Key Insights

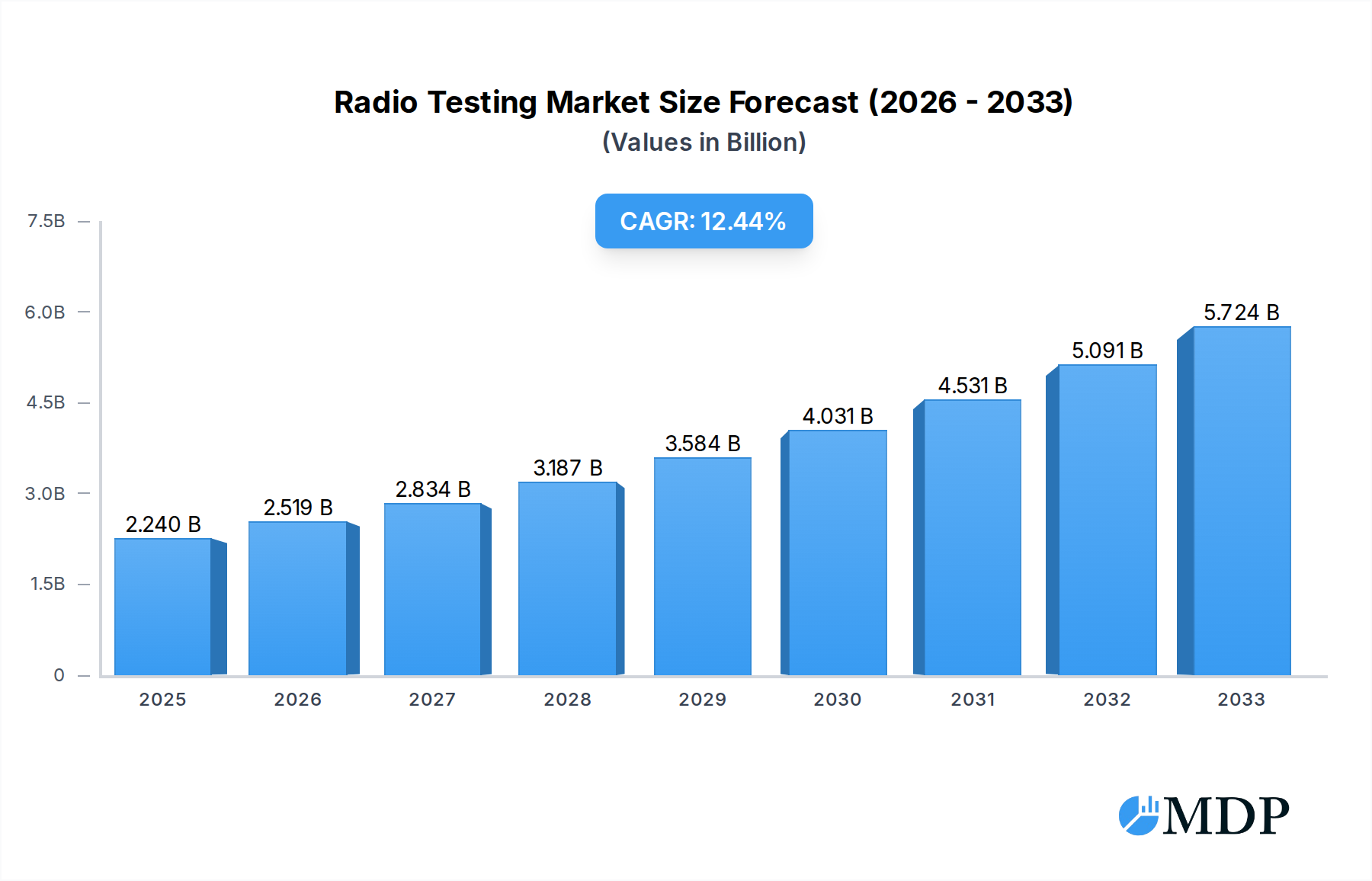

The global radio testing market is poised for significant expansion, projected to reach a USD 2.24 billion valuation by 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 12.28% anticipated throughout the forecast period of 2025-2033. Driving this upward trajectory are several key factors, notably the escalating demand for advanced aeronautical and nautical radio equipment, driven by advancements in aviation and maritime communication systems. Furthermore, the continuous expansion of the cellular sector, with the rollout of 5G and the development of future generations of mobile networks, necessitates rigorous testing to ensure compliance, performance, and safety. The increasing sophistication and adoption of medical devices, which often rely on wireless communication for data transmission and monitoring, also contribute substantially to market growth. Moreover, the proliferation of recognition systems, including RFID technology for inventory management and asset tracking, and the indispensable role of radar equipment in defense, automotive, and meteorological applications, are further propelling the market forward. The overarching trend towards greater connectivity and the increasing complexity of radio frequency (RF) enabled devices across various industries fuels the demand for comprehensive and accurate radio testing services.

Radio Testing Market Size (In Billion)

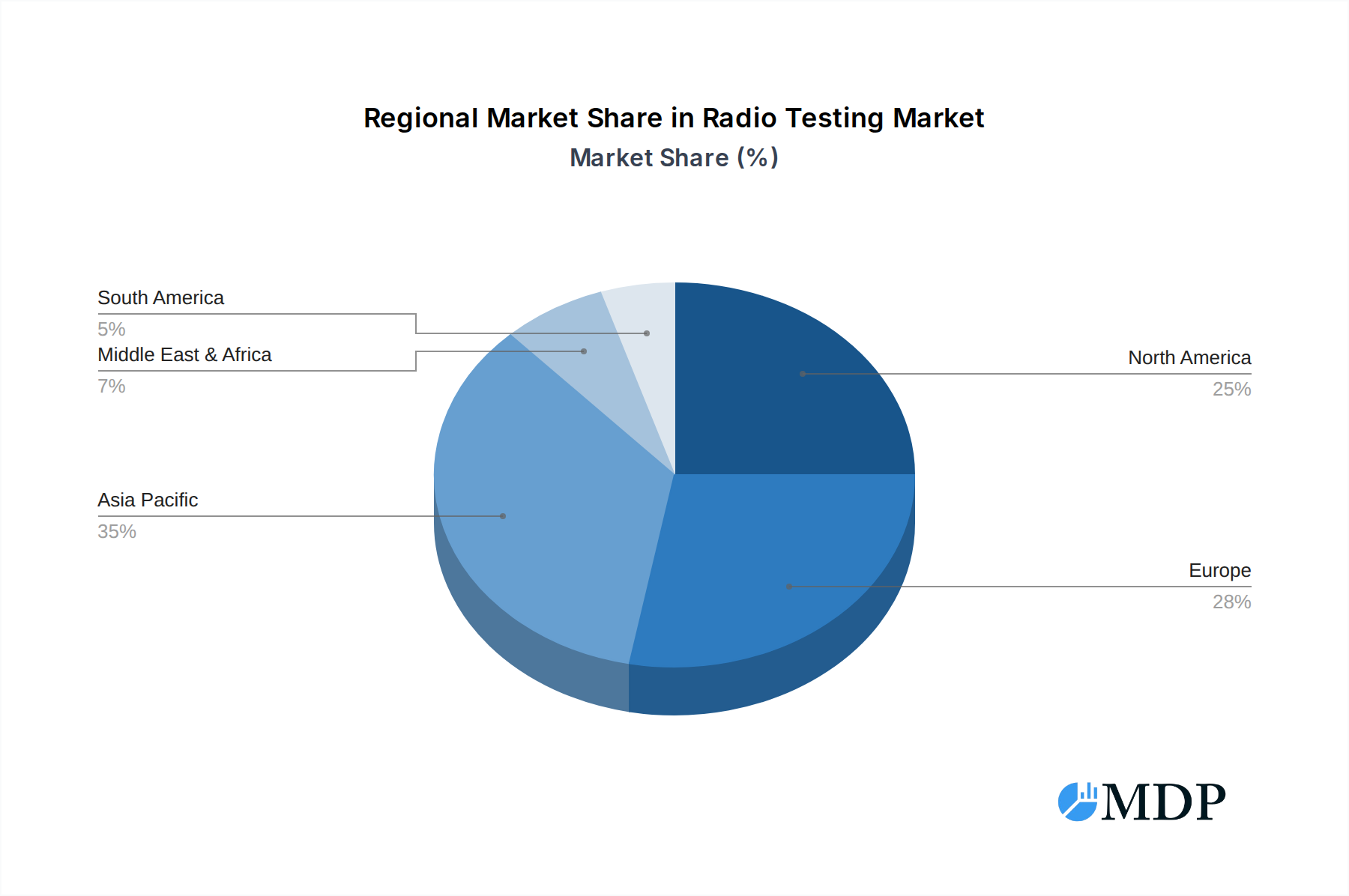

The market's expansion is also shaped by emerging trends such as the integration of Artificial Intelligence (AI) and Machine Learning (ML) in testing methodologies for enhanced efficiency and predictive analysis, alongside the growing adoption of wideband transmission systems and satellite radio technologies for broader coverage and higher data rates. While the market exhibits strong growth potential, certain restraints, such as the high cost of sophisticated testing equipment and the need for specialized expertise, could pose challenges. However, the increasing stringency of regulatory standards for electromagnetic compatibility (EMC) and radio frequency (RF) emissions globally is a significant tailwind, compelling manufacturers to invest heavily in testing to ensure product marketability and compliance. The market segmentation reveals a diverse application landscape, with aeronautical and nautical radio equipment, cellular, medical devices, and radar equipment being prominent segments. High Frequency (HF) and Very High Frequency (VHF) testing remain critical, alongside the growing importance of Active RFID Technology. Geographically, the Asia Pacific region, particularly China and India, is expected to be a dominant force due to its burgeoning manufacturing sector and increasing adoption of advanced technologies, while North America and Europe remain crucial markets with established regulatory frameworks and technological innovation.

Radio Testing Company Market Share

Radio Testing Market Report: Comprehensive Analysis and Future Outlook (2019-2033)

Unlock the billion-dollar potential of the global radio testing market with this definitive, SEO-optimized report. Delve into critical insights, market dynamics, and future trends impacting key segments like Cellular, Aeronautical, and Medical Devices. This report, meticulously researched for the period 2019–2033 with a base year of 2025, provides actionable intelligence for industry stakeholders, including manufacturers, service providers, regulators, and investors. Discover the competitive landscape, leading players, and emerging opportunities driving the billion-dollar radio testing industry.

Radio Testing Market Dynamics & Concentration

The global radio testing market, projected to reach billions in value, exhibits moderate concentration. Key innovation drivers include the relentless demand for faster, more reliable wireless communication, the proliferation of IoT devices, and the evolving regulatory landscape. Regulatory frameworks from bodies like the FCC and ETSI are paramount, dictating testing protocols and compliance standards, thereby shaping market entry and product development. Product substitutes, while limited in the core testing services, can emerge in the form of advanced simulation software and in-house testing capabilities. End-user trends are strongly influenced by the burgeoning adoption of 5G technology, the increasing complexity of connected devices, and the growing emphasis on cybersecurity. Mergers and acquisitions (M&A) activities are a significant factor in market concentration, with larger entities acquiring specialized testing firms to expand their service portfolios and geographic reach. Recent M&A deal counts indicate a trend towards consolidation, driven by the need for economies of scale and enhanced technological expertise. The market share distribution among the top players reflects a competitive yet consolidated environment, with a few dominant entities holding a substantial portion of the total market value.

Radio Testing Industry Trends & Analysis

The radio testing industry is experiencing robust growth, driven by several interconnected trends and technological advancements. The compound annual growth rate (CAGR) for this sector is projected to remain strong throughout the forecast period of 2025–2033, fueled by the continuous evolution of wireless technologies and the increasing need for rigorous compliance. Market penetration is deepening across various end-use applications, from mission-critical aerospace and defense systems to the ubiquitous consumer electronics sector. The escalating adoption of 5G and the subsequent rollout of 6G standards are primary catalysts, demanding sophisticated testing solutions to ensure interoperability, performance, and spectrum efficiency. Furthermore, the expansion of the Internet of Things (IoT) ecosystem, encompassing smart homes, industrial automation, and wearable devices, introduces a vast array of radio-enabled products requiring extensive testing for reliability and security. The medical device industry, with its stringent safety and regulatory requirements, also presents a significant growth avenue, necessitating specialized radio testing to prevent interference and ensure patient safety. Consumer preferences are increasingly leaning towards seamless connectivity and data security, pushing manufacturers to invest heavily in comprehensive radio testing to meet these expectations and gain a competitive edge. Competitive dynamics are characterized by a blend of established global players offering a wide spectrum of services and niche specialists focusing on specific technologies or regulatory domains. Technological disruptions, such as the development of advanced antenna technologies, artificial intelligence-driven testing methodologies, and software-defined radio (SDR), are reshaping the testing landscape, demanding continuous adaptation and innovation from service providers. The increasing complexity and miniaturization of electronic components also pose testing challenges, requiring more sophisticated and precise measurement techniques. The overall trend indicates a sustained upward trajectory for the radio testing market, underpinned by technological progress and expanding application scopes, reaching billions in global market value.

Leading Markets & Segments in Radio Testing

The radio testing market demonstrates significant regional and segmental dominance, driven by technological adoption, economic factors, and regulatory mandates.

Dominant Region and Country Analysis

While a comprehensive global overview is essential, specific regions are emerging as key hubs for radio testing expenditure and innovation. North America and Europe have historically led due to mature telecommunications infrastructure, stringent regulatory environments, and high adoption rates of advanced wireless technologies. However, the Asia-Pacific region, particularly China, South Korea, and Japan, is rapidly ascending in prominence. This surge is attributed to substantial investments in 5G infrastructure deployment, a thriving consumer electronics manufacturing base, and a growing emphasis on domestic technological development. Economic policies in these emerging markets, aimed at fostering innovation and local manufacturing, directly translate into increased demand for radio testing services. Infrastructure development, especially the widespread deployment of 5G base stations and related network components, necessitates extensive pre- and post-deployment testing to ensure optimal performance and compliance.

Dominant Application Segments

The Cellular segment stands out as a primary driver of radio testing demand, with the ongoing evolution from 5G to the nascent stages of 6G development creating a perpetual need for testing new devices, network infrastructure, and interoperability. The sheer volume of cellular-enabled devices manufactured globally underpins this segment's dominance.

- Key Drivers for Cellular Dominance:

- Continuous technological advancements (e.g., mmWave, Massive MIMO).

- Global 5G network expansion and upgrades.

- Proliferation of smartphones, wearables, and connected vehicles.

- Increasing data traffic and demand for higher bandwidth.

The Aeronautical and Nautical Radio Equipment segment is another critical area, characterized by stringent safety regulations and the imperative for faultless communication systems. The complexity and mission-critical nature of aerospace and maritime applications demand the highest levels of testing accuracy and reliability.

- Key Drivers for Aeronautical and Nautical Dominance:

- Unwavering safety and security requirements in aviation and shipping.

- Technological upgrades in aircraft and vessel communication systems.

- Increasing use of satellite communication for navigation and data transfer.

- Stringent compliance with international aviation and maritime standards.

The Medical Devices segment is experiencing significant growth due to the increasing integration of wireless connectivity in healthcare. From remote patient monitoring to implantable devices, these applications require rigorous testing to ensure both efficacy and patient safety, free from electromagnetic interference.

- Key Drivers for Medical Device Dominance:

- Rise of telehealth and remote patient monitoring.

- Development of wireless implantable medical devices.

- Strict regulatory compliance (e.g., FDA, CE marking).

- Need to prevent electromagnetic interference with sensitive medical equipment.

Dominant Types of Radio Frequency

While various frequencies are tested, the High Frequency (HF) and Very High Frequency (VHF) bands remain crucial due to their widespread use in traditional communication systems, broadcasting, and specific industrial applications. However, the emergence of Wideband Transmission Systems, often utilizing higher frequencies, is increasingly gaining traction, especially with the advent of advanced wireless protocols.

- Key Drivers for HF/VHF and Wideband Transmission:

- Established infrastructure and applications for HF/VHF.

- Demand for high-speed data transfer and increased capacity with wideband systems.

- Technological advancements enabling efficient use of wider spectrums.

The Satellite Radio segment is also pivotal, supporting global communication, navigation (GPS), and broadcasting, all of which rely on precise radio testing for signal integrity and performance. The Recognition System segment, encompassing technologies like RFID, is rapidly expanding with the growth of logistics, supply chain management, and access control systems.

Radio Testing Product Developments

Product developments in radio testing are characterized by increased automation, miniaturization, and enhanced accuracy. Innovations are focusing on software-defined testing platforms that offer greater flexibility and adaptability to evolving wireless standards like 5G Advanced and future 6G technologies. Advanced signal generators and analyzers capable of covering wider bandwidths and higher frequencies are becoming standard. Competitive advantages are being forged through the development of AI-powered testing solutions that can predict potential issues, optimize test sequences, and reduce overall testing time and cost. Integration of real-time data analytics and cloud-based testing capabilities are also emerging as key differentiators, allowing for remote testing and collaborative analysis of results, ultimately driving efficiency and accuracy in the billion-dollar radio testing market.

Key Drivers of Radio Testing Growth

The radio testing market's expansion is propelled by a confluence of technological, economic, and regulatory forces. The relentless advancement in wireless communication technologies, from the widespread adoption of 5G to the foundational research for 6G, necessitates continuous testing to ensure performance, interoperability, and adherence to evolving standards. Economically, the booming proliferation of connected devices across consumer electronics, automotive, and industrial IoT sectors creates a sustained demand for validation and certification. Regulatory frameworks worldwide, which mandate compliance for electromagnetic compatibility (EMC), spectrum usage, and safety, act as a crucial driver, pushing manufacturers to invest in comprehensive testing services to gain market access and avoid costly recalls. Furthermore, the increasing complexity of wireless systems, including the integration of multiple wireless technologies within a single device, amplifies the need for sophisticated testing solutions to guarantee seamless operation and prevent interference, contributing billions in market value.

Challenges in the Radio Testing Market

Despite robust growth, the radio testing market faces several significant challenges that can impact its trajectory. The rapid pace of technological evolution, particularly in wireless communications, requires testing laboratories to constantly update their equipment and expertise, incurring substantial capital investment and training costs. Evolving regulatory requirements, while a driver, can also be a hurdle if they become overly complex or inconsistent across different regions, leading to compliance delays. Supply chain disruptions for specialized testing components and equipment can impact the ability of labs to deliver services promptly. Furthermore, intense competition among testing service providers can lead to price pressures, challenging profitability, especially for smaller independent laboratories. The need for specialized skilled personnel capable of operating advanced testing equipment and interpreting complex results also presents a perennial challenge. These factors collectively can temper the market's growth potential, even within this billions-valued industry.

Emerging Opportunities in Radio Testing

The radio testing market is ripe with emerging opportunities driven by technological breakthroughs and strategic market expansion. The ongoing development and deployment of 6G wireless technology present a vast new frontier for testing services, requiring novel approaches to spectrum management, higher frequencies, and advanced signal processing. The expanding ecosystem of the Internet of Things (IoT), particularly in industrial automation and smart cities, is generating a significant demand for reliable and secure wireless connectivity testing. Strategic partnerships between testing laboratories and technology developers, or between testing providers and regulatory bodies, can foster innovation and streamline compliance processes. Furthermore, the increasing focus on cybersecurity in wireless communications creates opportunities for specialized testing focused on vulnerability assessment and secure data transmission. The growing adoption of software-defined radios (SDRs) and artificial intelligence (AI) in testing methodologies offers avenues for developing more efficient, automated, and predictive testing solutions, further enhancing the value proposition in this billions-dollar market.

Leading Players in the Radio Testing Sector

- Applus + Laboratories

- Bureau Veritas

- ByteSnap

- Cecert

- CETECOM

- CMA Testing

- Compliance Direction Systems

- CSA Group Bayern

- DEKRA

- Element

- Elite Electronic Engineering

- EMC Technologies

- EMCC

- Eurofins MET Labs

- Eurofins Scientific

- Fortive

- Intertek

- IPS

- KEYMILE-DZS

- Keysight Technologies

- LabTest Certification

- NTS

- RN Electronics

- Rohde & Schwarz

- SGS

- TOYO

- TÜV Rheinland

- TÜV SÜD Japan

- TÜVNORD CERT

- Underwriters Laboratories (UL)

Key Milestones in Radio Testing Industry

- 2019: Widespread adoption and testing of early 5G devices and infrastructure globally.

- 2020: Increased focus on regulatory compliance for IoT devices and their radio emissions.

- 2021: Emergence of advanced testing solutions for mmWave frequencies, critical for 5G deployment.

- 2022: Significant growth in testing demand for automotive radar and V2X communication systems.

- 2023: Enhanced testing for cybersecurity aspects of wireless devices and networks.

- 2024: Intensified research and development for 6G technologies, leading to early-stage testing needs.

- 2025 (Estimated): Continued global rollout of 5G-Advanced, driving demand for interoperability and performance testing.

- 2026-2033 (Forecast): Gradual transition to pre-commercial and commercial 6G testing, alongside sustained demand for testing across established and emerging wireless applications, contributing billions to the market.

Strategic Outlook for Radio Testing Market

The strategic outlook for the radio testing market is exceptionally positive, driven by an accelerating pace of technological innovation and expanding global connectivity. The transition to 6G, coupled with the ubiquitous growth of IoT, AI-driven applications, and the connected automotive sector, will create sustained demand for sophisticated testing services. Laboratories that invest in cutting-edge technologies, such as AI-powered analytics and advanced simulation capabilities, and focus on specialized segments like cybersecurity and critical infrastructure, will be well-positioned for growth. Strategic partnerships and acquisitions will likely continue to shape the competitive landscape, consolidating expertise and expanding service offerings. The market's ability to adapt to evolving regulatory frameworks and provide efficient, accurate, and cost-effective testing solutions will be paramount to capturing its billions in future potential.

Radio Testing Segmentation

-

1. Application

- 1.1. Aeronautical and Nautical Radio Equipment

- 1.2. Cellular

- 1.3. Medical Devices

- 1.4. Recognition System

- 1.5. Radar Equipment

- 1.6. Satellite Radio

- 1.7. Wideband Transmission Systems

- 1.8. Others

-

2. Types

- 2.1. Low Frequency

- 2.2. High Frequency

- 2.3. Very High Frequency (VHF)

- 2.4. Active RFID Technology

Radio Testing Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Radio Testing Regional Market Share

Geographic Coverage of Radio Testing

Radio Testing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Radio Testing Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aeronautical and Nautical Radio Equipment

- 5.1.2. Cellular

- 5.1.3. Medical Devices

- 5.1.4. Recognition System

- 5.1.5. Radar Equipment

- 5.1.6. Satellite Radio

- 5.1.7. Wideband Transmission Systems

- 5.1.8. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Low Frequency

- 5.2.2. High Frequency

- 5.2.3. Very High Frequency (VHF)

- 5.2.4. Active RFID Technology

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Radio Testing Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aeronautical and Nautical Radio Equipment

- 6.1.2. Cellular

- 6.1.3. Medical Devices

- 6.1.4. Recognition System

- 6.1.5. Radar Equipment

- 6.1.6. Satellite Radio

- 6.1.7. Wideband Transmission Systems

- 6.1.8. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Low Frequency

- 6.2.2. High Frequency

- 6.2.3. Very High Frequency (VHF)

- 6.2.4. Active RFID Technology

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Radio Testing Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aeronautical and Nautical Radio Equipment

- 7.1.2. Cellular

- 7.1.3. Medical Devices

- 7.1.4. Recognition System

- 7.1.5. Radar Equipment

- 7.1.6. Satellite Radio

- 7.1.7. Wideband Transmission Systems

- 7.1.8. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Low Frequency

- 7.2.2. High Frequency

- 7.2.3. Very High Frequency (VHF)

- 7.2.4. Active RFID Technology

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Radio Testing Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aeronautical and Nautical Radio Equipment

- 8.1.2. Cellular

- 8.1.3. Medical Devices

- 8.1.4. Recognition System

- 8.1.5. Radar Equipment

- 8.1.6. Satellite Radio

- 8.1.7. Wideband Transmission Systems

- 8.1.8. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Low Frequency

- 8.2.2. High Frequency

- 8.2.3. Very High Frequency (VHF)

- 8.2.4. Active RFID Technology

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Radio Testing Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aeronautical and Nautical Radio Equipment

- 9.1.2. Cellular

- 9.1.3. Medical Devices

- 9.1.4. Recognition System

- 9.1.5. Radar Equipment

- 9.1.6. Satellite Radio

- 9.1.7. Wideband Transmission Systems

- 9.1.8. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Low Frequency

- 9.2.2. High Frequency

- 9.2.3. Very High Frequency (VHF)

- 9.2.4. Active RFID Technology

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Radio Testing Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aeronautical and Nautical Radio Equipment

- 10.1.2. Cellular

- 10.1.3. Medical Devices

- 10.1.4. Recognition System

- 10.1.5. Radar Equipment

- 10.1.6. Satellite Radio

- 10.1.7. Wideband Transmission Systems

- 10.1.8. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Low Frequency

- 10.2.2. High Frequency

- 10.2.3. Very High Frequency (VHF)

- 10.2.4. Active RFID Technology

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Applus + Laboratories

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Bureau Veritas

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ByteSnap

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Cecert

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 CETECOM

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 CMA Testing

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Compliance Direction Systems

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 CSA Group Bayern

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 DEKRA

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Element

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Elite Electronic Engineering

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 EMC Technologies

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 EMCC

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Eurofins MET Labs

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Eurofins Scientific

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Fortive

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Intertek

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 IPS

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 KEYMILE-DZS

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Keysight Technologies

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 LabTest Certification

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 NTS

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 RN Electronics

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Rohde & Schwarz

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 SGS

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 TOYO

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 TÜV Rheinland

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 TÜV SÜD Japan

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 TÜVNORD CERT

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 Underwriters Laboratories (UL)

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.1 Applus + Laboratories

List of Figures

- Figure 1: Global Radio Testing Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Radio Testing Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Radio Testing Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Radio Testing Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Radio Testing Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Radio Testing Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Radio Testing Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Radio Testing Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Radio Testing Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Radio Testing Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Radio Testing Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Radio Testing Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Radio Testing Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Radio Testing Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Radio Testing Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Radio Testing Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Radio Testing Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Radio Testing Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Radio Testing Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Radio Testing Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Radio Testing Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Radio Testing Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Radio Testing Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Radio Testing Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Radio Testing Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Radio Testing Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Radio Testing Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Radio Testing Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Radio Testing Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Radio Testing Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Radio Testing Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Radio Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Radio Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Radio Testing Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Radio Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Radio Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Radio Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Radio Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Radio Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Radio Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Radio Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Radio Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Radio Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Radio Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Radio Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Radio Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Radio Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Radio Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Radio Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Radio Testing Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Radio Testing?

The projected CAGR is approximately 12.28%.

2. Which companies are prominent players in the Radio Testing?

Key companies in the market include Applus + Laboratories, Bureau Veritas, ByteSnap, Cecert, CETECOM, CMA Testing, Compliance Direction Systems, CSA Group Bayern, DEKRA, Element, Elite Electronic Engineering, EMC Technologies, EMCC, Eurofins MET Labs, Eurofins Scientific, Fortive, Intertek, IPS, KEYMILE-DZS, Keysight Technologies, LabTest Certification, NTS, RN Electronics, Rohde & Schwarz, SGS, TOYO, TÜV Rheinland, TÜV SÜD Japan, TÜVNORD CERT, Underwriters Laboratories (UL).

3. What are the main segments of the Radio Testing?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Radio Testing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Radio Testing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Radio Testing?

To stay informed about further developments, trends, and reports in the Radio Testing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence