1. Automated Liquid Handlers

- 1.2. Automated Plate Handlers

- 1.3. Robotic Arms

- 1.4. Automated Storage and Retrieval Systems (AS/RS)

- 1.5. Vision Systems

Lab Automation in Clinical Diagnostics Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Lab Automation in Clinical Diagnostics Market Regional Market Share

Geographic Coverage of Lab Automation in Clinical Diagnostics Market

Lab Automation in Clinical Diagnostics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Equipment

- 5.1.1. Automated Liquid Handlers

- 5.1.2. Automated Plate Handlers

- 5.1.3. Robotic Arms

- 5.1.4. Automated Storage and Retrieval Systems (AS/RS)

- 5.1.5. Vision Systems

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Equipment

- 6. Global Lab Automation in Clinical Diagnostics Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Equipment

- 6.1.1. Automated Liquid Handlers

- 6.1.2. Automated Plate Handlers

- 6.1.3. Robotic Arms

- 6.1.4. Automated Storage and Retrieval Systems (AS/RS)

- 6.1.5. Vision Systems

- 6.1. Market Analysis, Insights and Forecast - by Equipment

- 7. North America Lab Automation in Clinical Diagnostics Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Equipment

- 7.1.1. Automated Liquid Handlers

- 7.1.2. Automated Plate Handlers

- 7.1.3. Robotic Arms

- 7.1.4. Automated Storage and Retrieval Systems (AS/RS)

- 7.1.5. Vision Systems

- 7.1. Market Analysis, Insights and Forecast - by Equipment

- 8. Europe Lab Automation in Clinical Diagnostics Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Equipment

- 8.1.1. Automated Liquid Handlers

- 8.1.2. Automated Plate Handlers

- 8.1.3. Robotic Arms

- 8.1.4. Automated Storage and Retrieval Systems (AS/RS)

- 8.1.5. Vision Systems

- 8.1. Market Analysis, Insights and Forecast - by Equipment

- 9. Asia Pacific Lab Automation in Clinical Diagnostics Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Equipment

- 9.1.1. Automated Liquid Handlers

- 9.1.2. Automated Plate Handlers

- 9.1.3. Robotic Arms

- 9.1.4. Automated Storage and Retrieval Systems (AS/RS)

- 9.1.5. Vision Systems

- 9.1. Market Analysis, Insights and Forecast - by Equipment

- 10. Rest of the World Lab Automation in Clinical Diagnostics Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Equipment

- 10.1.1. Automated Liquid Handlers

- 10.1.2. Automated Plate Handlers

- 10.1.3. Robotic Arms

- 10.1.4. Automated Storage and Retrieval Systems (AS/RS)

- 10.1.5. Vision Systems

- 10.1. Market Analysis, Insights and Forecast - by Equipment

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Thermo Fisher Scientific

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Danaher Corporation

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Hudson Robotics

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Becton Dickinson

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Synchron Lab Automation

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Agilent Technologies Inc

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Siemens Healthineers AG

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Tecan Group Ltd

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Perkinelmer Inc

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Honeywell International Inc

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Bio-Rad Laboratories Inc

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Roche Holding AG

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Shimadzu Corporation

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 Aurora Biomed*List Not Exhaustive

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.1 Thermo Fisher Scientific

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Lab Automation in Clinical Diagnostics Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Lab Automation in Clinical Diagnostics Market Revenue (billion), by Equipment 2025 & 2033

- Figure 3: North America Lab Automation in Clinical Diagnostics Market Revenue Share (%), by Equipment 2025 & 2033

- Figure 4: North America Lab Automation in Clinical Diagnostics Market Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Lab Automation in Clinical Diagnostics Market Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Lab Automation in Clinical Diagnostics Market Revenue (billion), by Equipment 2025 & 2033

- Figure 7: Europe Lab Automation in Clinical Diagnostics Market Revenue Share (%), by Equipment 2025 & 2033

- Figure 8: Europe Lab Automation in Clinical Diagnostics Market Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Lab Automation in Clinical Diagnostics Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Lab Automation in Clinical Diagnostics Market Revenue (billion), by Equipment 2025 & 2033

- Figure 11: Asia Pacific Lab Automation in Clinical Diagnostics Market Revenue Share (%), by Equipment 2025 & 2033

- Figure 12: Asia Pacific Lab Automation in Clinical Diagnostics Market Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Lab Automation in Clinical Diagnostics Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Rest of the World Lab Automation in Clinical Diagnostics Market Revenue (billion), by Equipment 2025 & 2033

- Figure 15: Rest of the World Lab Automation in Clinical Diagnostics Market Revenue Share (%), by Equipment 2025 & 2033

- Figure 16: Rest of the World Lab Automation in Clinical Diagnostics Market Revenue (billion), by Country 2025 & 2033

- Figure 17: Rest of the World Lab Automation in Clinical Diagnostics Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Equipment 2020 & 2033

- Table 2: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Equipment 2020 & 2033

- Table 4: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Equipment 2020 & 2033

- Table 6: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Equipment 2020 & 2033

- Table 8: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Equipment 2020 & 2033

- Table 10: Global Lab Automation in Clinical Diagnostics Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Lab Automation in Clinical Diagnostics Market?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the Lab Automation in Clinical Diagnostics Market?

Key companies in the market include Thermo Fisher Scientific, Danaher Corporation, Hudson Robotics, Becton Dickinson, Synchron Lab Automation, Agilent Technologies Inc, Siemens Healthineers AG, Tecan Group Ltd, Perkinelmer Inc, Honeywell International Inc, Bio-Rad Laboratories Inc, Roche Holding AG, Shimadzu Corporation, Aurora Biomed*List Not Exhaustive.

3. What are the main segments of the Lab Automation in Clinical Diagnostics Market?

The market segments include Equipment.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.36 billion as of 2022.

5. What are some drivers contributing to market growth?

Flexibility and Adaptability of Lab Automation Systems; Growing Demand from Drug Discovery and Genomics.

6. What are the notable trends driving market growth?

Automated Liquid Handlers is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Flexibility and Adaptability of Lab Automation Systems; Growing Demand from Drug Discovery and Genomics.

8. Can you provide examples of recent developments in the market?

March 2021 - Roche announced the launch of cobas pure integrated solutions in countries accepting the CE mark. This new compact analyzer combines three technologies on a single platform helping to simplify daily operations in labs with limited space and resources.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Lab Automation in Clinical Diagnostics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Lab Automation in Clinical Diagnostics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Lab Automation in Clinical Diagnostics Market?

To stay informed about further developments, trends, and reports in the Lab Automation in Clinical Diagnostics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence