Key Insights

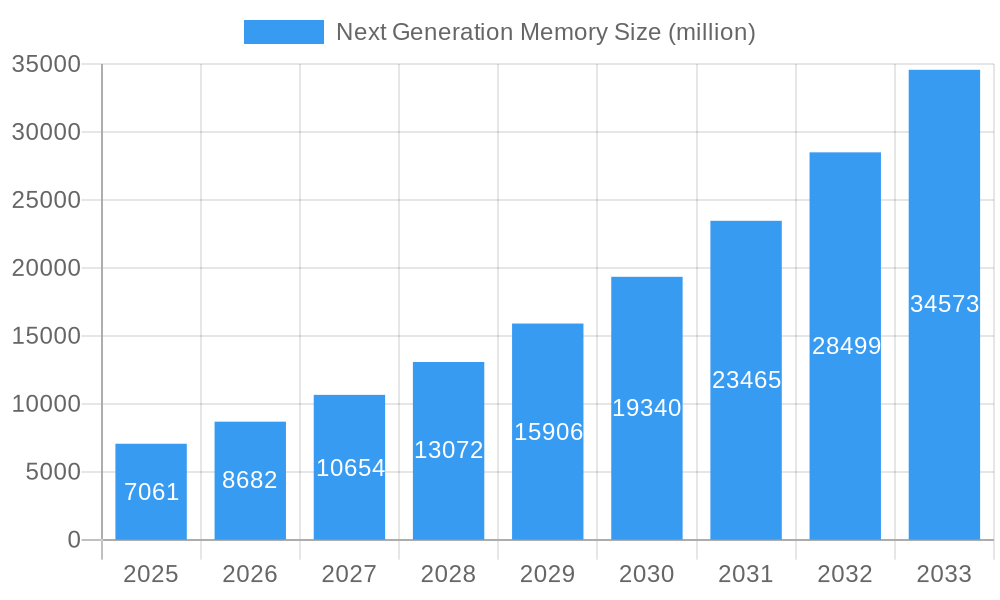

The Next Generation Memory market is projected for significant expansion, anticipating a market size of $15.1 billion by 2025. This growth is underpinned by a robust CAGR of 24.5% from the base year 2025 through 2033. Key drivers include escalating demand for enhanced performance, greater storage density, and reduced power consumption across diverse and expanding applications. Consumer electronics, notably smartphones, wearables, and gaming consoles, are a major contributor, requiring accelerated data access and processing. Concurrently, the enterprise storage sector is undergoing a transformation, with businesses demanding more efficient memory for cloud computing, big data analytics, and AI. The automotive sector's adoption of autonomous driving and advanced infotainment systems also boosts the need for specialized, high-endurance memory. Furthermore, the expansion of telecommunications, including 5G and IoT networks, necessitates memory solutions capable of managing high-volume data streams with minimal latency.

Next Generation Memory Market Size (In Billion)

Innovative memory technologies such as PCM, ReRAM, and MRAM are leading this paradigm shift, offering superior alternatives to conventional NAND and DRAM. These advancements promise improved speed, endurance, and energy efficiency, enabling novel device architectures and capabilities. Potential challenges may include substantial R&D and manufacturing costs for these advanced technologies, alongside the necessity for broad ecosystem development and standardization. Nevertheless, continuous innovation, strategic partnerships, and increased investment are anticipated to mitigate these obstacles, cementing the pivotal role of Next Generation Memory in future digital infrastructure and electronic devices.

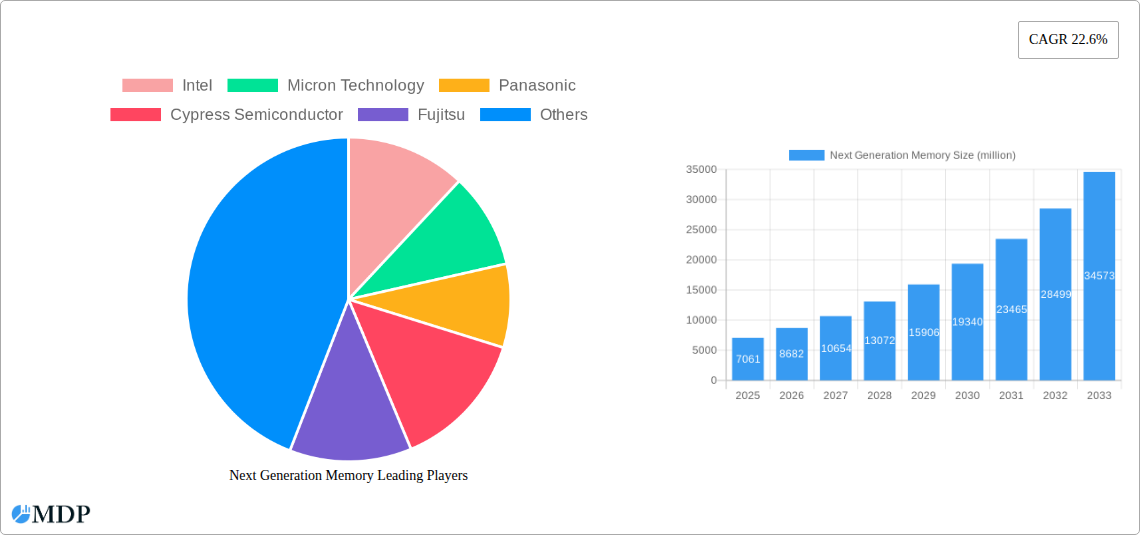

Next Generation Memory Company Market Share

Next Generation Memory Market: Comprehensive Analysis and Forecast (2019–2033)

This in-depth market report provides an exhaustive analysis of the global Next Generation Memory market, meticulously examining key trends, growth drivers, and competitive landscapes from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this report offers invaluable insights for industry stakeholders seeking to capitalize on the burgeoning demand for advanced memory solutions. We explore the dynamic interplay of technological innovation, evolving end-user needs, and strategic market maneuvers that are shaping the future of memory technology, offering actionable intelligence and data-driven forecasts.

Next Generation Memory Market Dynamics & Concentration

The Next Generation Memory market is characterized by a moderate to high concentration, driven by significant R&D investments and the complex manufacturing processes involved. Key innovation drivers include the persistent demand for higher density, increased speed, and enhanced energy efficiency across a multitude of applications. Regulatory frameworks are gradually evolving to accommodate the advancements in semiconductor technology, particularly concerning data security and privacy. Product substitutes, while present, are often outperformed by next-generation memory in terms of performance metrics. End-user trends are heavily influenced by the proliferation of AI, IoT, and edge computing, all of which require robust and efficient memory solutions. Mergers and acquisitions (M&A) activities, while not as frequent as in more mature markets, are strategically important for companies looking to consolidate intellectual property and expand their market reach. For instance, recent M&A deals have seen established players acquire smaller, innovative firms to integrate novel memory technologies. The market share distribution indicates a competitive landscape where established semiconductor giants and specialized memory developers vie for dominance. Expected M&A deal counts are projected to be in the tens over the forecast period, signaling continued consolidation and strategic realignments.

Next Generation Memory Industry Trends & Analysis

The global Next Generation Memory market is poised for substantial expansion, with an estimated Compound Annual Growth Rate (CAGR) of approximately 25% from 2025 to 2033. This robust growth is propelled by a confluence of factors, including the insatiable demand for faster and more energy-efficient data storage and processing capabilities, fueled by the exponential rise of data generation across diverse sectors. Technological disruptions are at the forefront, with advancements in materials science and fabrication techniques enabling the development of memory technologies like Phase-Change Memory (PCM), Resistive Random-Access Memory (ReRAM), Magnetoresistive Random-Access Memory (MRAM), and Ferroelectric Random-Access Memory (FeRAM) to overcome the limitations of traditional DRAM and NAND flash. Consumer preferences are increasingly leaning towards devices with enhanced performance and longer battery life, directly benefiting the adoption of next-generation memory solutions in smartphones, wearables, and high-performance computing devices. The competitive dynamics within the industry are intensifying, with key players like Intel, Micron Technology, Panasonic, and Cypress Semiconductor investing heavily in research and development to gain a competitive edge. Furthermore, the growing penetration of technologies like Artificial Intelligence (AI), Internet of Things (IoT), and edge computing necessitates advanced memory architectures that can handle massive datasets with low latency and power consumption, thereby driving market adoption. The increasing integration of these technologies into automotive systems for autonomous driving and advanced driver-assistance systems (ADAS), as well as in enterprise storage solutions for big data analytics and cloud computing, further underscores the significant growth trajectory of the next-generation memory market. The projected market penetration of these advanced memory types is expected to rise from an estimated 15% in 2025 to over 40% by 2033.

Leading Markets & Segments in Next Generation Memory

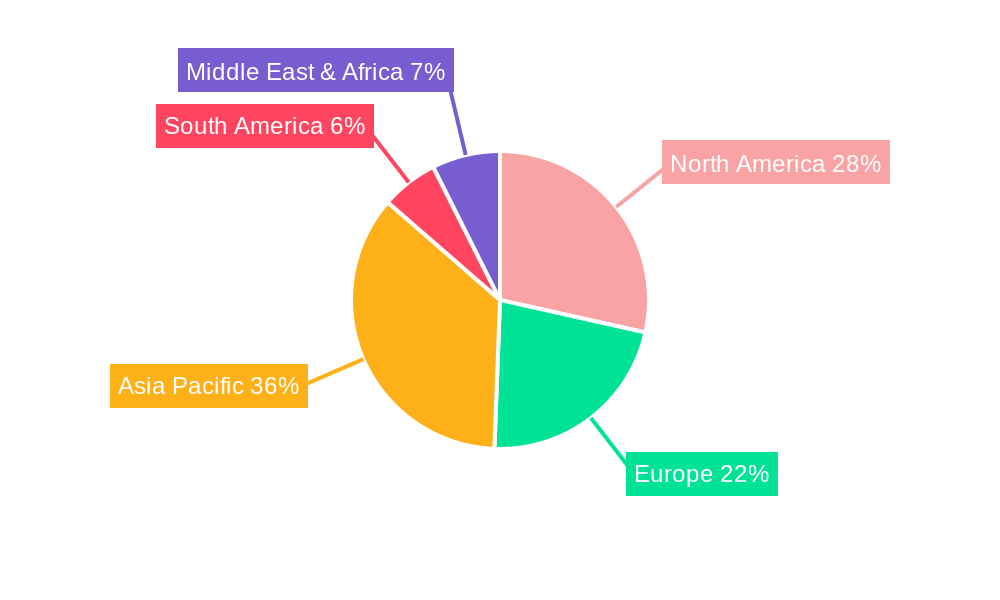

The dominance within the Next Generation Memory market is multifaceted, with specific regions and application segments exhibiting significant traction. North America, particularly the United States, is a leading market, driven by its strong presence in semiconductor research and development, substantial government funding for technological innovation, and the high concentration of leading technology companies. Economic policies that favor R&D tax credits and intellectual property protection further bolster this leadership. Within the application segments, Consumer Electronics is a major driver, accounting for an estimated 30% of the market share in 2025. The ever-increasing demand for faster, more powerful, and energy-efficient smartphones, tablets, laptops, and gaming consoles directly fuels the adoption of next-generation memory. Key drivers in this segment include the relentless pursuit of thinner and lighter devices, longer battery life, and immersive user experiences.

Following closely, Enterprise Storage represents another critical segment, expected to capture approximately 25% of the market share. The explosion of big data, coupled with the rise of cloud computing and data analytics, necessitates high-speed, high-density, and non-volatile memory solutions for servers, data centers, and storage arrays. Economic policies supporting digital transformation and infrastructure upgrades within businesses are significant contributors.

The Automotive and Transportation segment is experiencing rapid growth, driven by the increasing sophistication of in-car electronics, the development of autonomous driving technologies, and the integration of advanced infotainment systems. This segment is projected to hold around 18% of the market share. The strict safety and reliability requirements, coupled with the need for high-performance processing in real-time applications, make next-generation memory indispensable.

Telecommunications is another vital application, with an estimated 15% market share. The rollout of 5G networks and the expansion of data infrastructure demand memory solutions that can handle massive data throughput and low latency for base stations, routers, and network equipment.

The Military and Aerospace segment, while smaller at approximately 7% market share, represents a high-value market due to the stringent reliability, durability, and performance requirements for defense systems, avionics, and space exploration. The "Others" segment, encompassing industrial automation, medical devices, and emerging IoT applications, accounts for the remaining 5%.

In terms of memory type, MRAM is anticipated to lead in market penetration and growth, driven by its combination of speed, endurance, and non-volatility, making it ideal for embedded systems, cache memory, and data logging applications. ReRAM and PCM are also poised for significant growth due to their potential for high density and low power consumption. FeRAM, while niche, holds promise in specific applications requiring high speed and low power.

Next Generation Memory Product Developments

Next-generation memory technologies are marked by rapid product innovation, focusing on delivering superior performance, enhanced energy efficiency, and increased storage density. Companies are developing MRAM solutions with improved speeds and larger capacities for embedded applications and as a replacement for SRAM in high-performance computing. ReRAM and PCM are seeing advancements in their ability to offer non-volatility with DRAM-like speeds, making them attractive for emerging computing architectures and AI accelerators. Innovations in material science and device architecture are enabling these technologies to achieve competitive advantages in terms of endurance, data retention, and cost-effectiveness, positioning them as key enablers for future electronic devices and systems.

Key Drivers of Next Generation Memory Growth

The growth of the Next Generation Memory market is primarily driven by several interconnected factors. Technologically, the insatiable demand for faster data processing, higher storage densities, and reduced power consumption across all electronic devices is paramount. The proliferation of Artificial Intelligence (AI), Machine Learning (ML), and the Internet of Things (IoT) necessitates memory solutions that can handle massive data volumes with low latency. Economically, the increasing digitalization of industries and the expansion of cloud computing infrastructure create a sustained demand for advanced storage and memory. Regulatory factors, such as data privacy laws and the increasing focus on energy efficiency standards for electronic devices, also indirectly support the adoption of next-generation memory technologies that offer better performance per watt.

Challenges in the Next Generation Memory Market

Despite the promising outlook, the Next Generation Memory market faces several challenges. High manufacturing costs associated with developing and scaling new fabrication processes remain a significant barrier. Intense competition from established memory technologies like DRAM and NAND flash, which have benefited from decades of optimization and economies of scale, poses a persistent threat. Supply chain complexities and the need for specialized materials and equipment can also lead to production bottlenecks and increased lead times. Furthermore, the long qualification cycles required for adoption in critical applications like automotive and aerospace can slow down market penetration. Regulatory hurdles concerning the environmental impact of manufacturing and the disposal of electronic waste also require careful consideration and innovative solutions.

Emerging Opportunities in Next Generation Memory

Catalysts for long-term growth in the Next Generation Memory market are abundant, driven by continuous technological breakthroughs and evolving market demands. The convergence of AI and edge computing presents a significant opportunity for embedded non-volatile memory solutions that can perform computations directly at the data source. Strategic partnerships between memory manufacturers and semiconductor foundries are crucial for accelerating innovation and reducing time-to-market. Furthermore, the growing demand for specialized memory in emerging fields like quantum computing and neuromorphic computing opens up entirely new avenues for application and market expansion. The increasing focus on sustainable electronics also provides an opportunity for next-generation memory technologies that offer superior energy efficiency.

Leading Players in the Next Generation Memory Sector

Intel Micron Technology Panasonic Cypress Semiconductor Fujitsu Everspin ROHM Semiconductor Adesto Technologies Crossbar

Key Milestones in Next Generation Memory Industry

- 2019: Launch of advanced MRAM products with enhanced speed and endurance for embedded applications.

- 2020: Significant investments in R&D for next-generation memory by major semiconductor companies.

- 2021: Increased adoption of PCM and ReRAM in niche high-performance computing applications.

- 2022: Development of new materials and fabrication techniques to improve ReRAM density and reliability.

- 2023: Growing interest and initial product development for FeRAM in low-power IoT devices.

- 2024: Announcements of strategic collaborations to accelerate the commercialization of next-generation memory.

Strategic Outlook for Next Generation Memory Market

The strategic outlook for the Next Generation Memory market is exceptionally positive, driven by an accelerating pace of innovation and the escalating demands of emerging technologies. Growth accelerators include the continuous refinement of MRAM, ReRAM, and PCM technologies to achieve higher densities, faster speeds, and improved energy efficiency, making them indispensable for AI, edge computing, and 5G infrastructure. Strategic opportunities lie in forging deeper collaborations between chip designers, device manufacturers, and end-users to co-create tailored memory solutions for specific applications, thereby shortening development cycles and increasing market penetration. The ongoing global push towards digitalization and advanced analytics will continue to fuel demand, solidifying the position of next-generation memory as a cornerstone of future technological advancements.

Next Generation Memory Segmentation

-

1. Application

- 1.1. Consumer Electronics

- 1.2. Enterprise Storage

- 1.3. Automotive and Transportation

- 1.4. Military and Aerospace

- 1.5. Telecommunications

- 1.6. Others

-

2. Type

- 2.1. PCM

- 2.2. ReRAM

- 2.3. MRAM

- 2.4. FeRAM

Next Generation Memory Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Next Generation Memory Regional Market Share

Geographic Coverage of Next Generation Memory

Next Generation Memory REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 24.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Next Generation Memory Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Consumer Electronics

- 5.1.2. Enterprise Storage

- 5.1.3. Automotive and Transportation

- 5.1.4. Military and Aerospace

- 5.1.5. Telecommunications

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. PCM

- 5.2.2. ReRAM

- 5.2.3. MRAM

- 5.2.4. FeRAM

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Next Generation Memory Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Consumer Electronics

- 6.1.2. Enterprise Storage

- 6.1.3. Automotive and Transportation

- 6.1.4. Military and Aerospace

- 6.1.5. Telecommunications

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. PCM

- 6.2.2. ReRAM

- 6.2.3. MRAM

- 6.2.4. FeRAM

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Next Generation Memory Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Consumer Electronics

- 7.1.2. Enterprise Storage

- 7.1.3. Automotive and Transportation

- 7.1.4. Military and Aerospace

- 7.1.5. Telecommunications

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. PCM

- 7.2.2. ReRAM

- 7.2.3. MRAM

- 7.2.4. FeRAM

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Next Generation Memory Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Consumer Electronics

- 8.1.2. Enterprise Storage

- 8.1.3. Automotive and Transportation

- 8.1.4. Military and Aerospace

- 8.1.5. Telecommunications

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. PCM

- 8.2.2. ReRAM

- 8.2.3. MRAM

- 8.2.4. FeRAM

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Next Generation Memory Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Consumer Electronics

- 9.1.2. Enterprise Storage

- 9.1.3. Automotive and Transportation

- 9.1.4. Military and Aerospace

- 9.1.5. Telecommunications

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. PCM

- 9.2.2. ReRAM

- 9.2.3. MRAM

- 9.2.4. FeRAM

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Next Generation Memory Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Consumer Electronics

- 10.1.2. Enterprise Storage

- 10.1.3. Automotive and Transportation

- 10.1.4. Military and Aerospace

- 10.1.5. Telecommunications

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. PCM

- 10.2.2. ReRAM

- 10.2.3. MRAM

- 10.2.4. FeRAM

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Intel

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Micron Technology

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Panasonic

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Cypress Semiconductor

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Fujitsu

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Everspin

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ROHM Semiconductor

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Adesto Technologies

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Crossbar

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Intel

List of Figures

- Figure 1: Global Next Generation Memory Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Next Generation Memory Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Next Generation Memory Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Next Generation Memory Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Next Generation Memory Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Next Generation Memory Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Next Generation Memory Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Next Generation Memory Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Next Generation Memory Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Next Generation Memory Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Next Generation Memory Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Next Generation Memory Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Next Generation Memory Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Next Generation Memory Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Next Generation Memory Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Next Generation Memory Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Next Generation Memory Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Next Generation Memory Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Next Generation Memory Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Next Generation Memory Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Next Generation Memory Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Next Generation Memory Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Next Generation Memory Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Next Generation Memory Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Next Generation Memory Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Next Generation Memory Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Next Generation Memory Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Next Generation Memory Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Next Generation Memory Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Next Generation Memory Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Next Generation Memory Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Next Generation Memory Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Next Generation Memory Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Next Generation Memory Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Next Generation Memory Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Next Generation Memory Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Next Generation Memory Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Next Generation Memory Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Next Generation Memory Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Next Generation Memory Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Next Generation Memory Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Next Generation Memory Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Next Generation Memory Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Next Generation Memory Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Next Generation Memory Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Next Generation Memory Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Next Generation Memory Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Next Generation Memory Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Next Generation Memory Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Next Generation Memory Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Next Generation Memory?

The projected CAGR is approximately 24.5%.

2. Which companies are prominent players in the Next Generation Memory?

Key companies in the market include Intel, Micron Technology, Panasonic, Cypress Semiconductor, Fujitsu, Everspin, ROHM Semiconductor, Adesto Technologies, Crossbar.

3. What are the main segments of the Next Generation Memory?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.1 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Next Generation Memory," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Next Generation Memory report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Next Generation Memory?

To stay informed about further developments, trends, and reports in the Next Generation Memory, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence