Key Insights

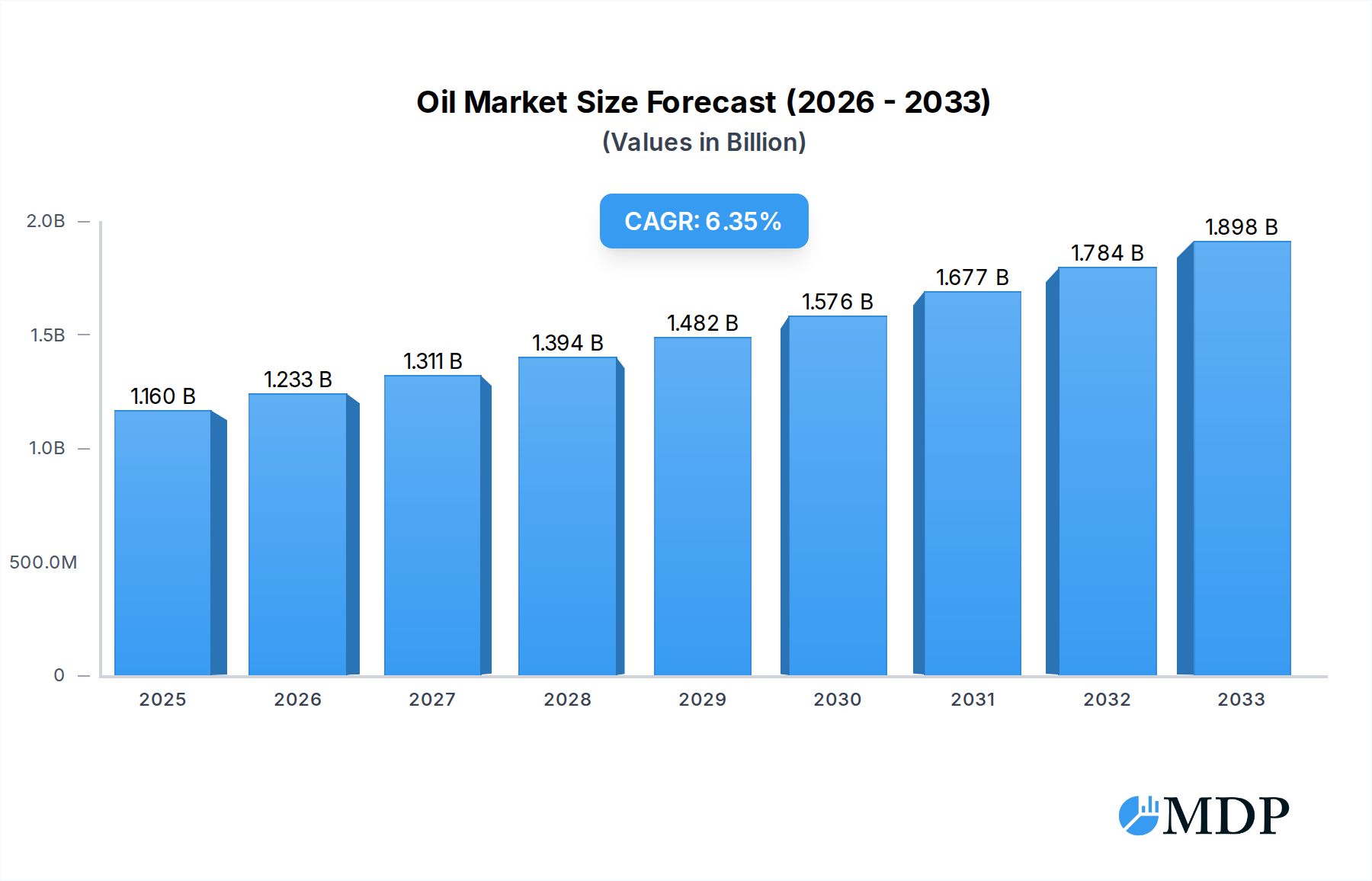

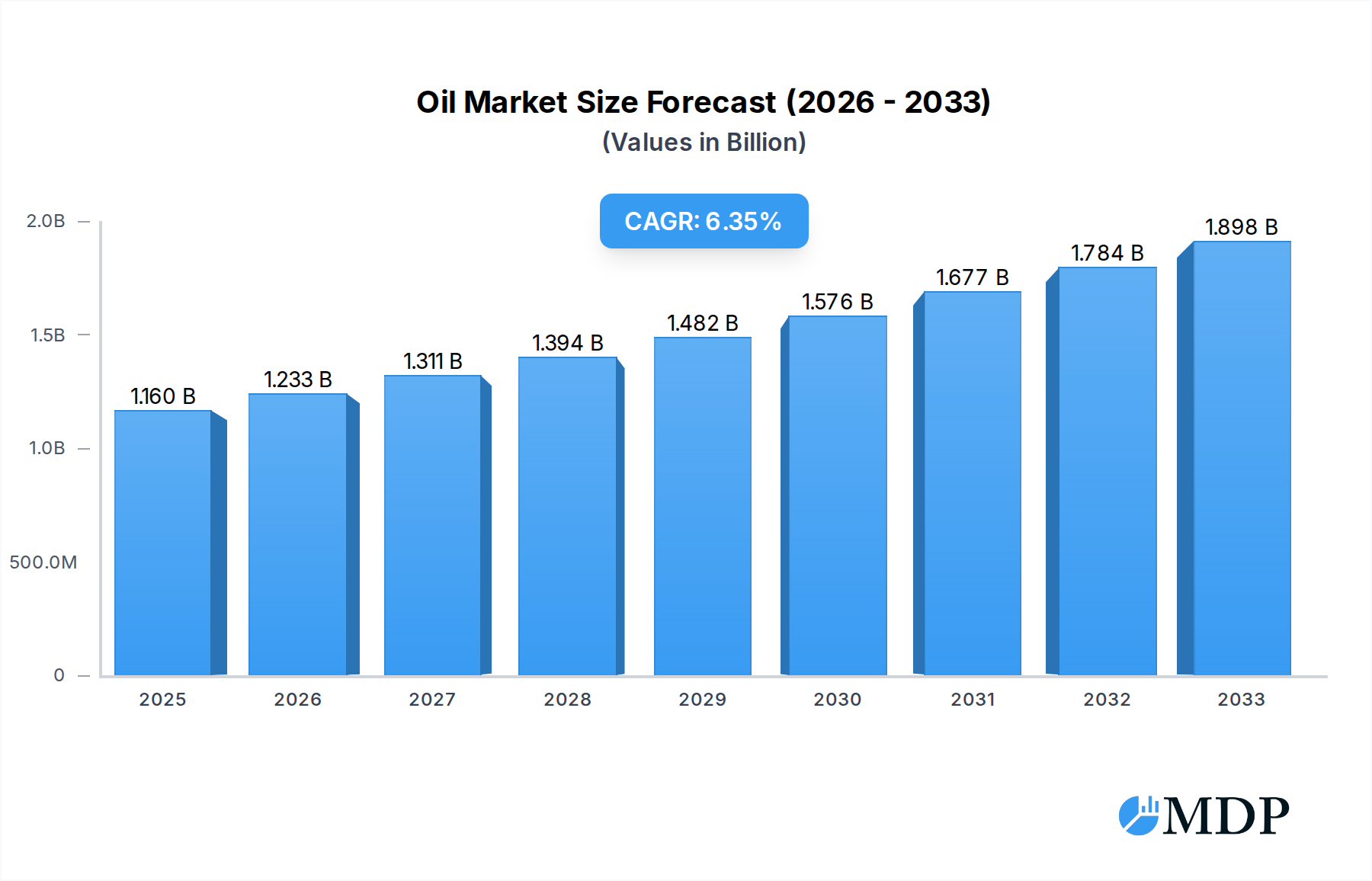

The global Oil & Gas Main Automation Contractor (MAC) market is poised for robust expansion, with a current market size estimated at USD 1.16 Billion in 2025 and projected to grow at a Compound Annual Growth Rate (CAGR) of 6.28% through 2033. This impressive growth is fueled by a critical need for enhanced operational efficiency, safety, and compliance across the entire oil and gas value chain. Key drivers include the increasing complexity of offshore and onshore exploration and production, the necessity for sophisticated automation in midstream infrastructure to manage vast volumes of hydrocarbons, and the imperative for advanced control systems in downstream refining and petrochemical operations. Furthermore, the continuous drive for digital transformation within the industry, encompassing the adoption of Industrial Internet of Things (IIoT), artificial intelligence, and advanced analytics, is a significant growth catalyst. This technological integration allows for predictive maintenance, real-time monitoring, and optimized resource allocation, ultimately boosting productivity and reducing operational expenditures.

Oil & Gas Main Automation Contractor Industry Market Size (In Billion)

The market is segmented into distinct operational areas, with the Upstream sector, encompassing both offshore and onshore activities, representing a significant portion due to the inherent complexities and scale of exploration and extraction. The Midstream sector also presents substantial opportunities as it involves the transportation and storage of oil and gas, demanding high levels of automation for safety and efficiency. The Downstream sector, comprising refining and petrochemical plants, relies heavily on advanced automation for process control and product quality. Project size also dictates market dynamics, with both small to medium-sized projects (USD 5 million to USD 30 million) and large-scale ventures (USD 31 million and Above) contributing to the overall market landscape. Major industry players like ABB Ltd, Honeywell International Inc., Emerson Electric Co., Siemens AG, Schneider Electric SE, Rockwell Automation Inc., and Yokogawa Electric Corporation are at the forefront, innovating and providing integrated automation solutions that address the evolving needs of the oil and gas industry, particularly in regions with substantial exploration and production activities.

Oil & Gas Main Automation Contractor Industry Company Market Share

Oil & Gas Main Automation Contractor Market Report: Comprehensive Analysis & Future Outlook (2019-2033)

This in-depth market intelligence report provides a definitive analysis of the Oil & Gas Main Automation Contractor (MAC) industry, a critical sector underpinning the efficiency, safety, and profitability of upstream, midstream, and downstream operations. Covering the extensive study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033, this report delves into market dynamics, industry trends, leading segments, and the strategic landscape. Discover actionable insights into market concentration, innovation drivers, regulatory influences, and the evolving needs of end-users. Explore key industry developments, significant project sizes ranging from USD 5 million to USD 30 million (Small and Medium) and USD 31 million and Above (Large), and the competitive strategies of major players like ABB Lt, Honeywell International Inc, Emerson Electric Co, Siemens AG, Schneider Electric SE, Rockwell Automation Inc, and Yokogawa Electric Corporation. Essential for strategists, investors, and decision-makers, this report illuminates the future trajectory of oil and gas automation contracting.

Oil & Gas Main Automation Contractor Industry Market Dynamics & Concentration

The Oil & Gas Main Automation Contractor (MAC) industry is characterized by a moderate to high concentration, driven by the substantial capital requirements, specialized expertise, and long-term project lifecycles inherent in this sector. The market share distribution is led by a few key global players, often holding significant portions of large-scale projects. Innovation drivers are predominantly centered on digital transformation initiatives, including the adoption of Industrial Internet of Things (IIoT), artificial intelligence (AI) for predictive maintenance and operational optimization, and advanced cybersecurity solutions. Regulatory frameworks play a crucial role, with stringent safety and environmental compliance mandates influencing technology choices and contractor selection, particularly in regions with robust oversight like North America and Europe. Product substitutes, while present in individual automation components, are less of a direct threat to integrated MAC solutions which offer end-to-end project management and lifecycle support. End-user trends are shifting towards greater automation, remote operational capabilities, and enhanced data analytics to improve efficiency and reduce operational costs. Mergers & Acquisitions (M&A) activities are a significant aspect of market dynamics, with companies seeking to consolidate their market positions, expand their technological portfolios, and gain access to new geographic regions. The number of M&A deals is expected to remain steady, reflecting a strategic consolidation within the industry to capture economies of scale and offer more comprehensive service offerings.

Oil & Gas Main Automation Contractor Industry Industry Trends & Analysis

The Oil & Gas Main Automation Contractor (MAC) industry is experiencing robust growth, propelled by several key trends and analytical factors. The Compound Annual Growth Rate (CAGR) is projected to be substantial, fueled by the continuous need for modernizing aging infrastructure and developing new energy resources globally. A significant growth driver is the relentless pursuit of operational efficiency and cost reduction across the entire oil and gas value chain, from exploration and production to refining and distribution. Technological disruptions are at the forefront of this evolution, with the increasing adoption of digitalization, IIoT, AI, machine learning, and cloud computing. These technologies enable enhanced real-time monitoring, predictive maintenance, remote operations, and optimized process control, leading to reduced downtime and improved safety. Consumer preferences, in this context, are increasingly focused on contractors offering integrated solutions that encompass design, engineering, procurement, construction, commissioning, and ongoing lifecycle support. There is a growing demand for cybersecurity services to protect critical infrastructure from sophisticated cyber threats. Competitive dynamics are intensifying, with established MACs focusing on leveraging their deep industry expertise and established client relationships, while newer entrants are vying for market share through innovative technological offerings and agile service delivery models. Market penetration of advanced automation solutions is expected to deepen, especially in emerging markets and for offshore and complex onshore projects. The drive towards sustainability and reduced carbon footprints is also influencing the adoption of automation technologies that can optimize energy consumption and emissions. The inherent complexities and high stakes of oil and gas operations necessitate reliable, integrated automation, positioning MACs as indispensable partners in ensuring operational integrity and maximizing asset value.

Leading Markets & Segments in Oil & Gas Main Automation Contractor Industry

The Oil & Gas Main Automation Contractor (MAC) industry exhibits distinct leadership across various regions and project segments. Dominantly, the Downstream segment, encompassing refining and petrochemical operations, historically commands a significant portion of the market due to the complexity of processes and the high value of refined products, necessitating advanced automation for precision and safety. However, the Upstream sector, particularly Offshore operations, is also a major contributor, driven by the challenging environments and the critical need for sophisticated automation to ensure efficient extraction and subsea control. The Midstream segment, focusing on transportation and storage, is steadily growing with the expansion of pipelines and LNG infrastructure.

In terms of project size, Large projects (USD 31 million and Above) represent the most substantial market share, as they involve the complete lifecycle automation of entire facilities, from design to commissioning. These large-scale endeavors require extensive expertise and significant capital investment, attracting the most prominent MACs. However, the Small and Medium (USD 5 million to USD 30 million) project segment is experiencing considerable growth, reflecting increased investment in modular facilities, upgrades to existing infrastructure, and specialized automation solutions for smaller field developments.

Key drivers for dominance in these segments include:

- Economic Policies: Government incentives, favorable investment climates, and energy security policies significantly influence capital expenditure in oil and gas projects, thereby driving demand for MAC services. Regions with strong economic growth and a high demand for energy tend to lead in project initiation.

- Infrastructure Development: The presence of extensive existing infrastructure or the planned development of new pipelines, refineries, and offshore platforms directly correlates with the demand for automation services. Countries with ambitious energy infrastructure expansion plans are prime markets.

- Technological Adoption Rates: Regions and companies that are early adopters of advanced automation technologies, such as AI, IIoT, and predictive analytics, will see higher demand for MACs capable of implementing and integrating these solutions.

- Regulatory Environment: Stringent safety and environmental regulations often necessitate advanced automation systems, pushing the adoption of sophisticated MAC solutions to ensure compliance and operational integrity.

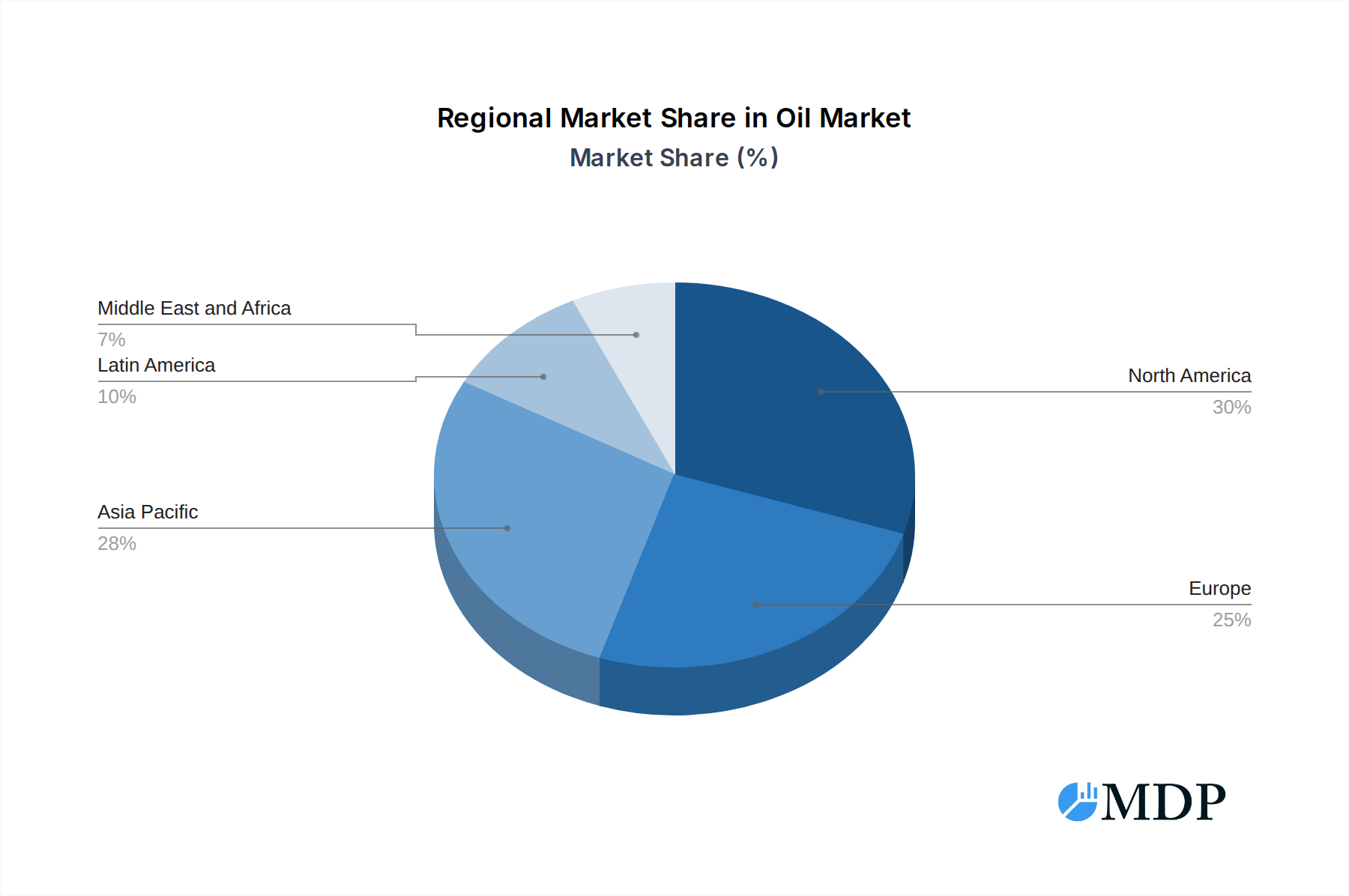

Detailed dominance analysis reveals that North America and the Middle East are leading regions, driven by significant upstream and downstream investments. Asia-Pacific is a rapidly growing market, fueled by increasing energy demand and infrastructure development.

Oil & Gas Main Automation Contractor Industry Product Developments

Product developments in the Oil & Gas Main Automation Contractor (MAC) industry are increasingly focused on intelligent, connected, and data-driven solutions. Innovations include advanced distributed control systems (DCS) with enhanced cybersecurity features, modular automation platforms for faster deployment, and AI-powered analytics for predictive maintenance and process optimization. The integration of IIoT sensors and cloud-based platforms allows for real-time monitoring and remote management of assets, improving operational efficiency and safety. These developments offer competitive advantages by enabling contractors to provide more comprehensive lifecycle management, reduce project execution times, and deliver higher levels of operational reliability and performance for oil and gas clients.

Key Drivers of Oil & Gas Main Automation Contractor Industry Growth

Several key factors are propelling the growth of the Oil & Gas Main Automation Contractor (MAC) industry. Technologically, the ongoing digital transformation and the adoption of Industry 4.0 principles, including AI, IIoT, and big data analytics, are critical. These advancements enable enhanced operational efficiency, predictive maintenance, and remote monitoring, leading to significant cost savings and improved safety. Economically, the demand for energy, coupled with investments in new exploration and production (E&P) projects, as well as the modernization of existing infrastructure, directly fuels the need for sophisticated automation solutions. Regulatory factors, such as increasing safety and environmental compliance standards globally, also drive the adoption of advanced automation technologies to ensure adherence and minimize risks.

Challenges in the Oil & Gas Main Automation Contractor Industry Market

The Oil & Gas Main Automation Contractor (MAC) industry faces several significant challenges. Regulatory hurdles continue to evolve, requiring constant adaptation and compliance with increasingly stringent safety and environmental standards across different jurisdictions. Supply chain issues, exacerbated by global disruptions, can lead to project delays and increased costs for critical components and specialized equipment. Intense competitive pressures from both established players and agile new entrants can impact profit margins and market share. Furthermore, the significant upfront capital investment required for large-scale automation projects can be a barrier for some clients. The skilled labor shortage in specialized automation and cybersecurity fields also presents a continuous challenge for contractors seeking to execute complex projects effectively.

Emerging Opportunities in Oil & Gas Main Automation Contractor Industry

Emerging opportunities in the Oil & Gas Main Automation Contractor (MAC) industry are predominantly driven by the global energy transition and the pursuit of operational excellence. The increasing demand for digital transformation solutions, including AI-driven optimization, IIoT integration, and advanced cybersecurity, presents a significant growth catalyst. Strategic partnerships and collaborations between MACs, technology providers, and energy companies are fostering innovation and enabling the development of integrated, end-to-end solutions. Furthermore, the expansion of renewable energy integration within existing oil and gas infrastructure, and the development of new energy sources, will necessitate specialized automation expertise. Market expansion into emerging economies with growing energy demands also offers substantial long-term growth potential.

Leading Players in the Oil & Gas Main Automation Contractor Industry Sector

- ABB Lt

- Honeywell International Inc

- Emerson Electric Co

- Siemens AG

- Schneider Electric SE

- Rockwell Automation Inc

- Yokogawa Electric Corporation

Key Milestones in Oil & Gas Main Automation Contractor Industry Industry

- June 2022: Honeywell and Anchorage Investments Ltd inked a memorandum of understanding (MoU), paving the way for Honeywell's industrial autonomous technologies to be incorporated into the Anchor Benitoite Petrochemicals Complex in Egypt's Suez Canal Economic Zone. This agreement initiates deliberations to appoint Honeywell Process Solutions (HPS) as the integrated main automation contractor (IMAC) for the facility, highlighting a focus on advanced autonomous solutions and strategic regional partnerships.

- January 2022: Honeywell, a recognized leader in Main Automation Contracts (MAC), established a new state-of-the-art production facility for oil and gas projects in the Kingdom of Saudi Arabia (KSA). This facility, a result of the Elster Instromet Saudi Arabia joint venture with Gas Arabian Services, is designed for advanced manufacturing and assembly of liquid fuel and natural gas solutions, signaling a significant commitment to localized advanced manufacturing and supporting regional project execution.

Strategic Outlook for Oil & Gas Main Automation Contractor Industry Market

The strategic outlook for the Oil & Gas Main Automation Contractor (MAC) industry remains exceptionally strong, driven by the imperative for operational efficiency, safety, and sustainability in the global energy sector. Future growth will be significantly shaped by the continued adoption of digital technologies, including AI, IIoT, and cloud computing, which enhance predictive capabilities and remote operations. Strategic opportunities lie in offering integrated lifecycle automation solutions that address the evolving needs of both traditional oil and gas operations and the emerging energy landscape, such as green hydrogen production and carbon capture. Collaborations with technology providers and a focus on cybersecurity will be crucial for maintaining a competitive edge and securing long-term contracts for complex, large-scale projects across upstream, midstream, and downstream segments.

Oil & Gas Main Automation Contractor Industry Segmentation

-

1. Sector

- 1.1. Upstream (Offshore and Onshore)

- 1.2. Midstream

- 1.3. Downstream

-

2. Project Size

- 2.1. Small and Medium (USD 5 million to USD 30 million)

- 2.2. Large (USD 31 million and Above)

Oil & Gas Main Automation Contractor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Oil & Gas Main Automation Contractor Industry Regional Market Share

Geographic Coverage of Oil & Gas Main Automation Contractor Industry

Oil & Gas Main Automation Contractor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream (Offshore and Onshore)

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Project Size

- 5.2.1. Small and Medium (USD 5 million to USD 30 million)

- 5.2.2. Large (USD 31 million and Above)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Global Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Upstream (Offshore and Onshore)

- 6.1.2. Midstream

- 6.1.3. Downstream

- 6.2. Market Analysis, Insights and Forecast - by Project Size

- 6.2.1. Small and Medium (USD 5 million to USD 30 million)

- 6.2.2. Large (USD 31 million and Above)

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. North America Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 7.1.1. Upstream (Offshore and Onshore)

- 7.1.2. Midstream

- 7.1.3. Downstream

- 7.2. Market Analysis, Insights and Forecast - by Project Size

- 7.2.1. Small and Medium (USD 5 million to USD 30 million)

- 7.2.2. Large (USD 31 million and Above)

- 7.1. Market Analysis, Insights and Forecast - by Sector

- 8. Europe Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 8.1.1. Upstream (Offshore and Onshore)

- 8.1.2. Midstream

- 8.1.3. Downstream

- 8.2. Market Analysis, Insights and Forecast - by Project Size

- 8.2.1. Small and Medium (USD 5 million to USD 30 million)

- 8.2.2. Large (USD 31 million and Above)

- 8.1. Market Analysis, Insights and Forecast - by Sector

- 9. Asia Pacific Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 9.1.1. Upstream (Offshore and Onshore)

- 9.1.2. Midstream

- 9.1.3. Downstream

- 9.2. Market Analysis, Insights and Forecast - by Project Size

- 9.2.1. Small and Medium (USD 5 million to USD 30 million)

- 9.2.2. Large (USD 31 million and Above)

- 9.1. Market Analysis, Insights and Forecast - by Sector

- 10. Latin America Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 10.1.1. Upstream (Offshore and Onshore)

- 10.1.2. Midstream

- 10.1.3. Downstream

- 10.2. Market Analysis, Insights and Forecast - by Project Size

- 10.2.1. Small and Medium (USD 5 million to USD 30 million)

- 10.2.2. Large (USD 31 million and Above)

- 10.1. Market Analysis, Insights and Forecast - by Sector

- 11. Middle East and Africa Oil & Gas Main Automation Contractor Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Sector

- 11.1.1. Upstream (Offshore and Onshore)

- 11.1.2. Midstream

- 11.1.3. Downstream

- 11.2. Market Analysis, Insights and Forecast - by Project Size

- 11.2.1. Small and Medium (USD 5 million to USD 30 million)

- 11.2.2. Large (USD 31 million and Above)

- 11.1. Market Analysis, Insights and Forecast - by Sector

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ABB Lt

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Honeywell International Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Emerson Electric Co

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Siemens AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Schneider Electric SE

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Rockwell Automation Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Yokogawa Electric Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 ABB Lt

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Oil & Gas Main Automation Contractor Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 3: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 4: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 5: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 6: North America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 9: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 10: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 11: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 12: Europe Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 15: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 16: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 17: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 18: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 21: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 22: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 23: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 24: Latin America Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Sector 2025 & 2033

- Figure 27: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Sector 2025 & 2033

- Figure 28: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Project Size 2025 & 2033

- Figure 29: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Project Size 2025 & 2033

- Figure 30: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Oil & Gas Main Automation Contractor Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 2: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 3: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 5: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 6: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 8: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 9: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 11: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 12: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 14: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 15: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Sector 2020 & 2033

- Table 17: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Project Size 2020 & 2033

- Table 18: Global Oil & Gas Main Automation Contractor Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oil & Gas Main Automation Contractor Industry?

The projected CAGR is approximately 6.28%.

2. Which companies are prominent players in the Oil & Gas Main Automation Contractor Industry?

Key companies in the market include ABB Lt, Honeywell International Inc, Emerson Electric Co, Siemens AG, Schneider Electric SE, Rockwell Automation Inc, Yokogawa Electric Corporation.

3. What are the main segments of the Oil & Gas Main Automation Contractor Industry?

The market segments include Sector, Project Size.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.16 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Preference of Oil and Gas Companies for a MAC Approach to Avoid Project Management and Integration Complexities.

6. What are the notable trends driving market growth?

Upstream Segment to Witness Significant Growth.

7. Are there any restraints impacting market growth?

Additional Costs Associated with Machine Safety Systems.

8. Can you provide examples of recent developments in the market?

June 2022: In a significant development, Honeywell and Anchorage Investments Ltd inked a memorandum of understanding (MoU), opening the door for Honeywell's cutting-edge industrial autonomous technologies to be incorporated into the advanced Anchor Benitoite Petrochemicals Complex, located within Egypt's Suez Canal Economic Zone. As per the terms of the MoU, both companies will commence initial deliberations to appoint Honeywell Process Solutions (HPS) as the integrated main automation contractor (IMAC) for the facility.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oil & Gas Main Automation Contractor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oil & Gas Main Automation Contractor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oil & Gas Main Automation Contractor Industry?

To stay informed about further developments, trends, and reports in the Oil & Gas Main Automation Contractor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence