Key Insights

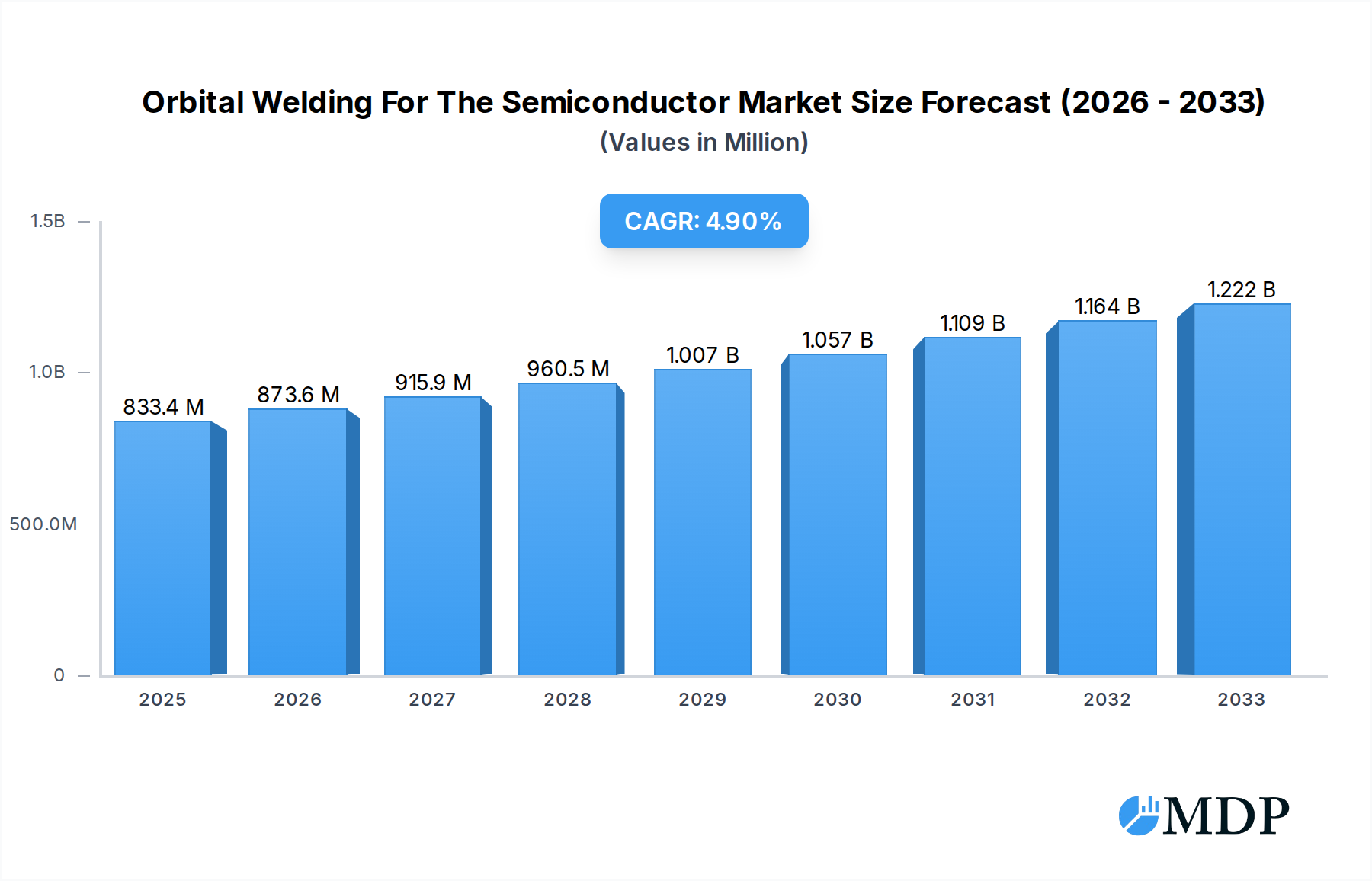

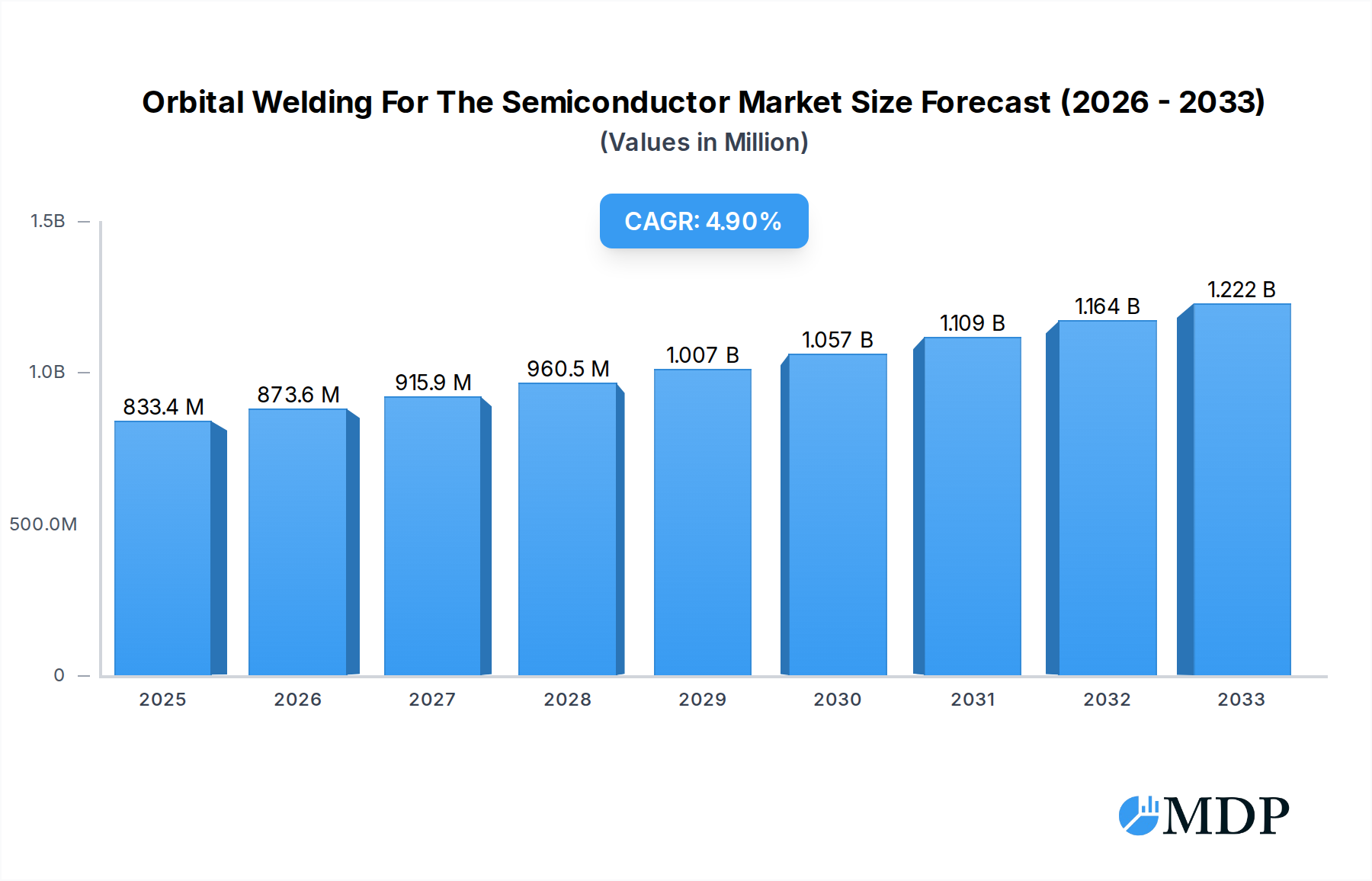

The global Orbital Welding for Semiconductor market is poised for significant expansion, projected to reach an estimated $833.4 million in 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 4.8%, indicating a steady and sustained upward trajectory for the foreseeable future. A primary driver for this market is the escalating demand for high-purity gas delivery systems within the semiconductor manufacturing process. As semiconductor fabrication becomes increasingly sophisticated, the need for exceptionally clean and precise welding solutions for gas lines, vacuum systems, and other critical infrastructure is paramount. This directly fuels the adoption of orbital welding technology, which offers superior weld integrity, reduced contamination, and enhanced process control compared to traditional manual welding methods. Furthermore, the market is benefiting from the continuous evolution of semiconductor manufacturing technologies, including advancements in node technologies and the increasing complexity of integrated circuits, all of which necessitate advanced and reliable manufacturing processes.

Orbital Welding For The Semiconductor Market Size (In Million)

The market is segmented into key applications and types that highlight areas of significant opportunity and adoption. In terms of application, High Purity Gas Delivery stands out as a dominant segment, directly correlating with the technological demands of semiconductor production. Other applications within the semiconductor ecosystem also contribute to market growth. On the type front, TIG Welding and MIG Welding are prominent, with advancements in automated orbital welding systems for both offering enhanced efficiency and precision. Companies like Magnatech LLC, Orbitalum Tools GmbH, and Arc Machines, Inc. are at the forefront, offering innovative solutions that cater to these specific needs. The market's growth is further supported by extensive investments in semiconductor manufacturing facilities globally, particularly in Asia Pacific and North America, driven by the burgeoning demand for electronic devices. While the market is robust, potential restraints such as the high initial investment cost for advanced orbital welding equipment and the need for specialized skilled labor could pose challenges. However, the long-term benefits in terms of product quality, yield improvement, and operational efficiency are expected to outweigh these concerns.

Orbital Welding For The Semiconductor Company Market Share

Orbital Welding For The Semiconductor: Precision, Purity, and Progress

This comprehensive Orbital Welding for Semiconductor market report delves deep into the critical technologies and trends shaping the fabrication of ultra-pure semiconductor components. Covering the Study Period: 2019–2033, with a Base Year: 2025 and a Forecast Period: 2025–2033, this analysis provides unparalleled insights for industry stakeholders. It examines the pivotal role of advanced welding solutions, essential for High Purity Gas Delivery and other critical semiconductor manufacturing applications.

Orbital Welding For The Semiconductor Market Dynamics & Concentration

The orbital welding market for the semiconductor industry is characterized by a moderate to high concentration, with key players dominating specialized segments. Major companies like Magnatech LLC, Orbitalum Tools GmbH, Arc Machines, Inc., and Swagelok command significant market share, driven by their advanced technological capabilities and long-standing relationships with semiconductor manufacturers. Innovation is a primary driver, with continuous advancements in TIG Welding and MIG Welding technologies focusing on enhanced precision, speed, and automation. Regulatory frameworks, particularly those emphasizing purity standards and safety, heavily influence market entry and product development. Product substitutes, while existing, often fall short in meeting the stringent purity and reliability requirements of semiconductor fabrication. End-user trends, such as miniaturization and increased chip complexity, necessitate more sophisticated and automated welding solutions. Mergers and acquisitions (M&A) activities, though not excessively frequent, are strategic moves aimed at consolidating market position, acquiring new technologies, and expanding geographical reach. Recent M&A deal counts stand at approximately 5 to 10 significant transactions within the historical period, contributing to market consolidation. The estimated market share of the top 3 players is projected to be around 60% by the base year, indicating a concentrated yet competitive landscape.

Orbital Welding For The Semiconductor Industry Trends & Analysis

The orbital welding industry for semiconductors is poised for substantial growth, fueled by the insatiable demand for advanced microchips and the ever-increasing complexity of semiconductor manufacturing processes. The market is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 8% to 10% from 2025 to 2033. This robust expansion is underpinned by several key trends. Firstly, the relentless drive for smaller, faster, and more powerful semiconductors necessitates an unwavering focus on material purity and weld integrity. Orbital welding, with its inherent precision and control, is paramount in preventing contamination and ensuring leak-tight connections in high-purity gas delivery systems, which are the lifeblood of wafer fabrication.

Technological disruptions are continuously reshaping the industry. The integration of artificial intelligence (AI) and machine learning (ML) in orbital welding systems is enabling real-time process optimization, predictive maintenance, and enhanced automation. This allows for greater consistency, reduced human error, and faster throughput on the manufacturing floor. Advanced sensor technologies provide immediate feedback on weld parameters, ensuring adherence to the strictest quality standards. Furthermore, the development of specialized welding heads and power sources tailored for exotic materials and challenging geometries found in advanced semiconductor equipment further pushes the boundaries of what's achievable.

Consumer preferences, indirectly, are a significant driver. The proliferation of smartphones, data centers, AI-driven applications, and the Internet of Things (IoT) creates an escalating demand for semiconductors, thereby stimulating investment in advanced manufacturing infrastructure. This, in turn, drives the adoption of state-of-the-art orbital welding equipment capable of meeting the high-volume, high-precision demands of the industry.

Competitive dynamics are intensifying as more companies invest in R&D and seek to capture market share. Key players are focusing on developing integrated solutions that encompass welding equipment, automation, software, and comprehensive support services. The market penetration of highly automated and intelligent orbital welding systems is expected to rise significantly, moving from approximately 30% in the historical period to an estimated 65% by 2033. This shift is driven by the need to reduce operational costs, improve efficiency, and meet the exacting quality standards of the semiconductor sector. The increasing prevalence of "Others" applications beyond traditional gas delivery, such as fluid handling and vacuum systems, also represents a significant growth avenue.

Leading Markets & Segments in Orbital Welding For The Semiconductor

The High Purity Gas Delivery segment stands as the undisputed leader within the orbital welding for semiconductor market. This dominance stems from the fundamental requirement of semiconductor fabrication for ultra-pure gases to deposit thin films and etch intricate patterns onto silicon wafers. Any contamination or leakage in these gas delivery systems can lead to catastrophic failures, rendering entire batches of chips unusable. Consequently, the demand for precision, hermetic sealing, and material integrity in these systems is paramount, making orbital welding the indispensable technology of choice. The market value for this segment is estimated to be in the hundreds of millions annually.

Within the application landscape, the sub-segment focusing on gas distribution manifolds, regulators, and process piping is particularly significant. The economic policies supporting the growth of the semiconductor industry globally, coupled with substantial government investments in domestic chip manufacturing, act as powerful economic drivers. For instance, initiatives like the CHIPS Act in the United States are directly stimulating the construction of new semiconductor fabs, thereby increasing the demand for high-purity gas delivery systems and the orbital welding solutions required for their assembly. Infrastructure development, including the expansion of cleanroom facilities and the establishment of new manufacturing hubs, further propels the growth of this segment.

TIG Welding represents the most prevalent and critical welding type within the semiconductor industry, accounting for an estimated 70% of the market. This is due to its inherent ability to provide precise control over heat input, leading to clean, high-quality welds with minimal spatter and distortion, crucial for maintaining the pristine environment of semiconductor manufacturing. The technology's suitability for joining a wide range of specialized alloys used in semiconductor equipment, such as stainless steel, Hastelloy, and Inconel, further solidifies its position.

The market value for TIG welding in this sector is estimated to be in the high hundreds of millions, with a projected CAGR of approximately 9%. MIG Welding, while less prevalent, is gaining traction in specific applications where speed and productivity are prioritized, particularly in the assembly of larger components or less critical lines. Its market share is growing, albeit from a smaller base, projected to increase from around 15% to 25% over the forecast period. The "Others" category for welding types encompasses advanced techniques like laser welding and electron beam welding, which are niche but growing in importance for highly specialized applications demanding extreme precision or the joining of dissimilar materials. The combined market value for these leading segments is projected to reach billions of dollars by the end of the forecast period, underscoring the critical importance of orbital welding in the semiconductor ecosystem.

Orbital Welding For The Semiconductor Product Developments

Recent product developments in orbital welding for the semiconductor sector are heavily focused on enhancing automation, intelligence, and precision. Companies are introducing advanced orbital welding heads with integrated sensor technology that provide real-time monitoring of weld parameters, enabling dynamic adjustments for optimal weld quality. The development of intuitive software platforms, often incorporating AI algorithms, allows for simplified programming, remote operation, and comprehensive data logging, crucial for traceability and quality control in semiconductor manufacturing. Furthermore, innovations in power sources are enabling faster welding speeds without compromising weld integrity. Competitive advantages are being gained by vendors offering integrated solutions that combine welding equipment with advanced automation and data analytics, thereby streamlining the manufacturing process for semiconductor fabs and equipment manufacturers. These advancements are directly addressing the growing need for increased throughput, reduced contamination risks, and consistent, high-purity weldments.

Key Drivers of Orbital Welding For The Semiconductor Growth

The growth of the orbital welding market for the semiconductor industry is propelled by a confluence of powerful factors. The insatiable global demand for advanced semiconductors, driven by innovations in AI, 5G, and the Internet of Things, directly translates into increased investment in semiconductor manufacturing infrastructure. This expansion necessitates advanced welding solutions for the critical high-purity gas and fluid delivery systems that are integral to wafer fabrication. Technological advancements in orbital welding itself, such as increased automation, real-time process monitoring, and the ability to weld exotic materials, are continuously improving efficiency and purity standards, making them indispensable for modern fabs. Furthermore, stringent regulatory requirements aimed at ensuring the highest levels of purity and reliability in semiconductor manufacturing environments create a sustained demand for high-quality, contamination-free welds, which orbital welding excels at providing. The projected market size for orbital welding equipment and consumables is expected to reach approximately 1.5 billion dollars by 2033.

Challenges in the Orbital Welding For The Semiconductor Market

Despite the robust growth, the orbital welding for semiconductor market faces several challenges. The stringent purity requirements of the semiconductor industry translate into exceptionally high costs for consumables and specialized equipment, creating a significant barrier to entry for new players and increasing the capital expenditure for semiconductor manufacturers. Supply chain disruptions, particularly for specialized materials and components used in high-end welding systems, can lead to project delays and increased costs. The highly specialized nature of the technology also necessitates a skilled workforce for operation and maintenance, and a shortage of trained technicians can impact operational efficiency. Furthermore, while automation is a key driver, the initial investment in sophisticated automated orbital welding systems can be substantial, posing a challenge for smaller companies or those in rapidly evolving markets.

Emerging Opportunities in Orbital Welding For The Semiconductor

Emerging opportunities in the orbital welding for the semiconductor market are centered around technological innovation and market expansion. The increasing complexity of next-generation semiconductor architectures is creating a demand for even more precise and automated welding solutions, particularly for micro-scale components and novel materials. Advancements in AI and machine learning present opportunities for predictive maintenance of welding equipment and real-time process optimization, further enhancing efficiency and reducing downtime. Strategic partnerships between orbital welding equipment manufacturers and semiconductor equipment suppliers are expected to drive the development of integrated solutions tailored to specific fabrication processes. Furthermore, the global trend towards reshoring semiconductor manufacturing is creating new geographical markets and increasing the demand for localized sales, service, and support of orbital welding technologies.

Leading Players in the Orbital Welding For The Semiconductor Sector

- Magnatech LLC

- Orbitalum Tools GmbH

- Arc Machines, Inc.

- Swagelok

- Orbital Fabrications

- Orbitec GmbH

- Triplenine Group

- INVAC Systems

- Universal Orbital Systems

- POLYSOUDE

- Custom Control Solutions, Inc.

- Ichor Systems

Key Milestones in Orbital Welding For The Semiconductor Industry

- 2019: Introduction of AI-powered process control in advanced orbital welding systems, improving weld consistency.

- 2020: Launch of ultra-compact orbital welding heads designed for confined spaces within semiconductor manufacturing equipment.

- 2021: Significant investment in R&D for automated orbital welding solutions by leading market players to meet rising demand.

- 2022: Strategic partnerships formed between orbital welding specialists and semiconductor equipment manufacturers to develop integrated solutions.

- 2023: Increased adoption of remote monitoring and control capabilities for orbital welding equipment, enhancing operational flexibility.

- 2024: Enhanced sensor integration in orbital welding heads providing real-time data for quality assurance.

Strategic Outlook for Orbital Welding For The Semiconductor Market

The strategic outlook for the orbital welding for the semiconductor market is exceptionally positive, driven by sustained demand for advanced microchips and continuous technological evolution. Growth accelerators include the increasing trend towards automation and intelligent welding systems, offering enhanced precision and efficiency vital for semiconductor fabrication. The ongoing expansion of semiconductor manufacturing facilities globally, coupled with government initiatives to boost domestic production, will further fuel the demand for high-quality orbital welding solutions. Companies focusing on developing integrated offerings that encompass advanced welding technology, automation software, and comprehensive service and support packages are well-positioned for significant market penetration. Furthermore, innovations in welding exotic materials and addressing the challenges of micro-welding for next-generation semiconductor components will unlock substantial future market potential.

Orbital Welding For The Semiconductor Segmentation

-

1. Application

- 1.1. High Purity Gas Delivery

- 1.2. Others

-

2. Type

- 2.1. TIG Welding

- 2.2. MIG Welding

- 2.3. Others

Orbital Welding For The Semiconductor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

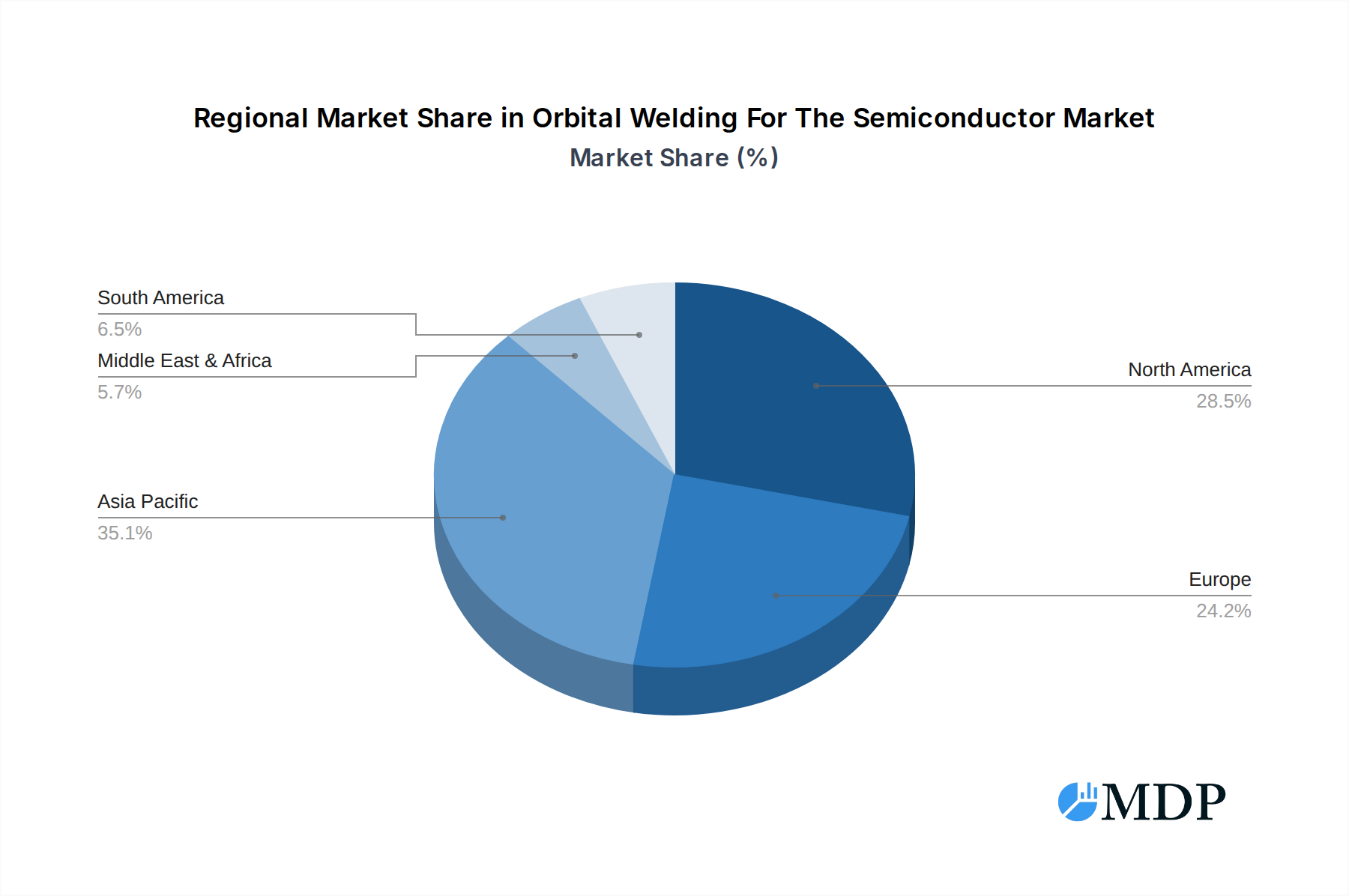

Orbital Welding For The Semiconductor Regional Market Share

Geographic Coverage of Orbital Welding For The Semiconductor

Orbital Welding For The Semiconductor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Orbital Welding For The Semiconductor Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. High Purity Gas Delivery

- 5.1.2. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. TIG Welding

- 5.2.2. MIG Welding

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Orbital Welding For The Semiconductor Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. High Purity Gas Delivery

- 6.1.2. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. TIG Welding

- 6.2.2. MIG Welding

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Orbital Welding For The Semiconductor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. High Purity Gas Delivery

- 7.1.2. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. TIG Welding

- 7.2.2. MIG Welding

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Orbital Welding For The Semiconductor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. High Purity Gas Delivery

- 8.1.2. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. TIG Welding

- 8.2.2. MIG Welding

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Orbital Welding For The Semiconductor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. High Purity Gas Delivery

- 9.1.2. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. TIG Welding

- 9.2.2. MIG Welding

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Orbital Welding For The Semiconductor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. High Purity Gas Delivery

- 10.1.2. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. TIG Welding

- 10.2.2. MIG Welding

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Magnatech LLC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Orbitalum Tools GmbH

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Arc Machines Inc.

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Swagelok

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Orbital Fabrications

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Orbitec GmbH

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Triplenine Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 INVAC Systems

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Universal Orbital Systems

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 POLYSOUDE

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Custom Control Solutions Inc.

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Ichor Systems

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Magnatech LLC

List of Figures

- Figure 1: Global Orbital Welding For The Semiconductor Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Orbital Welding For The Semiconductor Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Orbital Welding For The Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Orbital Welding For The Semiconductor Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Orbital Welding For The Semiconductor Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Orbital Welding For The Semiconductor Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Orbital Welding For The Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Orbital Welding For The Semiconductor Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Orbital Welding For The Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Orbital Welding For The Semiconductor Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Orbital Welding For The Semiconductor Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Orbital Welding For The Semiconductor Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Orbital Welding For The Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Orbital Welding For The Semiconductor Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Orbital Welding For The Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Orbital Welding For The Semiconductor Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Orbital Welding For The Semiconductor Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Orbital Welding For The Semiconductor Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Orbital Welding For The Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Orbital Welding For The Semiconductor Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Orbital Welding For The Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Orbital Welding For The Semiconductor Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Orbital Welding For The Semiconductor Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Orbital Welding For The Semiconductor Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Orbital Welding For The Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Orbital Welding For The Semiconductor Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Orbital Welding For The Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Orbital Welding For The Semiconductor Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Orbital Welding For The Semiconductor Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Orbital Welding For The Semiconductor Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Orbital Welding For The Semiconductor Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Orbital Welding For The Semiconductor Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Orbital Welding For The Semiconductor Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Orbital Welding For The Semiconductor?

The projected CAGR is approximately 4.8%.

2. Which companies are prominent players in the Orbital Welding For The Semiconductor?

Key companies in the market include Magnatech LLC, Orbitalum Tools GmbH, Arc Machines, Inc., Swagelok, Orbital Fabrications, Orbitec GmbH, Triplenine Group, INVAC Systems, Universal Orbital Systems, POLYSOUDE, Custom Control Solutions, Inc., Ichor Systems.

3. What are the main segments of the Orbital Welding For The Semiconductor?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Orbital Welding For The Semiconductor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Orbital Welding For The Semiconductor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Orbital Welding For The Semiconductor?

To stay informed about further developments, trends, and reports in the Orbital Welding For The Semiconductor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence