Key Insights

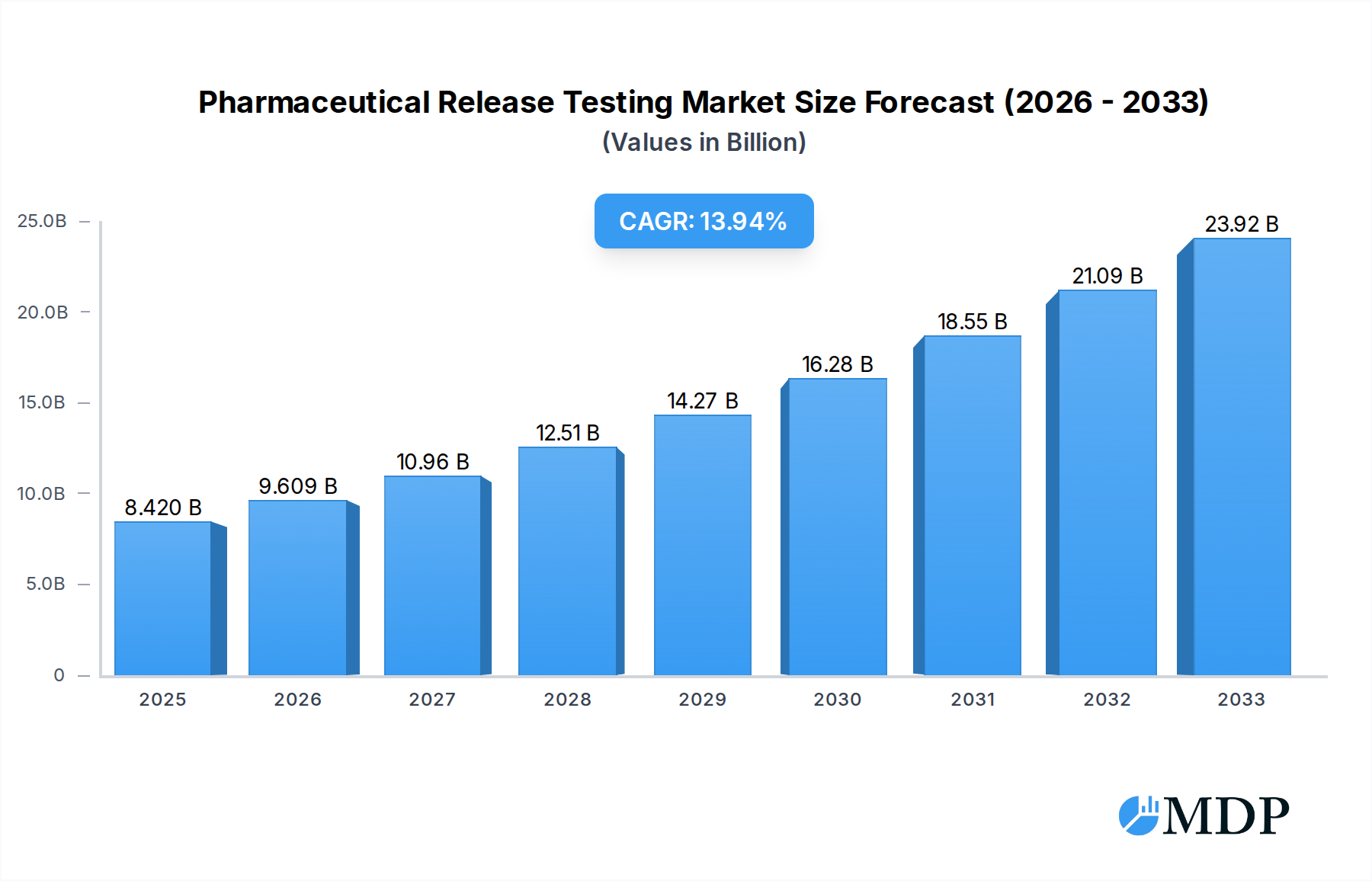

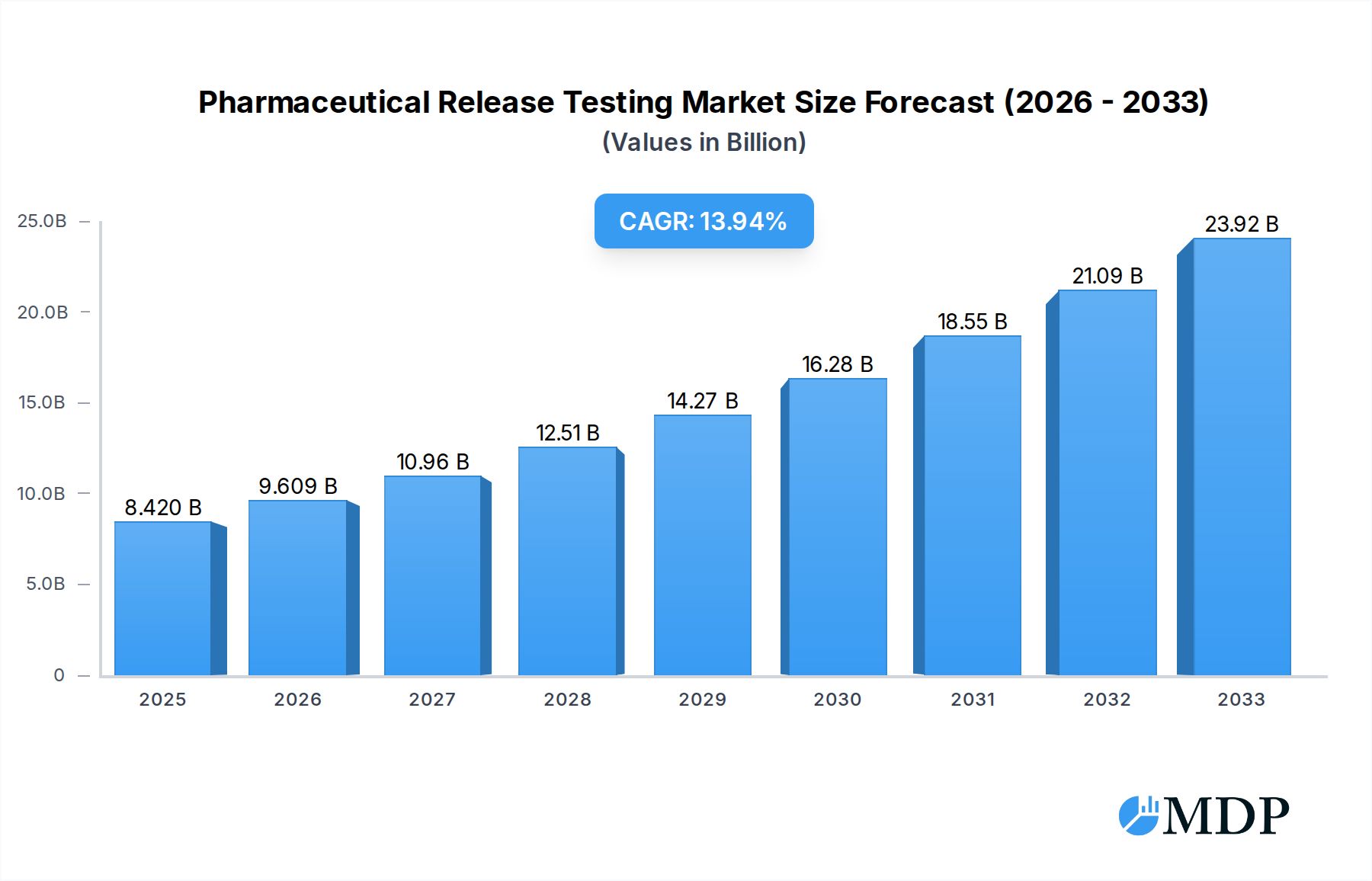

The global Pharmaceutical Release Testing market is poised for substantial growth, projected to reach USD 8.42 billion by 2025, driven by an impressive compound annual growth rate (CAGR) of 14.19%. This robust expansion is fueled by the increasing complexity of drug development, stringent regulatory requirements, and the continuous introduction of new pharmaceutical products. Pharmaceutical companies, both large and small, are heavily investing in comprehensive release testing to ensure the safety, efficacy, and quality of their medicines before they reach the market. The rising prevalence of chronic diseases and the growing demand for novel therapeutics further accentuate the need for reliable and advanced release testing solutions. The market's trajectory indicates a strong reliance on specialized analytical services, highlighting the critical role of contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs) in supporting pharmaceutical innovation and regulatory compliance.

Pharmaceutical Release Testing Market Size (In Billion)

The market is segmented into chemical and physical testing, catering to diverse analytical needs across the drug lifecycle. Key drivers include the escalating cost of drug recalls, the increasing outsourcing of pharmaceutical testing services by companies seeking specialized expertise and cost-efficiency, and the growing trend towards personalized medicine, which necessitates more complex and individualized quality control measures. However, challenges such as the high cost of advanced testing equipment and the shortage of skilled personnel in analytical sciences could temper growth. Despite these hurdles, the market's inherent demand for quality assurance in pharmaceuticals, coupled with technological advancements in analytical instrumentation and automation, paints a very positive outlook for the coming years. Major players are actively engaged in strategic collaborations and acquisitions to expand their service offerings and geographical reach, further solidifying the market's growth trajectory.

Pharmaceutical Release Testing Company Market Share

This in-depth report provides an exhaustive analysis of the global Pharmaceutical Release Testing market, offering critical insights for industry stakeholders, including Big Pharmaceutical Companies and Small and Medium Pharmaceutical Companies. Delve into the intricate dynamics, key trends, leading segments, and future trajectory of this vital sector, encompassing both Chemical Testing and Physical Testing. With a study period spanning from 2019 to 2033, a base year of 2025, and a forecast period from 2025 to 2033, this report equips you with the knowledge to navigate market challenges and capitalize on emerging opportunities. Discover detailed market share data, CAGR projections, and the impact of industry developments on market growth.

Pharmaceutical Release Testing Market Dynamics & Concentration

The Pharmaceutical Release Testing market exhibits a moderately concentrated landscape, with several prominent players vying for market share, estimated at over 100 billion. Key innovation drivers include the increasing complexity of drug formulations, the demand for advanced analytical techniques, and the continuous push for enhanced product safety and efficacy. Regulatory frameworks, such as those established by the FDA and EMA, play a pivotal role in shaping market dynamics, dictating stringent testing protocols and quality standards. Product substitutes, while limited due to the specialized nature of release testing, can emerge in the form of evolving analytical technologies or internal testing capabilities developed by larger pharmaceutical entities. End-user trends are heavily influenced by the growing outsourcing of testing services by both Big Pharmaceutical Companies and Small and Medium Pharmaceutical Companies, seeking cost efficiencies and access to specialized expertise. Mergers and acquisitions (M&A) activity is a significant factor in market concentration, with an estimated 10 billion in M&A deals observed annually. Strategic acquisitions allow companies to expand their service portfolios, geographic reach, and technological capabilities, thereby consolidating market power.

- Market Concentration: Moderate, with a few key players holding significant market share, estimated at over 100 billion.

- Innovation Drivers: Increasing drug complexity, demand for advanced analytics, product safety, and efficacy.

- Regulatory Frameworks: Strict guidelines from FDA, EMA, and other global health authorities are paramount.

- Product Substitutes: Limited, primarily evolving analytical technologies or in-house testing capabilities.

- End-User Trends: Growing outsourcing by both large and small pharmaceutical companies.

- M&A Activities: Significant, with an estimated 10 billion in deals annually, driving consolidation.

Pharmaceutical Release Testing Industry Trends & Analysis

The Pharmaceutical Release Testing industry is poised for robust growth, driven by a confluence of escalating demand for safe and effective pharmaceuticals, stringent regulatory oversight, and rapid technological advancements. The Compound Annual Growth Rate (CAGR) for this market is projected to be approximately 8%, leading to an estimated market size exceeding 250 billion by 2033. Growth drivers are multifaceted, encompassing the expanding pipeline of biologics and complex small molecules, which necessitate sophisticated and highly specialized release testing methodologies. The increasing prevalence of chronic diseases globally fuels the demand for novel drug development, consequently amplifying the need for comprehensive release testing throughout the drug lifecycle. Technological disruptions are a significant force, with the adoption of automation, artificial intelligence (AI), and advanced spectroscopic techniques revolutionizing the speed, accuracy, and efficiency of testing. For instance, AI-powered data analysis can significantly reduce the time required for complex chromatographic or spectroscopic data interpretation, contributing to faster batch release. Consumer preferences for safer and more reliable medications, coupled with heightened public awareness regarding drug quality, further compel pharmaceutical manufacturers to invest heavily in rigorous release testing. Competitive dynamics are characterized by a strategic focus on expanding service offerings, investing in cutting-edge technologies, and establishing strong regulatory compliance credentials. Companies are increasingly differentiating themselves through specialized expertise in areas like biosimilar testing, sterile product testing, and advanced impurity profiling. Market penetration is also being driven by the growing need for specialized contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs) that can offer end-to-end release testing solutions. The estimated market penetration is currently at 70%, with significant room for expansion, especially in emerging economies. The increasing outsourcing trend, estimated to account for over 50% of total release testing expenditure, underscores the value proposition offered by specialized testing service providers. The integration of digital technologies, such as blockchain for secure data management and IoT for real-time monitoring of testing equipment, is further shaping the industry landscape, promising enhanced traceability and operational transparency. The global pharmaceutical market's estimated value of over 1.5 trillion directly correlates with the substantial investment in its foundational element: release testing.

Leading Markets & Segments in Pharmaceutical Release Testing

The Pharmaceutical Release Testing market is characterized by the dominance of Big Pharmaceutical Companies as the primary consumers of these critical services, accounting for an estimated 75% of the total market revenue, projected to reach over 180 billion. This dominance stems from their extensive drug portfolios, high-volume production, and the sheer scale of their research and development activities, which necessitate vast and continuous release testing. Big Pharma companies often partner with multiple specialized testing providers to ensure comprehensive coverage and redundancy in their supply chains, seeking partners with proven track records and advanced technological capabilities. Their stringent quality requirements and regulatory compliance demands drive significant investment in sophisticated analytical methods and robust quality assurance systems.

In terms of testing types, Chemical Testing holds a commanding position, representing approximately 60% of the market share, valued at over 150 billion. This segment encompasses a wide array of analytical techniques crucial for verifying the identity, purity, potency, and stability of drug substances and drug products. These include chromatography (HPLC, GC), spectroscopy (UV-Vis, IR, Mass Spectrometry), titrations, and dissolution testing, all vital for ensuring that active pharmaceutical ingredients (APIs) meet predefined specifications and that the final dosage form delivers the intended therapeutic effect.

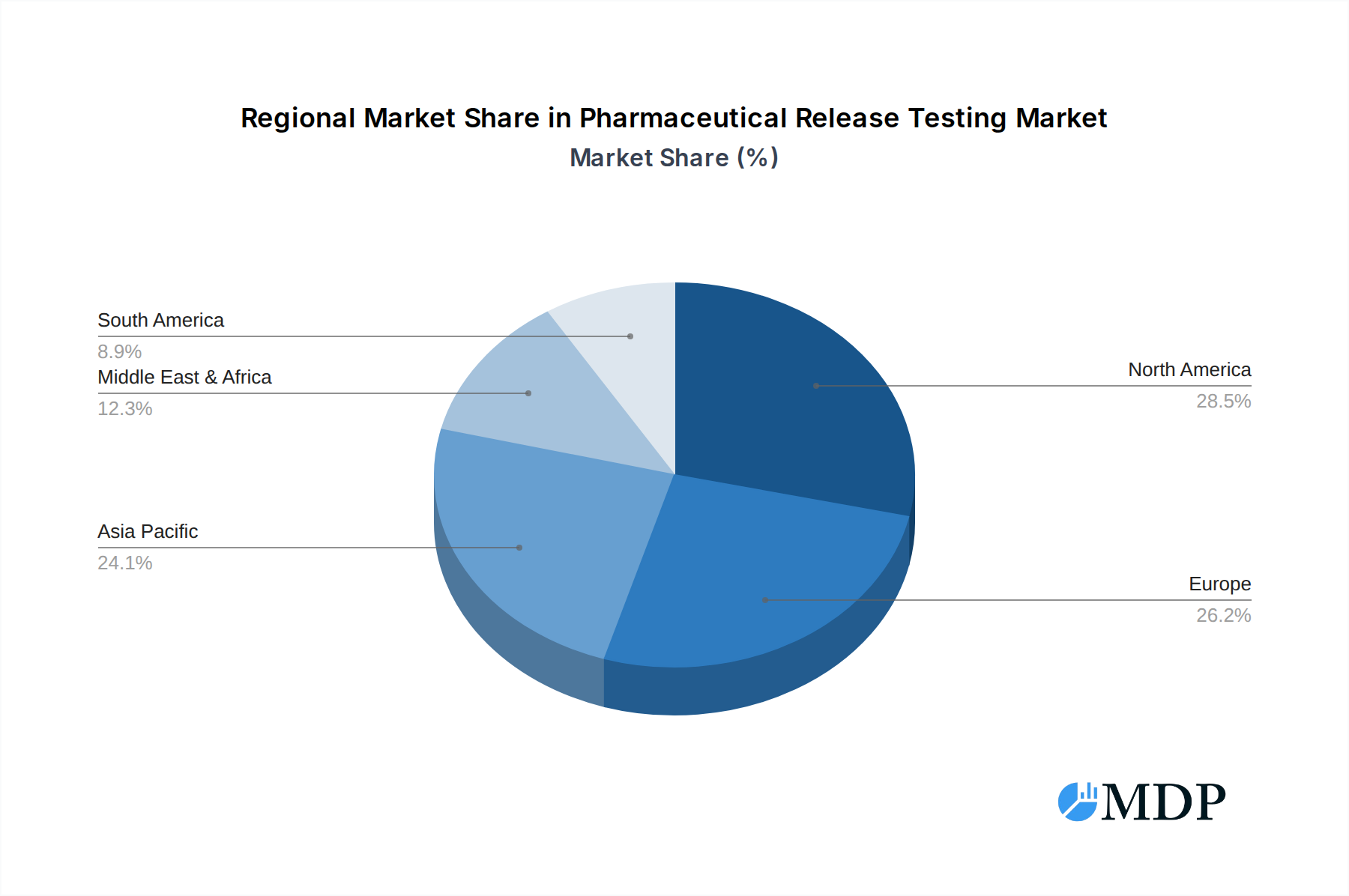

The United States stands as the largest and most influential regional market for Pharmaceutical Release Testing, commanding an estimated 40% of the global market share, projected to exceed 100 billion. This leadership is attributed to several key drivers:

- Robust Pharmaceutical Industry: The presence of a significant number of Big Pharmaceutical Companies and a thriving biotech sector fuels substantial demand for release testing.

- Stringent Regulatory Environment: The Food and Drug Administration (FDA) enforces rigorous quality control and testing standards, compelling manufacturers to invest heavily in compliant release testing.

- High R&D Investment: The US leads global pharmaceutical R&D expenditure, translating into a constant flow of new drug candidates requiring extensive testing.

- Advanced Technological Adoption: The widespread adoption of cutting-edge analytical instrumentation and automation in testing laboratories enhances efficiency and accuracy.

- Strong CRO/CDMO Ecosystem: A well-established network of contract research and manufacturing organizations provides specialized release testing services, catering to the diverse needs of the industry.

While Small and Medium Pharmaceutical Companies represent a smaller market share individually, their collective demand is significant and growing, contributing an estimated 25% to the market, valued at over 60 billion. These companies often leverage outsourcing more heavily due to resource constraints, making them key clients for flexible and cost-effective release testing solutions.

Pharmaceutical Release Testing Product Developments

Recent product developments in Pharmaceutical Release Testing are focused on enhancing speed, accuracy, and automation. Innovations include the integration of artificial intelligence and machine learning for accelerated data analysis, advanced spectroscopic techniques offering more comprehensive molecular insights, and the development of miniaturized, portable testing devices for on-site analysis. These advancements enable quicker batch release, improve impurity detection capabilities, and provide more detailed characterization of drug substances and products. Competitive advantages are being gained through the ability to offer integrated solutions that combine multiple analytical techniques and provide real-time data monitoring, ultimately leading to improved product quality and reduced time-to-market.

Key Drivers of Pharmaceutical Release Testing Growth

The growth of the Pharmaceutical Release Testing market is propelled by several critical factors. Firstly, the escalating complexity of novel drug molecules, particularly biologics and gene therapies, necessitates more sophisticated and specialized testing methods. Secondly, continuously evolving and increasingly stringent global regulatory requirements, enforced by bodies like the FDA and EMA, mandate rigorous quality control and assurance, driving demand for compliant testing services. Economic factors, such as the growing global healthcare expenditure and the expanding pharmaceutical market itself, indirectly fuel investment in release testing. Technological advancements in analytical instrumentation, including automation and AI, are improving the efficiency and accuracy of testing, further supporting market expansion.

- Technological Advancements: AI-driven data analysis, advanced chromatography, and spectroscopy.

- Regulatory Stringency: Evolving and stricter guidelines from global health authorities.

- Drug Development Pipeline: Increasing number of complex biologics and personalized medicines.

- Global Healthcare Expenditure: Rising investments in pharmaceuticals and healthcare services.

Challenges in the Pharmaceutical Release Testing Market

Despite robust growth prospects, the Pharmaceutical Release Testing market faces several significant challenges. Navigating complex and ever-evolving regulatory landscapes across different geographies can be costly and time-consuming, with deviations leading to significant delays or product recalls. Supply chain disruptions, particularly for specialized reagents and equipment, can impact testing timelines and operational continuity. Intense competition among testing service providers can lead to price pressures, potentially affecting profit margins. Furthermore, the high cost of advanced analytical instrumentation and the need for highly skilled personnel present considerable investment barriers, especially for smaller players. The estimated impact of regulatory hurdles on project timelines can be up to 20%, and supply chain issues can lead to delays of 10% to 15%.

- Regulatory Hurdles: Complex and dynamic global compliance requirements.

- Supply Chain Issues: Disruptions in the availability of specialized reagents and equipment.

- Competitive Pressures: Price wars and the need for continuous differentiation.

- High Investment Costs: Significant capital required for advanced instrumentation and skilled workforce.

Emerging Opportunities in Pharmaceutical Release Testing

Emerging opportunities in the Pharmaceutical Release Testing market are largely driven by technological innovation and strategic market expansion. The growing demand for biosimilar and biopharmaceutical testing presents a significant growth avenue, requiring specialized expertise in areas like immunogenicity and protein characterization. The increasing adoption of personalized medicine and cell and gene therapies will drive the need for highly specialized and rapid release testing solutions. Furthermore, the expansion of pharmaceutical manufacturing in emerging economies, coupled with their developing regulatory frameworks, offers substantial opportunities for testing service providers to establish a strong presence. Strategic partnerships and collaborations between testing laboratories and pharmaceutical companies can foster innovation and streamline the development process. The integration of digital technologies, such as blockchain for enhanced data integrity and traceability, also presents a promising future.

Leading Players in the Pharmaceutical Release Testing Sector

- Intertek

- Eurofins

- SGS

- Almac

- Excite Pharma Services

- Charles River Laboratories

- Bio-Rad

- Element

- Merck

- Boston Analytical

- ALS Life Sciences

- Reading Scientific Services

- Lucideon

- Tepnel Pharma Services

- Nutrasource

- Vetter Pharma

- WESSLING

- TUV SUD

- Sotax

- Pace Analytical

- Tergus Pharma

- Symbiosis

- Broughton Group

Key Milestones in Pharmaceutical Release Testing Industry

- 2019: Increased adoption of QbD (Quality by Design) principles influencing release testing strategies.

- 2020: Surge in demand for rapid microbial testing methods due to pandemic-related supply chain pressures.

- 2021: Significant investment in automation and AI for data analysis in release testing laboratories.

- 2022: Growing focus on impurity profiling and elemental analysis for complex drug products.

- 2023: Expansion of specialized testing services for biologics and biosimilars.

- 2024: Increased adoption of advanced spectroscopic techniques for enhanced drug characterization.

- 2025 (Estimated): Further integration of digital technologies like blockchain for enhanced data security and traceability.

- 2026 (Projected): Greater emphasis on sustainability in testing methodologies and waste reduction.

- 2027 (Projected): Increased collaboration between CROs and Big Pharma for integrated release testing solutions.

- 2028 (Projected): Maturation of AI-driven predictive analytics for release testing outcomes.

- 2029 (Projected): Development of novel, miniaturized testing devices for point-of-care applications.

- 2030 (Projected): Widespread adoption of continuous manufacturing models, impacting release testing paradigms.

- 2031 (Projected): Enhanced focus on cybersecurity for sensitive analytical data.

- 2032 (Projected): Further specialization in testing for advanced therapeutic modalities like cell and gene therapies.

- 2033 (Projected): Global harmonization of regulatory requirements for release testing becoming more prevalent.

Strategic Outlook for Pharmaceutical Release Testing Market

The strategic outlook for the Pharmaceutical Release Testing market remains exceptionally strong, fueled by an unwavering commitment to drug safety and efficacy. Growth accelerators will continue to be driven by the relentless innovation in pharmaceutical R&D, leading to increasingly complex drug molecules that demand sophisticated analytical solutions. The ongoing expansion of the global pharmaceutical market, particularly in emerging economies, will provide significant untapped potential. Companies that strategically invest in cutting-edge technologies, cultivate deep expertise in specialized testing areas like biologics and advanced therapies, and maintain robust compliance with evolving regulatory standards will be best positioned for sustained success. Furthermore, fostering strong client relationships through reliable service delivery and integrated solutions will be paramount in navigating this dynamic and critical sector of the pharmaceutical industry.

Pharmaceutical Release Testing Segmentation

-

1. Application

- 1.1. Big Pharmaceutical Companies

- 1.2. Small and Medium Pharmaceutical Companies

-

2. Types

- 2.1. Chemical Testing

- 2.2. Physical Testing

Pharmaceutical Release Testing Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Pharmaceutical Release Testing Regional Market Share

Geographic Coverage of Pharmaceutical Release Testing

Pharmaceutical Release Testing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.19% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Pharmaceutical Release Testing Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Big Pharmaceutical Companies

- 5.1.2. Small and Medium Pharmaceutical Companies

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Chemical Testing

- 5.2.2. Physical Testing

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Pharmaceutical Release Testing Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Big Pharmaceutical Companies

- 6.1.2. Small and Medium Pharmaceutical Companies

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Chemical Testing

- 6.2.2. Physical Testing

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Pharmaceutical Release Testing Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Big Pharmaceutical Companies

- 7.1.2. Small and Medium Pharmaceutical Companies

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Chemical Testing

- 7.2.2. Physical Testing

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Pharmaceutical Release Testing Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Big Pharmaceutical Companies

- 8.1.2. Small and Medium Pharmaceutical Companies

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Chemical Testing

- 8.2.2. Physical Testing

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Pharmaceutical Release Testing Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Big Pharmaceutical Companies

- 9.1.2. Small and Medium Pharmaceutical Companies

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Chemical Testing

- 9.2.2. Physical Testing

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Pharmaceutical Release Testing Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Big Pharmaceutical Companies

- 10.1.2. Small and Medium Pharmaceutical Companies

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Chemical Testing

- 10.2.2. Physical Testing

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Intertek

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Eurofins

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SGS

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Almac

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Excite Pharma Services

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Charles River Laboratories

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bio-Rad

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Element

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Merck

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Boston Analytical

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 ALS Life Sciences

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Reading Scientific Services

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Lucideon

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Tepnel Pharma Services

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Nutrasource

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Vetter Pharma

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 WESSLING

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 TUV SUD

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Sotax

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Pace Analytical

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Tergus Pharma

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Symbiosis

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Broughton Group

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.1 Intertek

List of Figures

- Figure 1: Global Pharmaceutical Release Testing Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Pharmaceutical Release Testing Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Pharmaceutical Release Testing Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Pharmaceutical Release Testing Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Pharmaceutical Release Testing Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Pharmaceutical Release Testing Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Pharmaceutical Release Testing Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Pharmaceutical Release Testing Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Pharmaceutical Release Testing Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Pharmaceutical Release Testing Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Pharmaceutical Release Testing Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Pharmaceutical Release Testing Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Pharmaceutical Release Testing Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Pharmaceutical Release Testing Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Pharmaceutical Release Testing Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Pharmaceutical Release Testing Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Pharmaceutical Release Testing Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Pharmaceutical Release Testing Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Pharmaceutical Release Testing Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Pharmaceutical Release Testing Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Pharmaceutical Release Testing Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Pharmaceutical Release Testing Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Pharmaceutical Release Testing Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Pharmaceutical Release Testing Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Pharmaceutical Release Testing Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Pharmaceutical Release Testing Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Pharmaceutical Release Testing Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Pharmaceutical Release Testing Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Pharmaceutical Release Testing Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Pharmaceutical Release Testing Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Pharmaceutical Release Testing Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Pharmaceutical Release Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Pharmaceutical Release Testing Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pharmaceutical Release Testing?

The projected CAGR is approximately 14.19%.

2. Which companies are prominent players in the Pharmaceutical Release Testing?

Key companies in the market include Intertek, Eurofins, SGS, Almac, Excite Pharma Services, Charles River Laboratories, Bio-Rad, Element, Merck, Boston Analytical, ALS Life Sciences, Reading Scientific Services, Lucideon, Tepnel Pharma Services, Nutrasource, Vetter Pharma, WESSLING, TUV SUD, Sotax, Pace Analytical, Tergus Pharma, Symbiosis, Broughton Group.

3. What are the main segments of the Pharmaceutical Release Testing?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pharmaceutical Release Testing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pharmaceutical Release Testing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pharmaceutical Release Testing?

To stay informed about further developments, trends, and reports in the Pharmaceutical Release Testing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence