Key Insights

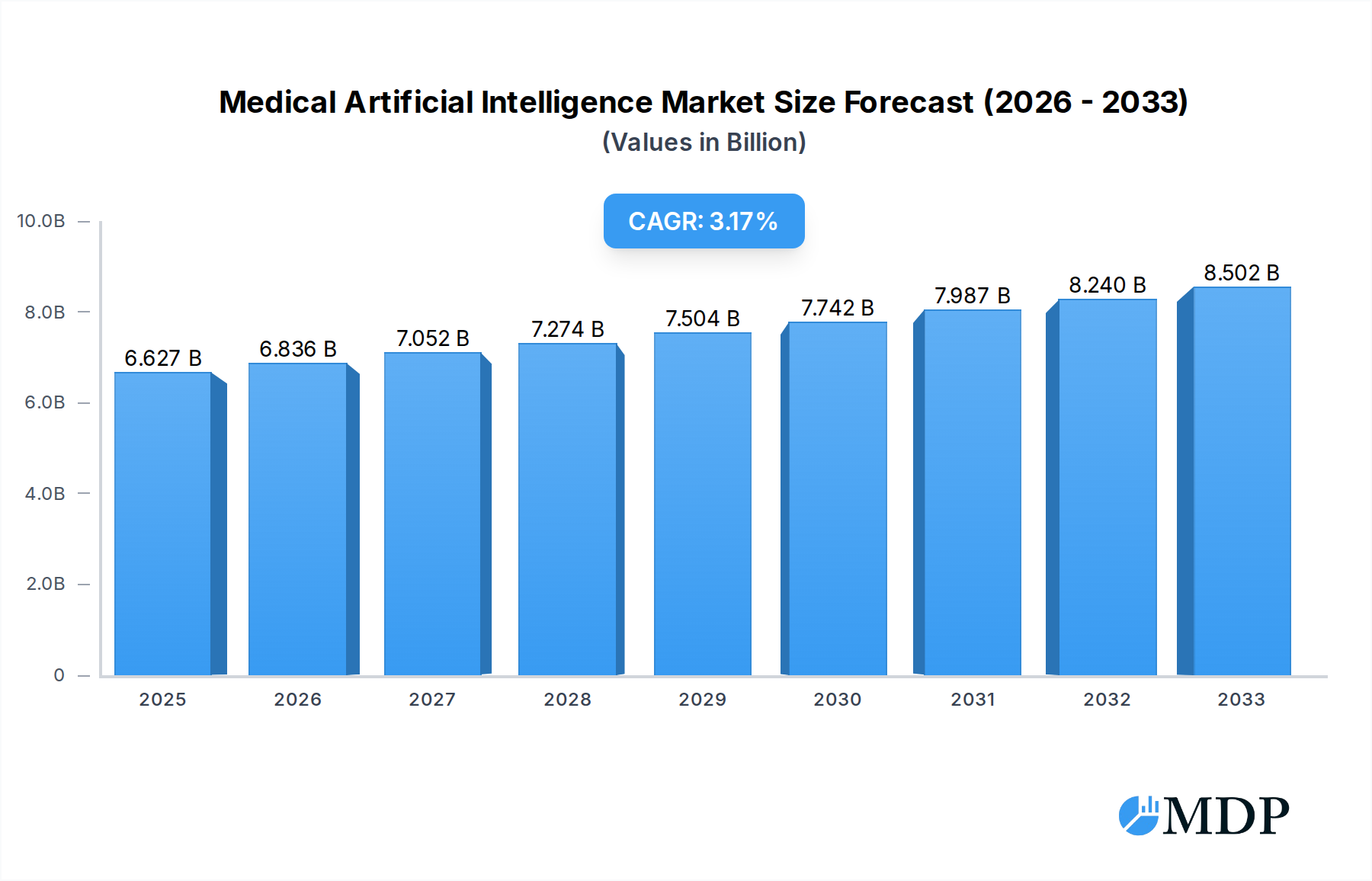

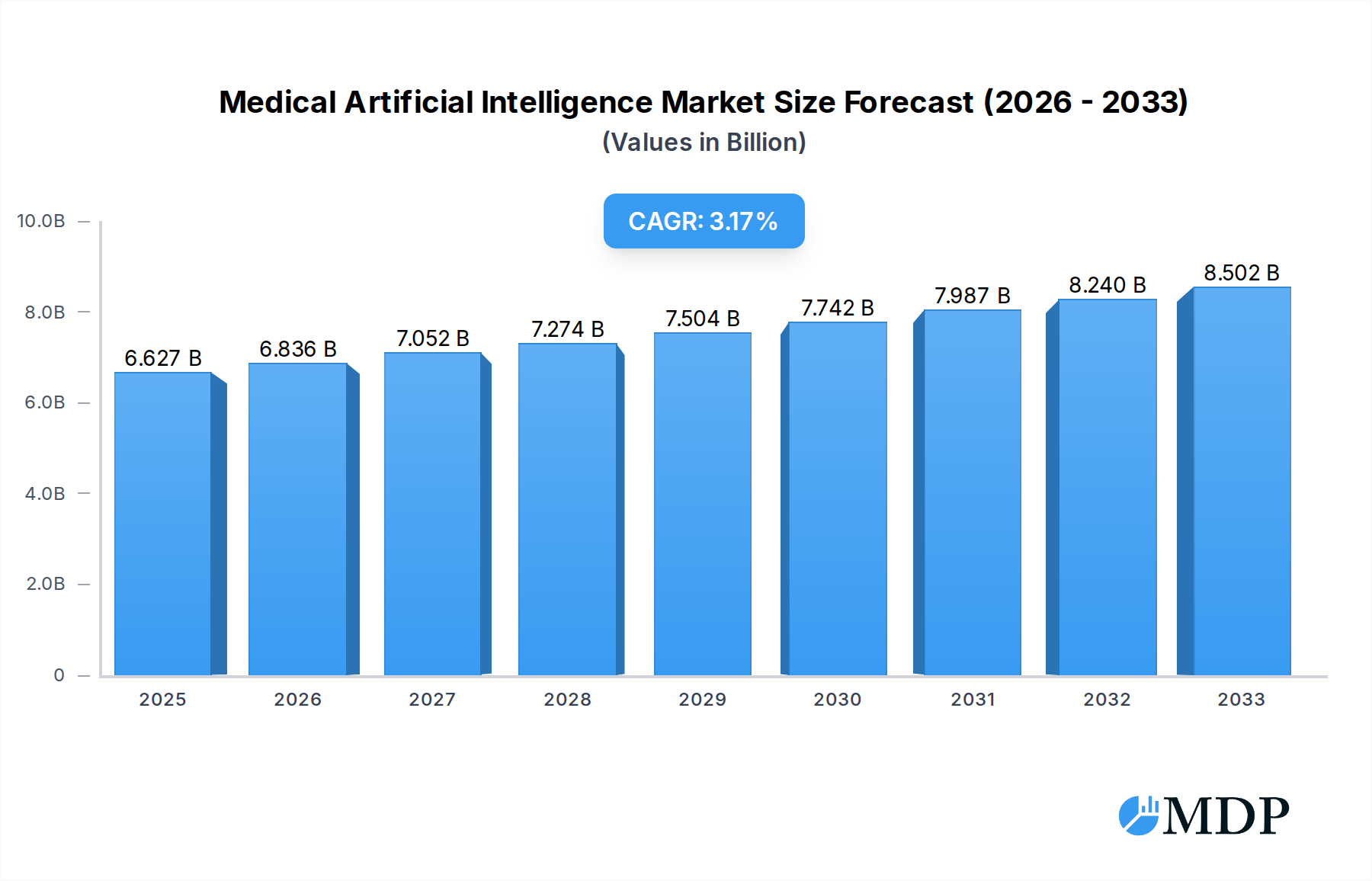

The global Medical Artificial Intelligence market is poised for significant growth, currently valued at $6626.5 million in 2025. This expansion is driven by the increasing adoption of AI technologies across various healthcare applications, including disease risk prediction, medical imaging assisted diagnosis, and clinical auxiliary diagnosis and treatment. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.3% from 2025 to 2033, indicating a steady and sustained upward trajectory. Key drivers fueling this growth include the escalating demand for personalized medicine, the need for improved diagnostic accuracy and efficiency, and the burgeoning volume of healthcare data that AI can effectively analyze. The integration of AI in smart health management and intelligent hospital operations is further contributing to its widespread adoption, promising to streamline workflows and enhance patient care outcomes.

Medical Artificial Intelligence Market Size (In Billion)

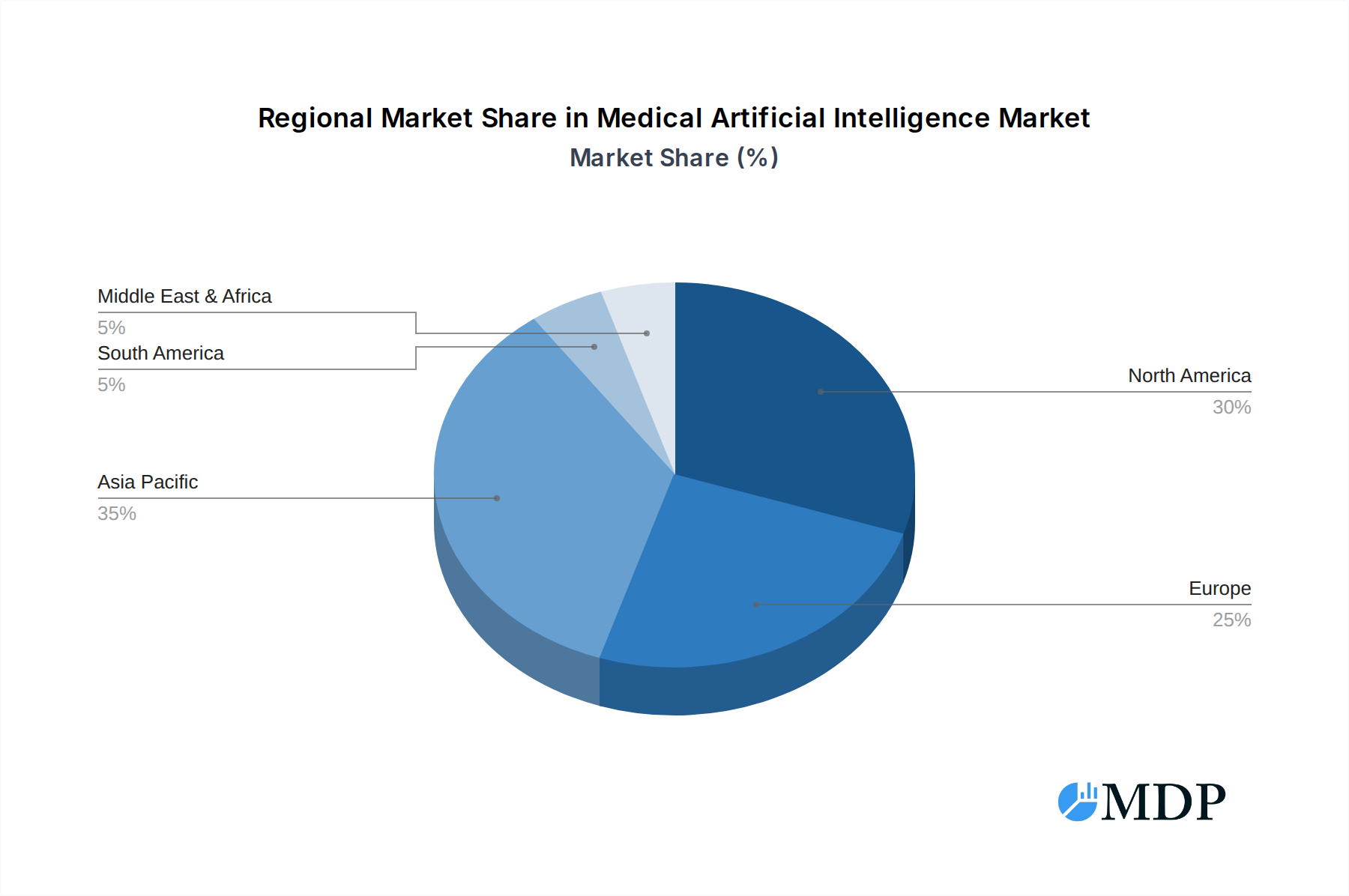

Emerging trends such as the development of sophisticated AI-powered virtual assistants for both patients and healthcare professionals, alongside advancements in AI for drug discovery and development, are expected to shape the future landscape of Medical AI. While the market demonstrates robust growth potential, certain restraints, such as data privacy concerns, regulatory hurdles, and the high cost of implementation, need to be strategically addressed. Despite these challenges, the market is characterized by intense competition among established tech giants, prominent healthcare technology providers, and innovative startups. The Asia Pacific region, led by China and India, is anticipated to be a significant growth engine due to increasing healthcare investments and a large patient pool. North America and Europe also represent mature markets with a strong focus on research and development, further solidifying the global significance of Medical AI.

Medical Artificial Intelligence Company Market Share

This in-depth report provides an indispensable analysis of the global Medical Artificial Intelligence (AI) market, offering a comprehensive roadmap for stakeholders navigating this rapidly evolving landscape. Covering a study period of 2019–2033, with a base year of 2025, this report delves into historical performance, current market dynamics, and future projections, making it essential for strategic decision-making. With an estimated CAGR of 35 million projected for the forecast period, the Medical AI market is poised for unprecedented growth. This analysis focuses on key segments including Hospital, Medical Institutions, and Others for applications, and Disease Risk Prediction, Medical Imaging Assisted Diagnosis, Clinical Auxiliary Diagnosis And Treatment, Smart Health Management, Intelligent Hospital Management, Virtual Assistant, and Others for types.

Medical Artificial Intelligence Market Dynamics & Concentration

The global Medical Artificial Intelligence market, projected to reach over $50 million by 2033, exhibits a dynamic and increasingly concentrated landscape. Key innovation drivers include advancements in machine learning algorithms, increased availability of healthcare data, and the growing demand for personalized medicine. Regulatory frameworks, while evolving, play a crucial role in shaping market entry and product approval, with significant efforts underway to ensure patient safety and data privacy. Product substitutes, though nascent, are beginning to emerge in areas like advanced analytics platforms that may indirectly impact AI adoption. End-user trends overwhelmingly favor AI solutions that demonstrably improve diagnostic accuracy, streamline clinical workflows, and enhance patient outcomes. Mergers and acquisitions (M&A) activities are on the rise, with an estimated 300 million M&A deals anticipated in the forecast period, as larger players seek to consolidate their market share and acquire innovative technologies. The market concentration is moderate but shifting towards key players with robust R&D capabilities and strategic partnerships, particularly in the Medical Imaging Assisted Diagnosis segment, which currently holds an estimated 30 million market share.

Medical Artificial Intelligence Industry Trends & Analysis

The Medical Artificial Intelligence industry is experiencing exponential growth, driven by a confluence of technological advancements, increasing healthcare expenditure, and a global imperative to improve patient care efficiency. The CAGR of 35 million over the 2025-2033 period signifies a robust expansion trajectory. Technological disruptions, such as the advent of deep learning, natural language processing (NLP), and computer vision, are revolutionizing diagnostic capabilities and therapeutic interventions. Consumer preferences are shifting towards proactive healthcare, with a growing demand for AI-powered tools that offer personalized health insights and facilitate remote monitoring. This trend is particularly evident in the Smart Health Management segment, which is projected to see a market penetration of over 40 million by 2030. Competitive dynamics are intensifying, with a blend of established technology giants, specialized AI startups, and traditional healthcare providers vying for market dominance. Key growth drivers include the increasing burden of chronic diseases, the need for cost-effective healthcare solutions, and the expanding adoption of electronic health records (EHRs), which provide the foundational data for AI algorithms. Furthermore, government initiatives and funding for digital health innovation are acting as significant catalysts. The integration of AI in drug discovery and development is another prominent trend, promising to accelerate the pace of pharmaceutical innovation and reduce R&D costs by an estimated 20 million annually. The deployment of AI in clinical decision support systems is improving diagnostic accuracy and reducing medical errors, leading to better patient outcomes and significant cost savings for healthcare systems, estimated at 45 million in reduced operational expenses. The rising demand for telemedicine and remote patient monitoring solutions, fueled by the COVID-19 pandemic, has further accelerated the adoption of AI-powered applications in healthcare. The market penetration of AI in hospitals is estimated to reach 50 million by 2033, as institutions increasingly recognize the value of AI in optimizing operations and enhancing patient care.

Leading Markets & Segments in Medical Artificial Intelligence

The Hospital application segment stands as the dominant force in the Medical Artificial Intelligence market, driven by the urgent need for operational efficiency, improved patient throughput, and enhanced diagnostic capabilities within these complex healthcare environments. This segment is projected to account for a significant portion of the market, estimated at over 60 million by the end of the forecast period. Within this segment, Medical Imaging Assisted Diagnosis emerges as the leading type, benefiting from rapid advancements in AI algorithms capable of analyzing complex medical scans with unparalleled speed and accuracy. The economic policies of major economies, such as substantial government investments in healthcare infrastructure and digital transformation initiatives, coupled with robust technological infrastructure, underpin the dominance of this segment.

- Dominance Drivers in Hospital Application:

- Economic Policies: Government funding for AI research and adoption in healthcare, tax incentives for technology implementation.

- Technological Infrastructure: Widespread availability of high-speed internet, cloud computing services, and advanced hardware for AI processing.

- Demand for Efficiency: Pressure on hospitals to reduce wait times, optimize resource allocation, and improve staff productivity.

- Improved Patient Outcomes: AI's ability to enhance diagnostic accuracy, personalize treatment plans, and predict patient deterioration.

The Medical Institutions segment, encompassing clinics, diagnostic centers, and specialized healthcare facilities, also represents a substantial and growing market, with an estimated size of over 35 million. This growth is fueled by the increasing adoption of AI for specialized diagnostic tasks and patient management.

- Dominance Drivers in Medical Institutions:

- Specialized AI Tools: Demand for AI solutions tailored to specific medical specialties, such as pathology or radiology.

- Cost-Effectiveness: AI's potential to reduce operational costs and improve the accuracy of diagnoses in smaller facilities.

- Remote Diagnostics: The rise of AI-powered tools enabling remote interpretation of medical data, expanding access to specialized care.

Furthermore, the Clinical Auxiliary Diagnosis And Treatment type is experiencing significant growth across all application segments, projected to reach over 40 million in market value. This is driven by AI's ability to assist clinicians in making more informed decisions, personalizing treatment regimens, and predicting patient responses to therapies. The Disease Risk Prediction segment, with an estimated market size of over 25 million, is also a key growth area, leveraging AI to identify individuals at high risk for various conditions, enabling early intervention and preventive care.

Medical Artificial Intelligence Product Developments

Product developments in Medical AI are characterized by rapid innovation, focusing on enhancing diagnostic accuracy, streamlining clinical workflows, and enabling personalized patient care. Companies are releasing advanced AI-powered platforms for medical imaging analysis, such as those capable of detecting subtle anomalies in X-rays, CT scans, and MRIs with greater precision. Furthermore, intelligent virtual assistants are being developed to manage patient appointments, provide health information, and support remote patient monitoring. The competitive advantage lies in the ability of these products to integrate seamlessly with existing healthcare IT systems, demonstrate a clear return on investment through improved efficiency and patient outcomes, and comply with stringent regulatory standards. Technological trends like federated learning are enabling the development of AI models without compromising patient data privacy.

Key Drivers of Medical Artificial Intelligence Growth

The explosive growth in the Medical Artificial Intelligence market is propelled by several powerful drivers. Technologically, advancements in machine learning algorithms, coupled with the increasing availability of large, high-quality healthcare datasets, are foundational. Economically, the escalating costs of healthcare globally and the growing demand for more efficient and accessible medical services create a strong impetus for AI adoption. Regulatory bodies are increasingly recognizing the potential of AI to improve healthcare outcomes, leading to clearer pathways for the approval and implementation of AI-based medical devices and software. The aging global population and the increasing prevalence of chronic diseases further amplify the need for AI-driven solutions in diagnosis, treatment, and management.

Challenges in the Medical Artificial Intelligence Market

Despite its immense potential, the Medical Artificial Intelligence market faces significant challenges that could impede its widespread adoption. Foremost among these are regulatory hurdles, with the complex and evolving nature of approvals for AI-powered medical devices creating uncertainty and delays. Data privacy and security concerns are paramount, as the handling of sensitive patient information requires robust safeguards and compliance with regulations like GDPR and HIPAA. The integration of AI systems with existing, often legacy, healthcare IT infrastructure can be technically challenging and costly. Furthermore, the "black box" nature of some AI algorithms can lead to a lack of trust and transparency among clinicians, necessitating explainable AI (XAI) solutions. The cost of implementing and maintaining AI systems, alongside the need for specialized expertise, also presents a barrier for many healthcare organizations, with implementation costs estimated to be upwards of 10 million for comprehensive hospital-wide systems.

Emerging Opportunities in Medical Artificial Intelligence

The future of Medical AI is ripe with emerging opportunities that promise to redefine healthcare delivery. Breakthroughs in generative AI are opening new avenues for drug discovery and development, potentially reducing the time and cost associated with bringing new treatments to market. Strategic partnerships between AI technology providers and pharmaceutical companies are becoming increasingly common, fostering collaborative innovation. The expansion of AI into emerging markets, where healthcare infrastructure is developing rapidly, presents significant growth potential. Furthermore, the application of AI in personalized preventive medicine and remote patient monitoring is poised to revolutionize how individuals manage their health, leading to better long-term outcomes and reduced healthcare burdens, with an estimated 5 million reduction in hospital readmissions annually.

Leading Players in the Medical Artificial Intelligence Sector

- Ali Health

- Ping An Healthcare And Technology Company Limited.

- Tencent

- Tianjin Happy Life Technology Co.,Ltd.

- WeDoctor

- Beijing Dongruan Wanghai Technology Co.,Ltd.

- Unisound AI Technology Co.,Ltd.

- iCarbonX

- Spring Rain Software

- Infervision Technology

- Zhejiang Taimei Medical Technology Co.,Ltd

- Sipai(Beijing)Network Techology Co.,Ltd.

- TINAVI Medical Technologies Co.,Ltd.

- Anhui iFLYHealth Co.,Ltd.

- Spiritual Doctor Zhihui

- General Electric

- Medtronic

- Johnson

- Siemens

- Nvidia Corporation

Key Milestones in Medical Artificial Intelligence Industry

- 2019: Launch of advanced AI-powered diagnostic tools for radiology, significantly improving detection rates for certain cancers.

- 2020: Increased adoption of AI-driven virtual assistants for patient triage and appointment scheduling amidst the COVID-19 pandemic.

- 2021: Significant M&A activity as major tech companies invest heavily in AI healthcare startups, with over 50 million in total deal value.

- 2022: Regulatory bodies begin to streamline approval processes for AI medical devices, fostering innovation.

- 2023: Widespread deployment of AI in drug discovery pipelines, leading to accelerated identification of potential therapeutic candidates.

- 2024: Introduction of sophisticated AI models for predictive analytics in disease risk assessment, enabling proactive health interventions.

Strategic Outlook for Medical Artificial Intelligence Market

The strategic outlook for the Medical Artificial Intelligence market remains exceptionally bright, driven by continued technological innovation, increasing healthcare demands, and supportive regulatory environments. Key growth accelerators include the expansion of AI into new therapeutic areas, the development of more sophisticated predictive analytics for population health management, and the increasing integration of AI into wearable devices for continuous health monitoring. Strategic opportunities lie in leveraging AI to address healthcare disparities, democratize access to high-quality medical expertise, and further personalize patient care. The focus will increasingly shift towards AI solutions that not only improve clinical outcomes but also demonstrably reduce healthcare costs and enhance patient experience, with an estimated 40 million in cost savings projected annually by 2030.

Medical Artificial Intelligence Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Medical Institutions

- 1.3. Others

-

2. Types

- 2.1. Disease Risk Prediction

- 2.2. Medical Imaging Assisted Diagnosis

- 2.3. Clinical Auxiliary Diagnosis And Treatment

- 2.4. Smart Health Management

- 2.5. Intelligent Hospital Management

- 2.6. Virtual Assistant

- 2.7. Others

Medical Artificial Intelligence Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Artificial Intelligence Regional Market Share

Geographic Coverage of Medical Artificial Intelligence

Medical Artificial Intelligence REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Medical Institutions

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Disease Risk Prediction

- 5.2.2. Medical Imaging Assisted Diagnosis

- 5.2.3. Clinical Auxiliary Diagnosis And Treatment

- 5.2.4. Smart Health Management

- 5.2.5. Intelligent Hospital Management

- 5.2.6. Virtual Assistant

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Medical Artificial Intelligence Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Medical Institutions

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Disease Risk Prediction

- 6.2.2. Medical Imaging Assisted Diagnosis

- 6.2.3. Clinical Auxiliary Diagnosis And Treatment

- 6.2.4. Smart Health Management

- 6.2.5. Intelligent Hospital Management

- 6.2.6. Virtual Assistant

- 6.2.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Medical Artificial Intelligence Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Medical Institutions

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Disease Risk Prediction

- 7.2.2. Medical Imaging Assisted Diagnosis

- 7.2.3. Clinical Auxiliary Diagnosis And Treatment

- 7.2.4. Smart Health Management

- 7.2.5. Intelligent Hospital Management

- 7.2.6. Virtual Assistant

- 7.2.7. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Medical Artificial Intelligence Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Medical Institutions

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Disease Risk Prediction

- 8.2.2. Medical Imaging Assisted Diagnosis

- 8.2.3. Clinical Auxiliary Diagnosis And Treatment

- 8.2.4. Smart Health Management

- 8.2.5. Intelligent Hospital Management

- 8.2.6. Virtual Assistant

- 8.2.7. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Medical Artificial Intelligence Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Medical Institutions

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Disease Risk Prediction

- 9.2.2. Medical Imaging Assisted Diagnosis

- 9.2.3. Clinical Auxiliary Diagnosis And Treatment

- 9.2.4. Smart Health Management

- 9.2.5. Intelligent Hospital Management

- 9.2.6. Virtual Assistant

- 9.2.7. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Medical Artificial Intelligence Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Medical Institutions

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Disease Risk Prediction

- 10.2.2. Medical Imaging Assisted Diagnosis

- 10.2.3. Clinical Auxiliary Diagnosis And Treatment

- 10.2.4. Smart Health Management

- 10.2.5. Intelligent Hospital Management

- 10.2.6. Virtual Assistant

- 10.2.7. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Medical Artificial Intelligence Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospital

- 11.1.2. Medical Institutions

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Disease Risk Prediction

- 11.2.2. Medical Imaging Assisted Diagnosis

- 11.2.3. Clinical Auxiliary Diagnosis And Treatment

- 11.2.4. Smart Health Management

- 11.2.5. Intelligent Hospital Management

- 11.2.6. Virtual Assistant

- 11.2.7. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ali Health

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Ping An Healthcare And Technology Company Limited.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Tencent

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Tianjin Happy Life Technology Co.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ltd.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 WeDoctor

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Beijing Dongruan Wanghai Technology Co.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Ltd.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Unisound AI Technology Co.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ltd.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 iCarbonX

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Spring Rain Software

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Infervision Technology

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Zhejiang Taimei Medical Technology Co.

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Ltd

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Sipai(Beijing)Network Techology Co.

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Ltd.

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 TINAVI Medical Technologies Co.

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Ltd.

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Anhui iFLYHealth Co.

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Ltd.

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Spiritual Doctor Zhihui

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 General Electric

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.24 Google

- 12.1.24.1. Company Overview

- 12.1.24.2. Products

- 12.1.24.3. Company Financials

- 12.1.24.4. SWOT Analysis

- 12.1.25 Medtronic

- 12.1.25.1. Company Overview

- 12.1.25.2. Products

- 12.1.25.3. Company Financials

- 12.1.25.4. SWOT Analysis

- 12.1.26 Johnson

- 12.1.26.1. Company Overview

- 12.1.26.2. Products

- 12.1.26.3. Company Financials

- 12.1.26.4. SWOT Analysis

- 12.1.27 Siemens

- 12.1.27.1. Company Overview

- 12.1.27.2. Products

- 12.1.27.3. Company Financials

- 12.1.27.4. SWOT Analysis

- 12.1.28 Nvidia Corporation

- 12.1.28.1. Company Overview

- 12.1.28.2. Products

- 12.1.28.3. Company Financials

- 12.1.28.4. SWOT Analysis

- 12.1.1 Ali Health

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Medical Artificial Intelligence Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Medical Artificial Intelligence Revenue (million), by Application 2025 & 2033

- Figure 3: North America Medical Artificial Intelligence Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Artificial Intelligence Revenue (million), by Types 2025 & 2033

- Figure 5: North America Medical Artificial Intelligence Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Medical Artificial Intelligence Revenue (million), by Country 2025 & 2033

- Figure 7: North America Medical Artificial Intelligence Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Artificial Intelligence Revenue (million), by Application 2025 & 2033

- Figure 9: South America Medical Artificial Intelligence Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Artificial Intelligence Revenue (million), by Types 2025 & 2033

- Figure 11: South America Medical Artificial Intelligence Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Medical Artificial Intelligence Revenue (million), by Country 2025 & 2033

- Figure 13: South America Medical Artificial Intelligence Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Artificial Intelligence Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Medical Artificial Intelligence Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Artificial Intelligence Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Medical Artificial Intelligence Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Medical Artificial Intelligence Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Medical Artificial Intelligence Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Artificial Intelligence Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Artificial Intelligence Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Artificial Intelligence Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Medical Artificial Intelligence Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Medical Artificial Intelligence Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Artificial Intelligence Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Artificial Intelligence Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Artificial Intelligence Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Artificial Intelligence Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Medical Artificial Intelligence Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Medical Artificial Intelligence Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Artificial Intelligence Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Artificial Intelligence Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Medical Artificial Intelligence Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Medical Artificial Intelligence Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Medical Artificial Intelligence Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Medical Artificial Intelligence Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Medical Artificial Intelligence Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Artificial Intelligence Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Medical Artificial Intelligence Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Medical Artificial Intelligence Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Artificial Intelligence Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Medical Artificial Intelligence Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Medical Artificial Intelligence Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Artificial Intelligence Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Medical Artificial Intelligence Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Medical Artificial Intelligence Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Artificial Intelligence Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Medical Artificial Intelligence Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Medical Artificial Intelligence Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Artificial Intelligence Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Artificial Intelligence?

The projected CAGR is approximately 3.3%.

2. Which companies are prominent players in the Medical Artificial Intelligence?

Key companies in the market include Ali Health, Ping An Healthcare And Technology Company Limited., Tencent, Tianjin Happy Life Technology Co., Ltd., WeDoctor, Beijing Dongruan Wanghai Technology Co., Ltd., Unisound AI Technology Co., Ltd., iCarbonX, Spring Rain Software, Infervision Technology, Zhejiang Taimei Medical Technology Co., Ltd, Sipai(Beijing)Network Techology Co., Ltd., TINAVI Medical Technologies Co., Ltd., Anhui iFLYHealth Co., Ltd., Spiritual Doctor Zhihui, General Electric, Google, Medtronic, Johnson, Siemens, Nvidia Corporation.

3. What are the main segments of the Medical Artificial Intelligence?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 6626.5 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Artificial Intelligence," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Artificial Intelligence report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Artificial Intelligence?

To stay informed about further developments, trends, and reports in the Medical Artificial Intelligence, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence