Key Insights

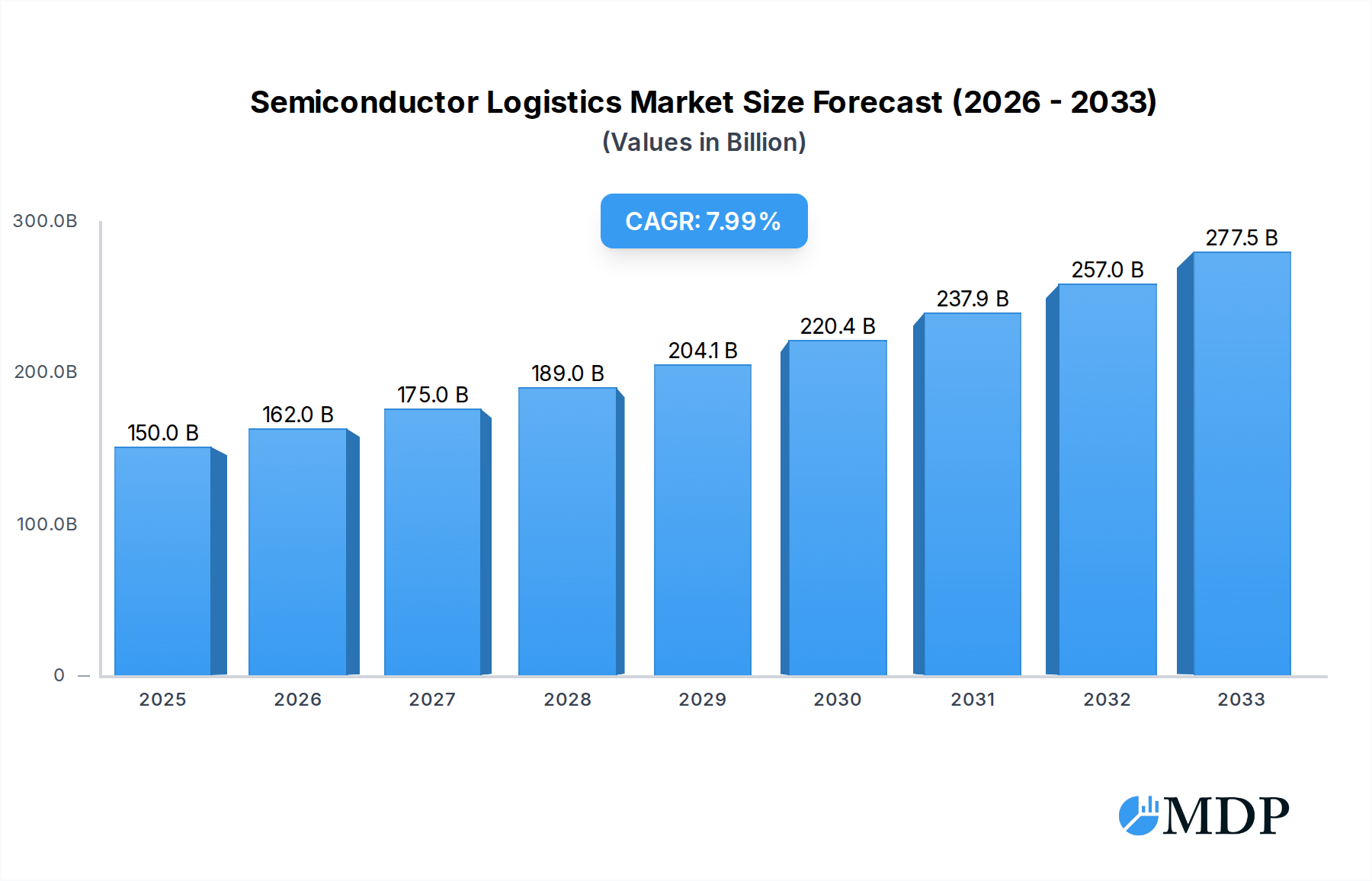

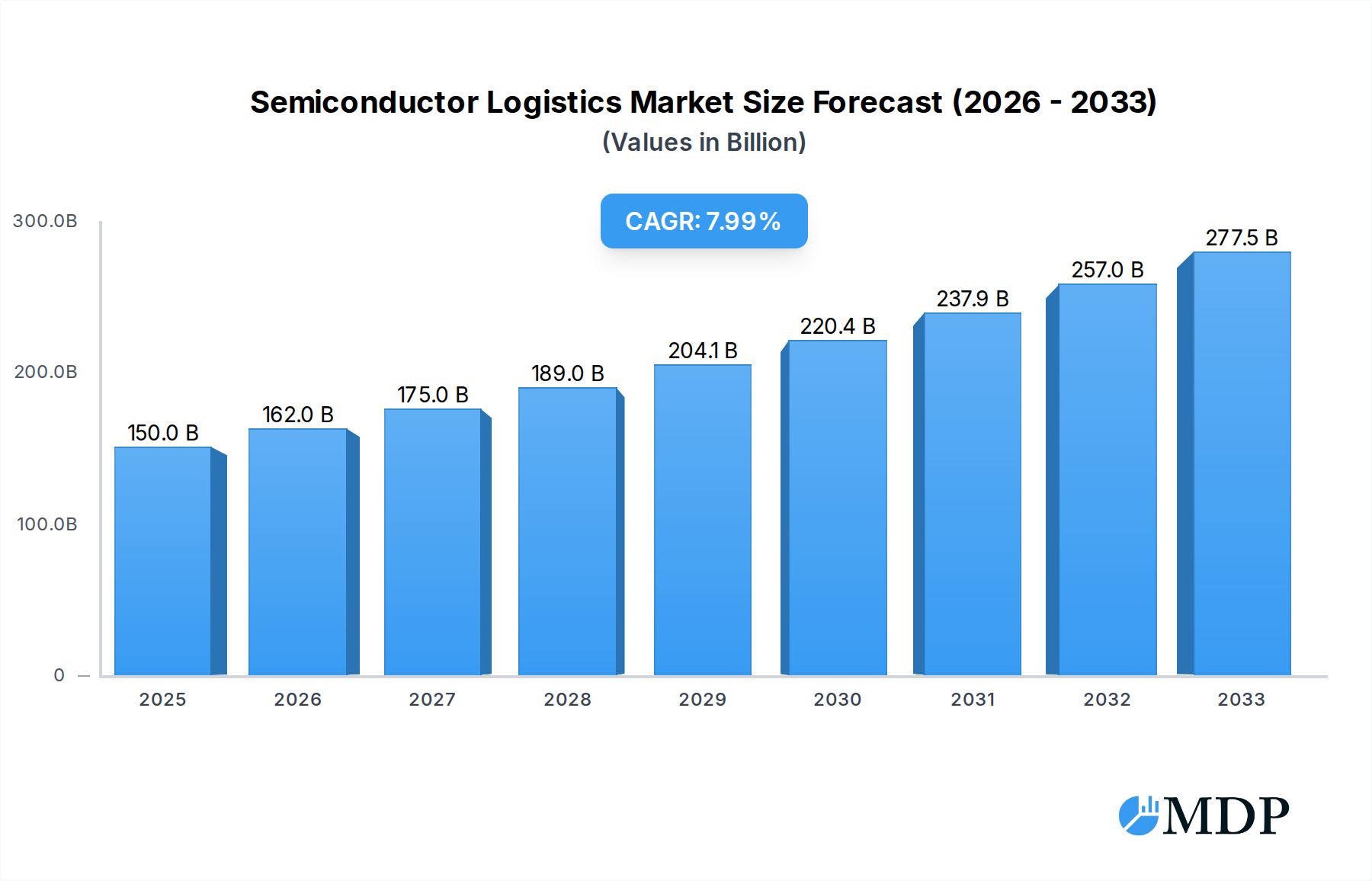

The global Semiconductor Logistics market is poised for significant expansion, with a projected market size of $150 billion in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 8% during the forecast period of 2025-2033. This upward trajectory is primarily driven by the escalating demand for semiconductors across a multitude of industries, including consumer electronics, automotive, telecommunications, and industrial automation. The increasing complexity and value of semiconductor components necessitate specialized logistics solutions, further fueling market expansion. Innovations in supply chain management, such as advanced tracking systems, temperature-controlled warehousing, and optimized transportation routes, are crucial for mitigating risks and ensuring the integrity of these sensitive products. The market is segmented by application into intrinsic and extrinsic semiconductors, and by transport type into sea, land, and air transport. The inherent fragility and high value of semiconductors strongly favor air transport for time-sensitive and high-value shipments, while sea and land transport cater to bulk movements and less time-critical components, demonstrating a strategic allocation of resources based on product characteristics and delivery timelines.

Semiconductor Logistics Market Size (In Billion)

The market landscape is characterized by intense competition among key players like DHL, Nippon Express, Kuehne + Nagel, and DB Schenker, who are continually investing in technology and infrastructure to enhance their service offerings. Emerging trends such as the rise of smart logistics, powered by IoT and AI, are revolutionizing how semiconductors are transported and managed, promising greater efficiency and reduced lead times. Furthermore, the growing emphasis on supply chain resilience, exacerbated by recent global disruptions, is driving greater collaboration and innovation among logistics providers to create more robust and agile networks. While growth is strong, challenges remain, including the high cost of specialized logistics, stringent regulatory requirements for handling sensitive materials, and the potential for geopolitical instability to disrupt global supply chains. Addressing these restraints through strategic partnerships, technological advancements, and proactive risk management will be critical for sustained success within this dynamic market.

Semiconductor Logistics Company Market Share

Semiconductor Logistics: Navigating a Billion-Dollar Industry's Future

This comprehensive report dives deep into the Semiconductor Logistics market, a critical and rapidly evolving sector underpinning global technology. With a study period spanning from 2019 to 2033, this analysis provides unparalleled insights into market dynamics, key trends, leading players, and future opportunities within this billion-dollar industry. Examining historical data from 2019-2024, a base year of 2025, and projecting growth through 2033, this report is an indispensable resource for any stakeholder looking to understand and capitalize on the semiconductor supply chain.

Semiconductor Logistics Market Dynamics & Concentration

The Semiconductor Logistics market is characterized by a moderate to high concentration, with a few key players dominating the global landscape. In the historical period (2019-2024), the market witnessed significant consolidation, with an estimated 15 M&A deals valued at over $5 billion in total. Innovation drivers are primarily fueled by the increasing complexity of semiconductor products, demanding specialized handling, temperature control, and anti-static measures. Regulatory frameworks, while crucial for ensuring compliance and security, can also present challenges, particularly across international borders. Product substitutes are limited, given the unique requirements of semiconductor transport, but advancements in packaging technology are gradually reducing some dependencies. End-user trends indicate a growing demand for just-in-time delivery and reduced lead times, pushing logistics providers to optimize their networks. Companies like DHL, Nippon Express, and Kuehne + Nagel hold substantial market shares, estimated to be over 20% combined, reflecting their established infrastructure and specialized capabilities.

- Market Share Snapshot (Estimated):

- DHL: ~8%

- Nippon Express: ~7%

- Kuehne + Nagel: ~6%

- Omni Logistics: ~4%

- DB Schenker: ~3%

- DSV: ~3%

- Yusen Logistics: ~2%

- MOL Logistics: ~1.5%

- Schnellecke: ~1%

- Hey Primo: <1%

- M&A Activity Drivers: Increased demand for specialized services, geographic expansion, and acquisition of technological capabilities.

Semiconductor Logistics Industry Trends & Analysis

The Semiconductor Logistics industry is poised for substantial growth, driven by several interconnected factors. The market is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 9.5% during the forecast period (2025-2033), reaching an estimated market value of over $150 billion. This growth is underpinned by the relentless demand for semiconductors across various applications, from consumer electronics and automotive to advanced computing and artificial intelligence. Technological disruptions, such as the adoption of IoT in warehousing, AI-powered route optimization, and advanced tracking solutions, are transforming operational efficiency and visibility. Consumer preferences are increasingly leaning towards faster delivery times and greater transparency throughout the supply chain. Competitive dynamics are intensifying, with established players investing heavily in technology and specialized infrastructure to meet the stringent demands of semiconductor manufacturers. Market penetration of advanced logistics solutions is expected to reach over 60% by the end of the forecast period.

The increasing reliance on advanced semiconductors for next-generation technologies like 5G, AI, and the Internet of Things (IoT) is a primary growth engine. The automotive industry's shift towards electric and autonomous vehicles, both heavily reliant on sophisticated chipsets, further amplifies this demand. Furthermore, the burgeoning market for high-performance computing and data centers necessitates a robust and efficient supply chain to support the rapid deployment of these critical components. Geopolitical factors and the drive for supply chain resilience are also influencing logistics strategies, with a growing emphasis on diversification and regionalization of manufacturing and logistics hubs. The development of smaller, more complex, and fragile semiconductor components demands specialized handling and packaging, pushing logistics providers to invest in state-of-the-art facilities and trained personnel. The evolving nature of semiconductor manufacturing processes, including the miniaturization and increased sensitivity of wafers, requires precise environmental controls throughout the transportation process, from origin to final destination. This includes maintaining specific temperature and humidity levels, as well as mitigating risks associated with vibration and electrostatic discharge (ESD). The industry is also witnessing a rise in demand for end-to-end logistics solutions, encompassing warehousing, inventory management, freight forwarding, and last-mile delivery, all tailored to the unique needs of the semiconductor sector. The growing adoption of digital technologies, including blockchain for enhanced traceability and security, and predictive analytics for demand forecasting and risk management, is further revolutionizing the operational landscape of semiconductor logistics.

Leading Markets & Segments in Semiconductor Logistics

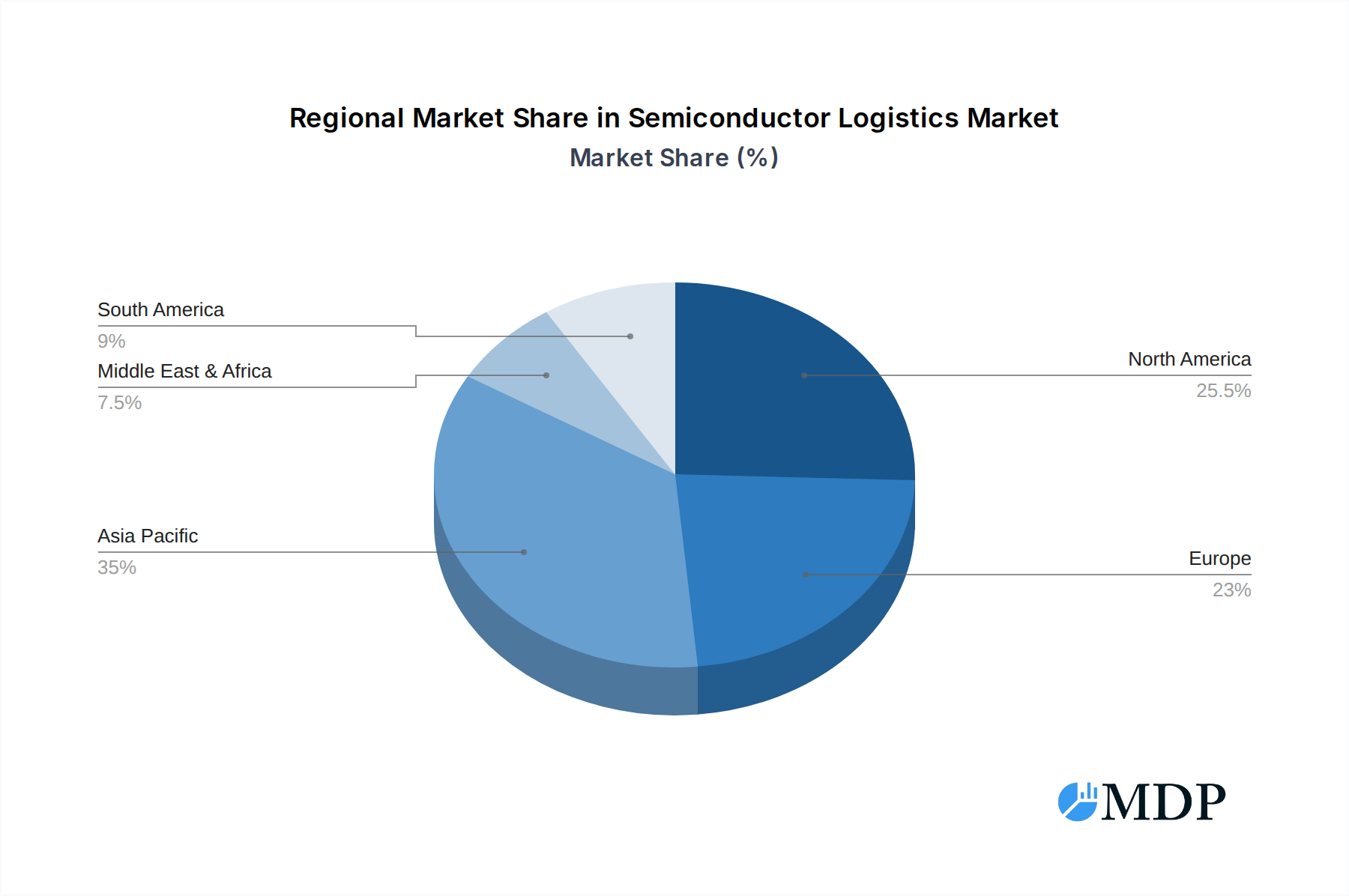

The Semiconductor Logistics market exhibits distinct regional strengths and segment dominance. Asia-Pacific remains the dominant region, driven by its significant concentration of semiconductor manufacturing facilities and end-user markets. China, Taiwan, South Korea, and Japan are pivotal hubs, contributing an estimated 45% to the global logistics market value within this sector.

Application Segment Dominance:

- Intrinsic Semiconductor: This segment, encompassing raw wafers, dies, and bare components, represents a substantial portion of the market due to its foundational role in all semiconductor production. The demand for highly controlled environments and specialized handling for these sensitive materials drives significant logistics investment.

- Key Drivers: Manufacturing hubs in Asia-Pacific, rigorous quality control requirements, and the need for specialized cleanroom logistics.

- Extrinsic Semiconductor: This segment includes packaged chips, integrated circuits, and finished semiconductor devices. Its growth is directly tied to the booming consumer electronics, automotive, and telecommunications sectors.

- Key Drivers: High volume demand from global electronics manufacturers, growth in emerging markets, and the increasing complexity of end-user devices.

Type Segment Dominance:

- Sea Transport: While generally slower, sea transport remains a cost-effective option for bulk shipments of less time-sensitive components and finished goods, particularly for intercontinental trade. Its dominance is observed in the movement of lower-value components and raw materials.

- Key Drivers: Cost-efficiency for large volumes, established global shipping routes, and its role in connecting major manufacturing hubs.

- Land Transport: Crucial for regional distribution and last-mile delivery, land transport, including road and rail, offers flexibility and speed for moving finished goods to assembly plants and distribution centers.

- Key Drivers: Facilitating just-in-time deliveries, connecting inland manufacturing sites to ports, and supporting regional supply chain integration.

- Air Transport: Indispensable for high-value, time-sensitive shipments of critical components, prototypes, and finished products, air transport commands a significant share of the market, especially for urgent deliveries and during supply chain disruptions.

- Key Drivers: Speed and reliability for critical shipments, global network of airports, and its role in mitigating production downtime.

Economic policies in key manufacturing nations, such as government incentives for semiconductor production and trade agreements, significantly influence regional dominance. Infrastructure development, including specialized logistics facilities, advanced warehousing, and efficient transportation networks, further solidifies the leadership of certain regions and countries within the Semiconductor Logistics market.

Semiconductor Logistics Product Developments

Recent product developments in Semiconductor Logistics focus on enhancing efficiency, security, and traceability. Innovations in smart packaging, incorporating real-time temperature and humidity monitoring, are gaining traction. Advanced tracking solutions, utilizing IoT and blockchain technology, provide unprecedented visibility into the supply chain, mitigating risks of tampering and loss. Specialized containers designed for anti-static and vibration dampening are becoming standard for high-value chip transportation. These developments offer competitive advantages by ensuring product integrity, reducing damage claims, and meeting the stringent quality requirements of semiconductor manufacturers.

Key Drivers of Semiconductor Logistics Growth

The Semiconductor Logistics market is propelled by several interconnected growth drivers. The relentless surge in demand for semiconductors across diverse industries, including automotive, consumer electronics, AI, and 5G infrastructure, is a primary catalyst. Technological advancements, such as miniaturization and increased complexity of chips, necessitate specialized handling and sophisticated logistics. Government initiatives and subsidies aimed at boosting domestic semiconductor manufacturing and supply chain resilience are also significant growth accelerators. Furthermore, the increasing emphasis on just-in-time delivery and reduced lead times by end-users compels logistics providers to optimize their networks for speed and efficiency.

Challenges in the Semiconductor Logistics Market

Despite robust growth, the Semiconductor Logistics market faces notable challenges. The inherent fragility and high value of semiconductor products make them susceptible to damage, requiring specialized handling and stringent environmental controls, increasing operational costs. Geopolitical tensions and trade disputes can disrupt global supply chains, leading to delays and increased shipping costs. Regulatory hurdles and customs complexities, particularly for cross-border shipments of sensitive materials, can create significant bottlenecks. Intense competition and the need for continuous investment in advanced technologies also pressure profit margins for logistics providers.

Emerging Opportunities in Semiconductor Logistics

Emerging opportunities within the Semiconductor Logistics market are centered around technological integration and strategic partnerships. The widespread adoption of AI and machine learning for predictive analytics in demand forecasting and route optimization presents significant potential for cost savings and improved efficiency. The development of specialized, temperature-controlled and ESD-protected warehousing facilities in emerging semiconductor manufacturing hubs offers substantial growth prospects. Furthermore, strategic collaborations between semiconductor manufacturers and logistics providers, focusing on end-to-end supply chain solutions and risk management, are poised to drive long-term success and market expansion.

Leading Players in the Semiconductor Logistics Sector

The Semiconductor Logistics sector is populated by a network of highly specialized and globally recognized logistics providers. These companies offer tailored solutions to meet the unique demands of the semiconductor supply chain.

- DHL

- Omni Logistics

- Nippon Express

- Kuehne + Nagel

- Yusen Logistics

- DB Schenker

- DSV

- Hey Primo

- MOL Logistics

- Schnellecke

Key Milestones in Semiconductor Logistics Industry

- 2019: Increased adoption of IoT for real-time shipment tracking and condition monitoring.

- 2020: Heightened focus on supply chain resilience due to global disruptions, leading to diversification strategies.

- 2021: Significant investments in specialized, temperature-controlled warehousing to meet growing demand for sensitive components.

- 2022: Growing interest in AI-powered logistics solutions for route optimization and demand forecasting.

- 2023: Expansion of specialized air freight services to accommodate urgent deliveries of high-value semiconductor components.

- 2024: Increased collaboration between logistics providers and semiconductor manufacturers to optimize end-to-end supply chains.

Strategic Outlook for Semiconductor Logistics Market

The Semiconductor Logistics market is positioned for sustained growth, driven by increasing demand for advanced technologies and the ongoing expansion of global semiconductor manufacturing. Strategic opportunities lie in the continued adoption of digital technologies, such as AI and blockchain, to enhance visibility and efficiency. Investments in specialized infrastructure, particularly in emerging manufacturing regions, and the development of end-to-end, integrated logistics solutions will be crucial for capturing market share. Collaborations and partnerships will be key to navigating complex supply chains and ensuring resilience in the face of evolving global dynamics.

Semiconductor Logistics Segmentation

-

1. Application

- 1.1. Intrinsic Semiconductor

- 1.2. Extrinsic Semiconductor

-

2. Types

- 2.1. Sea Transport

- 2.2. Land Transport

- 2.3. Air Transport

Semiconductor Logistics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Semiconductor Logistics Regional Market Share

Geographic Coverage of Semiconductor Logistics

Semiconductor Logistics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Semiconductor Logistics Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Intrinsic Semiconductor

- 5.1.2. Extrinsic Semiconductor

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Sea Transport

- 5.2.2. Land Transport

- 5.2.3. Air Transport

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Semiconductor Logistics Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Intrinsic Semiconductor

- 6.1.2. Extrinsic Semiconductor

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Sea Transport

- 6.2.2. Land Transport

- 6.2.3. Air Transport

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Semiconductor Logistics Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Intrinsic Semiconductor

- 7.1.2. Extrinsic Semiconductor

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Sea Transport

- 7.2.2. Land Transport

- 7.2.3. Air Transport

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Semiconductor Logistics Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Intrinsic Semiconductor

- 8.1.2. Extrinsic Semiconductor

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Sea Transport

- 8.2.2. Land Transport

- 8.2.3. Air Transport

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Semiconductor Logistics Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Intrinsic Semiconductor

- 9.1.2. Extrinsic Semiconductor

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Sea Transport

- 9.2.2. Land Transport

- 9.2.3. Air Transport

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Semiconductor Logistics Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Intrinsic Semiconductor

- 10.1.2. Extrinsic Semiconductor

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Sea Transport

- 10.2.2. Land Transport

- 10.2.3. Air Transport

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 DHL

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Omni Logistics

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Nippon Express

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Kuehne + Nagel

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Yusen Logistics

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 DB Schenker

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 DSV

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Hey Primo

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 MOL Logistics

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Schnellecke

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 DHL

List of Figures

- Figure 1: Global Semiconductor Logistics Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Semiconductor Logistics Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Semiconductor Logistics Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Semiconductor Logistics Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Semiconductor Logistics Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Semiconductor Logistics Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Semiconductor Logistics Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Semiconductor Logistics Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Semiconductor Logistics Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Semiconductor Logistics Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Semiconductor Logistics Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Semiconductor Logistics Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Semiconductor Logistics Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Semiconductor Logistics Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Semiconductor Logistics Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Semiconductor Logistics Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Semiconductor Logistics Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Semiconductor Logistics Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Semiconductor Logistics Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Semiconductor Logistics Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Semiconductor Logistics Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Semiconductor Logistics Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Semiconductor Logistics Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Semiconductor Logistics Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Semiconductor Logistics Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Semiconductor Logistics Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Semiconductor Logistics Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Semiconductor Logistics Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Semiconductor Logistics Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Semiconductor Logistics Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Semiconductor Logistics Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semiconductor Logistics Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Semiconductor Logistics Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Semiconductor Logistics Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Semiconductor Logistics Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Semiconductor Logistics Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Semiconductor Logistics Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Semiconductor Logistics Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Semiconductor Logistics Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Semiconductor Logistics Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Semiconductor Logistics Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Semiconductor Logistics Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Semiconductor Logistics Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Semiconductor Logistics Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Semiconductor Logistics Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Semiconductor Logistics Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Semiconductor Logistics Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Semiconductor Logistics Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Semiconductor Logistics Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Semiconductor Logistics Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Logistics?

The projected CAGR is approximately 8%.

2. Which companies are prominent players in the Semiconductor Logistics?

Key companies in the market include DHL, Omni Logistics, Nippon Express, Kuehne + Nagel, Yusen Logistics, DB Schenker, DSV, Hey Primo, MOL Logistics, Schnellecke.

3. What are the main segments of the Semiconductor Logistics?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 150 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Logistics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Logistics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Logistics?

To stay informed about further developments, trends, and reports in the Semiconductor Logistics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence