Key Insights

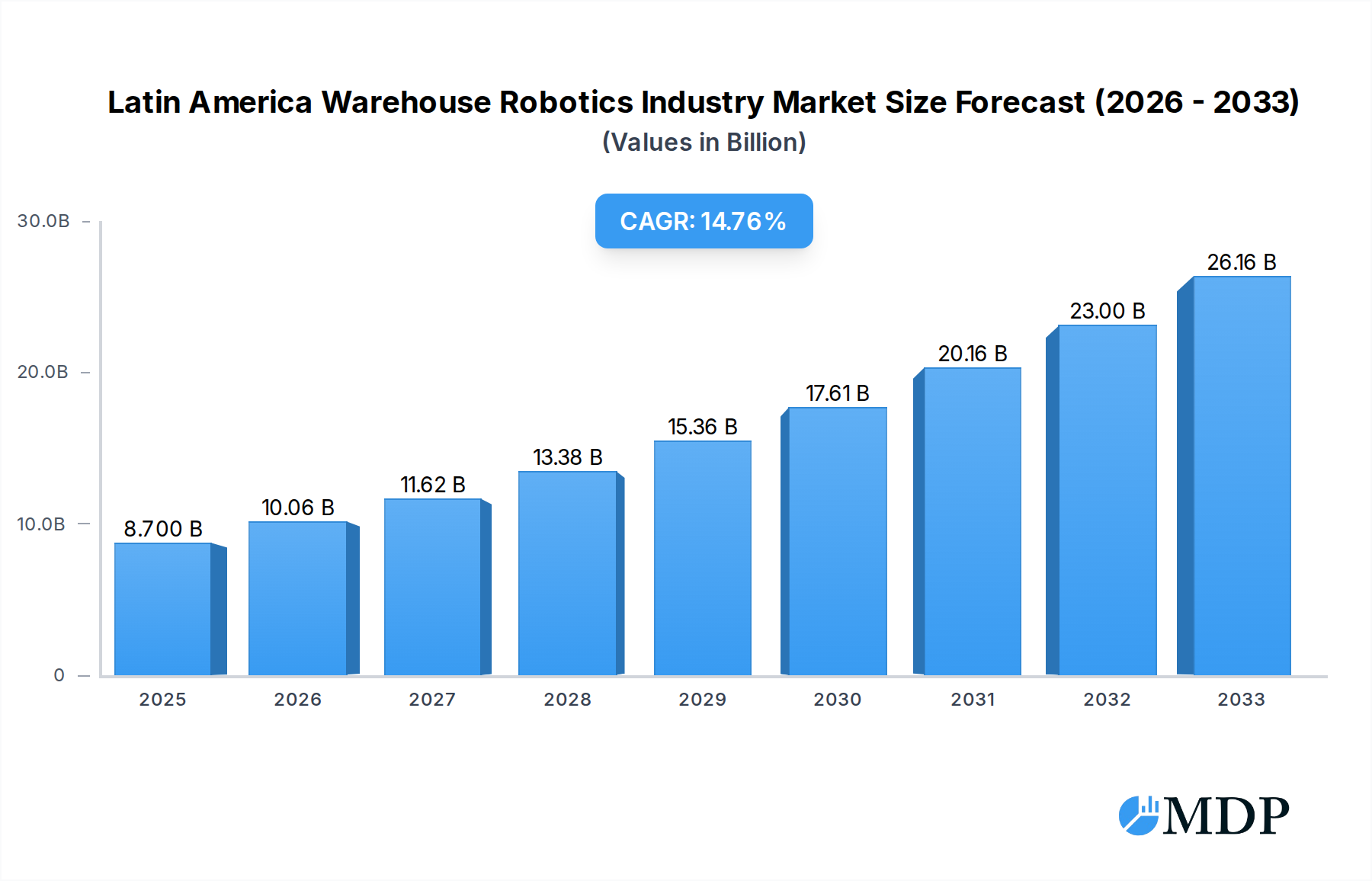

The Latin America Warehouse Robotics Industry is poised for significant expansion, driven by the imperative to enhance operational efficiency, reduce costs, and address labor shortages across diverse sectors. With a projected market size of $8.7 billion in 2025, the region is set to witness an impressive Compound Annual Growth Rate (CAGR) of 15.7% during the forecast period of 2025-2033. This robust growth is primarily fueled by the increasing adoption of industrial robots, automated storage and retrieval systems (ASRS), and mobile robots (AGVs and AMRs) by key end-users such as the Food and Beverage, Automotive, and Retail industries. The demand for sophisticated sorting systems and advanced palletizers further underscores the market's upward trajectory, as businesses seek to optimize their supply chain operations for greater speed and accuracy. Emerging economies within Latin America, including Brazil, Mexico, and Colombia, are at the forefront of this technological revolution, investing heavily in warehouse automation to remain competitive in the global marketplace. The inherent benefits of robotics, such as improved safety, reduced errors, and 24/7 operational capabilities, are compelling compelling factors for businesses to embrace these advanced solutions.

Latin America Warehouse Robotics Industry Market Size (In Billion)

Several pivotal trends are shaping the Latin America warehouse robotics landscape. The escalating demand for e-commerce fulfillment, particularly in the Retail and Food & Beverage sectors, necessitates faster picking, packing, and shipping processes, which warehouse robotics are uniquely positioned to deliver. Furthermore, the integration of AI and machine learning with robotic systems is enabling more intelligent and adaptable automation solutions, allowing for real-time optimization of warehouse workflows. While the initial investment cost can be a restraining factor for some smaller enterprises, the long-term return on investment through increased productivity and reduced operational expenditure is proving to be a significant incentive. The expanding use of mobile robots (AGVs and AMRs) for material handling and the growing sophistication of ASRS for space optimization are key indicators of the market's maturity and its capacity to cater to a wide spectrum of warehousing needs. As more companies in Latin America recognize the transformative power of these technologies, the market is expected to achieve substantial and sustained growth.

Latin America Warehouse Robotics Industry Company Market Share

Dive deep into the burgeoning Latin America warehouse robotics market with our comprehensive report. This indispensable analysis forecasts a significant market expansion, projected to reach over $25 billion by 2033, driven by robust CAGR of 18.5% from 2025 to 2033. Explore the intricate dynamics shaping this rapidly evolving sector, from technological advancements and end-user adoption to key player strategies and emerging opportunities. Essential for logistics providers, manufacturers, investors, and technology developers seeking to capitalize on the region's transformative potential.

Latin America Warehouse Robotics Industry Market Dynamics & Concentration

The Latin America warehouse robotics market, projected to reach over $25 billion by 2033, exhibits moderate concentration with a few dominant players alongside a growing number of innovative newcomers. Innovation is a primary driver, fueled by the pressing need for increased efficiency, reduced operational costs, and improved accuracy in warehousing and logistics across the region. Key innovation areas include advancements in Artificial Intelligence (AI) for smarter robot navigation, enhanced human-robot collaboration, and the development of more agile and adaptable robotic systems. Regulatory frameworks are gradually evolving, with some countries beginning to implement guidelines for automation and industrial safety, though inconsistencies remain a challenge. Product substitutes, such as manual labor and basic automation tools, are gradually losing ground as the cost-effectiveness and performance of robotics become more apparent. End-user trends are strongly influenced by the rapid growth of e-commerce, demanding faster fulfillment times and increased order accuracy, making automation a critical necessity. Furthermore, the increasing sophistication of the automotive and pharmaceutical sectors, coupled with the expanding food and beverage industry's need for efficient cold chain logistics, are significant adoption drivers. Mergers and acquisitions (M&A) are present but not yet widespread, indicating a market ripe for consolidation and strategic partnerships. For instance, the recent acquisition of Fetch Robotics by Zebra Technologies signifies a trend towards larger players integrating specialized robotics capabilities. We anticipate approximately 15-20 significant M&A deals within the study period as companies seek to expand their technological portfolios and market reach.

Latin America Warehouse Robotics Industry Industry Trends & Analysis

The Latin America warehouse robotics industry is experiencing a paradigm shift, characterized by accelerating adoption and transformative technological integration. The market is projected to expand from an estimated $8 billion in 2025 to over $25 billion by 2033, exhibiting a compelling compound annual growth rate (CAGR) of 18.5% during the forecast period. This robust growth is primarily propelled by the unrelenting surge in e-commerce, which necessitates optimized inventory management, faster order fulfillment, and more accurate picking and packing processes. The inherent labor shortages and rising labor costs in many Latin American countries further amplify the attractiveness of robotic automation as a sustainable and cost-effective solution. Technological disruptions are playing a pivotal role, with the increasing sophistication of Artificial Intelligence (AI) and Machine Learning (ML) enabling robots to perform more complex tasks, learn from their environment, and collaborate seamlessly with human workers. The advent of Autonomous Mobile Robots (AMRs) is revolutionizing material handling, offering greater flexibility and adaptability compared to traditional Automated Guided Vehicles (AGVs). Consumer preferences for quicker delivery times and personalized shopping experiences are directly translating into demands for highly efficient and responsive warehousing operations, which robots are uniquely positioned to deliver. Competitive dynamics are intensifying as both established global players and agile local startups vie for market share. Companies are increasingly focusing on offering integrated solutions that encompass hardware, software, and after-sales support to cater to the diverse needs of the Latin American market. Market penetration, while still in its nascent stages compared to developed economies, is rapidly increasing, with an estimated 25-30% of large-scale warehouses exploring or implementing robotic solutions by the end of the forecast period. The ongoing digital transformation across various industries, from retail and food & beverage to automotive and pharmaceuticals, is creating a fertile ground for the widespread adoption of warehouse robotics.

Leading Markets & Segments in Latin America Warehouse Robotics Industry

The Latin America warehouse robotics market is witnessing significant expansion across various segments, with certain regions and end-user industries emerging as dominant forces. Brazil stands out as the leading market, driven by its large economy, extensive manufacturing base, and the rapid growth of its e-commerce sector, accounting for approximately 30% of the regional market share. Mexico follows closely, benefiting from its strong manufacturing and export capabilities, particularly in the automotive and electronics industries.

By Type:

- Mobile Robots (AGVs and AMRs): This segment is experiencing the most substantial growth, projected to capture over 40% of the market by 2033. Their flexibility, scalability, and ability to navigate dynamic environments make them ideal for a wide range of warehouse operations.

- Automated Storage and Retrieval Systems (ASRS): ASRS holds a significant share, around 20%, especially in high-density storage needs for industries like retail and food & beverage.

- Industrial Robots: This segment, including robotic arms for picking and palletizing, constitutes roughly 15% of the market, crucial for repetitive tasks.

- Conveyors and Sortation Systems: These traditional automation components still hold a strong presence, accounting for approximately 15%, often integrated with newer robotic solutions.

By Function:

- Storage: This is the most dominant function, accounting for over 50% of robotic applications, encompassing inventory management and order picking.

- Packaging: With the e-commerce boom, automated packaging solutions are seeing rapid adoption, representing around 20% of the market.

- Trans-shipments: Increasingly important for distribution centers, this function accounts for approximately 15%.

By End User:

- Retail: The e-commerce surge has made retail the leading end-user, accounting for an estimated 35% of the market.

- Food and Beverage: This sector's demand for efficiency, hygiene, and cold chain logistics makes it a key adopter, representing roughly 25%.

- Automotive: With complex supply chains and JIT manufacturing, the automotive industry is a significant player, contributing around 20%.

- Electrical and Electronics: Similar to automotive, this sector benefits from precise and efficient handling of high-value components.

- Pharmaceutical: The stringent regulatory requirements and need for accuracy drive adoption, though at a smaller percentage currently.

Key drivers for dominance in these segments include supportive economic policies, investment in infrastructure development, and a growing awareness of the ROI offered by warehouse automation. The increasing adoption of Industry 4.0 principles across Latin American industries is further fueling the demand for these advanced robotic solutions.

Latin America Warehouse Robotics Industry Product Developments

Product developments in Latin America's warehouse robotics sector are characterized by a strong emphasis on enhanced autonomy, AI-driven decision-making, and seamless integration with existing warehouse management systems. Innovations are focusing on creating more adaptable robots capable of handling a wider variety of goods, from delicate produce to heavy industrial parts, with increased precision. The development of swarm robotics and collaborative robots (cobots) that can work alongside human operators safely and efficiently is a significant trend, boosting productivity and reducing the risk of injury. Furthermore, advancements in battery technology are leading to longer operational times and faster charging capabilities, addressing a key concern for large-scale deployments. These developments are aimed at providing businesses with scalable, flexible, and cost-effective solutions that can be quickly implemented to meet evolving market demands.

Key Drivers of Latin America Warehouse Robotics Industry Growth

Several interconnected factors are propelling the growth of the Latin America warehouse robotics industry. The exponential growth of e-commerce is a primary catalyst, demanding greater speed, accuracy, and efficiency in order fulfillment. Technological advancements, particularly in AI, machine learning, and sensor technology, are making robots more intelligent, versatile, and cost-effective. Furthermore, the increasing cost of labor and the persistent shortage of skilled warehouse personnel across the region are making automation an indispensable solution for businesses. Government initiatives promoting industrial modernization and digital transformation are also playing a crucial role in encouraging investment in robotics. Finally, the growing awareness of the significant ROI achievable through improved operational efficiency, reduced errors, and enhanced safety is driving widespread adoption.

Challenges in the Latin America Warehouse Robotics Industry Market

Despite the promising growth trajectory, the Latin America warehouse robotics industry faces several significant challenges. High upfront investment costs for robotic systems can be a substantial barrier for small and medium-sized enterprises (SMEs), hindering wider market penetration. Infrastructure limitations, including unreliable power grids and underdeveloped connectivity in certain regions, can impact the performance and scalability of robotic deployments. A significant skills gap exists, with a shortage of trained personnel to operate, maintain, and program these advanced systems, necessitating extensive training programs. Moreover, navigating diverse and sometimes fragmented regulatory landscapes across different Latin American countries can add complexity and delays to market entry and expansion. Intense competition from established global players and increasingly sophisticated local integrators also presents a challenge for newer entrants.

Emerging Opportunities in Latin America Warehouse Robotics Industry

The Latin America warehouse robotics industry is ripe with emerging opportunities for growth and innovation. The increasing adoption of Industry 4.0 principles across manufacturing and logistics sectors is creating a strong demand for smart automation solutions. The burgeoning e-commerce market, especially in countries like Brazil and Mexico, presents vast potential for companies offering end-to-end fulfillment solutions. Furthermore, the growing need for supply chain resilience and visibility is driving investment in advanced robotics for better inventory management and real-time tracking. Strategic partnerships between technology providers, logistics companies, and end-users can unlock new market segments and accelerate adoption. The development of tailored robotic solutions addressing specific regional challenges, such as those in the food and beverage or pharmaceutical industries, offers significant untapped potential.

Leading Players in the Latin America Warehouse Robotics Industry Sector

- Honeywell International Inc

- Syrius Robotics

- Fetch Robotics Inc

- Singapore Technologies Engineering Ltd (Aethon Incorporation)

- InVia Robotics Inc

- Omron Adept Technologies

- Toshiba Corporation

- Kiva Systems (Amazon Robotics LLC)

- Fanuc Corporation

- Geek+ Inc

- Grey Orange Pte Ltd

- Locus Robotic

- ABB Limited

Key Milestones in Latin America Warehouse Robotics Industry Industry

- 2019: Increased investment in e-commerce infrastructure driving early adoption of automated solutions.

- 2020: COVID-19 pandemic accelerates focus on touchless automation and efficiency gains.

- 2021: Significant venture capital funding rounds for leading robotics startups in the region.

- 2022: Growing awareness and pilot projects for Autonomous Mobile Robots (AMRs) in key markets.

- 2023: Major logistics providers begin large-scale implementation of robotic solutions.

- 2024 (Est.): Growing M&A activity as larger players seek to consolidate market presence.

Strategic Outlook for Latin America Warehouse Robotics Industry Market

The strategic outlook for the Latin America warehouse robotics industry is exceptionally bright, characterized by sustained growth driven by e-commerce expansion, technological advancements, and the imperative for operational efficiency. Companies that focus on providing integrated, scalable, and intelligent automation solutions, coupled with robust after-sales support, will be best positioned for success. Strategic partnerships and collaborations will be crucial for market penetration and the development of localized offerings. Embracing AI and machine learning for enhanced robot capabilities and exploring opportunities in emerging markets within the region will be key accelerators. Investment in workforce training and addressing infrastructure challenges will be vital for unlocking the full potential of this dynamic and rapidly evolving market.

Latin America Warehouse Robotics Industry Segmentation

-

1. Type

- 1.1. Industrial Robots

- 1.2. Sortation Systems

- 1.3. Conveyors

- 1.4. Palletizers

- 1.5. Automated Storage and Retrieval System (ASRS)

- 1.6. Mobile Robots (AGVs and AMRs)

- 1.7. Others

-

2. Function

- 2.1. Storage

- 2.2. Packaging

- 2.3. Trans-shipments

- 2.4. Other Functions

-

3. End User

- 3.1. Food and Beverage

- 3.2. Automotive

- 3.3. Retail

- 3.4. Electrical and Electronics

- 3.5. Pharmaceutical

- 3.6. Other End Users

Latin America Warehouse Robotics Industry Segmentation By Geography

-

1. Latin America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Mexico

- 1.6. Peru

- 1.7. Venezuela

- 1.8. Ecuador

- 1.9. Bolivia

- 1.10. Paraguay

Latin America Warehouse Robotics Industry Regional Market Share

Geographic Coverage of Latin America Warehouse Robotics Industry

Latin America Warehouse Robotics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Industrial Robots

- 5.1.2. Sortation Systems

- 5.1.3. Conveyors

- 5.1.4. Palletizers

- 5.1.5. Automated Storage and Retrieval System (ASRS)

- 5.1.6. Mobile Robots (AGVs and AMRs)

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Function

- 5.2.1. Storage

- 5.2.2. Packaging

- 5.2.3. Trans-shipments

- 5.2.4. Other Functions

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Food and Beverage

- 5.3.2. Automotive

- 5.3.3. Retail

- 5.3.4. Electrical and Electronics

- 5.3.5. Pharmaceutical

- 5.3.6. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Latin America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Latin America Warehouse Robotics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Industrial Robots

- 6.1.2. Sortation Systems

- 6.1.3. Conveyors

- 6.1.4. Palletizers

- 6.1.5. Automated Storage and Retrieval System (ASRS)

- 6.1.6. Mobile Robots (AGVs and AMRs)

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Function

- 6.2.1. Storage

- 6.2.2. Packaging

- 6.2.3. Trans-shipments

- 6.2.4. Other Functions

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Food and Beverage

- 6.3.2. Automotive

- 6.3.3. Retail

- 6.3.4. Electrical and Electronics

- 6.3.5. Pharmaceutical

- 6.3.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Honeywell International Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Syrius Robotics

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Fetch Robotics Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Singapore Technologies Engineering Ltd (Aethon Incorporation)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 InVia Robotics Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Omron Adept Technologies

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Toshiba Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Kiva Systems (Amazon Robotics LLC)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Fanuc Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Geek+ Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Grey Orange Pte Ltd

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Locus Robotic

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 ABB Limited

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Honeywell International Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Latin America Warehouse Robotics Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Latin America Warehouse Robotics Industry Share (%) by Company 2025

List of Tables

- Table 1: Latin America Warehouse Robotics Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Latin America Warehouse Robotics Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 3: Latin America Warehouse Robotics Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 4: Latin America Warehouse Robotics Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Latin America Warehouse Robotics Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Latin America Warehouse Robotics Industry Revenue billion Forecast, by Function 2020 & 2033

- Table 7: Latin America Warehouse Robotics Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 8: Latin America Warehouse Robotics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Brazil Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Argentina Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Chile Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Colombia Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Peru Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Venezuela Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Ecuador Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Bolivia Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Paraguay Latin America Warehouse Robotics Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Warehouse Robotics Industry?

The projected CAGR is approximately 15.7%.

2. Which companies are prominent players in the Latin America Warehouse Robotics Industry?

Key companies in the market include Honeywell International Inc, Syrius Robotics, Fetch Robotics Inc, Singapore Technologies Engineering Ltd (Aethon Incorporation), InVia Robotics Inc, Omron Adept Technologies, Toshiba Corporation, Kiva Systems (Amazon Robotics LLC), Fanuc Corporation, Geek+ Inc, Grey Orange Pte Ltd, Locus Robotic, ABB Limited.

3. What are the main segments of the Latin America Warehouse Robotics Industry?

The market segments include Type, Function, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.17 billion as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Number of SKUs; Increasing Investments in Technology and Robotics.

6. What are the notable trends driving market growth?

The Adoption of Industrial Robotics Expected to Act as a Significant Driving Factor.

7. Are there any restraints impacting market growth?

; Stringent Regulatory Requirements; Hight Cost.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Warehouse Robotics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Warehouse Robotics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Warehouse Robotics Industry?

To stay informed about further developments, trends, and reports in the Latin America Warehouse Robotics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence