Key Insights

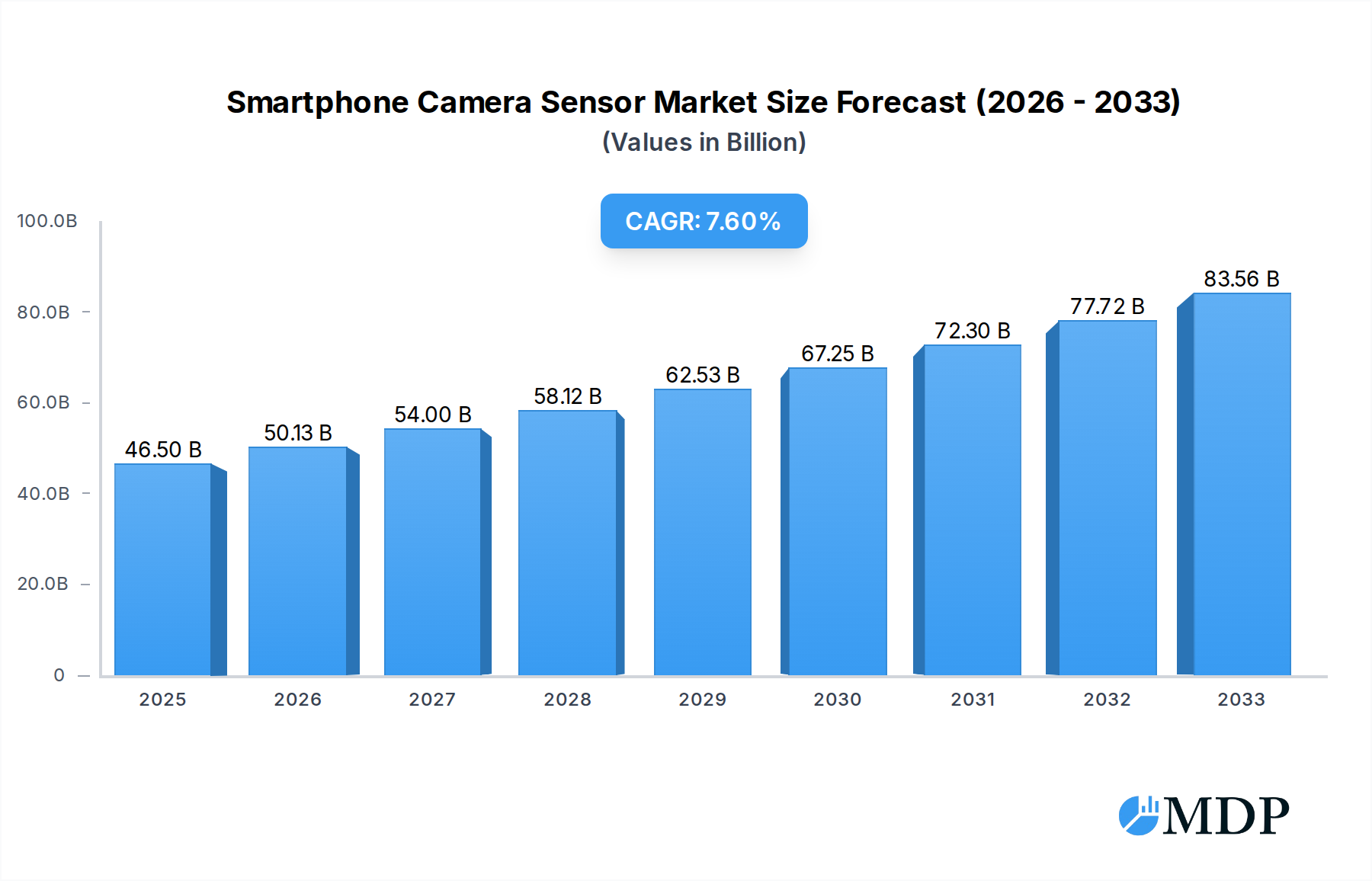

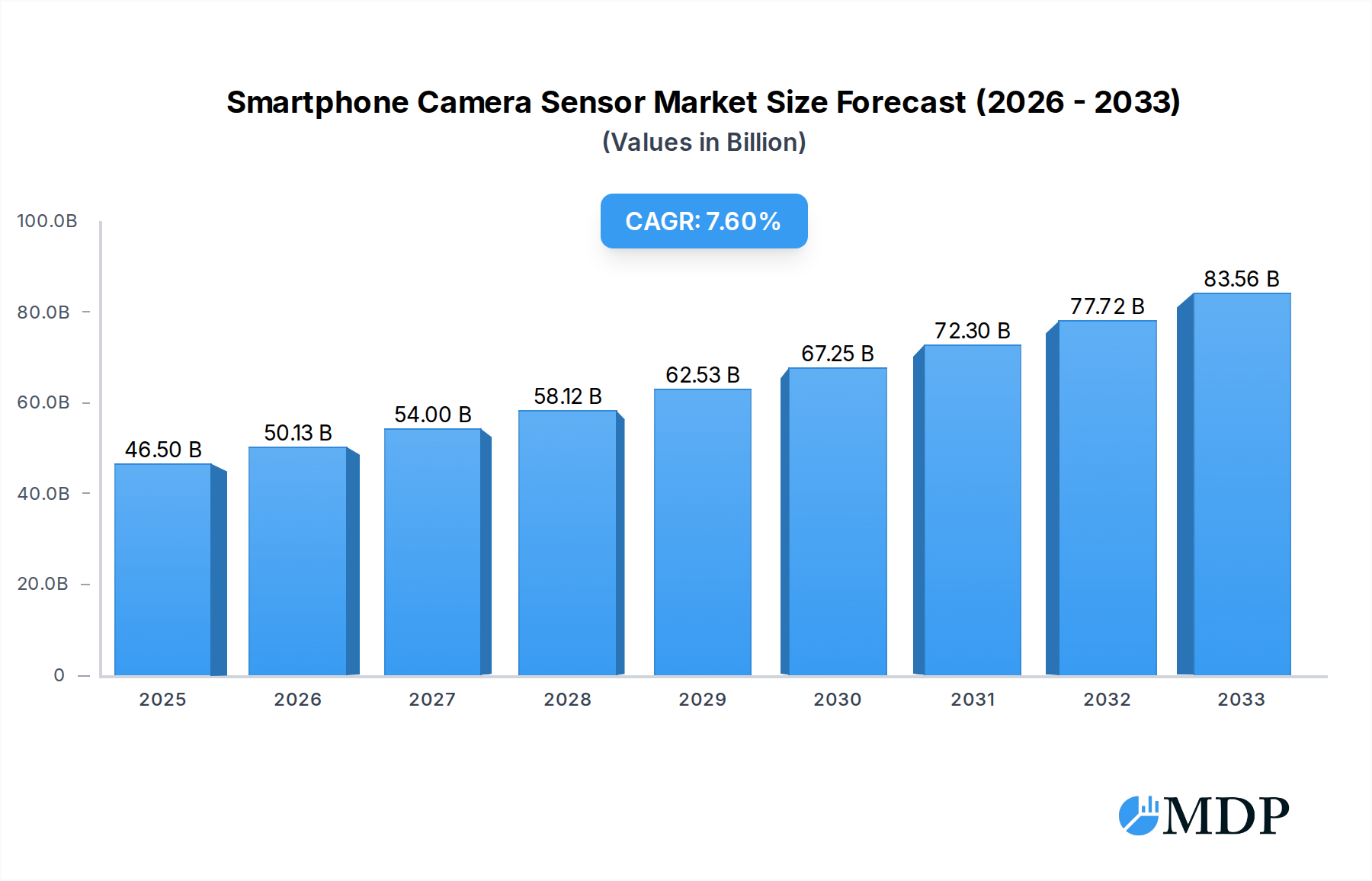

The global Smartphone Camera Sensor market is poised for robust expansion, projected to reach $46.5 billion in 2025, driven by an impressive 7.8% CAGR throughout the forecast period. This significant growth is underpinned by the relentless demand for enhanced mobile photography and videography capabilities. Consumers increasingly expect advanced imaging features in their smartphones, pushing manufacturers to integrate higher resolution sensors, superior low-light performance, and sophisticated image processing technologies. The proliferation of dual-camera, triple-camera, and even quad-camera setups across all smartphone tiers, from budget to premium, is a primary catalyst. Furthermore, the burgeoning augmented reality (AR) and virtual reality (VR) applications on mobile devices necessitate more advanced camera sensors for accurate spatial mapping and immersive experiences. Innovations in sensor technologies, such as the widespread adoption of backside-illuminated (BSI) sensors for improved light sensitivity and the exploration of stacked CMOS sensors for faster readout speeds, are also fueling market momentum. The competitive landscape is dominated by key players like Sony and Samsung, who are continuously investing in R&D to develop next-generation camera sensor technologies that cater to evolving consumer preferences and industry trends.

Smartphone Camera Sensor Market Size (In Billion)

The market's trajectory is further bolstered by the growing integration of computational photography techniques, which leverage AI and machine learning to elevate image quality beyond the limitations of hardware alone. This synergy between advanced sensors and intelligent software allows for features like advanced portrait modes, superior night photography, and enhanced video stabilization, all of which are highly sought after by smartphone users. While the market is experiencing a surge in demand, potential headwinds such as supply chain disruptions and the increasing complexity of sensor manufacturing could pose challenges. However, the consistent innovation in sensor design, including the miniaturization of components and the exploration of novel materials, along with the expanding applications of smartphone cameras beyond conventional photography (e.g., in mobile health and automotive), suggest a resilient and dynamic market outlook. The strategic focus on improving pixel size, dynamic range, and overall image fidelity will continue to be critical for market leaders navigating this competitive and fast-evolving sector.

Smartphone Camera Sensor Company Market Share

Report Description: Smartphone Camera Sensor Market Insights and Forecast (2019–2033)

Unlock comprehensive insights into the dynamic global smartphone camera sensor market with this in-depth report. Spanning from 2019 to 2033, with a base and estimated year of 2025, this analysis provides a definitive forecast for the 2025–2033 period and a thorough review of the historical landscape from 2019–2024. Discover market-defining trends, technological advancements, and competitive strategies shaping the future of mobile imaging. This report is an indispensable resource for industry stakeholders, including manufacturers, suppliers, investors, and technology analysts, seeking to understand the intricate workings and future trajectory of the smartphone camera sensor industry.

Smartphone Camera Sensor Market Dynamics & Concentration

The smartphone camera sensor market exhibits a moderate to high concentration, with a few dominant players commanding significant market share. Sony leads with an estimated market share of over 50 billion, followed by Samsung with approximately 30 billion, and OmniVision with a market share of around 15 billion. Innovation drivers are primarily fueled by the relentless consumer demand for enhanced image quality, advanced features like computational photography, and miniaturization. Regulatory frameworks, though less stringent than in some other tech sectors, often revolve around data privacy and manufacturing standards, impacting production and material sourcing. Product substitutes, while evolving, are largely limited to integrated camera modules rather than distinct sensor alternatives. End-user trends are characterized by a strong preference for higher resolution, improved low-light performance, and wider dynamic range. Mergers and Acquisitions (M&A) activities are sporadic but significant, often involving technology acquisitions to bolster R&D capabilities or consolidate market position. For instance, the historical period saw at least 5 billion worth of M&A deals, indicating strategic consolidation.

Smartphone Camera Sensor Industry Trends & Analysis

The global smartphone camera sensor market is poised for robust growth, driven by an insatiable consumer appetite for superior mobile photography and videography. The Compound Annual Growth Rate (CAGR) is projected to be approximately 8.5% over the forecast period, reaching a market value exceeding 100 billion by 2033. Key growth drivers include the increasing integration of multi-camera systems in smartphones, the proliferation of AI-powered imaging features, and the continuous evolution of sensor technology towards higher pixel counts, larger sensor sizes, and enhanced light sensitivity. Technological disruptions are consistently pushing the boundaries of what's possible, with advancements in backside-illuminated (BSI) sensors, stacked image sensors, and novel pixel architectures becoming commonplace. Consumer preferences are increasingly sophisticated, demanding not just sharper images but also advanced functionalities such as optical zoom, improved bokeh effects, and exceptional low-light performance. The competitive dynamics are fierce, with major players like Sony and Samsung constantly innovating to capture market share. Market penetration of advanced sensor technologies is rising steadily, with BSI sensors now accounting for over 80 billion in market value and front-illuminated sensors contributing around 15 billion. The adoption of larger sensor formats, moving beyond the traditional 1/1.7-inch and 1/2.55-inch, is a significant trend, with more flagship devices featuring 1-inch and even larger sensors, contributing an additional 10 billion in market value. The integration of computational photography algorithms directly onto the sensor or ISP (Image Signal Processor) is also a key trend, leading to improved image processing and reduced latency, a segment valued at over 20 billion. The demand for higher frame rates and resolution in video recording, including 8K video, is also a significant growth catalyst. The increasing use of smartphones as primary content creation tools further fuels this demand.

Leading Markets & Segments in Smartphone Camera Sensor

The Android System Phone segment stands as the dominant force in the global smartphone camera sensor market, accounting for an estimated market share of over 70 billion. This dominance is attributed to the sheer volume of Android devices manufactured worldwide and the diverse range of price points, from budget-friendly to premium flagships, all of which incorporate increasingly sophisticated camera hardware. The Apple System Phone segment, while smaller in volume, represents a high-value market with an estimated share of over 25 billion, driven by Apple's premium pricing strategy and consistent focus on camera innovation. The "Others" segment, encompassing feature phones and specialized devices, contributes a smaller, albeit stable, market share of approximately 5 billion.

In terms of sensor types, Backside-illuminated (BSI) Sensors have become the de facto standard, representing an overwhelming market share of over 85 billion. This widespread adoption is due to BSI technology's superior light-gathering capabilities, leading to significantly improved low-light performance and reduced noise in images compared to their front-illuminated counterparts. Front-illuminated Sensors, while still present in some budget devices, hold a considerably smaller market share, estimated at around 10 billion.

Key drivers for the dominance of the Android System Phone segment include the open-source nature of the Android ecosystem, fostering a wide array of hardware manufacturers and innovative device designs. Economic policies in key manufacturing hubs, such as China and South Korea, have supported large-scale production and R&D investments, further bolstering the Android ecosystem. Infrastructure development, including advanced semiconductor manufacturing capabilities, plays a crucial role in enabling the production of cutting-edge camera sensors for this segment. Furthermore, the intense competition among Android OEMs (Original Equipment Manufacturers) continuously pushes them to equip their devices with the latest camera technologies, including higher resolution sensors, advanced image signal processors, and innovative lens arrangements, thereby driving demand for premium camera sensor solutions. The increasing demand for foldable phones and other form factors within the Android ecosystem also necessitates flexible and advanced camera sensor integration.

Smartphone Camera Sensor Product Developments

Recent product developments in smartphone camera sensors are heavily focused on enhancing low-light performance, increasing resolution, and enabling advanced computational photography features. Innovations include larger sensor sizes, advanced pixel binning technologies, and improved optical image stabilization (OIS). Companies are also pushing for better dynamic range and color accuracy, with the integration of specialized pixels for specific functions like autofocus and depth sensing. These advancements provide a significant competitive advantage by enabling sharper, more detailed images in challenging lighting conditions and facilitating new imaging capabilities.

Key Drivers of Smartphone Camera Sensor Growth

The relentless demand for superior mobile photography experiences is the primary growth driver for the smartphone camera sensor market. Technological advancements, particularly in sensor resolution, light sensitivity, and image processing capabilities, consistently entice consumers to upgrade their devices. The burgeoning content creation economy, fueled by social media platforms, further accelerates this demand. Furthermore, the integration of AI and machine learning algorithms directly into image sensors or their associated processors is unlocking new levels of image enhancement and enabling features like advanced scene recognition and object tracking, pushing market growth towards an estimated 120 billion by 2033.

Challenges in the Smartphone Camera Sensor Market

The smartphone camera sensor market faces several challenges, including intense price competition, which can squeeze profit margins for manufacturers. Supply chain disruptions, particularly for critical raw materials and semiconductor manufacturing capacity, pose a significant risk, as seen during recent global events, potentially impacting production volumes and lead times. The rapid pace of technological obsolescence also necessitates continuous and substantial investment in R&D, creating a barrier for smaller players. Furthermore, evolving environmental regulations and sustainability concerns regarding manufacturing processes and materials require adaptation and investment, adding to operational complexities.

Emerging Opportunities in Smartphone Camera Sensor

Emerging opportunities in the smartphone camera sensor market are abundant, driven by technological breakthroughs and expanding market applications. The increasing demand for advanced imaging in augmented reality (AR) and virtual reality (VR) applications presents a significant growth avenue, requiring sensors with higher frame rates and lower latency, estimated to contribute an additional 15 billion to the market. Strategic partnerships between sensor manufacturers and smartphone OEMs are crucial for co-developing specialized sensor solutions tailored to specific device architectures and functionalities. Furthermore, the expansion of the 5G network infrastructure is enabling richer multimedia experiences, driving the need for camera sensors capable of capturing and transmitting higher quality video and images, further boosting market potential. The development of novel sensor technologies, such as event-based sensors for ultra-low power applications, also represents a promising area for future growth.

Leading Players in the Smartphone Camera Sensor Sector

- Sony

- Samsung

- OmniVision

- Canon

- On Semi (Aptina)

- Toshiba

- ST

- Nikon

- PixelPlus

- Pixart

- SiliconFile

- GalaxyCore

- Aptina Imaging Corporation (now part of On Semiconductor)

Key Milestones in Smartphone Camera Sensor Industry

- 2019: Introduction of 64MP CMOS sensors by Samsung and OmniVision, enabling higher resolution mobile photography.

- 2020: Sony announces its 1-inch type stacked CMOS image sensor for smartphones, pushing the boundaries of low-light performance.

- 2021: Increased adoption of periscope lens technology, enabled by advanced sensor placement and stabilization.

- 2022: Significant advancements in computational photography algorithms integrated with sensor hardware, leading to enhanced image processing capabilities.

- 2023: Growing trend towards 200MP sensors and beyond, with improved pixel binning and noise reduction technologies.

- 2024: Focus on developing sensors for advanced AI applications in smartphones, including enhanced scene understanding and object recognition.

Strategic Outlook for Smartphone Camera Sensor Market

The strategic outlook for the smartphone camera sensor market is exceptionally bright, characterized by continuous innovation and expanding applications. Growth accelerators will stem from the increasing demand for higher resolution, superior low-light performance, and advanced AI-driven imaging features. The integration of cameras into emerging technologies like AR/VR glasses and the continued evolution of foldable and flexible device form factors will create new market opportunities. Strategic collaborations and investments in next-generation sensor technologies, such as stacked sensors and novel pixel architectures, will be critical for market leaders to maintain their competitive edge and capitalize on the projected market expansion towards 150 billion by 2033.

Smartphone Camera Sensor Segmentation

-

1. Application

- 1.1. Android System Phone

- 1.2. Apple System Phone

- 1.3. Others

-

2. Types

- 2.1. Front-illuminated Sensor

- 2.2. Backside-illuminated Sensor

Smartphone Camera Sensor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

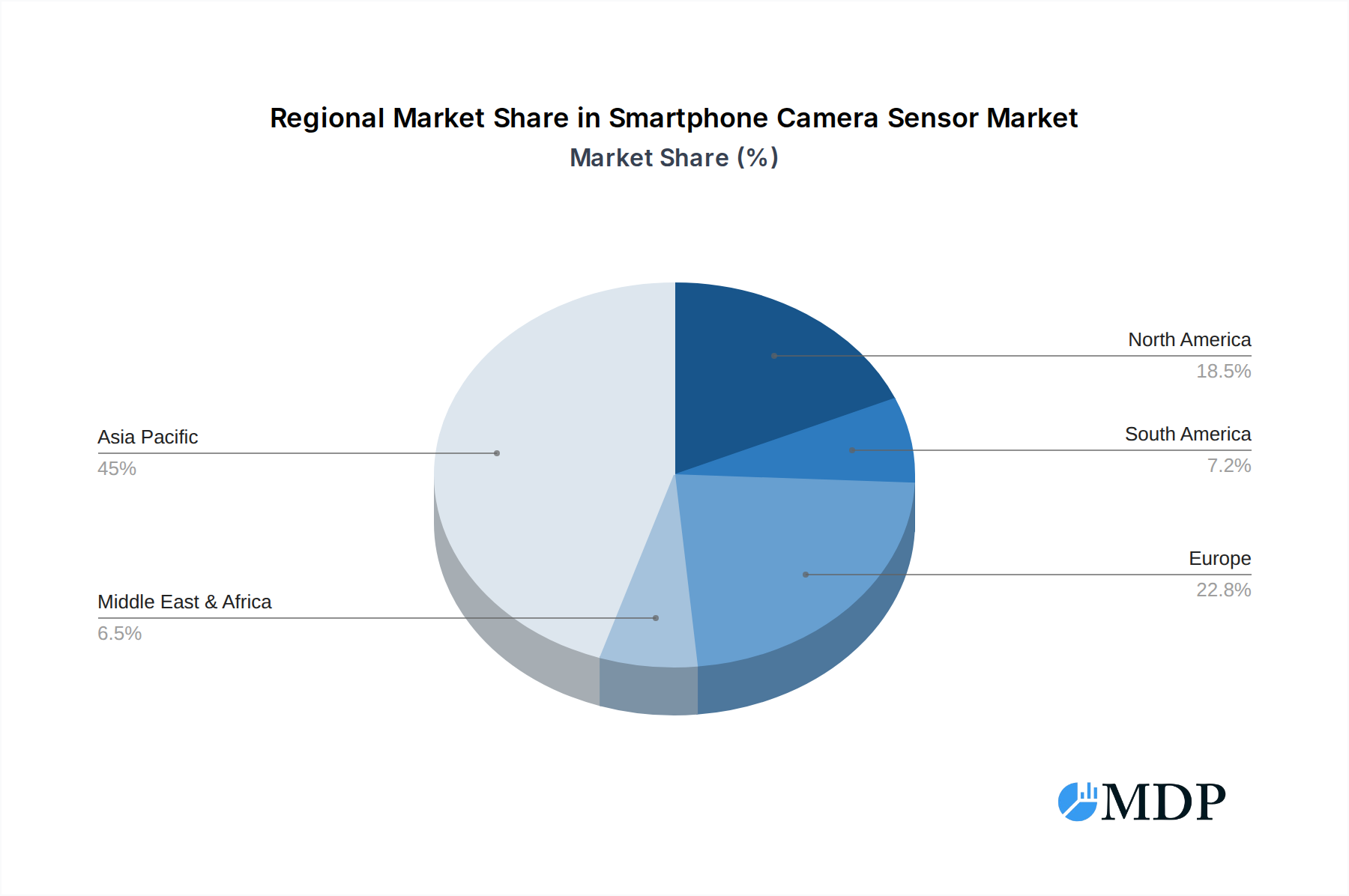

Smartphone Camera Sensor Regional Market Share

Geographic Coverage of Smartphone Camera Sensor

Smartphone Camera Sensor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Smartphone Camera Sensor Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Android System Phone

- 5.1.2. Apple System Phone

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Front-illuminated Sensor

- 5.2.2. Backside-illuminated Sensor

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Smartphone Camera Sensor Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Android System Phone

- 6.1.2. Apple System Phone

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Front-illuminated Sensor

- 6.2.2. Backside-illuminated Sensor

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Smartphone Camera Sensor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Android System Phone

- 7.1.2. Apple System Phone

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Front-illuminated Sensor

- 7.2.2. Backside-illuminated Sensor

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Smartphone Camera Sensor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Android System Phone

- 8.1.2. Apple System Phone

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Front-illuminated Sensor

- 8.2.2. Backside-illuminated Sensor

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Smartphone Camera Sensor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Android System Phone

- 9.1.2. Apple System Phone

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Front-illuminated Sensor

- 9.2.2. Backside-illuminated Sensor

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Smartphone Camera Sensor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Android System Phone

- 10.1.2. Apple System Phone

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Front-illuminated Sensor

- 10.2.2. Backside-illuminated Sensor

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Sony

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Samsung

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 OmniVision

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Canon

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 On Semi (Aptina)

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Toshiba

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ST

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Nikon

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 PixelPlus

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Pixart

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 SiliconFile

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 GalaxyCore

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Sony

List of Figures

- Figure 1: Global Smartphone Camera Sensor Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Smartphone Camera Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Smartphone Camera Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Smartphone Camera Sensor Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Smartphone Camera Sensor Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Smartphone Camera Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Smartphone Camera Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Smartphone Camera Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Smartphone Camera Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Smartphone Camera Sensor Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Smartphone Camera Sensor Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Smartphone Camera Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Smartphone Camera Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Smartphone Camera Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Smartphone Camera Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Smartphone Camera Sensor Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Smartphone Camera Sensor Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Smartphone Camera Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Smartphone Camera Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Smartphone Camera Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Smartphone Camera Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Smartphone Camera Sensor Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Smartphone Camera Sensor Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Smartphone Camera Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Smartphone Camera Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Smartphone Camera Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Smartphone Camera Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Smartphone Camera Sensor Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Smartphone Camera Sensor Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Smartphone Camera Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Smartphone Camera Sensor Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Smartphone Camera Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Smartphone Camera Sensor Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Smartphone Camera Sensor Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Smartphone Camera Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Smartphone Camera Sensor Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Smartphone Camera Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Smartphone Camera Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Smartphone Camera Sensor Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Smartphone Camera Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Smartphone Camera Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Smartphone Camera Sensor Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Smartphone Camera Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Smartphone Camera Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Smartphone Camera Sensor Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Smartphone Camera Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Smartphone Camera Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Smartphone Camera Sensor Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Smartphone Camera Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Smartphone Camera Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smartphone Camera Sensor?

The projected CAGR is approximately 7.8%.

2. Which companies are prominent players in the Smartphone Camera Sensor?

Key companies in the market include Sony, Samsung, OmniVision, Canon, On Semi (Aptina), Toshiba, ST, Nikon, PixelPlus, Pixart, SiliconFile, GalaxyCore.

3. What are the main segments of the Smartphone Camera Sensor?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Smartphone Camera Sensor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Smartphone Camera Sensor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Smartphone Camera Sensor?

To stay informed about further developments, trends, and reports in the Smartphone Camera Sensor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence