Key Insights

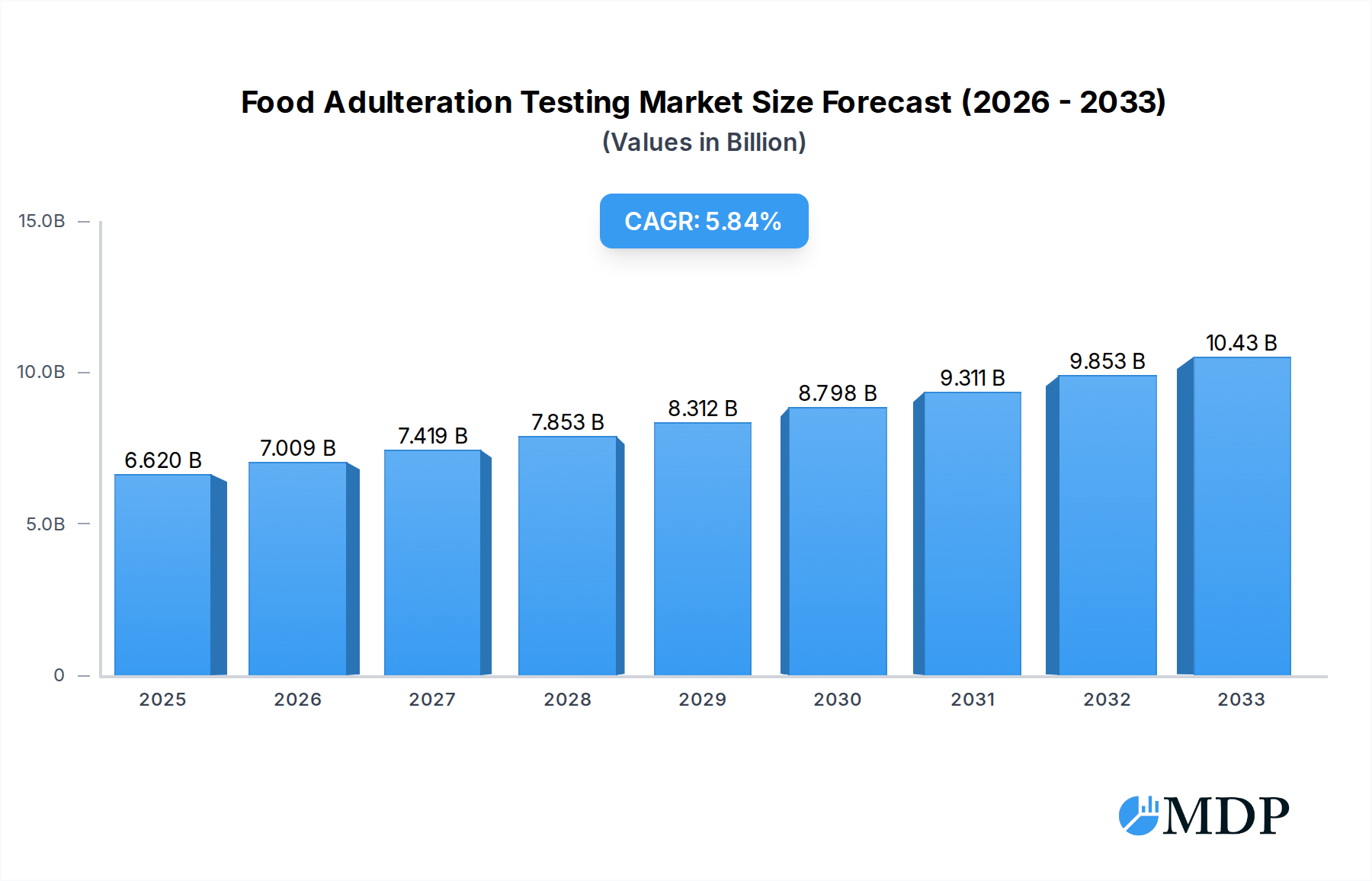

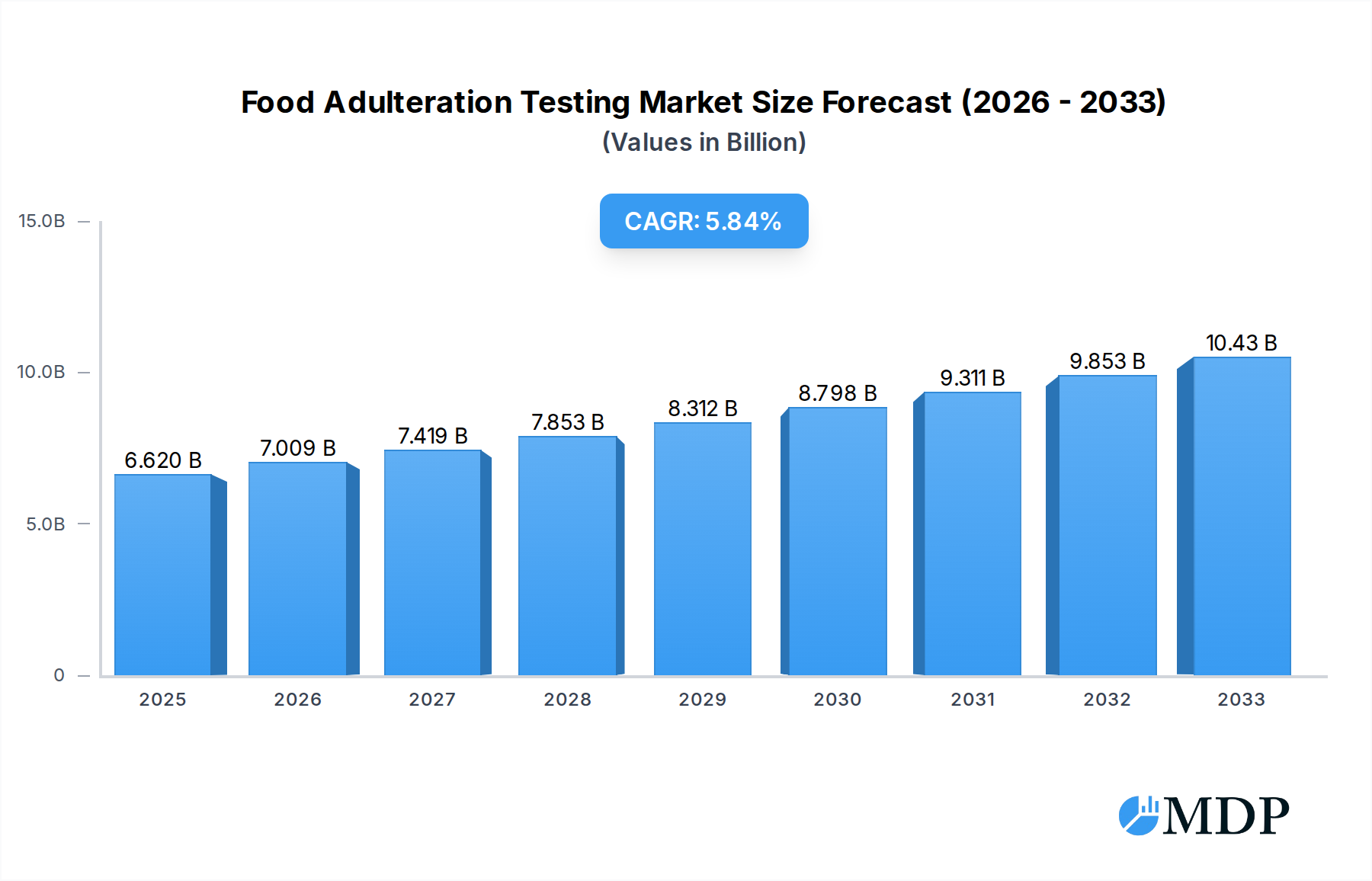

The global Food Adulteration Testing market is poised for significant expansion, projected to reach a substantial USD 6.62 billion in 2025. This robust growth is fueled by an anticipated Compound Annual Growth Rate (CAGR) of 5.5% over the forecast period of 2025-2033. The increasing consumer awareness regarding food safety, coupled with stringent regulatory frameworks implemented by governments worldwide, are primary catalysts driving demand for advanced testing solutions. Furthermore, the rising incidence of food fraud and adulteration incidents, often driven by economic motives, necessitates sophisticated analytical techniques to ensure product integrity and consumer health. Advancements in analytical technologies, such as the proliferation of high-performance liquid chromatography (HPLC) and high-performance thin-layer chromatography (HPTLC), are offering more accurate and efficient methods for detecting a wider range of adulterants, thereby stimulating market growth. The trend towards greater transparency in the food supply chain, amplified by social media and consumer advocacy groups, also plays a crucial role in pushing for more rigorous testing protocols.

Food Adulteration Testing Market Size (In Billion)

The market is segmented into key technologies, with High-Performance Liquid Chromatography (HPLC) and High Performance Thin Layer Chromatography (HPTLC) dominating the landscape due to their precision and versatility in identifying a broad spectrum of contaminants and adulterants. The 'Others' category likely encompasses newer technologies and methods gaining traction. Applications span across both Enterprise and Individual segments, reflecting the broad need for food safety assurance, from large-scale food manufacturers and regulatory bodies to individual consumers concerned about the quality of their food. Major industry players like Eurofins, SGS, Intertek, and Neogen are actively investing in research and development to enhance their testing capabilities and expand their service offerings, catering to the dynamic needs of the global food industry. Emerging markets, particularly in the Asia Pacific region, are expected to contribute significantly to market growth due to rapid industrialization and increasing disposable incomes, leading to higher consumption of processed foods and a greater emphasis on their safety.

Food Adulteration Testing Company Market Share

Here's an SEO-optimized and engaging report description for Food Adulteration Testing, incorporating high-traffic keywords and structured as requested.

Food Adulteration Testing Market Dynamics & Concentration

The global food adulteration testing market is characterized by a moderate to high concentration, driven by a growing awareness of food safety and increasing regulatory scrutiny. Key innovation drivers include advancements in analytical technologies for food analysis, such as High-Performance Liquid Chromatography (HPLC) and High Performance Thin Layer Chromatography (HPTLC), which enhance the speed, accuracy, and breadth of detection for various adulterants. Stringent food safety regulations worldwide are compelling food businesses to invest significantly in these testing services. Product substitutes, while present in the form of manual testing or less sophisticated equipment, are being rapidly outpaced by the precision and reliability of advanced methods. End-user trends reveal a growing demand from enterprise clients in the food manufacturing, processing, and retail sectors, alongside an increasing demand for individual consumer protection. Mergers and acquisitions (M&A) activities are notable, with companies like Eurofins, SGS, and Intertek Group actively consolidating their positions through strategic acquisitions to expand their service portfolios and geographical reach. The market anticipates a substantial increase in M&A deal counts as larger players seek to acquire specialized capabilities and smaller, innovative firms. Forecasts suggest a continued trend of consolidation, impacting market share distribution across key players like Auriga Research, Neogen, AMMAGENOMICS, Anacon Laboratories, PurityPortal, ALS, and SCIEX.

Food Adulteration Testing Industry Trends & Analysis

The food adulteration testing industry is poised for significant expansion, propelled by a confluence of robust growth drivers, transformative technological disruptions, evolving consumer preferences, and intense competitive dynamics. Over the study period of 2019–2033, the market is expected to exhibit a compound annual growth rate (CAGR) of approximately XX%, reflecting sustained demand for reliable food safety solutions. One of the primary growth drivers is the escalating global population and the subsequent increase in food production and consumption, which inherently raises the stakes for ensuring food integrity. Furthermore, the rise in complex global food supply chains has amplified the risk of adulteration, necessitating more sophisticated and frequent testing protocols.

Technological advancements are revolutionizing the food testing services landscape. Innovations in techniques like High-Performance Liquid Chromatography (HPLC), High Performance Thin Layer Chromatography (HPTLC), and Mass Spectrometry are enabling the detection of even trace levels of contaminants and adulterants, including undeclared ingredients, synthetic dyes, and banned substances. The integration of AI and machine learning in data analysis is further enhancing the efficiency and predictive capabilities of these testing methods.

Consumer preferences are increasingly shifting towards transparency and safety. Consumers are more informed and demanding about the origin and composition of their food, actively seeking products verified for authenticity and free from harmful adulterants. This heightened consumer awareness translates into greater pressure on food businesses to implement comprehensive food quality control measures, thereby boosting the demand for specialized testing services.

Competitive dynamics within the food adulteration testing market are characterized by intense rivalry among established global players and emerging specialized laboratories. Companies are differentiating themselves through the development of rapid, on-site testing solutions, expanding their accreditations, and offering comprehensive service packages covering a wide range of adulterants and food matrices. The food testing market penetration is expected to deepen, especially in developing economies where regulatory frameworks are strengthening and consumer awareness is rising. Strategic partnerships between technology providers and testing laboratories, as well as collaborations with regulatory bodies, are becoming more prevalent to address the evolving challenges and opportunities in ensuring food authenticity and safety. The increasing focus on food fraud detection and prevention will further fuel the growth of this vital sector.

Leading Markets & Segments in Food Adulteration Testing

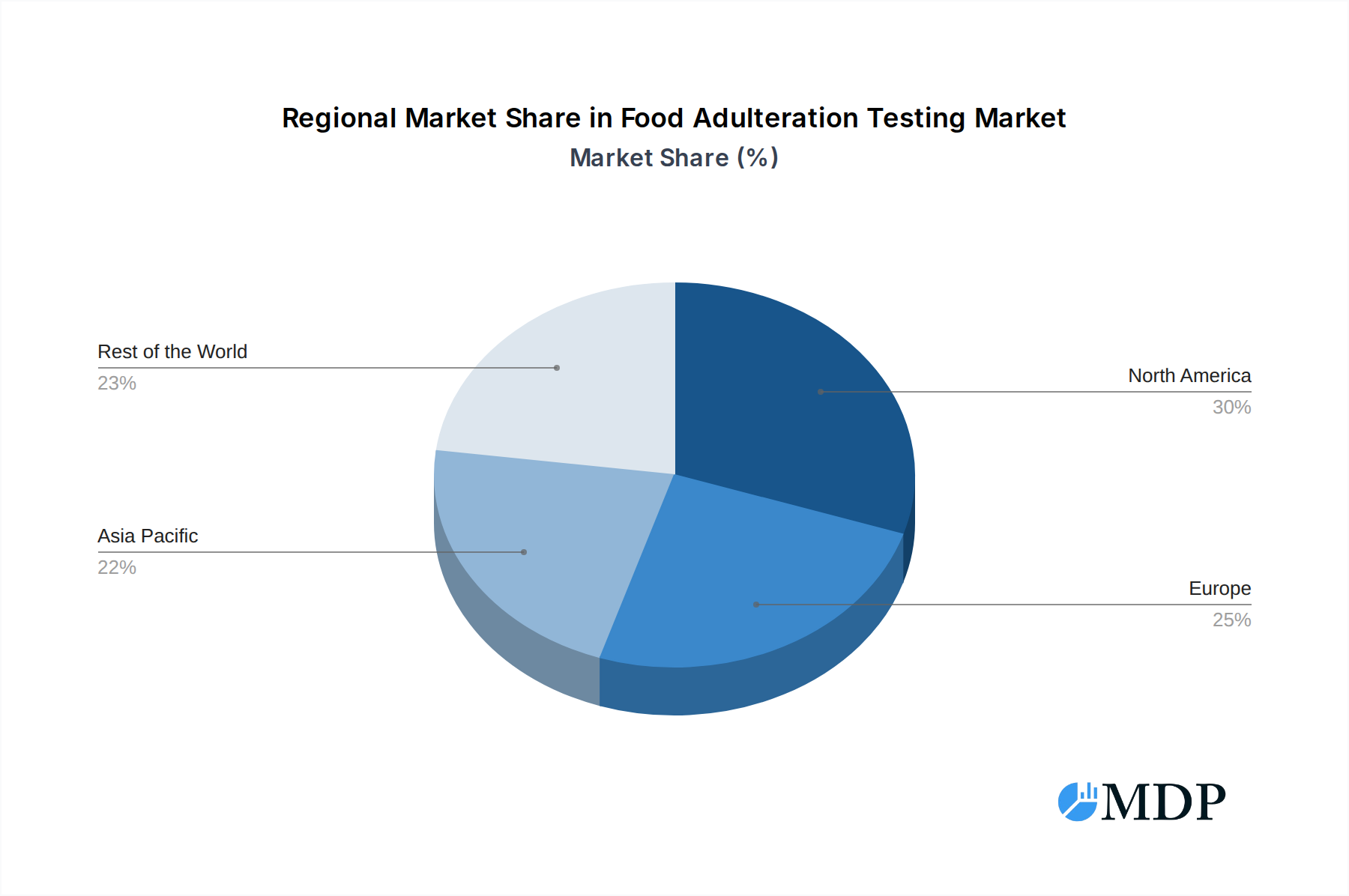

The food adulteration testing market showcases dominance across specific regions and segments, driven by distinct economic policies, infrastructure development, and regulatory landscapes. North America and Europe currently represent the leading markets, characterized by mature regulatory frameworks, high consumer spending on safe food products, and extensive adoption of advanced food analytical techniques.

Dominance Analysis by Type:

High-Performance Liquid Chromatography (HPLC): This segment exhibits significant dominance due to its versatility, sensitivity, and wide applicability in detecting a broad spectrum of adulterants, including pesticides, mycotoxins, and artificial sweeteners. Its widespread adoption in pharmaceutical and food industries for qualitative and quantitative analysis solidifies its leadership. Key drivers for HPLC's prominence include its well-established validation protocols and its ability to handle complex sample matrices.

High Performance Thin Layer Chromatography (HPTLC): While often employed for complementary analysis, HPTLC is gaining traction for its cost-effectiveness, rapid screening capabilities, and suitability for analyzing a large number of samples. Its dominance is particularly noted in resource-constrained environments or for initial screening purposes. The economic policies favoring cost-efficient quality control measures bolster its market penetration.

Others: This category encompasses a diverse range of analytical techniques, including Gas Chromatography-Mass Spectrometry (GC-MS), Fourier-Transform Infrared Spectroscopy (FTIR), DNA-based testing, and antibody-based assays. The "Others" segment's growing influence is driven by specialized applications, such as detecting GMOs, identifying allergenic ingredients, and authenticating the origin of food products. Technological breakthroughs in these niche areas are contributing to their increasing market share.

Dominance Analysis by Application:

Enterprise: This segment is the primary driver of market growth. Large-scale food manufacturers, processors, and retailers heavily invest in food adulteration testing services to comply with regulations, protect their brand reputation, and ensure consumer trust. Economic policies mandating stringent food safety standards and the infrastructure supporting widespread food distribution networks contribute to the enterprise segment's overwhelming dominance. Their need for comprehensive, accredited testing solutions fuels the demand for advanced laboratory services.

Individual: While smaller in market share, the individual consumer segment is a growing influencer. Increased consumer awareness regarding food safety and the availability of direct-to-consumer testing kits are contributing to this segment's expansion. Although regulatory frameworks primarily target businesses, the rising demand for personal assurance and the availability of consumer-grade food testing solutions are gradually increasing its significance.

The economic policies supporting robust food safety enforcement, coupled with advanced infrastructure for sample transportation and analysis, ensure the continued leadership of these dominant regions and segments in the global food adulteration testing market.

Food Adulteration Testing Product Developments

Recent product developments in food adulteration testing are significantly enhancing detection capabilities and market accessibility. Innovations in High-Performance Liquid Chromatography (HPLC) and High Performance Thin Layer Chromatography (HPTLC) systems are leading to more sensitive, faster, and cost-effective analytical methods. Companies are introducing portable and on-site testing devices that empower businesses and even individuals to conduct rapid screenings for common adulterants, reducing reliance on centralized laboratories for initial assessments. These advancements offer competitive advantages by enabling quicker response times to potential contamination events and supporting proactive food safety management. The focus is on developing user-friendly platforms with integrated data analysis for improved food quality control and food fraud detection.

Key Drivers of Food Adulteration Testing Growth

The food adulteration testing market is experiencing robust growth fueled by several interconnected factors. Increasingly stringent food safety regulations implemented globally by governmental bodies are a primary driver, compelling food businesses to invest in comprehensive testing to ensure compliance and avoid penalties. Technological advancements in analytical techniques, particularly in HPLC and HPTLC, are providing more sensitive, accurate, and rapid detection methods for a wider array of adulterants. Furthermore, a significant rise in consumer awareness and demand for safe, authentic food products is pressuring manufacturers to enhance their food quality control measures, thus driving the demand for independent testing services. Economic growth in emerging markets is also contributing, as developing nations are strengthening their food safety infrastructure and regulatory frameworks.

Challenges in the Food Adulteration Testing Market

Despite its growth, the food adulteration testing market faces several significant challenges. Regulatory hurdles, including varying international standards and the cost of achieving and maintaining accreditations, can be substantial. The complexity of global supply chains and the constant evolution of adulteration methods make it challenging to stay ahead of emerging threats, requiring continuous investment in new technologies and expertise. Furthermore, the high cost of advanced analytical equipment and skilled personnel can be a barrier, especially for smaller businesses. Competitive pressures also exist, with a crowded market potentially leading to price wars that can impact profit margins for testing service providers.

Emerging Opportunities in Food Adulteration Testing

Emerging opportunities in the food adulteration testing sector are abundant and diverse. The increasing demand for authentic and traceable food products presents a significant avenue for growth in food fraud detection and food authenticity testing. Technological breakthroughs, such as the development of rapid, on-site screening devices and advanced spectroscopic techniques, offer the potential to expand the market beyond traditional laboratory settings. Strategic partnerships between technology providers, testing laboratories, and food businesses can foster innovation and create comprehensive food safety solutions. Furthermore, the growing focus on sustainability and the detection of food waste-related issues will open new avenues for specialized testing services. Expansion into underserved emerging markets, where regulatory frameworks are rapidly evolving, also represents a substantial growth catalyst.

Leading Players in the Food Adulteration Testing Sector

- Auriga Research

- Neogen

- AMMAGENOMICS

- Eurofins

- Anacon Laboratories

- PurityPortal

- SGS

- Intertek

- ALS

- Intertek Group

- SCIEX

Key Milestones in Food Adulteration Testing Industry

- 2019: Increased regulatory focus on undisclosed allergens in food products, leading to enhanced testing protocols.

- 2020: Significant advancements in rapid screening technologies for common food adulterants, offering on-site testing capabilities.

- 2021: Growing emphasis on the detection of microplastics in food, prompting the development of specialized analytical methods.

- 2022: Expansion of DNA-based testing for species identification and origin verification in food products.

- 2023: heightened awareness and testing for synthetic food additives and illegal dyes across various food categories.

- 2024: Introduction of AI-powered data analysis tools to accelerate and improve the accuracy of food adulteration testing results.

Strategic Outlook for Food Adulteration Testing Market

The food adulteration testing market is set for continued substantial growth, driven by an unwavering global commitment to food safety and an escalating demand for transparency. Strategic opportunities lie in the further development and adoption of rapid, portable testing technologies, enabling decentralized food quality control. Investments in expanding capabilities for detecting emerging adulterants and tracing food origins will be crucial. Fostering collaborative partnerships between testing service providers, technology innovators, and regulatory bodies will accelerate the development of comprehensive and proactive food safety management systems. The market will increasingly benefit from the integration of advanced data analytics and AI, enhancing efficiency and predictive capabilities, ultimately securing a safer global food supply.

Food Adulteration Testing Segmentation

-

1. Type

- 1.1. High-Performance Liquid Chromatography

- 1.2. High Performance Thin Layer Chromatography

- 1.3. Others

-

2. Application

- 2.1. Enterprise

- 2.2. Individual

Food Adulteration Testing Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Food Adulteration Testing Regional Market Share

Geographic Coverage of Food Adulteration Testing

Food Adulteration Testing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Food Adulteration Testing Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. High-Performance Liquid Chromatography

- 5.1.2. High Performance Thin Layer Chromatography

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Enterprise

- 5.2.2. Individual

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Food Adulteration Testing Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. High-Performance Liquid Chromatography

- 6.1.2. High Performance Thin Layer Chromatography

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Enterprise

- 6.2.2. Individual

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. South America Food Adulteration Testing Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. High-Performance Liquid Chromatography

- 7.1.2. High Performance Thin Layer Chromatography

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Enterprise

- 7.2.2. Individual

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Food Adulteration Testing Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. High-Performance Liquid Chromatography

- 8.1.2. High Performance Thin Layer Chromatography

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Enterprise

- 8.2.2. Individual

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East & Africa Food Adulteration Testing Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. High-Performance Liquid Chromatography

- 9.1.2. High Performance Thin Layer Chromatography

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Enterprise

- 9.2.2. Individual

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific Food Adulteration Testing Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. High-Performance Liquid Chromatography

- 10.1.2. High Performance Thin Layer Chromatography

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Enterprise

- 10.2.2. Individual

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Auriga Research

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Neogen

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AMMAGENOMICS

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Eurofins

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Anacon Laboratories

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 PurityPortal

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 SGS

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Intertek

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 ALS

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Intertek Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 SCIEX

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Auriga Research

List of Figures

- Figure 1: Global Food Adulteration Testing Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Food Adulteration Testing Revenue (undefined), by Type 2025 & 2033

- Figure 3: North America Food Adulteration Testing Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Food Adulteration Testing Revenue (undefined), by Application 2025 & 2033

- Figure 5: North America Food Adulteration Testing Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Food Adulteration Testing Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Food Adulteration Testing Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Food Adulteration Testing Revenue (undefined), by Type 2025 & 2033

- Figure 9: South America Food Adulteration Testing Revenue Share (%), by Type 2025 & 2033

- Figure 10: South America Food Adulteration Testing Revenue (undefined), by Application 2025 & 2033

- Figure 11: South America Food Adulteration Testing Revenue Share (%), by Application 2025 & 2033

- Figure 12: South America Food Adulteration Testing Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Food Adulteration Testing Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Food Adulteration Testing Revenue (undefined), by Type 2025 & 2033

- Figure 15: Europe Food Adulteration Testing Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Food Adulteration Testing Revenue (undefined), by Application 2025 & 2033

- Figure 17: Europe Food Adulteration Testing Revenue Share (%), by Application 2025 & 2033

- Figure 18: Europe Food Adulteration Testing Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Food Adulteration Testing Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Food Adulteration Testing Revenue (undefined), by Type 2025 & 2033

- Figure 21: Middle East & Africa Food Adulteration Testing Revenue Share (%), by Type 2025 & 2033

- Figure 22: Middle East & Africa Food Adulteration Testing Revenue (undefined), by Application 2025 & 2033

- Figure 23: Middle East & Africa Food Adulteration Testing Revenue Share (%), by Application 2025 & 2033

- Figure 24: Middle East & Africa Food Adulteration Testing Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Food Adulteration Testing Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Food Adulteration Testing Revenue (undefined), by Type 2025 & 2033

- Figure 27: Asia Pacific Food Adulteration Testing Revenue Share (%), by Type 2025 & 2033

- Figure 28: Asia Pacific Food Adulteration Testing Revenue (undefined), by Application 2025 & 2033

- Figure 29: Asia Pacific Food Adulteration Testing Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific Food Adulteration Testing Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Food Adulteration Testing Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Food Adulteration Testing Revenue undefined Forecast, by Type 2020 & 2033

- Table 2: Global Food Adulteration Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 3: Global Food Adulteration Testing Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Food Adulteration Testing Revenue undefined Forecast, by Type 2020 & 2033

- Table 5: Global Food Adulteration Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 6: Global Food Adulteration Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Food Adulteration Testing Revenue undefined Forecast, by Type 2020 & 2033

- Table 11: Global Food Adulteration Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 12: Global Food Adulteration Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Food Adulteration Testing Revenue undefined Forecast, by Type 2020 & 2033

- Table 17: Global Food Adulteration Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 18: Global Food Adulteration Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Food Adulteration Testing Revenue undefined Forecast, by Type 2020 & 2033

- Table 29: Global Food Adulteration Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 30: Global Food Adulteration Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Food Adulteration Testing Revenue undefined Forecast, by Type 2020 & 2033

- Table 38: Global Food Adulteration Testing Revenue undefined Forecast, by Application 2020 & 2033

- Table 39: Global Food Adulteration Testing Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Food Adulteration Testing Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Adulteration Testing?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the Food Adulteration Testing?

Key companies in the market include Auriga Research, Neogen, AMMAGENOMICS, Eurofins, Anacon Laboratories, PurityPortal, SGS, Intertek, ALS, Intertek Group, SCIEX.

3. What are the main segments of the Food Adulteration Testing?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Food Adulteration Testing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Food Adulteration Testing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Food Adulteration Testing?

To stay informed about further developments, trends, and reports in the Food Adulteration Testing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence