Key Insights

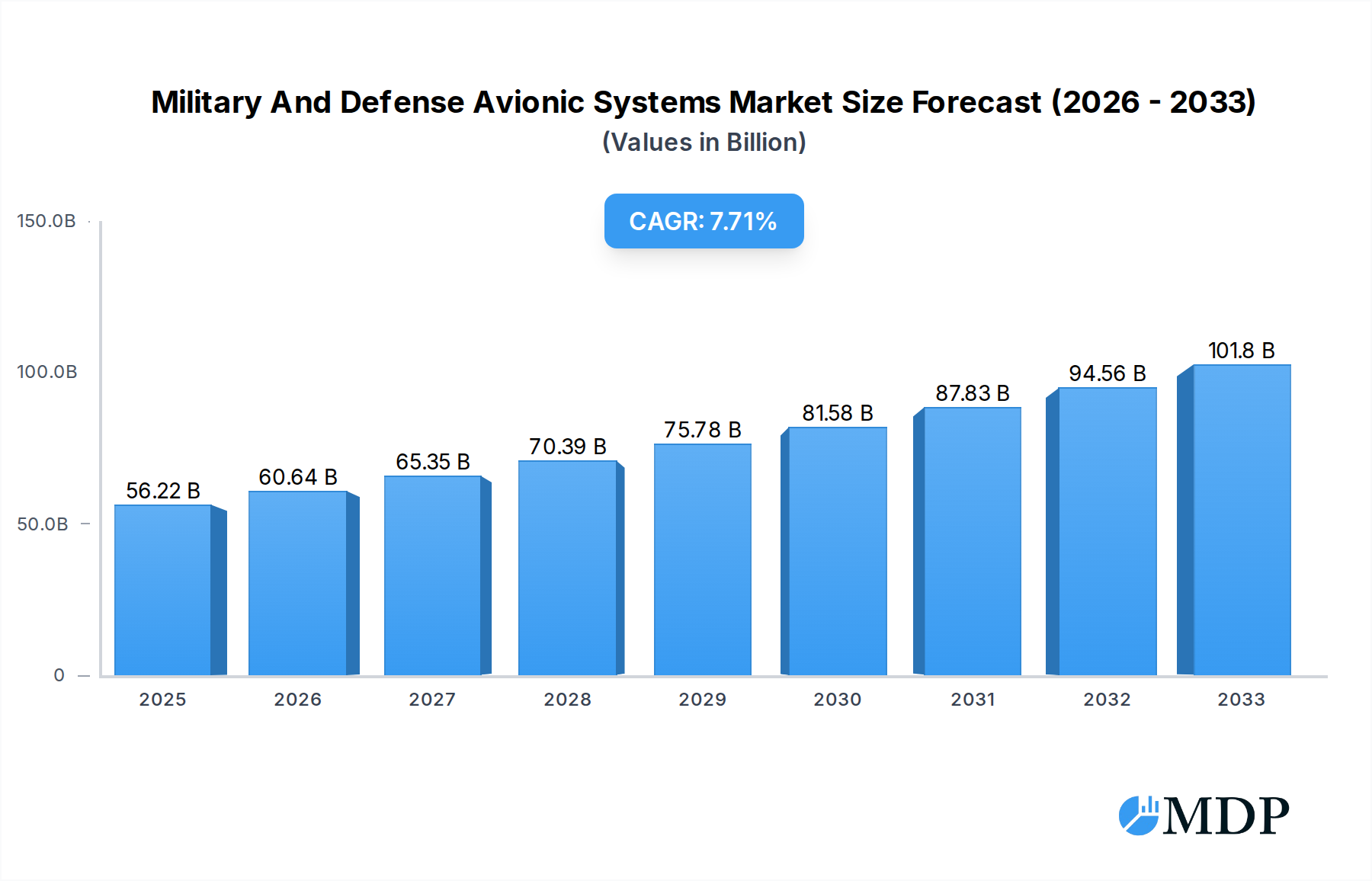

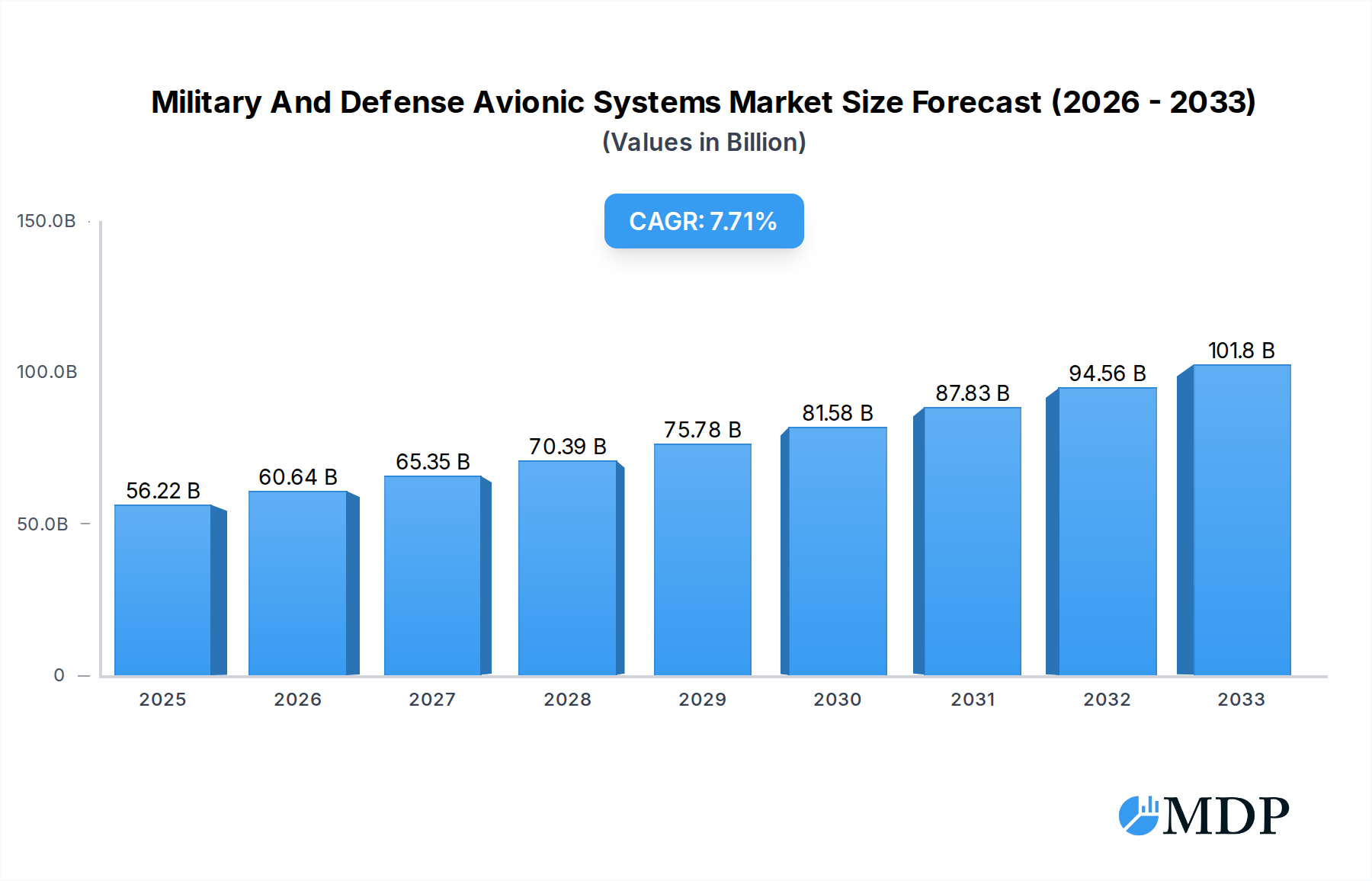

The global Military and Defense Avionics Systems market is poised for significant expansion, projected to reach $56.22 billion in 2025 and grow at a compound annual growth rate (CAGR) of 7.9% through 2033. This robust growth is fueled by increasing geopolitical tensions and the subsequent need for advanced defense capabilities across air, space, and naval platforms. Key drivers include the modernization of existing military fleets, the development of next-generation aircraft and spacecraft, and the escalating demand for sophisticated communication, navigation, and surveillance systems. The market’s expansion is further propelled by advancements in artificial intelligence, enhanced situational awareness technologies, and the integration of secure, networked avionics solutions to counter evolving threats. Investments in unmanned aerial vehicles (UAVs) and advanced combat aircraft are also contributing to this upward trajectory, emphasizing the critical role of cutting-edge avionics in ensuring operational superiority.

Military And Defense Avionic Systems Market Size (In Billion)

The market is segmented into crucial applications such as aircraft, spacecraft, and man-made satellites, with a focus on integrated solutions for monitoring, flight control, and communication and navigation. Emerging trends include the adoption of open architecture avionics for greater flexibility and interoperability, the integration of cyber-secure systems to protect against digital threats, and the increasing use of advanced sensor technologies for enhanced target acquisition and tracking. While the market demonstrates strong growth potential, it faces certain restraints, including the high cost of research and development for advanced avionics, stringent regulatory compliances, and the lengthy procurement cycles typical within the defense sector. Despite these challenges, the relentless pursuit of technological superiority by major defense players like Northrop Grumman, Boeing, and Lockheed Martin, alongside a growing emphasis on integrated battlefield awareness, will continue to shape and drive the military and defense avionics systems landscape.

Military And Defense Avionic Systems Company Market Share

Here is an SEO-optimized, engaging report description for Military And Defense Avionic Systems, designed for maximum search visibility and stakeholder attraction, without the need for further modification.

Military And Defense Avionic Systems Market Dynamics & Concentration

The Military and Defense Avionic Systems market is characterized by significant concentration, with a handful of major players like Northrop Grumman Corporation, Boeing, BAE Systems, Lockheed Martin Corporation, and Honeywell Aerospace holding substantial market share, estimated to be over 60% combined. Innovation is primarily driven by the relentless pursuit of enhanced mission capabilities, superior situational awareness, and reduced operational costs. Key innovation drivers include advancements in artificial intelligence, data fusion, cybersecurity, and miniaturization of components. Regulatory frameworks, governed by stringent defense procurement policies and international arms treaties, significantly influence market entry and product development. Product substitutes, while limited in core military applications, emerge in the form of upgrades and retrofits to existing platforms, delaying the adoption of entirely new systems. End-user trends are shifting towards networked warfare, unmanned aerial systems (UAS) integration, and enhanced survivability, demanding more sophisticated and adaptable avionic solutions. Merger and acquisition (M&A) activities remain a strategic tool for consolidation and technological acquisition. We project approximately 15 significant M&A deals annually during the forecast period, driven by the need to acquire specialized technologies and expand market reach. The market share of leading players is estimated to remain robust, with ongoing competitive strategies focused on R&D investments and strategic partnerships.

Military And Defense Avionic Systems Industry Trends & Analysis

The Military and Defense Avionic Systems industry is poised for robust growth, driven by escalating geopolitical tensions and the imperative for advanced military capabilities worldwide. The global market size is projected to reach several hundred billion dollars by 2033. A key growth driver is the increasing demand for modernized fighter jets, transport aircraft, and helicopters equipped with state-of-the-art avionic suites. This includes advanced communication, navigation, surveillance, and reconnaissance (CNSR) systems, as well as sophisticated flight control and mission management systems. Technological disruptions are transforming the landscape, with a significant impact from AI-powered decision support, augmented reality displays, and secure satellite communication. The integration of 5G and beyond for real-time data transmission is also a critical trend. Consumer preferences, within the defense context, are dictated by the operational effectiveness and survivability of platforms. There's a growing preference for modular, open-architecture systems that allow for easier upgrades and adaptation to evolving threats. Competitive dynamics are intense, with a continuous race to develop and deploy next-generation avionic solutions. The market penetration of advanced avionic systems in new platform acquisitions is estimated to be over 90%, while the retrofit market also presents substantial opportunities. The Compound Annual Growth Rate (CAGR) is projected to be in the high single digits, exceeding 8%, throughout the forecast period. The development of resilient and cyber-hardened systems is paramount, addressing the growing threat of electronic warfare and cyber-attacks. The increasing focus on unmanned systems is also a significant trend, demanding specialized avionic solutions for autonomous operation and swarm capabilities.

Leading Markets & Segments in Military And Defense Avionic Systems

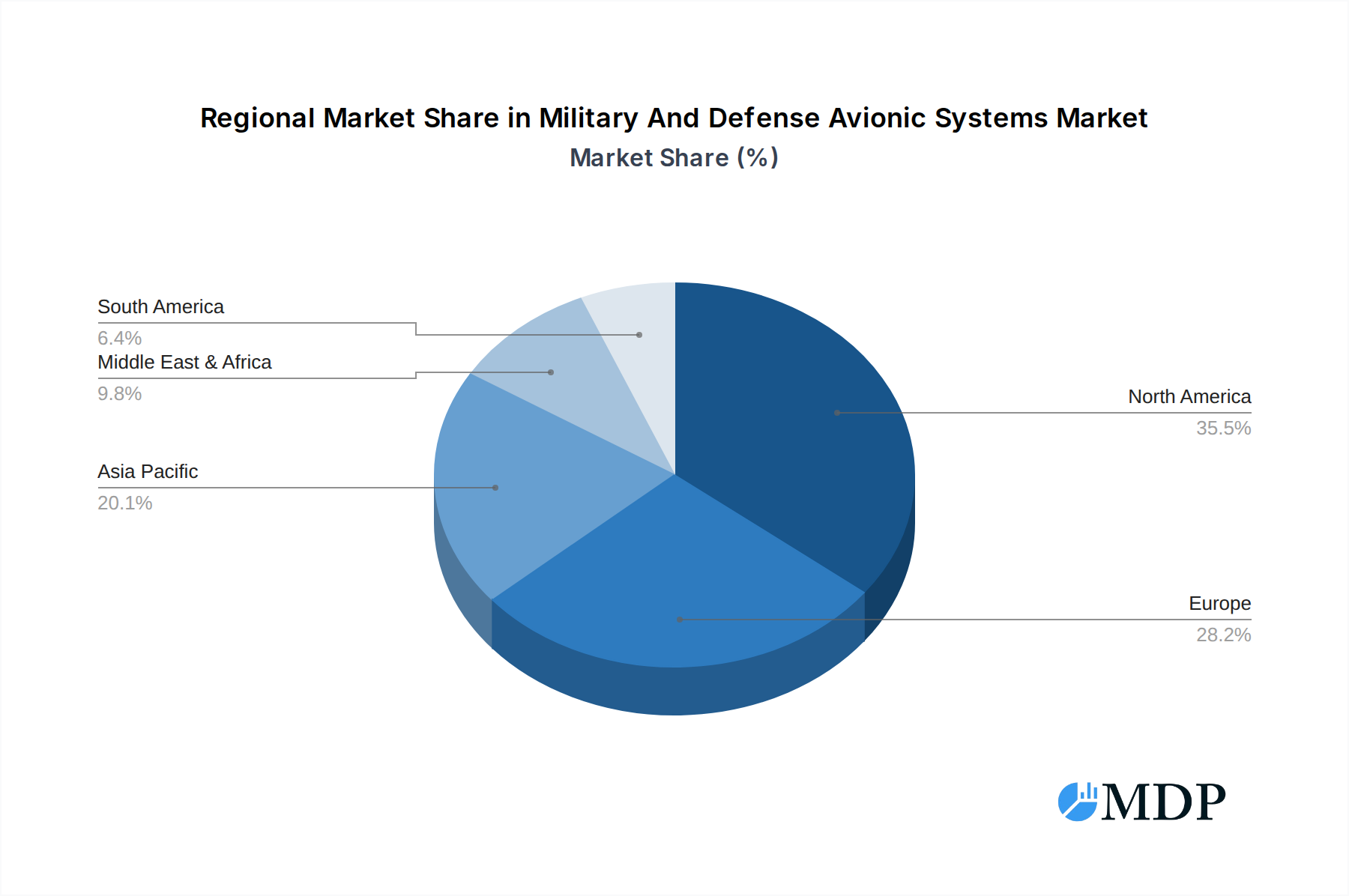

The Plane application segment is the dominant force within the Military and Defense Avionic Systems market, representing over 70% of the total market value. Within this segment, fighter jets and military transport aircraft are the primary consumers of advanced avionic systems. North America, particularly the United States, remains the leading market due to substantial defense budgets, ongoing modernization programs, and the presence of major aerospace and defense contractors.

Key Drivers for Plane Dominance:

- Technological Superiority: Nations are heavily investing in fighter aircraft equipped with cutting-edge avionics to maintain air superiority and conduct complex missions. This includes advanced radar, electronic warfare suites, and integrated sensor fusion systems.

- Global Security Imperatives: Ongoing geopolitical conflicts and the rise of new security challenges necessitate the deployment of advanced air power, driving demand for new aircraft and their avionic systems.

- Fleet Modernization: Many established air forces are undergoing significant modernization programs, replacing aging aircraft with newer platforms that incorporate the latest avionic technologies.

The Communication and Navigation Systems segment is the leading type of avionic system, accounting for approximately 35% of the market. This is due to their fundamental role in every military operation, ensuring command and control, situational awareness, and precise mission execution.

Key Drivers for Communication and Navigation Systems Dominance:

- Network-Centric Warfare: The increasing emphasis on networked operations requires robust and secure communication systems for seamless data sharing and coordination among disparate assets.

- Global Positioning and Reconnaissance: Advanced navigation systems are critical for precision strikes, troop deployment, and intelligence gathering, with an increasing reliance on secure GPS alternatives and multi-constellation receivers.

- Countermeasures and Electronic Warfare: The development of sophisticated jamming and spoofing technologies necessitates the continuous evolution of communication and navigation systems to ensure resilience and reliability.

The Spacecraft and Man-Made Satellite segments, while smaller in current market share, are experiencing significant growth, driven by the increasing reliance on space-based assets for reconnaissance, communication, and surveillance. The forecast period anticipates a substantial uptick in investment in these areas, particularly for advanced sensor payloads and resilient communication links.

Military And Defense Avionic Systems Product Developments

Recent product developments in Military and Defense Avionic Systems are characterized by a focus on enhanced situational awareness, improved survivability, and increased mission flexibility. Companies are rapidly integrating artificial intelligence and machine learning for real-time data analysis, predictive maintenance, and enhanced decision support for pilots. The miniaturization and ruggedization of components are enabling more compact and efficient systems for unmanned aerial vehicles (UAVs) and next-generation combat aircraft. Innovations in secure communication technologies, including quantum-resistant encryption and resilient satellite links, are also gaining prominence, addressing evolving cyber threats. These advancements provide a significant competitive advantage by offering superior operational capabilities and reducing the cognitive load on aircrews.

Key Drivers of Military And Defense Avionic Systems Growth

The primary growth drivers for the Military and Defense Avionic Systems market are multifaceted. Technologically, the relentless innovation in sensors, processing power, and artificial intelligence is enabling more sophisticated and capable avionic suites. Economic factors, such as increased global defense spending by major nations and the continuous need for fleet modernization, provide a strong foundation for market expansion. Regulatory frameworks, while stringent, also act as drivers by mandating the adoption of advanced safety and performance standards, pushing for the integration of newer technologies. For example, the ongoing upgrade of legacy aircraft fleets across numerous air forces necessitates the integration of modern avionic systems to meet evolving operational requirements.

Challenges in the Military And Defense Avionic Systems Market

The Military and Defense Avionic Systems market faces significant challenges that can impede growth. Stringent regulatory hurdles and lengthy procurement processes can delay the adoption of new technologies, impacting market entry for innovative companies. Supply chain disruptions, exacerbated by geopolitical events and component shortages, pose a constant threat to production timelines and cost management. Intense competition among established players and emerging technology providers drives down margins and necessitates continuous investment in R&D. The high cost of development and integration of cutting-edge avionic systems also presents a barrier, particularly for smaller defense contractors.

Emerging Opportunities in Military And Defense Avionic Systems

Emerging opportunities in the Military and Defense Avionic Systems market are largely driven by technological breakthroughs and evolving defense strategies. The burgeoning demand for unmanned systems, including drones and autonomous vehicles, presents a significant growth avenue for specialized avionic solutions. Strategic partnerships between traditional defense primes and innovative technology startups are facilitating the rapid integration of AI, cyber-security, and advanced sensor technologies. Furthermore, the expansion of space-based defense capabilities, including satellite constellations for intelligence, surveillance, and reconnaissance (ISR), is creating new markets for resilient and advanced avionic systems. The increasing focus on multi-domain operations also necessitates interoperable and interconnected avionic systems.

Leading Players in the Military And Defense Avionic Systems Sector

- Northrop Grumman Corporation

- Boeing

- BAE Systems

- Elbit Systems

- Embraer

- Rockwell Collins

- Leonardo

- Lockheed Martin Corporation

- Thales Group

- Airbus Helicopters

- Saab

- L3Harris

- Honeywell Aerospace

- Hilton Software

- GE

- ForeFlight

- Xavion

- Avidyne

- Aspen Avionics

- ENSCO Avionics

- Sagetech

Key Milestones in Military And Defense Avionic Systems Industry

- 2019: Introduction of AI-powered sensor fusion systems enhancing pilot situational awareness.

- 2020: Significant advancements in secure satellite communication technology for military applications.

- 2021: Major defense contractors began integrating quantum-resistant encryption into avionic systems.

- 2022: Increased investment in open-architecture avionic systems for modularity and upgradeability.

- 2023: Launch of next-generation flight control systems incorporating advanced autonomous capabilities.

- 2024: Growing adoption of augmented reality displays for mission planning and execution.

- 2025 (Estimated): Expected widespread integration of AI for predictive maintenance and operational optimization.

- 2026-2033 (Forecast): Continued evolution towards fully networked avionic systems and advanced cybersecurity solutions.

Strategic Outlook for Military And Defense Avionic Systems Market

The strategic outlook for the Military and Defense Avionic Systems market is exceptionally positive, fueled by continuous advancements in technology and sustained global defense investments. Growth accelerators include the increasing integration of artificial intelligence and machine learning, driving autonomous capabilities and enhanced decision-making. The demand for cybersecurity and resilient communication systems will remain paramount, creating opportunities for specialized solutions. Furthermore, the ongoing modernization of air forces globally, coupled with the rise of unmanned systems, will drive substantial market expansion. Strategic partnerships and R&D investments will be crucial for companies to maintain a competitive edge and capitalize on these burgeoning opportunities.

Military And Defense Avionic Systems Segmentation

-

1. Application

- 1.1. Plane

- 1.2. Spacecraft

- 1.3. Man-Made Satellite

-

2. Types

- 2.1. Monitoring System

- 2.2. Flight Control System

- 2.3. Communication and Navigation Systems

Military And Defense Avionic Systems Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Military And Defense Avionic Systems Regional Market Share

Geographic Coverage of Military And Defense Avionic Systems

Military And Defense Avionic Systems REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Military And Defense Avionic Systems Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Plane

- 5.1.2. Spacecraft

- 5.1.3. Man-Made Satellite

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Monitoring System

- 5.2.2. Flight Control System

- 5.2.3. Communication and Navigation Systems

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Military And Defense Avionic Systems Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Plane

- 6.1.2. Spacecraft

- 6.1.3. Man-Made Satellite

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Monitoring System

- 6.2.2. Flight Control System

- 6.2.3. Communication and Navigation Systems

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Military And Defense Avionic Systems Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Plane

- 7.1.2. Spacecraft

- 7.1.3. Man-Made Satellite

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Monitoring System

- 7.2.2. Flight Control System

- 7.2.3. Communication and Navigation Systems

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Military And Defense Avionic Systems Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Plane

- 8.1.2. Spacecraft

- 8.1.3. Man-Made Satellite

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Monitoring System

- 8.2.2. Flight Control System

- 8.2.3. Communication and Navigation Systems

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Military And Defense Avionic Systems Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Plane

- 9.1.2. Spacecraft

- 9.1.3. Man-Made Satellite

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Monitoring System

- 9.2.2. Flight Control System

- 9.2.3. Communication and Navigation Systems

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Military And Defense Avionic Systems Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Plane

- 10.1.2. Spacecraft

- 10.1.3. Man-Made Satellite

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Monitoring System

- 10.2.2. Flight Control System

- 10.2.3. Communication and Navigation Systems

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Northrop Grumman Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Boeing

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BAE Systems

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Elbit Systems

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Embraer

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Rockwell Collins

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Leonardo

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Lockheed Martin Corporation

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Thales Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Airbus Helicopters

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Saab

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 L3Harris

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Honeywell Aerospace

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Hilton Software

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 GE

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 ForeFlight

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Xavion

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Avidyne

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Aspen Avionics

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 ENSCO Avionics

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Sagetech

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 Northrop Grumman Corporation

List of Figures

- Figure 1: Global Military And Defense Avionic Systems Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Military And Defense Avionic Systems Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Military And Defense Avionic Systems Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Military And Defense Avionic Systems Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Military And Defense Avionic Systems Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Military And Defense Avionic Systems Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Military And Defense Avionic Systems Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Military And Defense Avionic Systems Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Military And Defense Avionic Systems Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Military And Defense Avionic Systems Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Military And Defense Avionic Systems Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Military And Defense Avionic Systems Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Military And Defense Avionic Systems Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Military And Defense Avionic Systems Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Military And Defense Avionic Systems Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Military And Defense Avionic Systems Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Military And Defense Avionic Systems Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Military And Defense Avionic Systems Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Military And Defense Avionic Systems Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Military And Defense Avionic Systems Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Military And Defense Avionic Systems Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Military And Defense Avionic Systems Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Military And Defense Avionic Systems Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Military And Defense Avionic Systems Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Military And Defense Avionic Systems Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Military And Defense Avionic Systems Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Military And Defense Avionic Systems Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Military And Defense Avionic Systems Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Military And Defense Avionic Systems Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Military And Defense Avionic Systems Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Military And Defense Avionic Systems Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Military And Defense Avionic Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Military And Defense Avionic Systems Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Military And Defense Avionic Systems?

The projected CAGR is approximately 7.9%.

2. Which companies are prominent players in the Military And Defense Avionic Systems?

Key companies in the market include Northrop Grumman Corporation, Boeing, BAE Systems, Elbit Systems, Embraer, Rockwell Collins, Leonardo, Lockheed Martin Corporation, Thales Group, Airbus Helicopters, Saab, L3Harris, Honeywell Aerospace, Hilton Software, GE, ForeFlight, Xavion, Avidyne, Aspen Avionics, ENSCO Avionics, Sagetech.

3. What are the main segments of the Military And Defense Avionic Systems?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Military And Defense Avionic Systems," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Military And Defense Avionic Systems report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Military And Defense Avionic Systems?

To stay informed about further developments, trends, and reports in the Military And Defense Avionic Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence