Key Insights

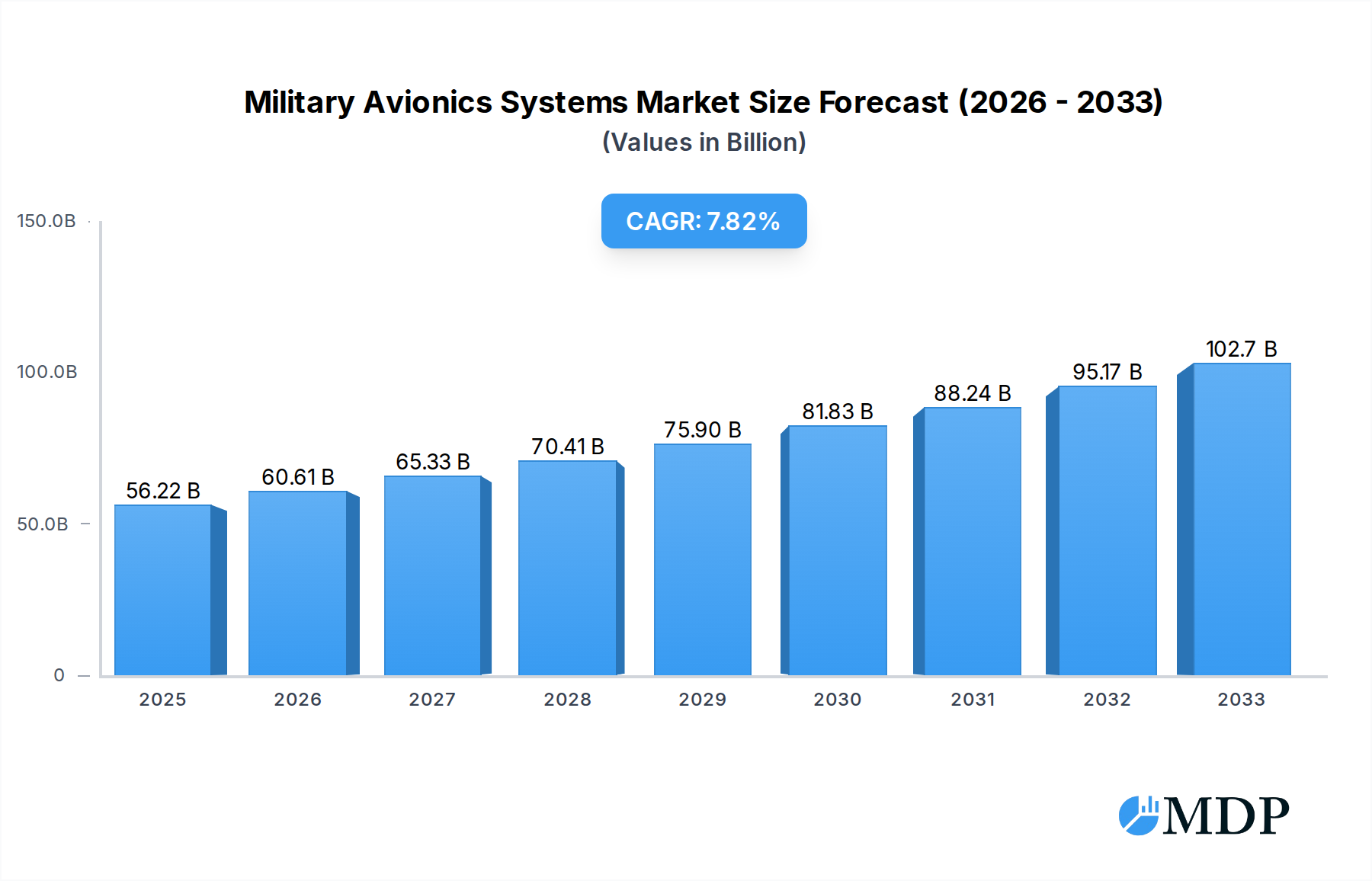

The global Military Avionics Systems market is poised for robust expansion, projected to reach USD 56.22 billion in 2025 and exhibiting a compelling Compound Annual Growth Rate (CAGR) of 7.9%. This significant growth is fueled by the escalating demand for advanced defense capabilities, driven by geopolitical complexities and the continuous need for enhanced situational awareness, precision targeting, and secure communication in modern warfare. Key applications such as defense operations, search and rescue missions, and intelligence, surveillance, and reconnaissance (ISR) are witnessing substantial investment, necessitating sophisticated avionics solutions. The market is further propelled by the integration of cutting-edge technologies like artificial intelligence (AI), machine learning, and advanced sensor fusion to improve aircraft performance, survivability, and mission effectiveness.

Military Avionics Systems Market Size (In Billion)

The evolving threat landscape and the increasing adoption of unmanned aerial systems (UAS) are significant drivers. Companies are heavily investing in research and development to introduce next-generation avionics, including highly integrated displays, advanced weapons systems, sophisticated navigation and communication modules, and robust electronic warfare systems. While the market benefits from these technological advancements and strategic imperatives, it also faces challenges such as high development and integration costs, stringent regulatory compliance, and the need for continuous software updates to counter evolving cyber threats. The forecast period, from 2025 to 2033, is expected to witness a sustained upward trajectory, underscoring the critical role of military avionics in national security and defense modernization efforts worldwide.

Military Avionics Systems Company Market Share

Military Avionics Systems Market: Comprehensive Report Description

This in-depth report delivers a critical analysis of the global Military Avionics Systems Market, a sector projected to reach trillions in valuation. Covering the Study Period (2019–2033), with a Base Year of 2025 and Forecast Period (2025–2033), this comprehensive study provides actionable intelligence for defense contractors, government agencies, and technology providers. Leveraging high-traffic keywords such as "military avionics," "defense electronics," "aerospace technology," "combat aircraft systems," and "ISR platforms," this report ensures maximum search visibility and attracts key industry stakeholders.

Military Avionics Systems Market Dynamics & Concentration

The Military Avionics Systems Market exhibits a dynamic landscape characterized by substantial market concentration and rapid innovation. The market share is significantly held by a few dominant players, including Honeywell, Rockwell Collins, and BAE Systems Plc, which collectively command an estimated xx% of the global market. Innovation drivers are predominantly fueled by the escalating demand for advanced Electronic Warfare Systems, enhanced Navigation Systems, and sophisticated Sensors to maintain battlefield superiority. Regulatory frameworks, primarily driven by defense spending policies and international security agreements, play a crucial role in shaping market entry and product development. Product substitutes, while emerging, are largely confined to niche applications and have yet to pose a significant threat to established integrated avionics solutions. End-user trends are heavily influenced by the need for modular, upgradeable systems that can adapt to evolving threats, leading to increased investments in open architecture designs. Mergers and Acquisitions (M&A) activities have been consistent, with an estimated xx M&A deals in the historical period, aimed at consolidating capabilities and expanding market reach. Prominent M&A activities include the integration of L-3 Avionics Systems into GE Aviation, strengthening their portfolio in critical defense electronics. The market is characterized by intense competition, with companies like Raytheon Company and Thales Group continuously investing in R&D to maintain their competitive edge.

Military Avionics Systems Industry Trends & Analysis

The Military Avionics Systems Industry is poised for significant growth, driven by a confluence of technological advancements, evolving geopolitical landscapes, and increasing defense budgets worldwide. The projected Compound Annual Growth Rate (CAGR) for the forecast period is an impressive xx%, indicating a robust expansion of the market. Market penetration of advanced digital avionics is steadily increasing, replacing legacy analog systems with sophisticated digital solutions that offer enhanced performance, reliability, and maintainability. Key growth drivers include the relentless pursuit of enhanced situational awareness for aircrews, the integration of artificial intelligence (AI) and machine learning (ML) for improved data processing and decision-making, and the growing adoption of networked avionics for seamless communication and data sharing across platforms. The demand for lighter, more power-efficient avionics components is also a significant trend, driven by the desire to improve aircraft performance and extend operational range. Technological disruptions are largely centered around the development of next-generation sensors, advanced radar systems, and cutting-edge electronic warfare capabilities. Consumer preferences, in this context, are defined by military end-users’ requirements for interoperability, cybersecurity, and the ability to integrate new technologies rapidly. Competitive dynamics are intense, with leading players like Honeywell, Rockwell Collins, and Raytheon Company vying for lucrative defense contracts. The industry is witnessing a rise in collaborative efforts between established defense giants and specialized technology firms, such as VPT, Inc. and ENSCO Avionics, to co-develop innovative solutions. The trend towards modular avionics architectures is also a significant factor, allowing for easier upgrades and customization of airborne systems. The ongoing modernization of air forces globally, coupled with the development of new combat aircraft and unmanned aerial vehicles (UAVs), further propels the demand for sophisticated military avionics. The increasing focus on electronic warfare capabilities, driven by the need to counter advanced adversary threats, is also a major contributor to market expansion. The global market size is estimated to be in the trillions, with significant contributions from North America and Europe.

Leading Markets & Segments in Military Avionics Systems

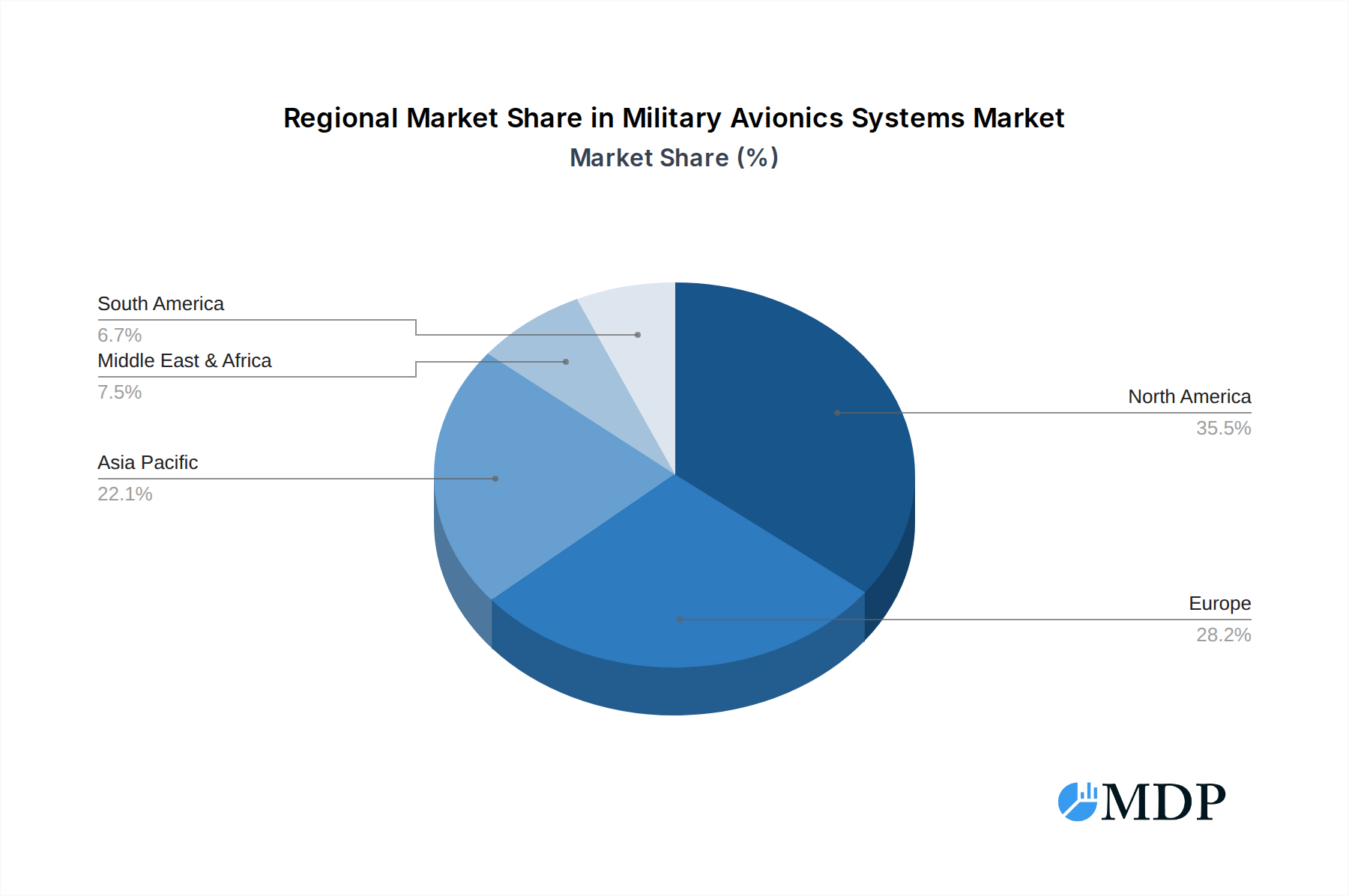

The Military Avionics Systems Market is dominated by the Defense Application, accounting for an estimated xx% of the overall market share. Within the Defense segment, key sub-segments driving growth include Navigation Systems, Communications, and Sensors, each critical for modern aerial warfare and intelligence gathering. The primary geographical market exhibiting leadership is North America, driven by substantial defense expenditures from the United States and Canada, coupled with a strong emphasis on technological innovation.

Dominant Region: North America

- Economic Policies: Robust government defense budgets and strategic geopolitical priorities in North America create a fertile ground for the adoption of advanced military avionics.

- Technological Hubs: The presence of leading aerospace and defense companies in the region fosters continuous innovation and rapid product development.

- Military Modernization Programs: Ongoing modernization initiatives for fighter jets, bombers, and surveillance aircraft necessitate upgrades and replacements of existing avionics systems.

Dominant Segment: Defense Application

- High-Demand Systems: Within the Defense application, Navigation Systems are crucial for precise targeting and mission execution in complex environments, with the market size reaching billions. Communications systems are essential for maintaining battlefield connectivity, and the demand for secure and high-bandwidth solutions is soaring, contributing billions to the market. Sensors, including radar, infrared, and electronic intelligence systems, are vital for reconnaissance and situational awareness, generating billions in revenue. Electronic Warfare Systems are increasingly critical to counter advanced threats, representing a rapidly growing segment valued in billions.

- Technological Advancement: Investments in AI and machine learning for improved data fusion and threat detection within defense platforms are significant growth accelerators.

- Threat Landscape: Evolving global threats necessitate constant upgrades and the development of sophisticated avionics to maintain a strategic advantage.

Dominant Type: Displays

- Enhanced Situational Awareness: Modern Displays in military aircraft are evolving from simple indicators to complex, multi-functional cockpit interfaces providing pilots with comprehensive situational awareness, driving market values into billions.

- Human-Machine Interface: Advancements in touch-screen technology, augmented reality overlays, and intuitive graphical user interfaces are enhancing pilot effectiveness and reducing cognitive load.

- Integration with Other Systems: Displays are increasingly integrated with Sensors, Navigation Systems, and Weapons Systems, providing a unified operational picture.

Emerging Segments

- Unmanned Aerial Vehicle (UAV) Avionics: The rapid growth of drone technology is creating a significant demand for specialized avionics solutions tailored for unmanned platforms, with market potential in billions.

- Cybersecurity in Avionics: As systems become more networked, the demand for robust cybersecurity solutions to protect critical avionics from cyber threats is paramount, representing a growing segment valued in billions.

Military Avionics Systems Product Developments

Recent product developments in Military Avionics Systems focus on enhanced processing power, reduced form factors, and improved interoperability. Innovations in solid-state data recorders, advanced radar processing units, and integrated cockpit displays are key. Companies are emphasizing the development of software-defined avionics that allow for rapid updates and adaptation to new mission requirements. The integration of AI for predictive maintenance and autonomous flight capabilities are also at the forefront. These developments provide competitive advantages by increasing mission effectiveness, reducing operational costs, and enhancing pilot safety in demanding military environments.

Key Drivers of Military Avionics Systems Growth

The growth of the Military Avionics Systems Market is propelled by several interconnected factors. Firstly, escalating geopolitical tensions and the need for advanced defense capabilities globally drive increased military spending, leading to modernization programs that heavily rely on sophisticated avionics. Secondly, rapid technological advancements in areas like AI, sensor fusion, and advanced communication systems enable the development of more capable and efficient avionics solutions. Thirdly, the growing demand for unmanned aerial systems (UAS) and the subsequent integration of their avionics into broader military networks is a significant catalyst. Finally, the increasing emphasis on electronic warfare and cyber defense capabilities necessitates the development and deployment of advanced electronic warfare avionics and secure communication systems, valued in billions.

Challenges in the Military Avionics Systems Market

Despite robust growth, the Military Avionics Systems Market faces several challenges. High research and development costs, coupled with stringent regulatory approval processes for military-grade hardware and software, can significantly prolong product lifecycles and increase expenditure, running into billions. Supply chain disruptions, particularly for specialized electronic components, pose a constant threat to timely production and delivery. The cybersecurity landscape presents an ongoing challenge, with the need for increasingly robust defenses against sophisticated cyber threats, requiring continuous investment in security solutions. Furthermore, the limited number of qualified personnel with specialized avionics expertise can create bottlenecks in development and maintenance. The transition to open-architecture systems also presents integration challenges with legacy platforms, requiring substantial investment.

Emerging Opportunities in Military Avionics Systems

The Military Avionics Systems Market is ripe with emerging opportunities driven by technological breakthroughs and evolving defense strategies. The burgeoning field of directed energy weapons necessitates the development of advanced avionics for targeting and control, opening new market avenues. The increasing adoption of AI and machine learning for autonomous operations and intelligent data processing presents significant growth potential, with billions invested in R&D. Strategic partnerships between established defense contractors and innovative technology startups are fostering the development of next-generation avionics solutions. Furthermore, the expansion of military operations in contested domains, such as cyber and electronic warfare, is creating a sustained demand for specialized avionics designed to counter emerging threats, representing a market valued in billions. The growing emphasis on space-based avionics for advanced reconnaissance and communication also offers a promising frontier.

Leading Players in the Military Avionics Systems Sector

- Avidyne

- GE Aviation

- Honeywell

- Rockwell Collins

- Thales Group

- Tel-Instrument

- VPT, Inc.

- Aspen Avionics

- Curtiss-Wright

- Elbit Systems

- ENSCO Avionics

- ForeFlight

- L-3 Avionics Systems

- Sagetech

- Xavion

- ZG Optique

- Zodiac Aerospace

- ARINC Incorporated

- BAE Systems Plc

- Boeing Military Aircraft

- Russion Aircraft Corporation MiG

- Raytheon Company

- Embraer SA

Key Milestones in Military Avionics Systems Industry

- 2019: Introduction of advanced sensor fusion technologies in fighter jet avionics, enhancing pilot situational awareness.

- 2020: Increased investment in AI-driven predictive maintenance for military aircraft avionics, leading to reduced downtime and cost savings.

- 2021: Significant advancements in secure communication avionics for unmanned aerial vehicles (UAVs), enabling longer-range and more reliable command and control.

- 2022: Development of next-generation cockpit displays incorporating augmented reality overlays for improved tactical information dissemination.

- 2023: Key acquisitions and mergers aimed at consolidating expertise in electronic warfare avionics to counter emerging threats.

- 2024: Launch of new modular avionics architectures designed for rapid upgrades and interoperability across diverse military platforms.

- 2025 (Estimated): Expected integration of advanced AI algorithms for autonomous decision-making in combat scenarios within advanced military aircraft.

- 2026 (Estimated): Rollout of enhanced cybersecurity solutions for military avionics to safeguard against sophisticated cyberattacks.

- 2027 (Estimated): Introduction of novel sensor technologies for enhanced multi-spectral intelligence gathering capabilities.

- 2028 (Estimated): Advancements in software-defined radio avionics for greater flexibility in communication spectrum management.

- 2029 (Estimated): Increased adoption of radiation-hardened components for space-based military avionics.

- 2030 (Estimated): Emergence of integrated avionics solutions for hypersonic weapon platforms.

- 2031 (Estimated): Development of advanced pilot-assist systems leveraging machine learning for complex flight maneuvers.

- 2032 (Estimated): Expansion of avionics capabilities for long-endurance unmanned maritime patrol aircraft.

- 2033 (Estimated): Further integration of quantum computing principles for advanced data processing in future military avionics.

Strategic Outlook for Military Avionics Systems Market

The strategic outlook for the Military Avionics Systems Market is overwhelmingly positive, characterized by continuous innovation and sustained demand from defense sectors worldwide. Growth accelerators include the ongoing global arms race, necessitating advanced technological superiority, and the rapid proliferation of unmanned systems, requiring sophisticated avionics integration. The increasing focus on networked warfare and the need for seamless data sharing across all domains will further drive the adoption of advanced communication and sensor avionics. Strategic opportunities lie in the development of open-architecture systems that facilitate rapid upgrades and adaptability, as well as in leveraging AI and machine learning to enhance mission effectiveness and reduce pilot workload. Companies that can effectively navigate the complex regulatory landscape and demonstrate robust cybersecurity capabilities will be best positioned for long-term success in this multi-trillion-dollar market.

Military Avionics Systems Segmentation

-

1. Application

- 1.1. Defense

- 1.2. Search

- 1.3. Rescue

-

2. Type

- 2.1. Displays

- 2.2. Weapons Systems

- 2.3. Navigation Systems

- 2.4. Sensors

- 2.5. Communications

- 2.6. Electronic Warfare Systems

- 2.7. Others

Military Avionics Systems Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Military Avionics Systems Regional Market Share

Geographic Coverage of Military Avionics Systems

Military Avionics Systems REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Military Avionics Systems Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Defense

- 5.1.2. Search

- 5.1.3. Rescue

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Displays

- 5.2.2. Weapons Systems

- 5.2.3. Navigation Systems

- 5.2.4. Sensors

- 5.2.5. Communications

- 5.2.6. Electronic Warfare Systems

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Military Avionics Systems Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Defense

- 6.1.2. Search

- 6.1.3. Rescue

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Displays

- 6.2.2. Weapons Systems

- 6.2.3. Navigation Systems

- 6.2.4. Sensors

- 6.2.5. Communications

- 6.2.6. Electronic Warfare Systems

- 6.2.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Military Avionics Systems Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Defense

- 7.1.2. Search

- 7.1.3. Rescue

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Displays

- 7.2.2. Weapons Systems

- 7.2.3. Navigation Systems

- 7.2.4. Sensors

- 7.2.5. Communications

- 7.2.6. Electronic Warfare Systems

- 7.2.7. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Military Avionics Systems Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Defense

- 8.1.2. Search

- 8.1.3. Rescue

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Displays

- 8.2.2. Weapons Systems

- 8.2.3. Navigation Systems

- 8.2.4. Sensors

- 8.2.5. Communications

- 8.2.6. Electronic Warfare Systems

- 8.2.7. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Military Avionics Systems Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Defense

- 9.1.2. Search

- 9.1.3. Rescue

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Displays

- 9.2.2. Weapons Systems

- 9.2.3. Navigation Systems

- 9.2.4. Sensors

- 9.2.5. Communications

- 9.2.6. Electronic Warfare Systems

- 9.2.7. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Military Avionics Systems Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Defense

- 10.1.2. Search

- 10.1.3. Rescue

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Displays

- 10.2.2. Weapons Systems

- 10.2.3. Navigation Systems

- 10.2.4. Sensors

- 10.2.5. Communications

- 10.2.6. Electronic Warfare Systems

- 10.2.7. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Avidyne

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 GE Aviation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Honeywell

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Rockwell Collins

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Thales Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Tel-Instrument

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 VPT Inc.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Aspen Avionics

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Curtiss-Wright

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Elbit Systems

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 ENSCO Avionics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 ForeFlight

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 L-3 Avionics Systems

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Sagetech

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Xavion

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 ZG Optique

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Zodiac Aerospace

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 ARINC Incorporated

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 BAE Systems Plc

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Boeing Military Aircraft

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Russion Aircraft Corporation MiG

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Raytheon Company

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Embraer SA

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.1 Avidyne

List of Figures

- Figure 1: Global Military Avionics Systems Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Military Avionics Systems Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Military Avionics Systems Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Military Avionics Systems Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Military Avionics Systems Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Military Avionics Systems Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Military Avionics Systems Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Military Avionics Systems Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Military Avionics Systems Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Military Avionics Systems Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Military Avionics Systems Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Military Avionics Systems Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Military Avionics Systems Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Military Avionics Systems Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Military Avionics Systems Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Military Avionics Systems Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Military Avionics Systems Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Military Avionics Systems Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Military Avionics Systems Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Military Avionics Systems Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Military Avionics Systems Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Military Avionics Systems Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Military Avionics Systems Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Military Avionics Systems Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Military Avionics Systems Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Military Avionics Systems Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Military Avionics Systems Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Military Avionics Systems Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Military Avionics Systems Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Military Avionics Systems Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Military Avionics Systems Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Military Avionics Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Military Avionics Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Military Avionics Systems Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Military Avionics Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Military Avionics Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Military Avionics Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Military Avionics Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Military Avionics Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Military Avionics Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Military Avionics Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Military Avionics Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Military Avionics Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Military Avionics Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Military Avionics Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Military Avionics Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Military Avionics Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Military Avionics Systems Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Military Avionics Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Military Avionics Systems Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Military Avionics Systems?

The projected CAGR is approximately 7.9%.

2. Which companies are prominent players in the Military Avionics Systems?

Key companies in the market include Avidyne, GE Aviation, Honeywell, Rockwell Collins, Thales Group, Tel-Instrument, VPT, Inc., Aspen Avionics, Curtiss-Wright, Elbit Systems, ENSCO Avionics, ForeFlight, L-3 Avionics Systems, Sagetech, Xavion, ZG Optique, Zodiac Aerospace, ARINC Incorporated, BAE Systems Plc, Boeing Military Aircraft, Russion Aircraft Corporation MiG, Raytheon Company, Embraer SA.

3. What are the main segments of the Military Avionics Systems?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Military Avionics Systems," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Military Avionics Systems report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Military Avionics Systems?

To stay informed about further developments, trends, and reports in the Military Avionics Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence