Key Insights

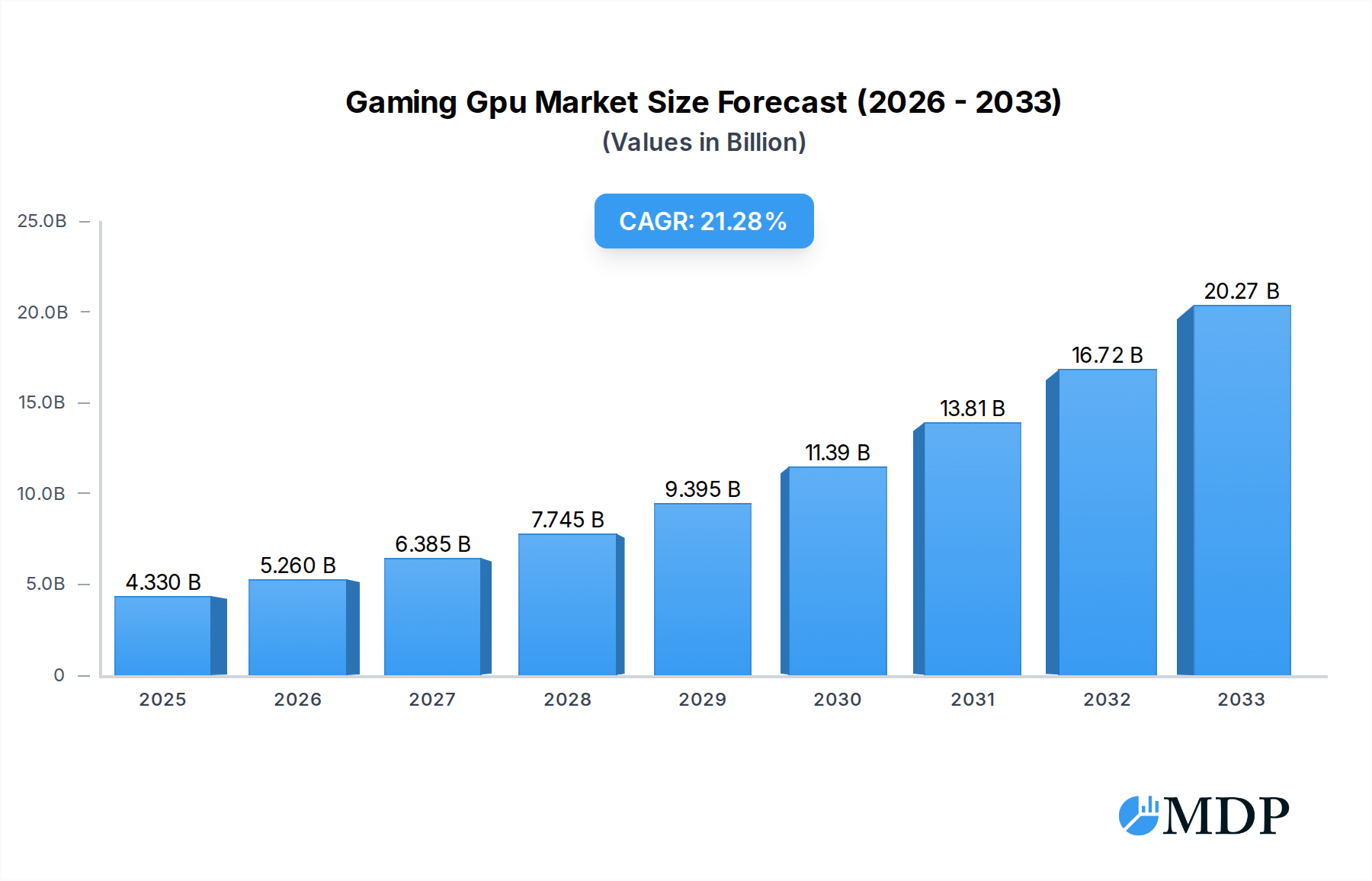

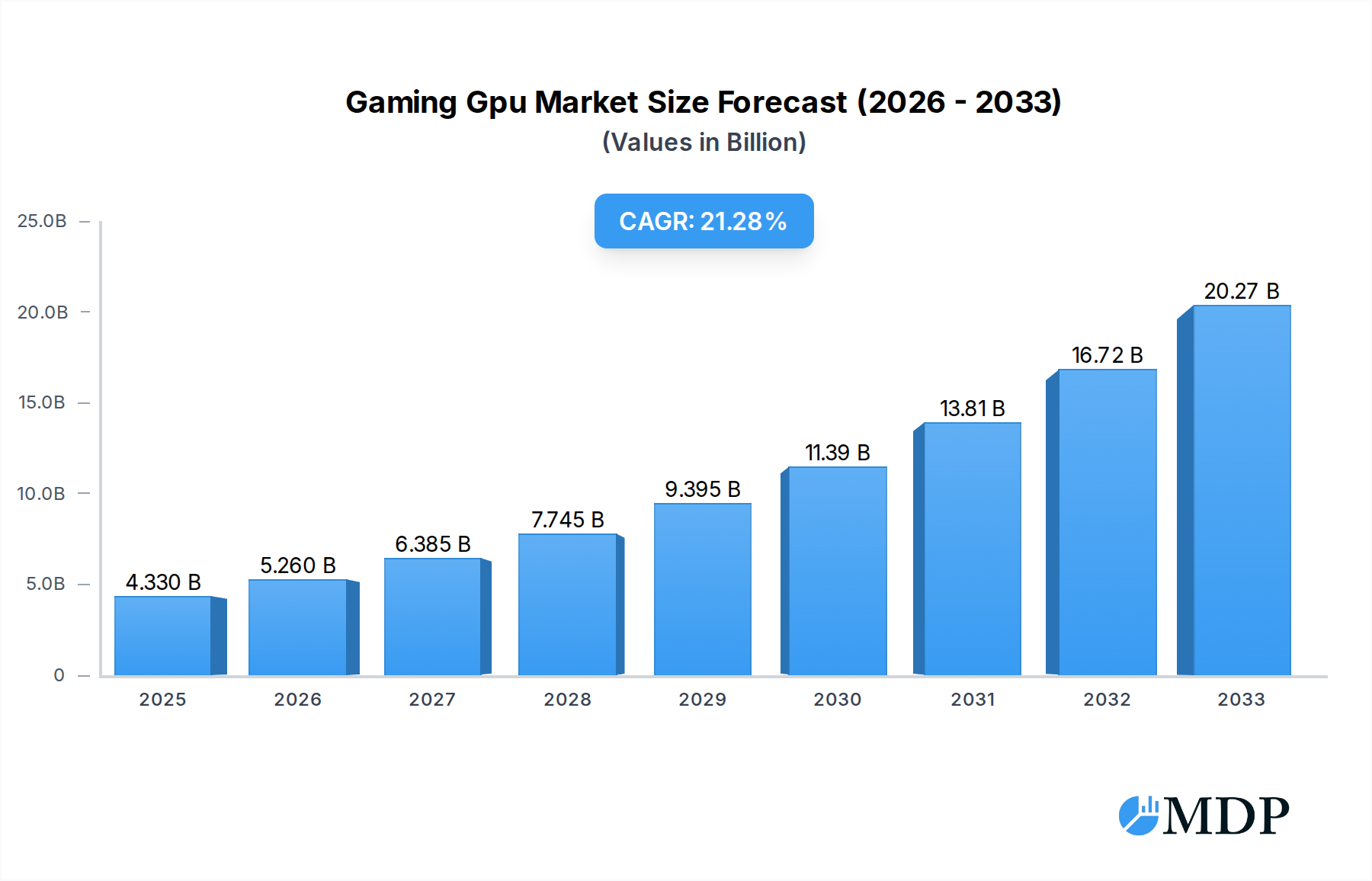

The global Gaming GPU market is experiencing a significant surge, projected to reach an impressive $4.33 billion by 2025. This robust growth is fueled by an exceptionally high Compound Annual Growth Rate (CAGR) of 21.4%, indicating a dynamic and rapidly expanding sector. The primary drivers behind this expansion include the escalating demand for high-fidelity gaming experiences, the increasing adoption of esports globally, and the continuous innovation in graphics technology that enables more immersive and realistic gameplay. The proliferation of powerful gaming consoles, coupled with the growing popularity of PCs and workstations for gaming, further solidifies the market's upward trajectory. Furthermore, the persistent evolution of virtual reality (VR) and augmented reality (AR) technologies, which heavily rely on advanced graphics processing, is also contributing to the robust market performance.

Gaming Gpu Market Size (In Billion)

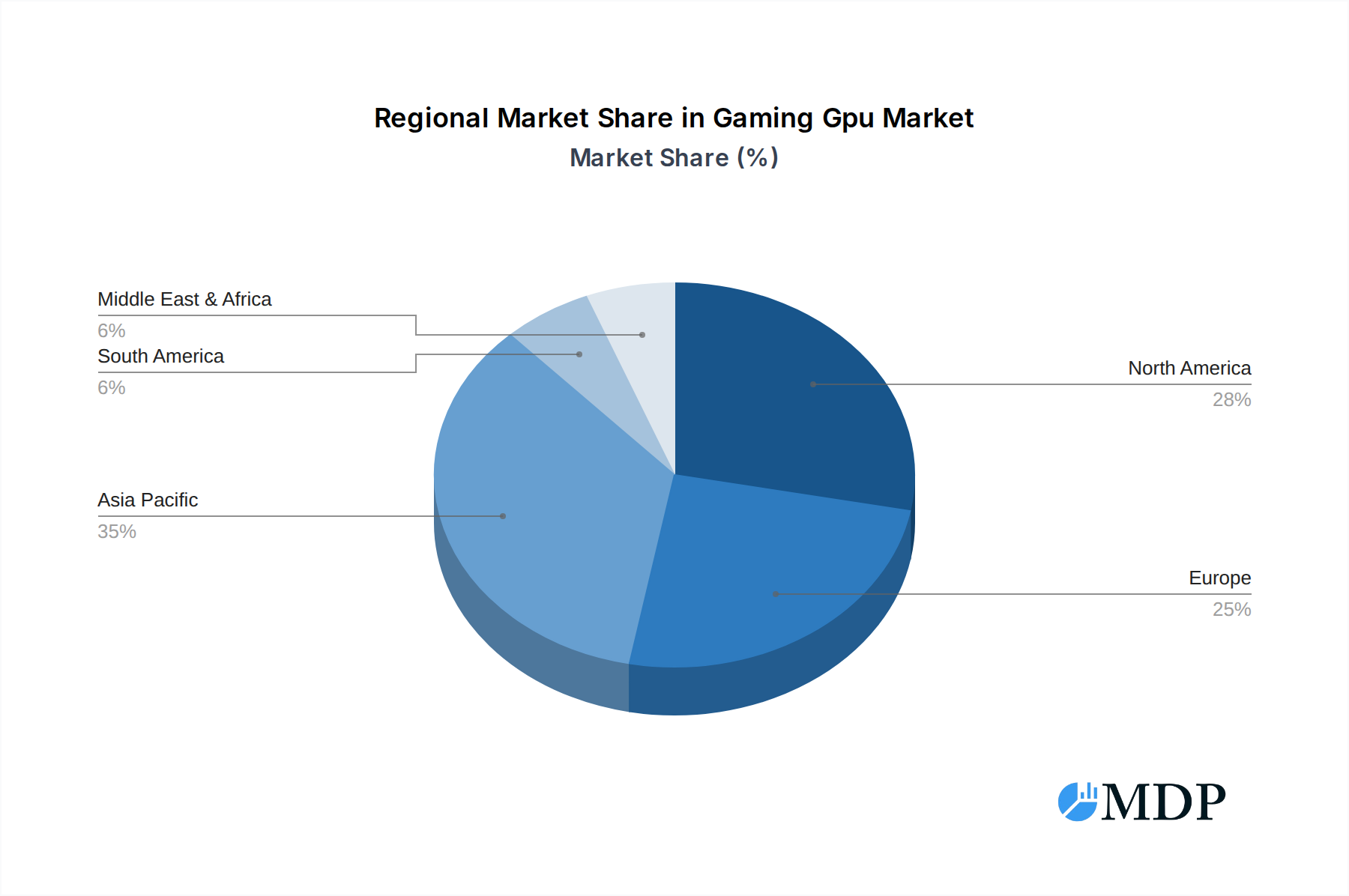

The market is segmented into two primary types: Dedicated Graphic Cards and Integrated Graphics Solutions, with dedicated cards dominating due to their superior performance capabilities for demanding gaming titles. By application, Mobile Devices, PCs and Workstations, and Gaming Consoles represent the key segments, each exhibiting strong growth. Leading companies like Intel Corporation, Advanced Micro Devices Inc., and Nvidia Corporation are at the forefront of this innovation, introducing cutting-edge GPUs that cater to the evolving needs of gamers. The market's expansion is global, with Asia Pacific, North America, and Europe showing particular strength due to significant gaming populations and high disposable incomes. Despite the immense growth, potential restraints such as the rising cost of high-end GPUs and supply chain disruptions could pose challenges, though the overall outlook remains overwhelmingly positive.

Gaming Gpu Company Market Share

Unveiling the Powerhouse of Digital Entertainment: Gaming GPU Market Dynamics and Future Trajectories

This in-depth report provides an indispensable analysis of the global Gaming GPU market, forecasting its trajectory from 2019 to 2033, with a base and estimated year of 2025. Delving into intricate market dynamics, technological advancements, and evolving consumer preferences, this report offers actionable insights for stakeholders navigating this rapidly expanding sector. With an estimated market size projected to reach billions of USD by 2033, understanding the forces shaping this industry is paramount.

Gaming Gpu Market Dynamics & Concentration

The global Gaming GPU market exhibits a dynamic and evolving concentration, driven by relentless innovation and strategic consolidations. Nvidia Corporation and Advanced Micro Devices Inc. continue to dominate, commanding significant market shares, estimated to be in the high billions of USD in revenue each. Intel Corporation is strategically increasing its presence, particularly in the integrated graphics segment, aiming to capture a substantial portion of the market valued in the billions of USD. ASUSTEK Computer Inc. and GIGA-BYTE Technology Co., Ltd., as key board partners, play a crucial role in the ecosystem, with their combined revenue from graphics card sales reaching billions of USD. Arm Limited and Qualcomm Technologies Inc. are making significant inroads into mobile and integrated GPU solutions, representing a growing market segment valued in the billions of USD.

Key dynamics influencing market concentration include:

- Innovation Drivers: The insatiable demand for higher frame rates, enhanced graphical fidelity (e.g., ray tracing, AI-powered upscaling), and immersive experiences fuels continuous R&D. This is evidenced by the billions of USD invested annually by leading companies in research and development.

- Regulatory Frameworks: While generally supportive, evolving regulations around energy efficiency and environmental impact could influence future product design and manufacturing, impacting costs in the billions of USD.

- Product Substitutes: Integrated graphics solutions are becoming increasingly powerful, posing a challenge to the dedicated GPU market, especially for entry-level and mainstream gaming, representing a market segment in the billions of USD.

- End-User Trends: The rise of cloud gaming, esports, and the increasing adoption of high-resolution displays (4K, 8K) are directly influencing GPU demand, contributing to billions of USD in market value.

- M&A Activities: Strategic acquisitions and partnerships, with deal values often in the billions of USD, are shaping the competitive landscape. For instance, the acquisition of chip design firms or companies with specialized AI or graphics technologies could significantly alter market shares. M&A deal counts are expected to remain robust, reflecting ongoing consolidation efforts, with several billion-dollar transactions anticipated.

Gaming Gpu Industry Trends & Analysis

The Gaming GPU industry is experiencing robust growth, driven by a confluence of technological advancements, evolving consumer preferences, and expanding market penetration. The Compound Annual Growth Rate (CAGR) for the global Gaming GPU market is projected to be in the healthy range of XX% over the forecast period (2025–2033), translating into a market size estimated to reach well over billions of USD by 2033. This growth is intrinsically linked to the increasing affordability and accessibility of high-performance computing, as well as the ever-growing demand for immersive and visually stunning gaming experiences across various platforms.

Technological disruptions are at the forefront of this expansion. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into GPU architectures is revolutionizing rendering capabilities, enabling technologies like AI-powered upscaling (e.g., DLSS, FSR) that boost frame rates and visual quality without significant hardware upgrades. This has led to a significant increase in the adoption of dedicated graphics cards, which are projected to hold a substantial market share in the billions of USD. Furthermore, advancements in ray tracing hardware have unlocked unprecedented levels of realism in lighting, shadows, and reflections, becoming a key selling point for new GPU releases and driving upgrades among enthusiast gamers. The development of new fabrication processes, allowing for smaller and more power-efficient chips, is also a critical factor, enabling manufacturers like Nvidia Corporation, Advanced Micro Devices Inc., and Intel Corporation to pack more performance into their offerings.

Consumer preferences are also playing a pivotal role. The rise of esports has created a massive and engaged audience demanding high refresh rates and competitive advantage, driving the sales of performance-oriented GPUs. Simultaneously, the mainstream gaming market is witnessing an increased demand for higher resolutions and graphical fidelity, pushing consumers towards more capable hardware. The increasing popularity of virtual reality (VR) and augmented reality (AR) technologies, while still nascent in widespread adoption, represents a significant future growth driver, requiring substantial graphical processing power, adding billions of dollars to the market potential.

Competitive dynamics are intensifying. Beyond the established players, emerging companies and the strategic alliances formed between hardware manufacturers, game developers, and platform holders are shaping the market. The battle for market share is fierce, with companies investing billions of dollars in R&D and marketing to secure their position. Arm Limited and Qualcomm Technologies Inc. are increasingly challenging the traditional GPU duopoly with their advanced mobile and integrated graphics solutions, particularly impacting the market for entry-level gaming PCs and mobile gaming devices, a segment collectively valued in the billions of USD. The focus on power efficiency and thermal management is also becoming a key differentiator, especially for gaming laptops and mobile devices. The continuous innovation in driver software and optimization for popular game titles further enhances the user experience and brand loyalty, contributing to the sustained growth of the Gaming GPU market, estimated to exceed billions of USD in the coming years.

Leading Markets & Segments in Gaming Gpu

The global Gaming GPU market is characterized by distinct regional strengths and segment dominance, offering significant opportunities for market players. Among the various segments, PCs and Workstations represent the largest and most mature market, driven by dedicated gamers and content creators. The market for high-performance gaming PCs, where dedicated graphics cards are essential, is projected to account for a substantial portion of the global market, estimated to be in the billions of USD annually. This dominance is fueled by the consistent release of graphically intensive PC games, the popularity of esports requiring top-tier performance, and the increasing integration of GPUs in professional workloads beyond gaming.

Within the Application segment:

PCs and Workstations: This segment is the primary driver of demand for high-end dedicated GPUs. Factors contributing to its leadership include:

- Economic Policies: Favorable economic conditions and disposable income in developed regions like North America and Europe enable consumers to invest in premium gaming hardware, contributing billions to the market.

- Infrastructure: Widespread availability of high-speed internet is crucial for downloading large game files and engaging in online multiplayer, supporting the growth of PC gaming.

- Technological Advancement: Continuous innovation in PC hardware, including faster CPUs, more RAM, and advanced cooling solutions, creates a synergistic environment for high-performance GPUs.

- Content Availability: A vast and ever-expanding library of PC games, with titles frequently pushing graphical boundaries, ensures sustained demand for powerful graphics cards.

Mobile Devices: While not directly driven by dedicated GPUs in the traditional sense, the processing power of SoCs (System on a Chip) with integrated graphics from companies like Qualcomm Technologies Inc. and Arm Limited is critical for mobile gaming. This segment is experiencing explosive growth, valued in the billions of USD, and is increasingly demanding more sophisticated mobile GPU capabilities.

Gaming Consoles: Console gaming, led by platforms from Sony Interactive Entertainment and Microsoft, represents another significant market segment for GPUs, although these are typically custom-designed integrated solutions rather than off-the-shelf components. The console market's consistent demand for powerful graphics, essential for delivering cinematic gaming experiences, contributes billions of USD to the overall GPU ecosystem.

Others: This category encompasses emerging applications like cloud gaming hardware, AI accelerators with gaming capabilities, and specialized gaming devices, representing a smaller but rapidly growing niche.

Within the Type segment:

- Dedicated Graphic Cards: This remains the cornerstone of high-performance gaming, with market revenue estimated in the billions of USD. Companies like Nvidia Corporation, Advanced Micro Devices Inc., and historically, EVGA Corporation and SAPPHIRE Technology Limited, are key players in this segment. The continuous evolution of architectures and feature sets like ray tracing and AI upscaling solidifies their dominance for enthusiast gamers.

- Integrated Graphics Solutions: Driven by advancements from Intel Corporation, Qualcomm Technologies Inc., and Arm Limited, integrated graphics are becoming increasingly capable, catering to a wider audience and lower-power devices. This segment is crucial for budget-conscious gamers and the mobile gaming market.

- Others: This includes specialized GPU solutions for embedded systems or unique gaming form factors.

The dominance of the PCs and Workstations segment, particularly for Dedicated Graphic Cards, is projected to continue through the forecast period, driven by the unwavering demand for cutting-edge gaming experiences and the ongoing investment in PC gaming infrastructure by billions of enthusiasts worldwide.

Gaming Gpu Product Developments

The Gaming GPU landscape is in a perpetual state of flux, marked by relentless product innovation aimed at delivering superior gaming experiences. Key developments focus on enhancing raw processing power, integrating advanced rendering technologies, and optimizing for efficiency. Companies like Nvidia Corporation and Advanced Micro Devices Inc. are consistently pushing the boundaries with new architectures that offer significant generational leaps in performance, often measured in billions of teraflops. The widespread adoption of real-time ray tracing, first popularized by Nvidia and now a competitive feature from AMD, has transformed visual fidelity, enabling more realistic lighting and reflections. Furthermore, AI-driven technologies such as DLSS (Deep Learning Super Sampling) and FSR (FidelityFX Super Resolution) are proving crucial, allowing for higher frame rates at higher resolutions with minimal perceived loss in image quality. These innovations provide a compelling competitive advantage by offering gamers enhanced performance and visual immersion, directly impacting the billions of USD spent on gaming hardware annually.

Key Drivers of Gaming Gpu Growth

The Gaming GPU market is propelled by a confluence of potent drivers, ensuring sustained growth in the coming years.

- Technological Advancements: The relentless pursuit of higher frame rates, photorealistic graphics, and immersive experiences fuels continuous innovation in GPU architectures, including advancements in ray tracing, AI upscaling, and increased processing power, representing billions of dollars in R&D investment.

- Growing Esports and Gaming Popularity: The global rise of competitive esports and the increasing adoption of gaming as a primary entertainment form across demographics create a perpetual demand for high-performance hardware, contributing billions to the market.

- Increasing PC and Console Gaming Penetration: The expanding accessibility of gaming PCs and consoles, particularly in emerging markets, coupled with the affordability of entry-level to mid-range GPUs, broadens the consumer base, driving volume sales in the billions.

- Demand for High-Resolution Displays and VR/AR: The adoption of 4K, 8K displays, and the burgeoning virtual and augmented reality markets necessitate increasingly powerful GPUs, creating significant demand for premium graphics cards valued in the billions.

- Content Creation and Streaming: The surge in content creation, game streaming, and professional applications that leverage GPU acceleration further diversifies the demand for these powerful components, adding billions to the overall market value.

Challenges in the Gaming Gpu Market

Despite robust growth, the Gaming GPU market faces several significant challenges that could impact its trajectory.

- Supply Chain Disruptions: Volatility in the global semiconductor supply chain, as experienced in recent years, can lead to product shortages and price inflation, hindering sales and impacting billions of dollars in potential revenue.

- Rising Component Costs: The increasing complexity and advanced manufacturing processes required for high-end GPUs contribute to escalating production costs, which can translate to higher retail prices and potentially dampen consumer demand for entry-level to mid-range segments, impacting billions of dollars in consumer spending.

- Intensifying Competition and Market Saturation: While innovation drives demand, intense competition among major players like Nvidia Corporation and Advanced Micro Devices Inc. can lead to price wars and reduced profit margins, affecting the billions in revenue.

- Cryptocurrency Mining Fluctuations: While less of a factor recently, periods of high cryptocurrency prices have historically led to significant demand for GPUs, diverting stock away from gamers and creating artificial scarcity and price hikes, impacting billions in gamer budgets.

- Economic Downturns and Consumer Spending: Global economic recessions or downturns can significantly reduce discretionary spending on high-ticket items like gaming GPUs, impacting billions of dollars in anticipated sales.

Emerging Opportunities in Gaming Gpu

The Gaming GPU market is ripe with emerging opportunities, fueled by technological breakthroughs and strategic market expansion.

- Advancements in AI and Machine Learning: The integration of AI in GPUs for gaming, such as predictive rendering and intelligent upscaling, presents a significant growth avenue, promising enhanced performance and visual fidelity, and potentially unlocking billions in new market value.

- Growth of Cloud Gaming Platforms: As cloud gaming matures, the demand for powerful server-grade GPUs will surge, creating a substantial new market segment valued in the billions of USD and offering opportunities for specialized hardware solutions.

- Expansion into Emerging Markets: Untapped potential in developing economies, where gaming is gaining popularity, offers significant opportunities for market expansion, especially for more accessible and cost-effective GPU solutions, contributing billions to future market growth.

- Metaverse and Extended Reality (XR) Development: The nascent but rapidly evolving metaverse and XR technologies will require immense graphical processing power, paving the way for next-generation GPUs designed for immersive digital experiences, a future market worth billions.

- Strategic Partnerships and Ecosystem Development: Collaborations between GPU manufacturers, game developers, and platform providers can accelerate innovation and create more integrated gaming ecosystems, fostering loyalty and driving sustained sales in the billions.

Leading Players in the Gaming Gpu Sector

- Nvidia Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- ASUSTEK Computer Inc

- GIGA-BYTE Technology Co., Ltd.

- Arm Limited

- Qualcomm Technologies Inc.

- Imagination Technologies Group

- SAPPHIRE Technology Limited

Key Milestones in Gaming Gpu Industry

- 2019: Launch of Nvidia GeForce RTX 20 series, popularizing real-time ray tracing.

- 2020: Release of AMD Radeon RX 6000 series, challenging Nvidia's performance dominance.

- 2020: Introduction of Nvidia DLSS 2.0, significantly improving AI upscaling performance.

- 2021: Continued global chip shortages impacting GPU availability and pricing.

- 2022: AMD announces its acquisition of Xilinx, strengthening its position in adaptive computing.

- 2022: Intel launches its first dedicated Arc Alchemist GPUs, entering the discrete graphics market.

- 2023: Nvidia launches its RTX 40 series, featuring Ada Lovelace architecture and enhanced AI capabilities.

- 2024: AMD introduces its RDNA 3 architecture, focusing on efficiency and performance gains.

- 2024-2025: Expected increase in GPU integration in laptops and mobile devices with improved power efficiency.

- 2025-2033: Anticipated growth in AI-powered graphics features and cloud gaming infrastructure.

Strategic Outlook for Gaming Gpu Market

The strategic outlook for the Gaming GPU market remains exceptionally bright, driven by a robust pipeline of technological innovation and expanding consumer engagement. Growth accelerators will include the continuous refinement of AI-driven rendering techniques, the increasing demand for higher fidelity in virtual and augmented reality experiences, and the proliferation of cloud gaming services requiring powerful server-side GPUs. The strategic focus for leading players like Nvidia Corporation and Advanced Micro Devices Inc. will likely center on differentiating through superior performance, power efficiency, and integrated AI capabilities, aiming to capture a larger share of the billions of dollars projected for the market. Furthermore, the expansion into emerging markets and the development of specialized GPU solutions for new applications beyond traditional gaming will be crucial for sustained long-term growth and profitability in this dynamic sector.

Gaming Gpu Segmentation

-

1. Application

- 1.1. Mobile Devices

- 1.2. PCs and Workstations

- 1.3. Gaming Consoles

- 1.4. Others

-

2. Type

- 2.1. Dedicated Graphic Cards

- 2.2. Integrated Graphics Solutions

- 2.3. Others

Gaming Gpu Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Gaming Gpu Regional Market Share

Geographic Coverage of Gaming Gpu

Gaming Gpu REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Gaming Gpu Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Mobile Devices

- 5.1.2. PCs and Workstations

- 5.1.3. Gaming Consoles

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Dedicated Graphic Cards

- 5.2.2. Integrated Graphics Solutions

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Gaming Gpu Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Mobile Devices

- 6.1.2. PCs and Workstations

- 6.1.3. Gaming Consoles

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Dedicated Graphic Cards

- 6.2.2. Integrated Graphics Solutions

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Gaming Gpu Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Mobile Devices

- 7.1.2. PCs and Workstations

- 7.1.3. Gaming Consoles

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Dedicated Graphic Cards

- 7.2.2. Integrated Graphics Solutions

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Gaming Gpu Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Mobile Devices

- 8.1.2. PCs and Workstations

- 8.1.3. Gaming Consoles

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Dedicated Graphic Cards

- 8.2.2. Integrated Graphics Solutions

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Gaming Gpu Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Mobile Devices

- 9.1.2. PCs and Workstations

- 9.1.3. Gaming Consoles

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Dedicated Graphic Cards

- 9.2.2. Integrated Graphics Solutions

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Gaming Gpu Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Mobile Devices

- 10.1.2. PCs and Workstations

- 10.1.3. Gaming Consoles

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Dedicated Graphic Cards

- 10.2.2. Integrated Graphics Solutions

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Intel Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Advanced Micro Devices Inc.

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Nvidia Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ASUSTEK Computer Inc

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 GIGA-BYTE Technology Co. Ltd.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Arm Limited

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Qualcomm Technologies Inc.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Imagination Technologies Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 EVGA Corporation

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 SAPPHIRE Technology Limited

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Intel Corporation

List of Figures

- Figure 1: Global Gaming Gpu Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Gaming Gpu Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Gaming Gpu Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Gaming Gpu Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Gaming Gpu Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Gaming Gpu Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Gaming Gpu Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Gaming Gpu Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Gaming Gpu Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Gaming Gpu Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Gaming Gpu Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Gaming Gpu Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Gaming Gpu Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Gaming Gpu Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Gaming Gpu Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Gaming Gpu Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Gaming Gpu Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Gaming Gpu Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Gaming Gpu Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Gaming Gpu Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Gaming Gpu Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Gaming Gpu Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Gaming Gpu Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Gaming Gpu Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Gaming Gpu Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Gaming Gpu Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Gaming Gpu Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Gaming Gpu Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Gaming Gpu Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Gaming Gpu Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Gaming Gpu Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Gaming Gpu Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Gaming Gpu Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Gaming Gpu Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Gaming Gpu Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Gaming Gpu Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Gaming Gpu Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Gaming Gpu Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Gaming Gpu Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Gaming Gpu Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Gaming Gpu Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Gaming Gpu Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Gaming Gpu Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Gaming Gpu Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Gaming Gpu Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Gaming Gpu Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Gaming Gpu Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Gaming Gpu Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Gaming Gpu Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Gaming Gpu Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gaming Gpu?

The projected CAGR is approximately 21.4%.

2. Which companies are prominent players in the Gaming Gpu?

Key companies in the market include Intel Corporation, Advanced Micro Devices Inc., Nvidia Corporation, ASUSTEK Computer Inc, GIGA-BYTE Technology Co., Ltd., Arm Limited, Qualcomm Technologies Inc., Imagination Technologies Group, EVGA Corporation, SAPPHIRE Technology Limited.

3. What are the main segments of the Gaming Gpu?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gaming Gpu," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gaming Gpu report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gaming Gpu?

To stay informed about further developments, trends, and reports in the Gaming Gpu, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence