Key Insights

The global market for Titanium Electronic Packaging is poised for significant expansion, projected to reach an estimated $450 million by 2025 and exhibit a robust Compound Annual Growth Rate (CAGR) of 12% through 2033. This impressive trajectory is fueled by the increasing demand for high-performance, durable, and lightweight electronic enclosures across critical industries. The inherent properties of titanium, such as its exceptional strength-to-weight ratio, corrosion resistance, and high-temperature tolerance, make it an indispensable material for applications where reliability and longevity are paramount. Key drivers include the burgeoning defense and aerospace sectors, which require advanced packaging solutions for sensitive electronic components operating in extreme environments. The medical industry also presents a substantial growth avenue, with titanium's biocompatibility making it ideal for implantable medical devices and sophisticated diagnostic equipment. Furthermore, the energy sector's need for resilient packaging in harsh exploration and production settings, alongside the high-bandwidth demands of optical networking, are contributing factors to this market's upward momentum.

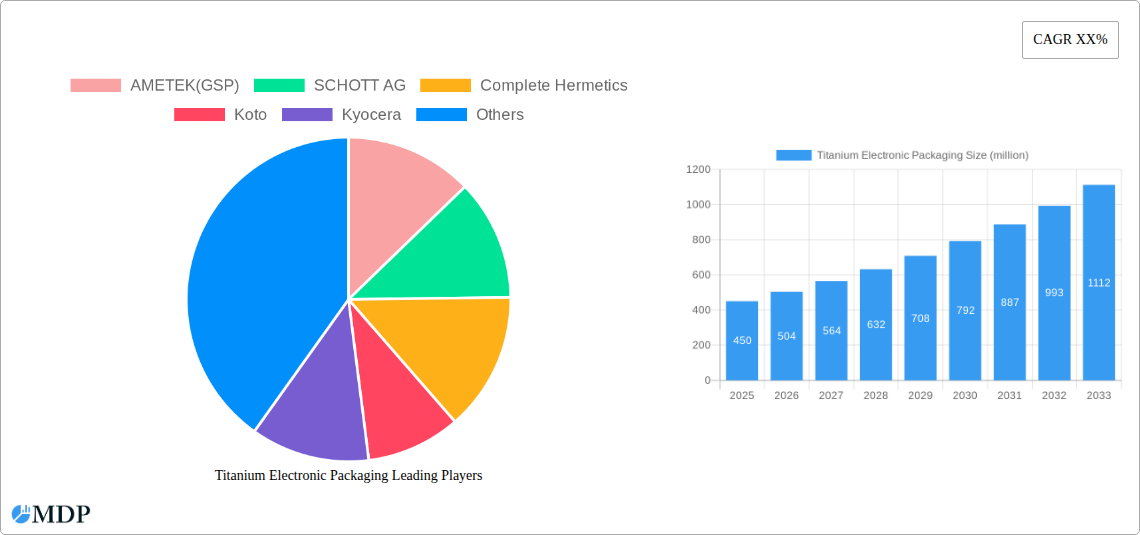

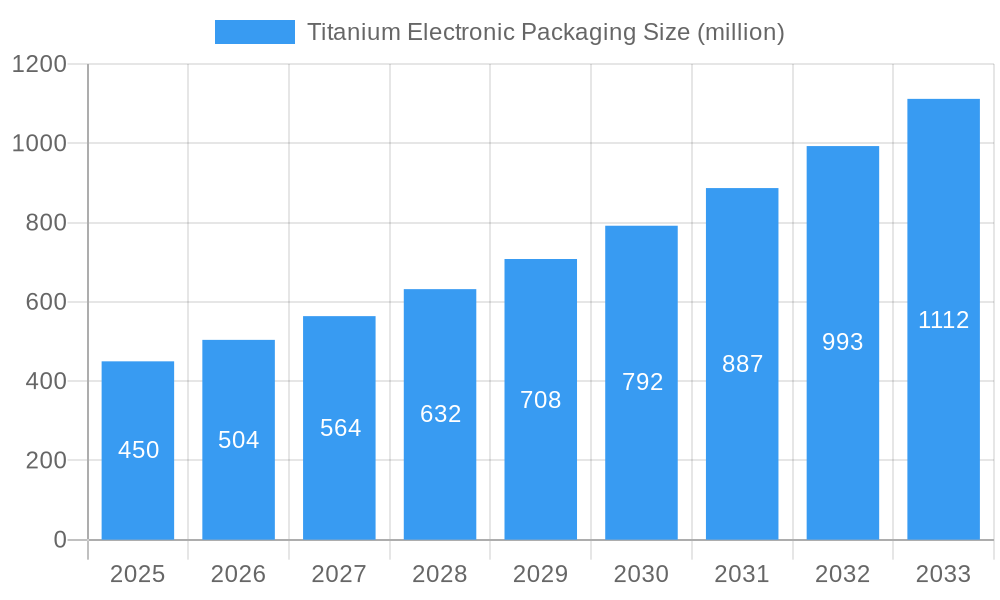

Titanium Electronic Packaging Market Size (In Million)

The market is segmented into Titanium Matrix Composite and Titanium Alloy types, with applications spanning Defense & Aerospace, Medical, Energy, and Optical Networking. While Titanium Alloys currently dominate due to their established manufacturing processes and cost-effectiveness, Titanium Matrix Composites are gaining traction, offering even superior performance characteristics for highly specialized applications. Emerging trends indicate a growing emphasis on miniaturization, enhanced thermal management, and advanced surface treatments for titanium electronic packaging. However, the market faces certain restraints, primarily the higher cost of titanium compared to alternative materials and the complexities associated with its manufacturing and fabrication. Despite these challenges, ongoing technological advancements in processing and an increasing recognition of titanium's long-term value proposition are expected to overcome these hurdles, paving the way for sustained market growth and innovation. Key players like AMETEK (GSP), SCHOTT AG, and Kyocera are actively investing in research and development to meet the evolving needs of this dynamic market.

Titanium Electronic Packaging Company Market Share

This in-depth report offers an unparalleled analysis of the global Titanium Electronic Packaging market, a critical component for high-performance electronic devices across demanding industries. Covering the historical period from 2019 to 2024, the base year of 2025, and a comprehensive forecast period extending to 2033, this report provides actionable insights into market dynamics, industry trends, leading players, and future opportunities. With a projected market size reaching XX million by 2025, the market is poised for significant expansion driven by the inherent advantages of titanium in extreme environments.

Titanium Electronic Packaging Market Dynamics & Concentration

The Titanium Electronic Packaging market exhibits a moderate concentration, with key players investing heavily in R&D to drive innovation. AMETEK (GSP) and SCHOTT AG hold significant market share, estimated at XX% and XX% respectively. Innovation drivers are primarily focused on enhanced thermal management, improved durability, and miniaturization, fueled by advancements in Titanium Matrix Composite materials. Regulatory frameworks, particularly in the Defense & Aerospace and Medical sectors, mandate stringent quality and reliability standards, favoring specialized manufacturers. Product substitutes, such as advanced ceramics and specialized polymers, pose a competitive threat but often fall short in offering titanium's unique combination of strength-to-weight ratio and corrosion resistance. End-user trends indicate a growing demand for robust and lightweight packaging solutions in sectors experiencing rapid technological evolution. Merger and Acquisition (M&A) activities have been strategic, with an estimated XX significant deals recorded in the historical period, aimed at consolidating market presence and acquiring specialized expertise.

- Market Share of Leading Players: AMETEK (GSP) - XX%, SCHOTT AG - XX%, Complete Hermetics - XX%, Koto - XX%, Kyocera - XX%.

- M&A Deal Counts (2019-2024): XX significant transactions.

- Key Innovation Drivers: Enhanced thermal dissipation, miniaturization, superior corrosion resistance, biocompatibility for medical applications.

Titanium Electronic Packaging Industry Trends & Analysis

The global Titanium Electronic Packaging market is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025–2033). This expansion is significantly influenced by the escalating demand from the Defense & Aerospace sector, where the lightweight yet incredibly strong nature of titanium is indispensable for critical components in aircraft, satellites, and defense systems. The Medical industry is another key driver, with titanium packaging offering excellent biocompatibility and resistance to sterilization processes, essential for implantable medical devices and sensitive diagnostic equipment. Market penetration is steadily increasing as more industries recognize the long-term cost-effectiveness and reliability offered by titanium solutions, despite the initial investment. Technological disruptions, such as advanced additive manufacturing (3D printing) of titanium components, are enabling more complex designs and reducing lead times. Consumer preferences, while indirect, are shifting towards more durable and high-performance electronic devices, indirectly boosting the demand for robust packaging materials. Competitive dynamics are characterized by intense R&D efforts, strategic partnerships, and a focus on specialized, high-value applications. The market is projected to reach a value of XX million by 2033.

Leading Markets & Segments in Titanium Electronic Packaging

The Defense & Aerospace segment is the dominant force in the Titanium Electronic Packaging market, accounting for an estimated XX% of the market share in the base year 2025. This dominance is fueled by stringent performance requirements, including extreme temperature tolerance, resistance to vibration and shock, and the critical need for weight reduction in aircraft and spacecraft. Key economic policies supporting defense spending and space exploration initiatives globally act as significant drivers. The United States leads in this segment due to its extensive defense budget and robust aerospace industry, followed closely by Europe and Asia-Pacific nations investing in their defense capabilities.

Within the Types segment, Titanium Alloy packaging holds the largest market share, estimated at XX% in 2025, owing to its established reliability and widespread availability. However, Titanium Matrix Composite is rapidly gaining traction, projected to grow at a CAGR of XX%, driven by its superior strength-to-weight ratio and customized properties for specialized applications.

In terms of Applications, the Medical segment is exhibiting a remarkable growth trajectory, with an estimated CAGR of XX%. This surge is attributed to the increasing prevalence of chronic diseases, the demand for advanced diagnostic imaging, and the development of sophisticated implantable devices, all of which benefit from titanium's biocompatibility and inertness. The global focus on healthcare infrastructure development further bolsters this segment.

- Dominant Application Segment: Defense & Aerospace (XX% market share in 2025).

- Key Drivers: High-performance demands, governmental defense spending, space exploration initiatives.

- Leading Geographies: United States, Europe, China.

- Dominant Type Segment: Titanium Alloy (XX% market share in 2025).

- Key Drivers: Proven reliability, cost-effectiveness for standard applications, established manufacturing processes.

- Fastest-Growing Application Segment: Medical (CAGR of XX%).

- Key Drivers: Biocompatibility, sterilization resistance, miniaturization of medical devices, increasing healthcare expenditure.

- Emerging Type Segment: Titanium Matrix Composite (CAGR of XX%).

- Key Drivers: Superior strength-to-weight ratio, tailored material properties, advanced manufacturing capabilities.

Titanium Electronic Packaging Product Developments

Recent product developments in Titanium Electronic Packaging are centered on enhancing thermal management and improving sealing capabilities for extreme environments. Innovations include advanced laser welding techniques for hermetic sealing, enabling smaller and lighter enclosures. The development of novel Titanium Matrix Composites is offering unprecedented strength and rigidity, crucial for high-vibration applications in aerospace and defense. Furthermore, manufacturers are focusing on developing biocompatible surface treatments for medical packaging, ensuring patient safety and device longevity. These advancements provide competitive advantages by enabling the miniaturization of electronic components and increasing the operational lifespan of devices in harsh conditions.

Key Drivers of Titanium Electronic Packaging Growth

The Titanium Electronic Packaging market is propelled by several key drivers. The relentless pursuit of miniaturization and enhanced performance in electronics, particularly in the defense, aerospace, and medical sectors, necessitates lightweight, durable, and high-performance packaging solutions. The growing demand for advanced medical devices, including implantable sensors and sophisticated diagnostic equipment, relies heavily on titanium's biocompatibility and resistance to corrosion. Furthermore, increasing government investments in defense modernization and space exploration programs globally are directly fueling the demand for titanium electronic packaging. Technological advancements in material science and manufacturing processes, such as additive manufacturing, are making titanium packaging more accessible and cost-effective for a wider range of applications.

Challenges in the Titanium Electronic Packaging Market

Despite its advantages, the Titanium Electronic Packaging market faces several challenges. The inherent cost of raw titanium and the complex manufacturing processes associated with it can lead to higher initial investment compared to alternative materials. Stringent regulatory requirements, especially in the aerospace and medical industries, add to development and qualification costs. Supply chain volatility and the availability of specialized titanium alloys can also pose logistical hurdles. Furthermore, the competitive landscape includes established players and emerging material technologies, requiring continuous innovation and cost optimization to maintain market share. The specialized nature of titanium packaging limits its adoption in lower-end consumer electronics where cost is a primary factor.

Emerging Opportunities in Titanium Electronic Packaging

Emerging opportunities in the Titanium Electronic Packaging market are abundant and driven by technological advancements and expanding applications. The growth of the Internet of Things (IoT) in industrial and defense sectors, requiring ruggedized and long-lasting electronic enclosures, presents a significant opportunity. The increasing demand for high-speed data transmission in optical networking solutions is also creating a niche for titanium packaging due to its electromagnetic shielding properties. Furthermore, advancements in additive manufacturing techniques are enabling the creation of complex, customized titanium electronic packaging solutions for niche applications, reducing lead times and design constraints. Strategic partnerships between material suppliers, packaging manufacturers, and end-users are expected to unlock further innovation and market penetration.

Leading Players in the Titanium Electronic Packaging Sector

- AMETEK (GSP)

- SCHOTT AG

- Complete Hermetics

- Koto

- Kyocera

- SGA Technologies

- Century Seals

- Qingdao KAIRUI Electronics Co.,Ltd.

- Dongchen Electronics

- Taizhou Hangyu Dianqi

- cetc40

- Bojing Electonics

- Beijing Hua Tian Chuang Ye Microelectronics Co.,Ltd.

- CCTC

- Rizhao Xuri Electronic Co.,Ltd.

- Bengbu Xingchuang Electronic Technology Co.,Ltd.

Key Milestones in Titanium Electronic Packaging Industry

- 2019: Increased investment in R&D for lightweight titanium alloys for next-generation aerospace applications.

- 2020: Introduction of advanced laser welding techniques for enhanced hermetic sealing in medical implants.

- 2021: Significant advancements in additive manufacturing (3D printing) of complex titanium electronic packaging designs.

- 2022: Regulatory approvals for new titanium alloys in critical defense systems, expanding market access.

- 2023: Strategic partnerships formed to develop integrated titanium-based electronic solutions for space exploration.

- 2024: Growing adoption of titanium matrix composites for high-temperature applications in energy sector.

Strategic Outlook for Titanium Electronic Packaging Market

The strategic outlook for the Titanium Electronic Packaging market is exceptionally positive, driven by sustained demand from high-growth sectors and ongoing technological advancements. Growth accelerators include the increasing adoption of advanced materials like Titanium Matrix Composites, further miniaturization of electronic components, and the expansion of additive manufacturing capabilities. Strategic opportunities lie in forging deeper collaborations within the value chain to develop bespoke solutions for evolving industry needs, particularly in the defense, aerospace, and medical fields. The market is poised for continued expansion as titanium packaging solidifies its position as the material of choice for critical applications demanding unparalleled reliability and performance.

Titanium Electronic Packaging Segmentation

-

1. Application

- 1.1. Defense & Aerospace

- 1.2. Medical

- 1.3. Energy

- 1.4. Optical Networking

-

2. Types

- 2.1. Titanium Matrix Composite

- 2.2. Titanium Alloy

Titanium Electronic Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

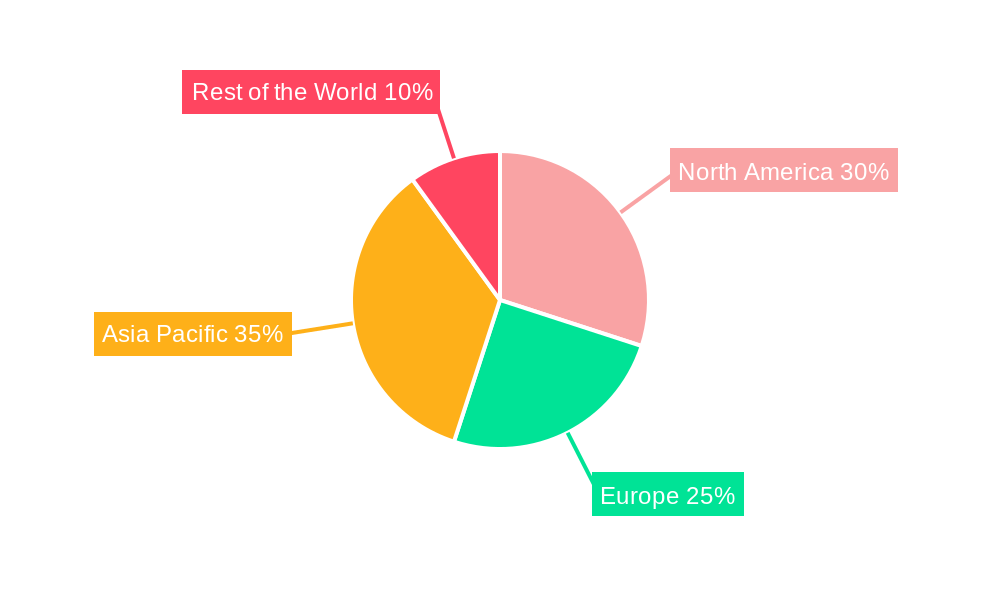

Titanium Electronic Packaging Regional Market Share

Geographic Coverage of Titanium Electronic Packaging

Titanium Electronic Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Titanium Electronic Packaging Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Defense & Aerospace

- 5.1.2. Medical

- 5.1.3. Energy

- 5.1.4. Optical Networking

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Titanium Matrix Composite

- 5.2.2. Titanium Alloy

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Titanium Electronic Packaging Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Defense & Aerospace

- 6.1.2. Medical

- 6.1.3. Energy

- 6.1.4. Optical Networking

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Titanium Matrix Composite

- 6.2.2. Titanium Alloy

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Titanium Electronic Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Defense & Aerospace

- 7.1.2. Medical

- 7.1.3. Energy

- 7.1.4. Optical Networking

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Titanium Matrix Composite

- 7.2.2. Titanium Alloy

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Titanium Electronic Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Defense & Aerospace

- 8.1.2. Medical

- 8.1.3. Energy

- 8.1.4. Optical Networking

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Titanium Matrix Composite

- 8.2.2. Titanium Alloy

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Titanium Electronic Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Defense & Aerospace

- 9.1.2. Medical

- 9.1.3. Energy

- 9.1.4. Optical Networking

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Titanium Matrix Composite

- 9.2.2. Titanium Alloy

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Titanium Electronic Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Defense & Aerospace

- 10.1.2. Medical

- 10.1.3. Energy

- 10.1.4. Optical Networking

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Titanium Matrix Composite

- 10.2.2. Titanium Alloy

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 AMETEK(GSP)

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 SCHOTT AG

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Complete Hermetics

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Koto

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Kyocera

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 SGA Technologies

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Century Seals

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Qingdao KAIRUI Electronics Co.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Ltd.

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Dongchen Electronics

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Taizhou Hangyu Dianqi

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 cetc40

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Bojing Electonics

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Beijing Hua Tian Chuang Ye Microelectronics Co.

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Ltd.

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 CCTC

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Rizhao Xuri Electronic Co.

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Ltd.

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Bengbu Xingchuang Electronic Technology Co.

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Ltd.

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 AMETEK(GSP)

List of Figures

- Figure 1: Global Titanium Electronic Packaging Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Titanium Electronic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Titanium Electronic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Titanium Electronic Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Titanium Electronic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Titanium Electronic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Titanium Electronic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Titanium Electronic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Titanium Electronic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Titanium Electronic Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Titanium Electronic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Titanium Electronic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Titanium Electronic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Titanium Electronic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Titanium Electronic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Titanium Electronic Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Titanium Electronic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Titanium Electronic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Titanium Electronic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Titanium Electronic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Titanium Electronic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Titanium Electronic Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Titanium Electronic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Titanium Electronic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Titanium Electronic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Titanium Electronic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Titanium Electronic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Titanium Electronic Packaging Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Titanium Electronic Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Titanium Electronic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Titanium Electronic Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Titanium Electronic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Titanium Electronic Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Titanium Electronic Packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Titanium Electronic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Titanium Electronic Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Titanium Electronic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Titanium Electronic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Titanium Electronic Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Titanium Electronic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Titanium Electronic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Titanium Electronic Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Titanium Electronic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Titanium Electronic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Titanium Electronic Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Titanium Electronic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Titanium Electronic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Titanium Electronic Packaging Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Titanium Electronic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Titanium Electronic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Titanium Electronic Packaging?

The projected CAGR is approximately 16%.

2. Which companies are prominent players in the Titanium Electronic Packaging?

Key companies in the market include AMETEK(GSP), SCHOTT AG, Complete Hermetics, Koto, Kyocera, SGA Technologies, Century Seals, Qingdao KAIRUI Electronics Co., Ltd., Dongchen Electronics, Taizhou Hangyu Dianqi, cetc40, Bojing Electonics, Beijing Hua Tian Chuang Ye Microelectronics Co., Ltd., CCTC, Rizhao Xuri Electronic Co., Ltd., Bengbu Xingchuang Electronic Technology Co., Ltd..

3. What are the main segments of the Titanium Electronic Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Titanium Electronic Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Titanium Electronic Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Titanium Electronic Packaging?

To stay informed about further developments, trends, and reports in the Titanium Electronic Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence