Key Insights

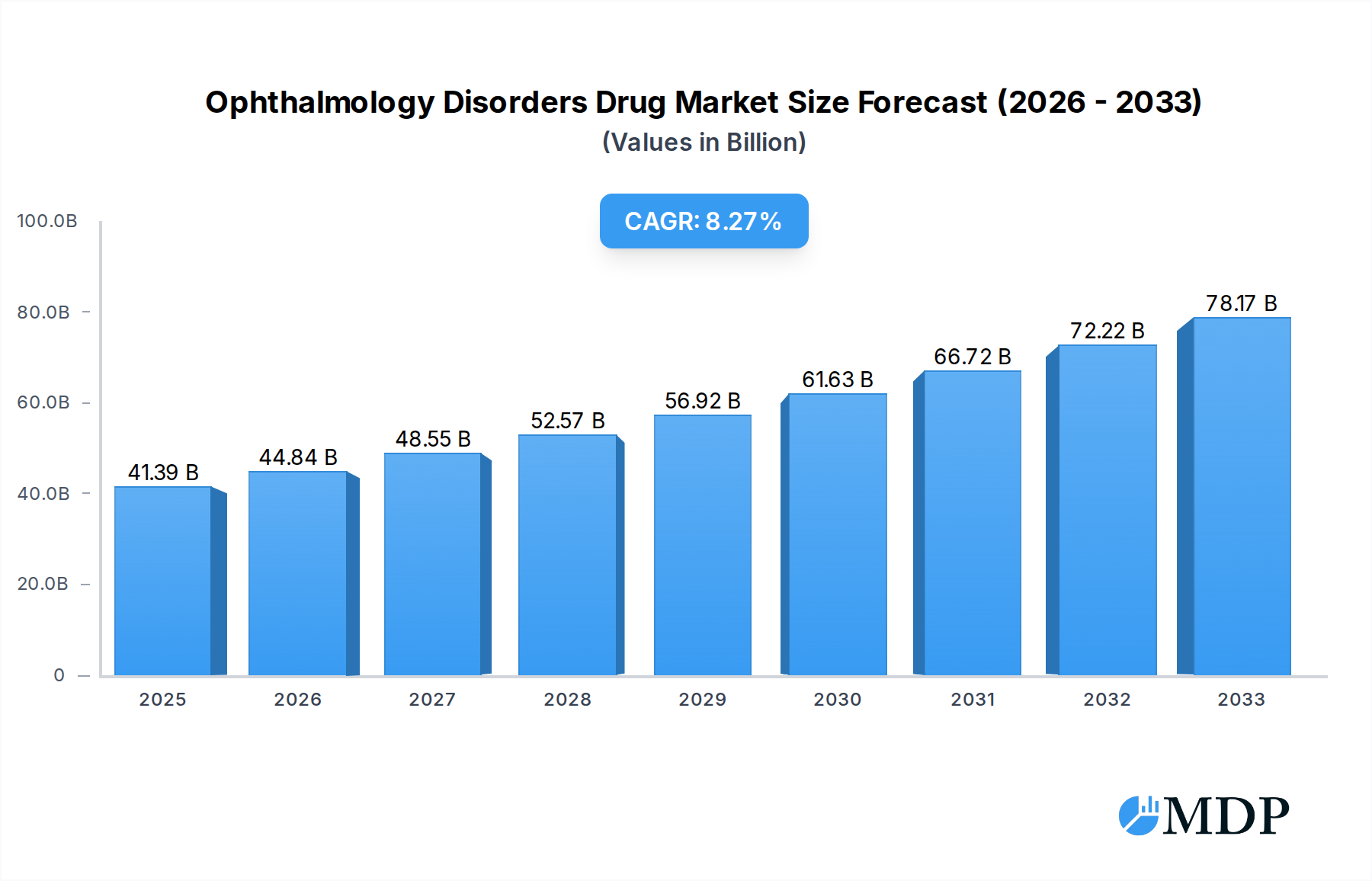

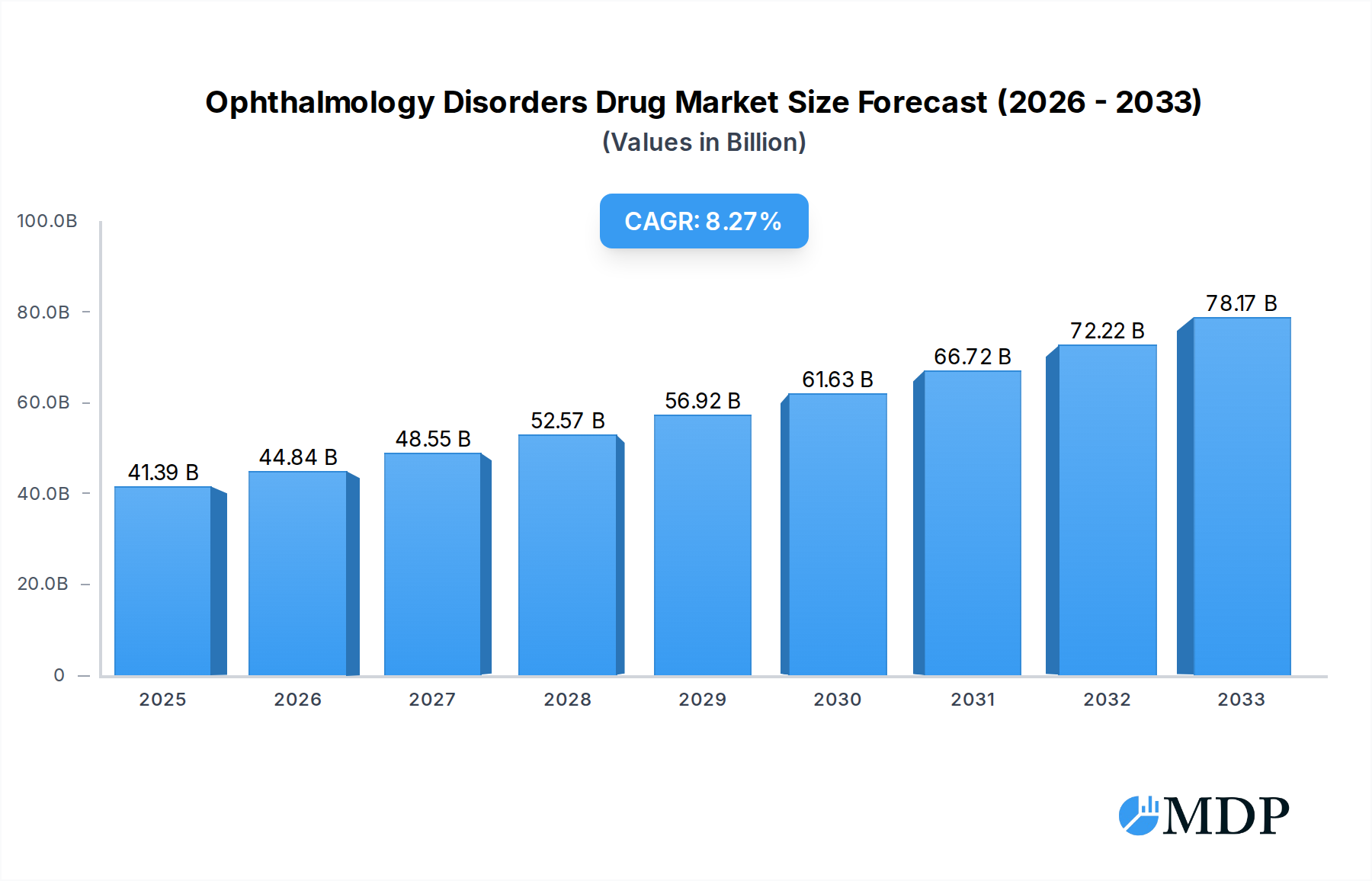

The global Ophthalmology Disorders Drug market is poised for significant expansion, projecting a market size of $41.39 billion in 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 8.51% through 2033. This robust growth trajectory is fueled by a confluence of factors, including a rising global prevalence of eye diseases, an aging population susceptible to various vision impairments, and increasing research and development investments in novel therapeutic solutions. Key therapeutic areas driving this expansion encompass Juvenile Macular Degeneration (Stargardt Disease), Leber Congenital Amaurosis (LCA), Leber’s Hereditary Optic Neuropathy (LHON), Usher Syndrome, and Retinitis Pigmentosa. The market's demand is also being shaped by the introduction of advanced drug delivery systems, such as oral medications and targeted injections, offering improved patient compliance and therapeutic efficacy. Furthermore, a growing awareness and diagnosis rate of rare ophthalmic conditions contribute to a larger addressable market.

Ophthalmology Disorders Drug Market Size (In Billion)

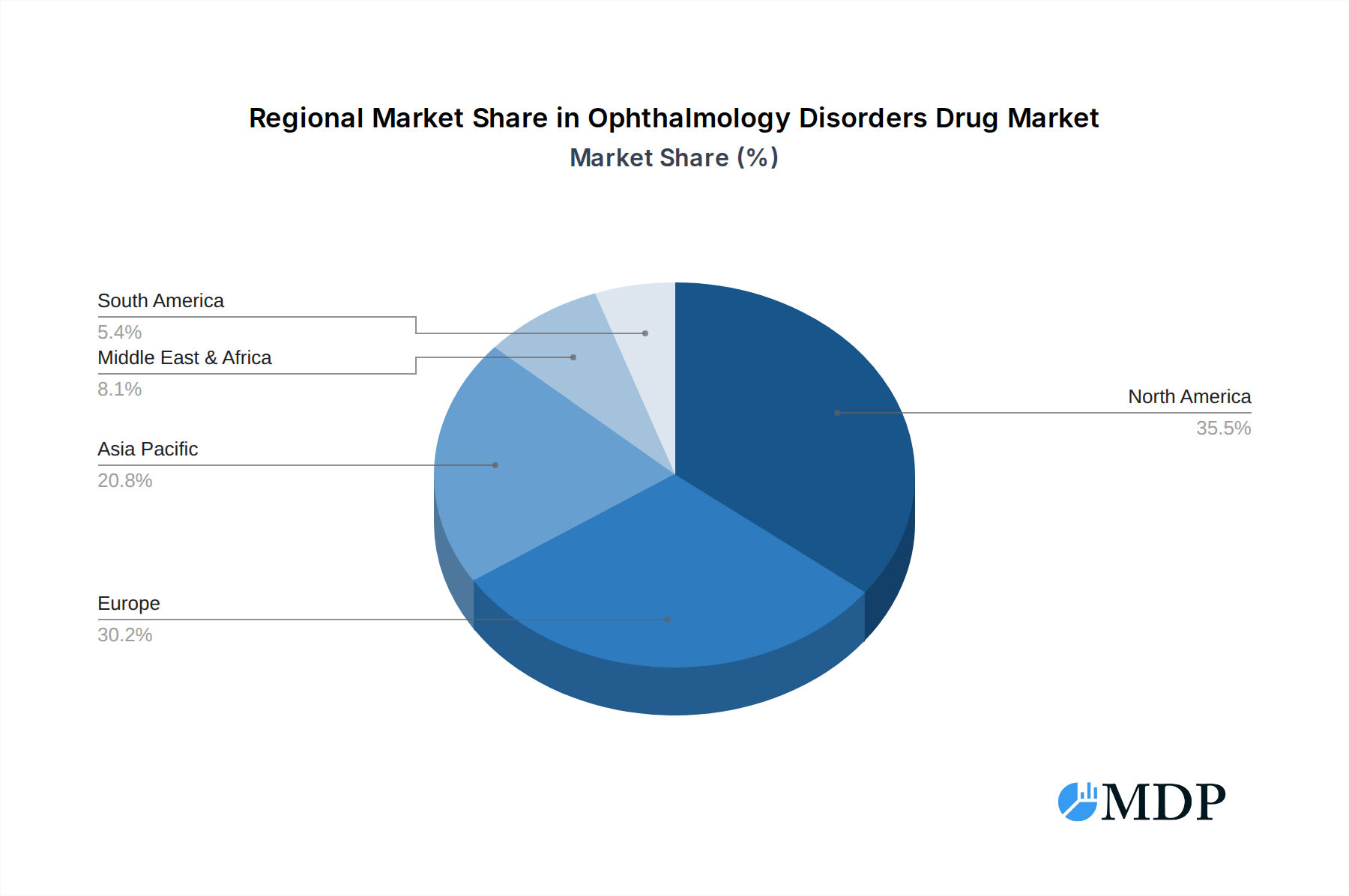

The competitive landscape is characterized by the presence of major pharmaceutical giants and innovative biotechnology firms, actively engaged in developing both established and next-generation treatments. Companies are focusing on gene therapies, small molecule inhibitors, and regenerative medicine approaches to address unmet medical needs. While the market demonstrates strong growth potential, certain restraints exist, including the high cost of drug development, stringent regulatory approvals, and the complexity of treating genetic ophthalmic disorders. However, the significant unmet medical need and the potential for life-changing treatments for patients suffering from vision loss continue to incentivize innovation and investment. Geographic segmentation reveals North America and Europe as leading markets, driven by advanced healthcare infrastructure and high healthcare expenditure, with Asia Pacific showing promising growth potential due to increasing healthcare access and a burgeoning patient population.

Ophthalmology Disorders Drug Company Market Share

Unlocking Vision: A Comprehensive Analysis of the Ophthalmology Disorders Drug Market (2019-2033)

This in-depth report provides a critical examination of the global Ophthalmology Disorders Drug Market, a rapidly evolving sector projected to witness substantial growth. Delving into the intricate dynamics, key trends, and strategic imperatives, this analysis is essential for pharmaceutical companies, research institutions, investors, and policymakers seeking to navigate and capitalize on opportunities within the retinal disease treatment landscape. The report covers a comprehensive study period from 2019 to 2033, with a base year of 2025, and forecasts for the period 2025-2033, building upon historical data from 2019-2024. Gain actionable insights into vision loss treatment, rare eye disease therapies, and inherited retinal disease drugs.

Ophthalmology Disorders Drug Market Dynamics & Concentration

The Ophthalmology Disorders Drug Market is characterized by moderate to high concentration, driven by significant R&D investments and stringent regulatory pathways for ophthalmic pharmaceuticals. Innovation remains a primary driver, with a strong focus on developing novel gene therapies for blindness, regenerative medicine for eye conditions, and targeted treatments for age-related macular degeneration (AMD) alternatives and inherited retinal diseases. The regulatory frameworks governing drug approval, particularly for orphan drugs, play a crucial role in shaping market access and commercialization strategies. Product substitutes, while evolving, are largely focused on supportive care or earlier stages of disease, highlighting the unmet need for effective therapeutic interventions. End-user trends indicate a growing demand for treatments addressing specific subtypes of retinal degeneration, with increasing patient advocacy for access to innovative therapies. Mergers and acquisitions (M&A) activities are anticipated to remain robust, as larger pharmaceutical entities seek to bolster their pipelines with cutting-edge technologies and acquire promising early-stage assets. For instance, a predicted xx billion in M&A deal counts over the forecast period underscores the consolidation trend.

- Market Concentration: Dominated by a mix of established pharmaceutical giants and agile biotechnology firms specializing in ophthalmology.

- Innovation Drivers: Gene therapy advancements, stem cell research, novel drug delivery systems, and precision medicine approaches for macular degeneration treatments.

- Regulatory Frameworks: FDA, EMA, and other regional health authorities' rigorous approval processes for vision restoration drugs.

- Product Substitutes: Primarily supportive therapies, visual aids, and early-stage interventions; limited direct substitutes for advanced stage blindness treatment.

- End-User Trends: Increasing patient awareness, demand for minimally invasive procedures, and preference for treatments addressing specific genetic mutations.

- M&A Activities: Strategic acquisitions of smaller biotech firms with promising R&D pipelines in retinal diseases and optic nerve disorders.

Ophthalmology Disorders Drug Industry Trends & Analysis

The Ophthalmology Disorders Drug Industry is poised for remarkable expansion, driven by a confluence of factors including an aging global population, increasing prevalence of eye conditions, and groundbreaking advancements in biotechnological research. The global market size for ophthalmology drugs is projected to reach an estimated xx billion by 2025, with a compound annual growth rate (CAGR) of approximately xx% from 2019-2024 and expected to accelerate further through 2033. Technological disruptions are at the forefront of this growth, particularly in the realm of gene therapy and personalized medicine. Innovations such as CRISPR-based gene editing and adeno-associated virus (AAV) vectors are revolutionizing the treatment of genetic eye diseases, offering hope for conditions previously deemed untreatable. Consumer preferences are shifting towards more effective and less invasive treatment modalities, with a growing interest in therapies that can preserve or restore vision rather than merely slow disease progression. The competitive landscape is becoming increasingly dynamic, with key players heavily investing in R&D and forging strategic alliances to gain a competitive edge in the treatment of Usher Syndrome, Leber Congenital Amaurosis (LCA), and Juvenile Macular Degeneration (Stargardt Disease). Market penetration is expected to deepen as regulatory approvals expand and novel therapies become more accessible to a wider patient demographic, particularly in emerging economies. The market penetration for advanced therapies is predicted to grow from xx% in 2025 to xx% by 2033.

Leading Markets & Segments in Ophthalmology Disorders Drug

The Ophthalmology Disorders Drug Market exhibits significant regional dominance and segmentation, with North America currently leading in terms of market share, driven by robust healthcare infrastructure, high R&D spending, and a strong presence of leading pharmaceutical and biotechnology companies. The United States, in particular, represents a pivotal market due to early adoption of innovative therapies and substantial patient populations suffering from conditions like Retinitis Pigmentosa (RP) and Leber’s Hereditary Optic Neuropathy (LHON). Within the application segment, Juvenile Macular Degeneration (Stargardt Disease) and Retinitis Pigmentosa (Retinitis) represent substantial growth areas, fueled by ongoing research and the development of targeted therapies. The treatment of Usher Syndrome, a complex genetic disorder affecting hearing and vision, is also gaining traction with the emergence of potential gene therapies. From a type perspective, Injection-based therapies continue to dominate due to their direct delivery to the eye, facilitating higher drug concentrations and efficacy for conditions such as age-related macular degeneration (AMD). However, the development of novel Oral formulations for systemic and targeted ocular delivery, and advanced External Use drug delivery systems are gaining momentum, offering greater patient convenience and potentially improved compliance for conditions like dry eye and certain forms of glaucoma. The market penetration of injection therapies is estimated at xx% in 2025, projected to reach xx% by 2033, while oral therapies are expected to grow from xx% to xx% within the same period.

- Dominant Region: North America, with the United States as the primary market, driven by advanced healthcare systems and significant R&D investment.

- Key Application Segments:

- Juvenile Macular Degeneration (Stargardt Disease): Growing demand for effective treatments to preserve central vision in young patients.

- Retinitis Pigmentosa (Retinitis): Significant unmet need and active research into gene therapies and neuroprotection.

- Usher Syndrome: Focus on genetic therapies to address the dual loss of sight and hearing.

- Leber Congenital Amaurosis (LCA): Early gene therapies showing promise for restoring vision in infants.

- Leber’s Hereditary Optic Neuropathy (LHON): Emergence of targeted therapies for this rare optic nerve disorder.

- Dominant Drug Type:

- Injection: Currently the most prevalent, offering targeted delivery for conditions like wet AMD.

- Oral: Increasing interest in developing systemic and targeted oral therapies for broader patient accessibility.

- External Use: Continued innovation in eye drops and other topical applications for various ocular surface diseases.

Ophthalmology Disorders Drug Product Developments

The Ophthalmology Disorders Drug Market is witnessing a wave of innovative product developments, particularly in gene therapy and regenerative medicine for inherited retinal diseases. Companies are leveraging cutting-edge technologies to create novel vision restoration drugs and therapies for Usher Syndrome. These advancements offer improved efficacy, targeted delivery mechanisms, and better patient outcomes for conditions like Leber Congenital Amaurosis (LCA) and Stargardt Disease. Key competitive advantages stem from the ability to address the root genetic causes of these disorders, offering potential for long-term vision preservation and even restoration. Technological trends are pushing the boundaries of what's possible in treating previously intractable vision loss disorders.

Key Drivers of Ophthalmology Disorders Drug Growth

Several key factors are propelling the growth of the Ophthalmology Disorders Drug Market. Technological advancements, particularly in gene therapy and regenerative medicine for eye conditions, are enabling the development of previously unimaginable treatments for rare eye diseases. The increasing global prevalence of age-related ocular conditions, coupled with a growing and aging population, significantly expands the patient pool. Furthermore, robust investments in research and development by both established pharmaceutical giants and innovative biotech firms are accelerating the discovery and commercialization of new vision loss treatments. Favorable regulatory pathways for orphan drugs also encourage the development of therapies for rare retinal degeneration disorders.

Challenges in the Ophthalmology Disorders Drug Market

Despite promising growth, the Ophthalmology Disorders Drug Market faces significant challenges. The high cost of developing and manufacturing advanced therapies, especially gene and cell therapies, leads to substantial pricing, creating accessibility issues for a broad patient base. Stringent and lengthy regulatory approval processes, while ensuring safety and efficacy, can delay market entry. Supply chain complexities for specialized biologics and the need for specialized administration further complicate market dynamics. Intense competition among companies developing similar therapeutic approaches also poses a challenge, requiring continuous innovation and differentiation in the treatment of Usher Syndrome and other complex ocular conditions.

Emerging Opportunities in Ophthalmology Disorders Drug

Emerging opportunities in the Ophthalmology Disorders Drug Market are primarily driven by breakthroughs in gene editing technologies and an increased understanding of the genetic underpinnings of various inherited retinal diseases. Strategic partnerships between academic institutions, biotech startups, and large pharmaceutical companies are fostering collaborative research and accelerating drug development pipelines for vision restoration drugs. The expanding pipeline of drugs targeting previously untreatable conditions like Juvenile Macular Degeneration (Stargardt Disease) and specific subtypes of Retinitis Pigmentosa (RP) presents significant market expansion potential. Furthermore, the growing focus on precision medicine and personalized treatments for rare eye diseases is opening new avenues for therapeutic innovation.

Leading Players in the Ophthalmology Disorders Drug Sector

- Sanofi

- Bayer

- Bausch + Lomb

- Novartis

- Takeda Pharmaceutical

- Roche

- Pfizer

- Allergan

- Gilead Sciences

- Kubota Pharmaceutical

- Alkeus Pharmaceuticals

- Astellas Pharma

- Ferrer Corporate

- Amgen Inc

- Editas Medicine Inc

- ProQR Therapeutics NV

- ReNeuron

- Amarantus BioScience

- Ocugen

- ReGenX Biosciences

- Sucampo Pharmaceuticals

- Orphagen Pharmaceuticals

- Okuvision

- Second Sight Medical

- Acucela

- Stealth BioTherapeutics

- Sun Pharma Advanced Research Company

- AmpliPhi Biosciences

- Applied Genetic Technologies

- Asklepios BioPharmaceutical

- Biovista

- Spark Therapeutics

- Caladrius Biosciences

- Dompe Farmaceutici

- Dormant Projects

- Grupo Ferrer Internacional

- ID Pharma

- InFlectis BioScience

- Ionis Pharmaceuticals

- Ixchel Pharma

- Khondrion

- Mimetogen Pharmaceuticals

- Mitotech

- M's Science

- Nanovector

- SanBio

Key Milestones in Ophthalmology Disorders Drug Industry

- 2019: Approval of Luxturna (voretigene neparvovec-rzyl) for RPE65 mutation-associated inherited retinal dystrophy.

- 2020: Initiation of clinical trials for gene therapies targeting specific subtypes of Retinitis Pigmentosa.

- 2021: Significant advancements in preclinical research for Usher Syndrome treatments utilizing CRISPR technology.

- 2022: Emergence of new therapeutic candidates for Leber Congenital Amaurosis (LCA) in Phase 1/2 trials.

- 2023: Increased M&A activity with acquisitions of early-stage biotech firms focused on ocular gene therapy.

- 2024: Promising early-stage data for novel oral treatments for certain types of macular degeneration.

- 2025: Expected regulatory submissions for advanced therapies targeting Stargardt Disease.

- 2026-2033: Anticipated wave of product launches for a range of rare and inherited retinal diseases.

Strategic Outlook for Ophthalmology Disorders Drug Market

The Ophthalmology Disorders Drug Market is set for substantial future growth, driven by an accelerating pipeline of gene therapies, regenerative medicines, and targeted small molecules. The increasing understanding of ocular disease pathogenesis and advancements in drug delivery systems will be key growth accelerators. Strategic opportunities lie in addressing unmet needs in rare and complex vision loss disorders, expanding into emerging markets, and forging strong partnerships to navigate the complex regulatory and reimbursement landscape. Companies that can effectively demonstrate the long-term value and improved quality of life offered by their innovative therapies will be best positioned for success.

Ophthalmology Disorders Drug Segmentation

-

1. Application

- 1.1. Juvenile Macular Degeneration (Stargardt Disease)

- 1.2. Leber Congenital Amaurosis (LCA)

- 1.3. Leber’s Hereditary Optic Neuropathy (LHON) (Leber Optic Atrophy)

- 1.4. Usher Syndrome

- 1.5. Retinitis Pigmentosa (Retinitis)

-

2. Type

- 2.1. Oral

- 2.2. Injection

- 2.3. External Use

Ophthalmology Disorders Drug Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ophthalmology Disorders Drug Regional Market Share

Geographic Coverage of Ophthalmology Disorders Drug

Ophthalmology Disorders Drug REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ophthalmology Disorders Drug Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Juvenile Macular Degeneration (Stargardt Disease)

- 5.1.2. Leber Congenital Amaurosis (LCA)

- 5.1.3. Leber’s Hereditary Optic Neuropathy (LHON) (Leber Optic Atrophy)

- 5.1.4. Usher Syndrome

- 5.1.5. Retinitis Pigmentosa (Retinitis)

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Oral

- 5.2.2. Injection

- 5.2.3. External Use

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Ophthalmology Disorders Drug Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Juvenile Macular Degeneration (Stargardt Disease)

- 6.1.2. Leber Congenital Amaurosis (LCA)

- 6.1.3. Leber’s Hereditary Optic Neuropathy (LHON) (Leber Optic Atrophy)

- 6.1.4. Usher Syndrome

- 6.1.5. Retinitis Pigmentosa (Retinitis)

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Oral

- 6.2.2. Injection

- 6.2.3. External Use

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Ophthalmology Disorders Drug Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Juvenile Macular Degeneration (Stargardt Disease)

- 7.1.2. Leber Congenital Amaurosis (LCA)

- 7.1.3. Leber’s Hereditary Optic Neuropathy (LHON) (Leber Optic Atrophy)

- 7.1.4. Usher Syndrome

- 7.1.5. Retinitis Pigmentosa (Retinitis)

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Oral

- 7.2.2. Injection

- 7.2.3. External Use

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ophthalmology Disorders Drug Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Juvenile Macular Degeneration (Stargardt Disease)

- 8.1.2. Leber Congenital Amaurosis (LCA)

- 8.1.3. Leber’s Hereditary Optic Neuropathy (LHON) (Leber Optic Atrophy)

- 8.1.4. Usher Syndrome

- 8.1.5. Retinitis Pigmentosa (Retinitis)

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Oral

- 8.2.2. Injection

- 8.2.3. External Use

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Ophthalmology Disorders Drug Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Juvenile Macular Degeneration (Stargardt Disease)

- 9.1.2. Leber Congenital Amaurosis (LCA)

- 9.1.3. Leber’s Hereditary Optic Neuropathy (LHON) (Leber Optic Atrophy)

- 9.1.4. Usher Syndrome

- 9.1.5. Retinitis Pigmentosa (Retinitis)

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Oral

- 9.2.2. Injection

- 9.2.3. External Use

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Ophthalmology Disorders Drug Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Juvenile Macular Degeneration (Stargardt Disease)

- 10.1.2. Leber Congenital Amaurosis (LCA)

- 10.1.3. Leber’s Hereditary Optic Neuropathy (LHON) (Leber Optic Atrophy)

- 10.1.4. Usher Syndrome

- 10.1.5. Retinitis Pigmentosa (Retinitis)

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Oral

- 10.2.2. Injection

- 10.2.3. External Use

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Sanofi

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Bayer

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Bausch + Lomb

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Novartis

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Usher Syndrome

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Takeda Pharmaceutical

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Roche

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Pfizer

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Allergan

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Gilead Sciences

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Kubota Pharmaceutical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Alkeus Pharmaceuticals

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Astellas Pharma

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Ferrer Corporate

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Amgen Inc

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Editas Medicine Inc

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 ProQR Therapeutics NV

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 ReNeuron

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Amarantus BioScience

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Ocugen

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 ReGenX Biosciences

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Sucampo Pharmaceuticals

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Orphagen Pharmaceuticals

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Okuvision

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Second Sight Medical

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Acucela

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 Stealth BioTherapeutics

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 Sun Pharma Advanced Research Company

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 AmpliPhi Biosciences

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 Applied Genetic Technologies

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.31 Asklepios BioPharmaceutical

- 11.2.31.1. Overview

- 11.2.31.2. Products

- 11.2.31.3. SWOT Analysis

- 11.2.31.4. Recent Developments

- 11.2.31.5. Financials (Based on Availability)

- 11.2.32 Biovista

- 11.2.32.1. Overview

- 11.2.32.2. Products

- 11.2.32.3. SWOT Analysis

- 11.2.32.4. Recent Developments

- 11.2.32.5. Financials (Based on Availability)

- 11.2.33 Spark Therapeutics

- 11.2.33.1. Overview

- 11.2.33.2. Products

- 11.2.33.3. SWOT Analysis

- 11.2.33.4. Recent Developments

- 11.2.33.5. Financials (Based on Availability)

- 11.2.34 Caladrius Biosciences

- 11.2.34.1. Overview

- 11.2.34.2. Products

- 11.2.34.3. SWOT Analysis

- 11.2.34.4. Recent Developments

- 11.2.34.5. Financials (Based on Availability)

- 11.2.35 Dompe Farmaceutici

- 11.2.35.1. Overview

- 11.2.35.2. Products

- 11.2.35.3. SWOT Analysis

- 11.2.35.4. Recent Developments

- 11.2.35.5. Financials (Based on Availability)

- 11.2.36 Dormant Projects

- 11.2.36.1. Overview

- 11.2.36.2. Products

- 11.2.36.3. SWOT Analysis

- 11.2.36.4. Recent Developments

- 11.2.36.5. Financials (Based on Availability)

- 11.2.37 Grupo Ferrer Internacional

- 11.2.37.1. Overview

- 11.2.37.2. Products

- 11.2.37.3. SWOT Analysis

- 11.2.37.4. Recent Developments

- 11.2.37.5. Financials (Based on Availability)

- 11.2.38 ID Pharma

- 11.2.38.1. Overview

- 11.2.38.2. Products

- 11.2.38.3. SWOT Analysis

- 11.2.38.4. Recent Developments

- 11.2.38.5. Financials (Based on Availability)

- 11.2.39 InFlectis BioScience

- 11.2.39.1. Overview

- 11.2.39.2. Products

- 11.2.39.3. SWOT Analysis

- 11.2.39.4. Recent Developments

- 11.2.39.5. Financials (Based on Availability)

- 11.2.40 Ionis Pharmaceuticals

- 11.2.40.1. Overview

- 11.2.40.2. Products

- 11.2.40.3. SWOT Analysis

- 11.2.40.4. Recent Developments

- 11.2.40.5. Financials (Based on Availability)

- 11.2.41 Ixchel Pharma

- 11.2.41.1. Overview

- 11.2.41.2. Products

- 11.2.41.3. SWOT Analysis

- 11.2.41.4. Recent Developments

- 11.2.41.5. Financials (Based on Availability)

- 11.2.42 Khondrion

- 11.2.42.1. Overview

- 11.2.42.2. Products

- 11.2.42.3. SWOT Analysis

- 11.2.42.4. Recent Developments

- 11.2.42.5. Financials (Based on Availability)

- 11.2.43 Mimetogen Pharmaceuticals

- 11.2.43.1. Overview

- 11.2.43.2. Products

- 11.2.43.3. SWOT Analysis

- 11.2.43.4. Recent Developments

- 11.2.43.5. Financials (Based on Availability)

- 11.2.44 Mitotech

- 11.2.44.1. Overview

- 11.2.44.2. Products

- 11.2.44.3. SWOT Analysis

- 11.2.44.4. Recent Developments

- 11.2.44.5. Financials (Based on Availability)

- 11.2.45 M's Science

- 11.2.45.1. Overview

- 11.2.45.2. Products

- 11.2.45.3. SWOT Analysis

- 11.2.45.4. Recent Developments

- 11.2.45.5. Financials (Based on Availability)

- 11.2.46 Nanovector

- 11.2.46.1. Overview

- 11.2.46.2. Products

- 11.2.46.3. SWOT Analysis

- 11.2.46.4. Recent Developments

- 11.2.46.5. Financials (Based on Availability)

- 11.2.47 SanBio

- 11.2.47.1. Overview

- 11.2.47.2. Products

- 11.2.47.3. SWOT Analysis

- 11.2.47.4. Recent Developments

- 11.2.47.5. Financials (Based on Availability)

- 11.2.1 Sanofi

List of Figures

- Figure 1: Global Ophthalmology Disorders Drug Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Ophthalmology Disorders Drug Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Ophthalmology Disorders Drug Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Ophthalmology Disorders Drug Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Ophthalmology Disorders Drug Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Ophthalmology Disorders Drug Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Ophthalmology Disorders Drug Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Ophthalmology Disorders Drug Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Ophthalmology Disorders Drug Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Ophthalmology Disorders Drug Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Ophthalmology Disorders Drug Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Ophthalmology Disorders Drug Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Ophthalmology Disorders Drug Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Ophthalmology Disorders Drug Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Ophthalmology Disorders Drug Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Ophthalmology Disorders Drug Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Ophthalmology Disorders Drug Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Ophthalmology Disorders Drug Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Ophthalmology Disorders Drug Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Ophthalmology Disorders Drug Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Ophthalmology Disorders Drug Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Ophthalmology Disorders Drug Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Ophthalmology Disorders Drug Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Ophthalmology Disorders Drug Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Ophthalmology Disorders Drug Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Ophthalmology Disorders Drug Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Ophthalmology Disorders Drug Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Ophthalmology Disorders Drug Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Ophthalmology Disorders Drug Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Ophthalmology Disorders Drug Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Ophthalmology Disorders Drug Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Ophthalmology Disorders Drug Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Ophthalmology Disorders Drug Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ophthalmology Disorders Drug?

The projected CAGR is approximately 8.51%.

2. Which companies are prominent players in the Ophthalmology Disorders Drug?

Key companies in the market include Sanofi, Bayer, Bausch + Lomb, Novartis, Usher Syndrome, Takeda Pharmaceutical, Roche, Pfizer, Allergan, Gilead Sciences, Kubota Pharmaceutical, Alkeus Pharmaceuticals, Astellas Pharma, Ferrer Corporate, Amgen Inc, Editas Medicine Inc, ProQR Therapeutics NV, ReNeuron, Amarantus BioScience, Ocugen, ReGenX Biosciences, Sucampo Pharmaceuticals, Orphagen Pharmaceuticals, Okuvision, Second Sight Medical, Acucela, Stealth BioTherapeutics, Sun Pharma Advanced Research Company, AmpliPhi Biosciences, Applied Genetic Technologies, Asklepios BioPharmaceutical, Biovista, Spark Therapeutics, Caladrius Biosciences, Dompe Farmaceutici, Dormant Projects, Grupo Ferrer Internacional, ID Pharma, InFlectis BioScience, Ionis Pharmaceuticals, Ixchel Pharma, Khondrion, Mimetogen Pharmaceuticals, Mitotech, M's Science, Nanovector, SanBio.

3. What are the main segments of the Ophthalmology Disorders Drug?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 41.39 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ophthalmology Disorders Drug," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ophthalmology Disorders Drug report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ophthalmology Disorders Drug?

To stay informed about further developments, trends, and reports in the Ophthalmology Disorders Drug, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence