Key Insights

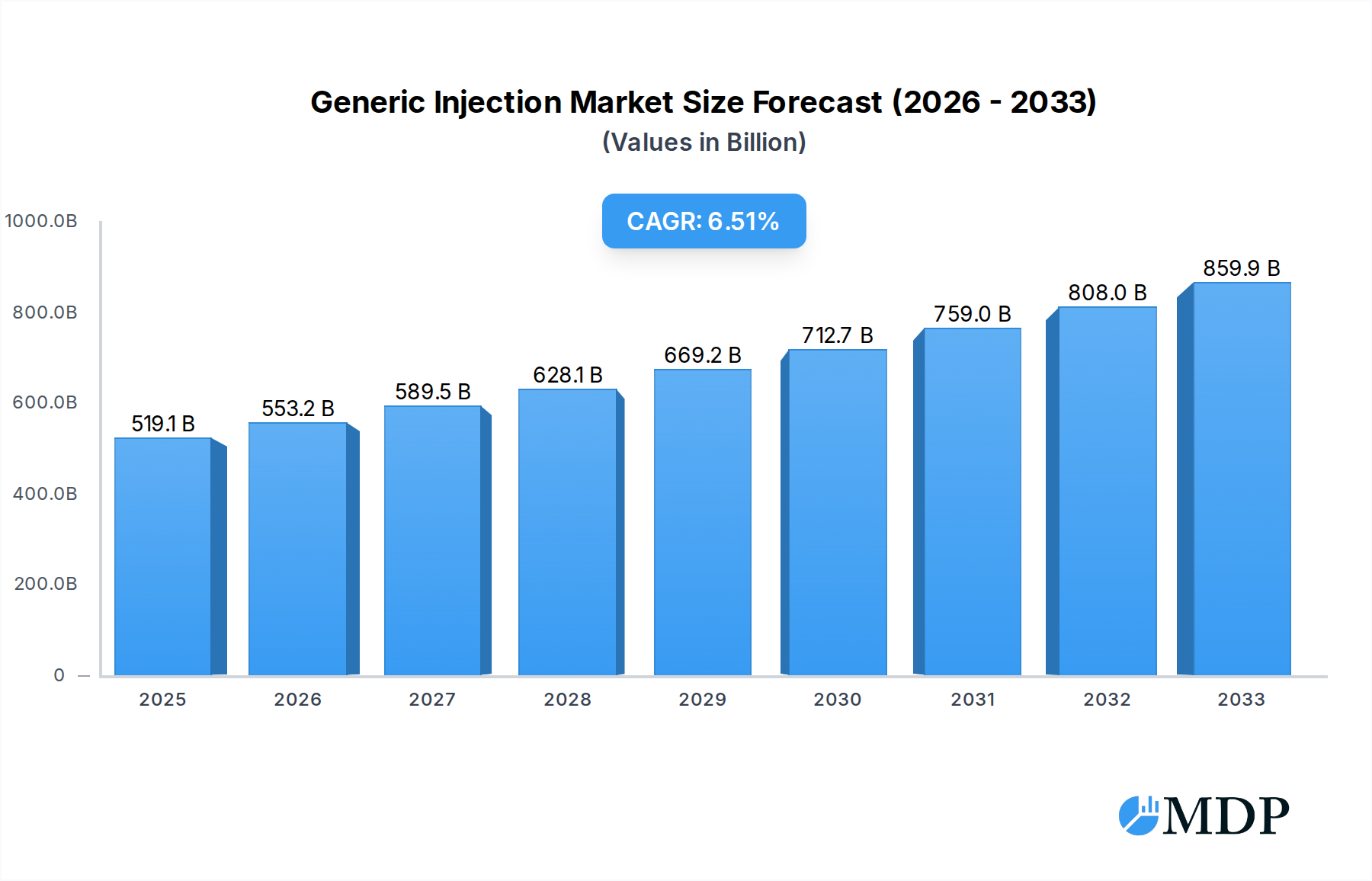

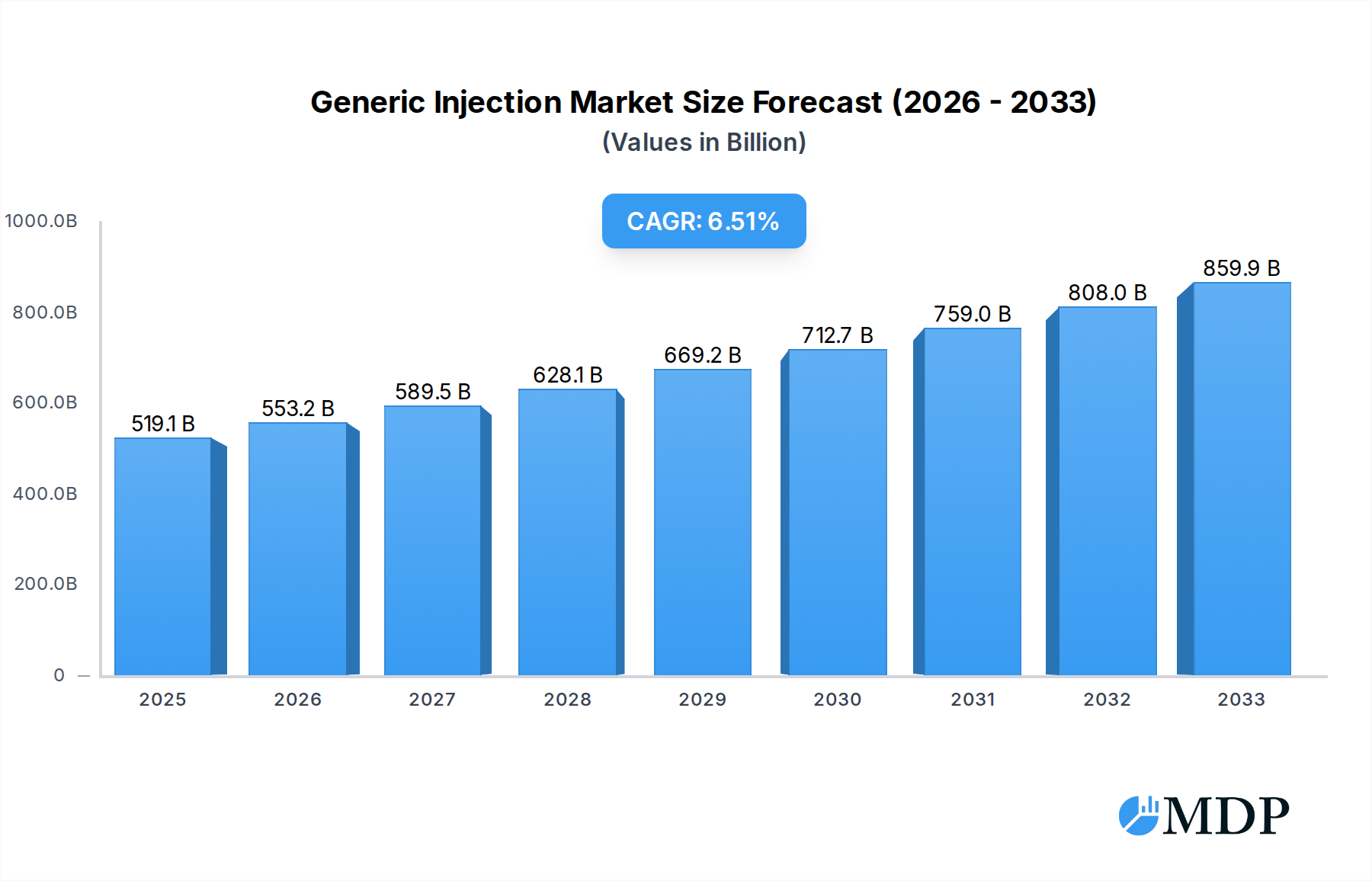

The global Generic Injection market is poised for robust expansion, projected to reach an estimated USD 519.11 billion in 2025. This growth is underpinned by a strong compound annual growth rate (CAGR) of 6.55%, indicating sustained momentum throughout the forecast period. A significant driver of this market's ascendancy is the increasing prevalence of chronic diseases worldwide, necessitating a greater demand for affordable and accessible therapeutic solutions. The aging global population further contributes to this trend, as older demographics typically require more ongoing medical treatment, including injectable medications. Furthermore, the growing pressure on healthcare systems to reduce costs, coupled with the expiry of patents on many branded drugs, creates a fertile ground for generic injectables to capture market share. Manufacturers are also investing in expanding their production capacities and developing new generic formulations, thereby enhancing product availability and affordability.

Generic Injection Market Size (In Billion)

The market is characterized by diverse applications, with hospitals representing a substantial segment due to their high volume of patient admissions and complex treatment protocols. Clinics also play a crucial role, particularly in outpatient settings and for chronic disease management. The market is further segmented by product type, with liquid injections dominating due to their ease of administration and widespread use. Powder for injection formulations, while requiring reconstitution, are essential for certain sensitive medications and offer advantages in terms of shelf-life and stability. Key players such as Sanofi, Fresenius, Viatris, Pfizer, and Teva Pharmaceuticals are actively engaged in research, development, and strategic partnerships to broaden their product portfolios and expand their geographical reach. Innovations in drug delivery systems and a focus on improving patient convenience are also emerging trends that are expected to shape the future of the generic injection market.

Generic Injection Company Market Share

Unlocking the Billion-Dollar Generic Injection Market: A Comprehensive Report (2019-2033)

Gain unparalleled insights into the rapidly expanding global Generic Injection market with this in-depth analysis. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this report provides a 360-degree view of market dynamics, trends, leading segments, and future opportunities. Essential for pharmaceutical manufacturers, investors, and healthcare providers, this report details critical market intelligence to inform your strategic decisions in this multi-billion dollar industry.

Generic Injection Market Dynamics & Concentration

The global Generic Injection market, projected to reach multi-billion dollar valuations, exhibits a moderate to high concentration, driven by established players and significant capital investment requirements. Innovation is primarily focused on cost-effective manufacturing processes, improved drug delivery systems, and bioequivalence studies to secure regulatory approvals. Regulatory frameworks, spearheaded by agencies like the FDA and EMA, play a pivotal role in market access, demanding stringent quality control and adherence to Good Manufacturing Practices (GMP). Product substitutes, while limited in the direct therapeutic sense, include alternative dosage forms or branded generics that can influence market share. End-user trends highlight a growing demand for accessible and affordable healthcare solutions, particularly in emerging economies. Mergers and Acquisitions (M&A) activity, estimated to involve several billion dollars in deal values and hundreds of transactions, is a significant driver of market consolidation and portfolio expansion, with companies like Sanofi, Viatris, and Teva Pharmaceuticals actively participating in such strategic moves to enhance their market presence and product offerings.

- Market Concentration: Moderate to High

- Innovation Drivers: Cost-efficient manufacturing, enhanced drug delivery, bioequivalence

- Regulatory Bodies: FDA, EMA, national health authorities

- End-User Trends: Demand for affordability and accessibility

- M&A Deal Count: XX (estimated)

- M&A Deal Value: XX Billion (estimated)

Generic Injection Industry Trends & Analysis

The global Generic Injection market is poised for substantial growth, driven by an aging global population, increasing prevalence of chronic diseases, and expanding healthcare access, especially in developing nations. The Compound Annual Growth Rate (CAGR) is projected to be robust, contributing significantly to the overall pharmaceutical market's multi-billion dollar expansion. Technological disruptions, such as advancements in aseptic processing, lyophilization techniques, and pre-filled syringe technology, are enhancing product stability, patient convenience, and manufacturing efficiency. Consumer preferences are increasingly leaning towards generic alternatives due to their cost-effectiveness, making them a preferred choice for healthcare providers and patients alike. Competitive dynamics are characterized by intense price competition, a strong emphasis on product quality and regulatory compliance, and strategic partnerships aimed at expanding market reach and product portfolios. Market penetration for generic injections continues to rise as healthcare systems globally seek to manage rising healthcare expenditures.

The increasing incidence of diseases such as diabetes, cardiovascular disorders, and cancer necessitates continuous and often injectable drug therapies, directly fueling the demand for generic formulations. The expiration of patents for blockbuster drugs also opens up significant opportunities for generic manufacturers to launch cost-effective alternatives, thereby increasing market access and affordability. Furthermore, government initiatives promoting the use of generic medicines to curb healthcare costs contribute significantly to market expansion. The development of more sophisticated manufacturing technologies allows for the production of complex generic injectables, including biologics, which were previously dominated by innovator companies. This shift expands the therapeutic areas covered by generic injections and presents new avenues for market growth. The shift towards home healthcare and self-administration of medications also favors the adoption of user-friendly injectable formats like pre-filled syringes and auto-injectors, which are increasingly being developed for generic drugs. The competitive landscape is dynamic, with both global pharmaceutical giants and specialized generic manufacturers vying for market share. Companies are investing heavily in research and development to not only replicate existing drugs but also to develop generics with improved pharmacokinetic profiles or extended release mechanisms. This innovation, coupled with strategic collaborations for distribution and marketing, plays a crucial role in shaping the industry's trajectory. The overall market penetration is further boosted by the expanding healthcare infrastructure in emerging economies, which is creating a larger patient base that can benefit from affordable generic injectable treatments.

Leading Markets & Segments in Generic Injection

The Generic Injection market is segmented by Application and Type, with significant regional dominance. The Hospital application segment is a primary driver, accounting for a substantial portion of the multi-billion dollar market value. This is attributed to the higher volume of injectable drug administration in inpatient settings, including critical care, surgery, and chronic disease management. Key drivers for hospital dominance include established procurement channels, the availability of specialized medical personnel for administration, and the need for immediate and potent therapeutic interventions.

- Dominant Application Segment: Hospital

- Key Drivers: High patient volume, critical care needs, established purchasing processes, physician preference for injectable efficacy.

- Economic Policies: Government reimbursements and formulary inclusions favoring generics in hospital settings significantly boost demand.

- Infrastructure: Well-equipped hospital facilities with trained staff are essential for safe and effective injection administration.

The Liquid Injection type segment holds a leading position, driven by its ease of administration, ready-to-use nature, and broad applicability across various therapeutic areas. The manufacturing processes for liquid formulations are relatively mature, contributing to their cost-effectiveness and widespread availability.

- Dominant Type Segment: Liquid Injection

- Key Drivers: Ease of administration, ready-to-use formulations, cost-effectiveness in manufacturing, wide range of therapeutic applications.

- Technological Advancements: Improvements in sterile filtration and packaging technologies enhance the shelf-life and safety of liquid injections.

- Consumer Preferences: For many acute conditions, liquid injections offer faster onset of action, a key factor in their continued dominance.

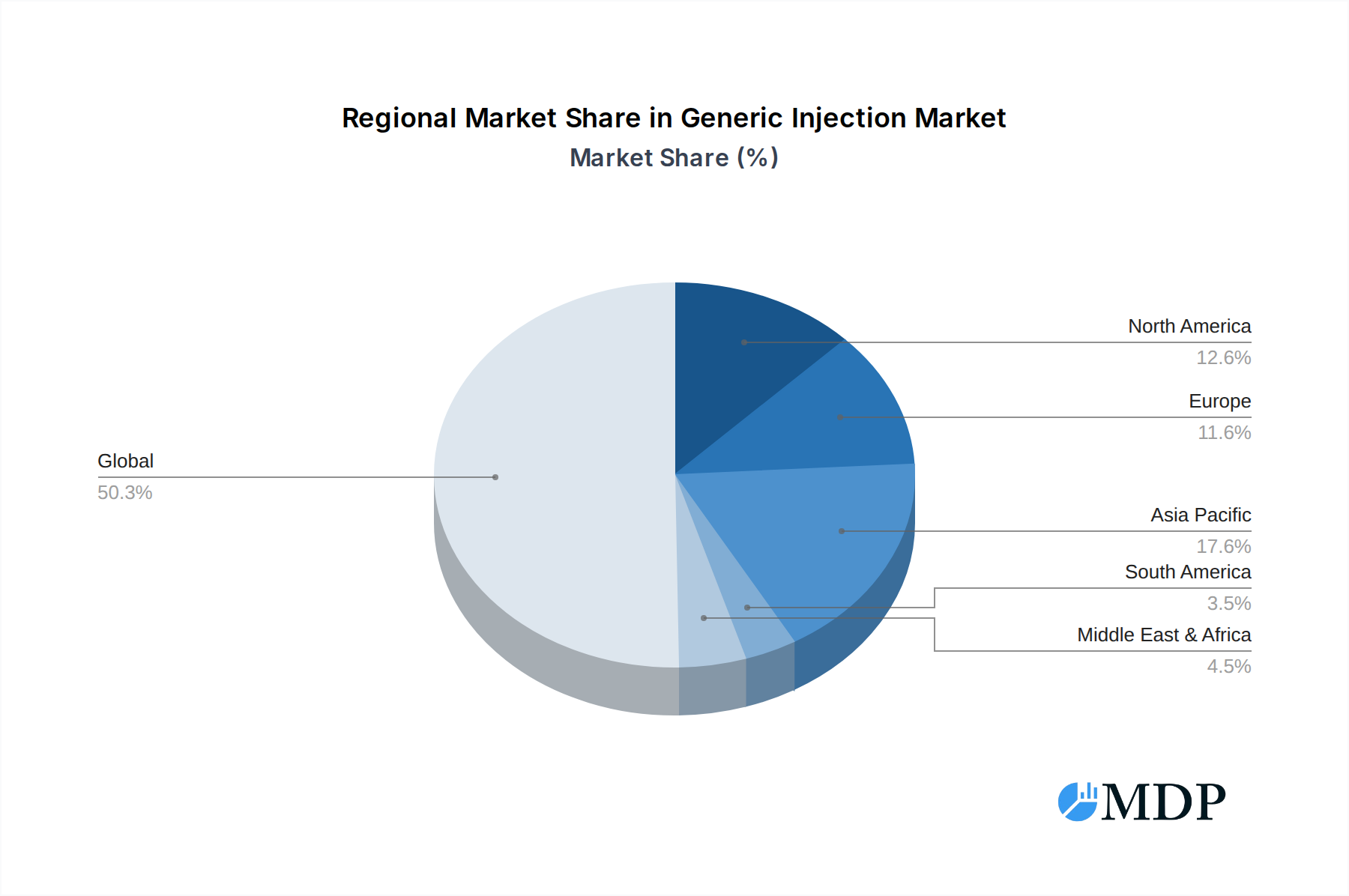

Geographically, North America and Europe currently represent the largest markets for generic injections, driven by their well-established healthcare systems, high disposable incomes, and robust regulatory frameworks that facilitate the approval and adoption of generics. However, the Asia-Pacific region is emerging as the fastest-growing market due to its large and expanding population, increasing healthcare expenditure, rising prevalence of chronic diseases, and a growing number of domestic generic manufacturers like Kelun Pharmaceutical and Jiangsu HRS.

- Dominant Regions: North America, Europe

- Fastest Growing Region: Asia-Pacific

- Economic Factors: Increasing per capita income and government spending on healthcare in Asia-Pacific.

- Demographic Shifts: Growing elderly population and rising lifestyle-related diseases in emerging markets.

- Regulatory Harmonization: Efforts towards aligning regulatory standards are facilitating market entry for generic manufacturers.

Generic Injection Product Developments

The Generic Injection market is witnessing continuous product innovation aimed at improving patient compliance and therapeutic outcomes. Companies are focusing on developing ready-to-use formulations, pre-filled syringes, and auto-injectors, offering enhanced convenience and ease of administration, particularly for self-administered medications. These developments are crucial for managing chronic conditions and reducing the burden on healthcare systems. Furthermore, advancements in drug delivery technologies are enabling the development of generics with modified-release profiles, potentially reducing dosing frequency and improving patient adherence. The focus on bioequivalence and complex generics also allows for the expansion of product portfolios into therapeutic areas previously dominated by innovator brands, creating significant market opportunities.

Key Drivers of Generic Injection Growth

The global Generic Injection market's expansion is propelled by several key factors. The patent expirations of blockbuster drugs continue to create substantial opportunities for generic manufacturers to introduce affordable alternatives, thereby increasing market accessibility and reducing healthcare costs. The growing global prevalence of chronic diseases like diabetes, cardiovascular disorders, and cancer necessitates long-term injectable therapies, driving consistent demand. Furthermore, aging global populations are more susceptible to these conditions, further amplifying the need for accessible treatments. Supportive government policies and reimbursement schemes promoting the use of generic medicines in healthcare systems worldwide play a crucial role in accelerating adoption and market penetration.

- Patent Expirations: Opening doors for affordable alternatives.

- Rising Chronic Disease Incidence: Increasing demand for long-term injectable treatments.

- Aging Global Population: Amplifying the need for accessible healthcare solutions.

- Government Initiatives: Promoting generic drug usage and cost containment.

Challenges in the Generic Injection Market

Despite its robust growth, the Generic Injection market faces several challenges. Stringent and evolving regulatory requirements for product approval, especially for complex generics and biosimil injections, can be a significant barrier, demanding substantial investment in R&D and clinical studies. Supply chain disruptions, exacerbated by geopolitical factors and raw material availability, can impact production timelines and costs, potentially leading to drug shortages. Intense price competition among numerous players can erode profit margins, making it challenging for smaller companies to sustain operations.

- Regulatory Hurdles: Complex approval processes for generics.

- Supply Chain Volatility: Risks associated with raw material sourcing and logistics.

- Price Erosion: Intense competition driving down profit margins.

Emerging Opportunities in Generic Injection

The Generic Injection market is ripe with emerging opportunities driven by technological advancements and evolving healthcare needs. The development of complex generics, including those involving challenging formulations or novel delivery systems, presents a significant growth avenue. Furthermore, the increasing focus on biosimil development for biologic drugs, which are administered via injection, offers substantial market potential. Strategic partnerships between generic manufacturers and technology providers can accelerate the development of innovative drug delivery devices, such as advanced auto-injectors and on-body injectors, enhancing patient convenience and adherence. Market expansion into underserved emerging economies, coupled with tailored product offerings, also represents a significant long-term growth catalyst.

Leading Players in the Generic Injection Sector

The global Generic Injection market is shaped by a consortium of established pharmaceutical giants and specialized generic manufacturers. These companies are instrumental in ensuring the availability of affordable and high-quality injectable medications worldwide. Key players driving innovation and market share include:

- Sanofi

- Fresenius

- Viatris

- Pfizer

- Teva Pharmaceuticals

- Hikma Pharmaceuticals

- Novartis

- Amneal Pharmaceuticals

- Gland Pharma

- Allergan

- Kelun Pharmaceutical

- Jiangsu HRS

- Qilu Pharmaceutical

- Chiatai Tianqing

- Hainan Poly Pharm

- Yangzijiang Pharmaceutical Industry

- Shijiazhuang Pharma Group

Key Milestones in Generic Injection Industry

The evolution of the Generic Injection market is marked by significant milestones that have shaped its current landscape and future trajectory. These developments, ranging from product launches to strategic alliances, underscore the dynamic nature of the industry.

- 2019: Increased regulatory focus on complex generic injectables, leading to heightened R&D investment.

- 2020: Accelerated adoption of pre-filled syringes due to pandemic-related convenience and safety concerns.

- 2021: Key patent expiries for major biologics opened avenues for biosimilar injectable development.

- 2022: Growing M&A activities aimed at portfolio diversification and market consolidation, with several billion dollar deals.

- 2023: Introduction of novel drug delivery systems for generic injectables, enhancing patient compliance.

- 2024: Enhanced supply chain resilience strategies implemented by leading manufacturers.

- 2025 (Estimated): Continued growth driven by emerging market expansion and increasing demand for affordable chronic disease management.

- 2026-2030: Anticipated surge in biosimilar launches, impacting multi-billion dollar therapeutic areas.

- 2031-2033: Maturation of advanced manufacturing technologies, leading to further cost efficiencies and product innovation.

Strategic Outlook for Generic Injection Market

The strategic outlook for the Generic Injection market remains exceptionally positive, fueled by an unwavering demand for accessible and affordable healthcare solutions. Growth accelerators include the continued pipeline of patent expirations for high-value drugs, the expanding global burden of chronic diseases, and favorable governmental policies promoting generic drug utilization. Companies are poised to capitalize on opportunities in complex generics and biosimil development, alongside strategic expansion into high-growth emerging markets. Investments in advanced manufacturing technologies and innovative drug delivery systems will be critical for maintaining a competitive edge and driving future market value in this multi-billion dollar sector.

Generic Injection Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Others

-

2. Types

- 2.1. Liquid Injection

- 2.2. Powder for Injection

Generic Injection Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Generic Injection Regional Market Share

Geographic Coverage of Generic Injection

Generic Injection REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.55% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Generic Injection Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Liquid Injection

- 5.2.2. Powder for Injection

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Generic Injection Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Liquid Injection

- 6.2.2. Powder for Injection

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Generic Injection Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Liquid Injection

- 7.2.2. Powder for Injection

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Generic Injection Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Liquid Injection

- 8.2.2. Powder for Injection

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Generic Injection Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Liquid Injection

- 9.2.2. Powder for Injection

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Generic Injection Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Liquid Injection

- 10.2.2. Powder for Injection

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Sanofi

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Fresenius

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Viatris

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Pfizer

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Teva Pharmaceuticals

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hikma Pharmaceuticals

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Novartis

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Amneal Pharmaceuticals

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Gland Pharma

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Allergan

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Kelun Pharmaceutical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Jiangsu HRS

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Qilu Pharmaceutical

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Chiatai Tianqing

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Hainan Poly Pharm

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Yangzijiang Pharmaceutical Industry

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Shijiazhuang Pharma Group

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Sanofi

List of Figures

- Figure 1: Global Generic Injection Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Generic Injection Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Generic Injection Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Generic Injection Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Generic Injection Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Generic Injection Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Generic Injection Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Generic Injection Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Generic Injection Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Generic Injection Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Generic Injection Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Generic Injection Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Generic Injection Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Generic Injection Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Generic Injection Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Generic Injection Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Generic Injection Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Generic Injection Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Generic Injection Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Generic Injection Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Generic Injection Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Generic Injection Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Generic Injection Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Generic Injection Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Generic Injection Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Generic Injection Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Generic Injection Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Generic Injection Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Generic Injection Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Generic Injection Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Generic Injection Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Generic Injection Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Generic Injection Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Generic Injection Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Generic Injection Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Generic Injection Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Generic Injection Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Generic Injection Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Generic Injection Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Generic Injection Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Generic Injection Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Generic Injection Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Generic Injection Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Generic Injection Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Generic Injection Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Generic Injection Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Generic Injection Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Generic Injection Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Generic Injection Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Generic Injection Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Generic Injection?

The projected CAGR is approximately 6.55%.

2. Which companies are prominent players in the Generic Injection?

Key companies in the market include Sanofi, Fresenius, Viatris, Pfizer, Teva Pharmaceuticals, Hikma Pharmaceuticals, Novartis, Amneal Pharmaceuticals, Gland Pharma, Allergan, Kelun Pharmaceutical, Jiangsu HRS, Qilu Pharmaceutical, Chiatai Tianqing, Hainan Poly Pharm, Yangzijiang Pharmaceutical Industry, Shijiazhuang Pharma Group.

3. What are the main segments of the Generic Injection?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Generic Injection," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Generic Injection report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Generic Injection?

To stay informed about further developments, trends, and reports in the Generic Injection, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence