Key Insights

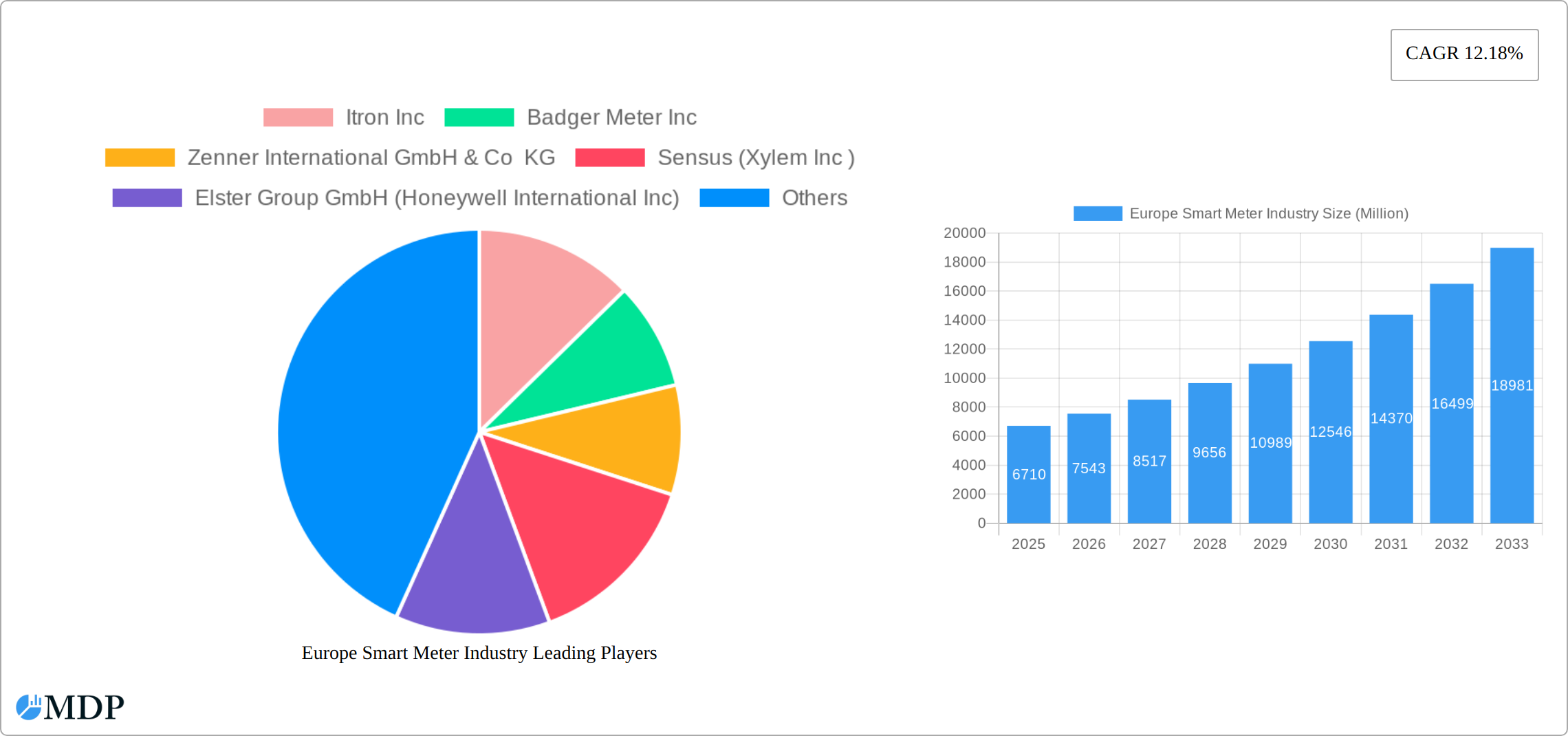

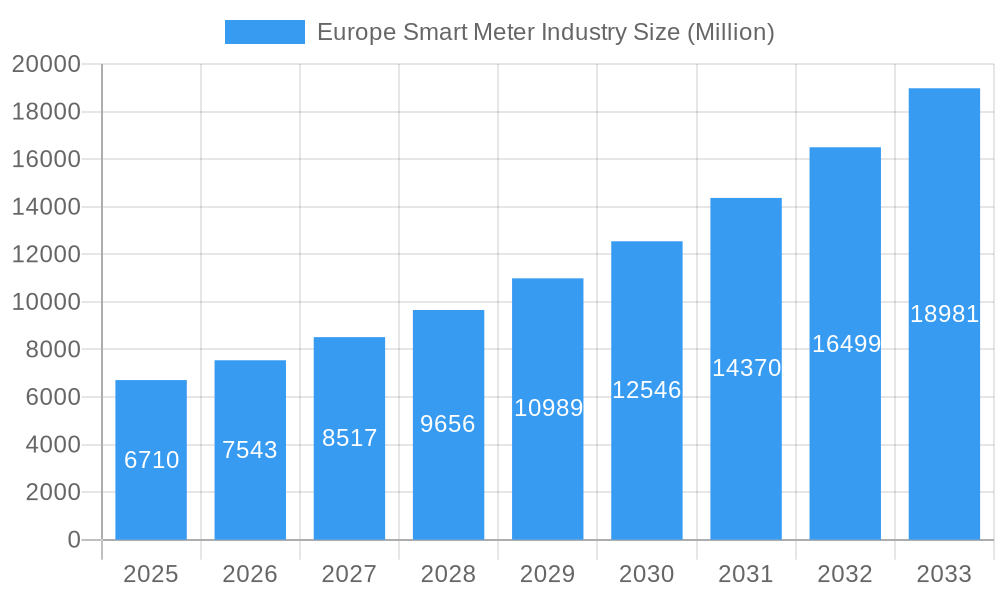

The European smart meter market, valued at €6.71 billion in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 12.18% from 2025 to 2033. This surge is driven primarily by increasing government regulations mandating smart meter deployment across residential, commercial, and industrial sectors to enhance energy efficiency, reduce carbon emissions, and improve grid management. The rising adoption of renewable energy sources further fuels this market expansion, as smart meters enable better integration and monitoring of intermittent renewable energy generation. Technological advancements, such as the development of advanced metering infrastructure (AMI) and the integration of smart meters with IoT platforms, are also contributing significantly to market growth. Competition among major players like Itron, Badger Meter, and Landis+GYR is intensifying, leading to innovation in meter functionalities and cost reductions, making smart meter adoption more accessible.

Europe Smart Meter Industry Market Size (In Billion)

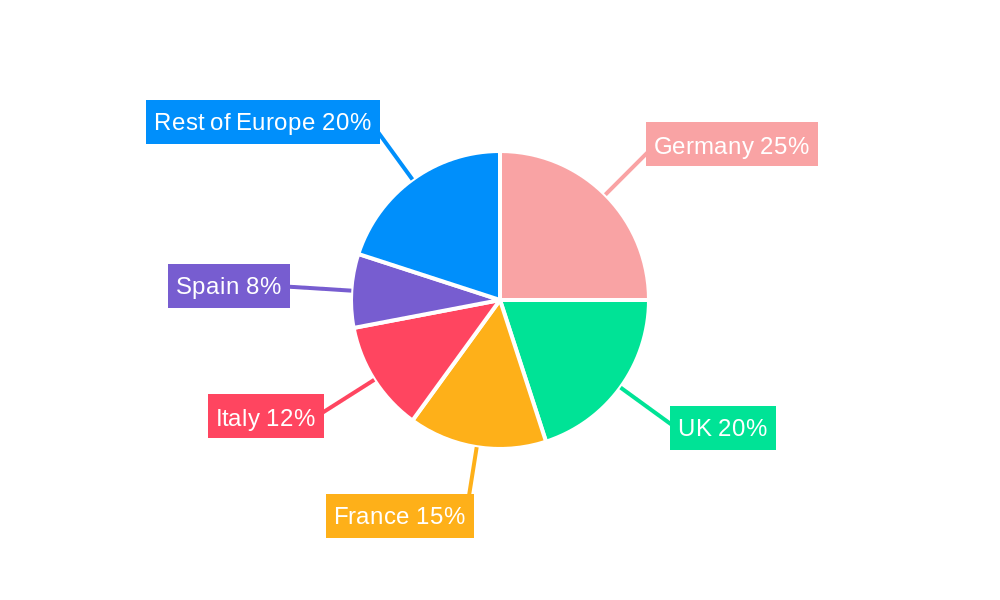

Within the European market, Germany, the United Kingdom, France, and Italy represent the largest national markets, driven by their established energy infrastructures and proactive government policies. However, growth potential exists in other European countries as they implement similar smart meter initiatives. Market segmentation reveals a strong preference for smart electricity meters, followed by smart gas and water meters. The residential sector currently dominates the end-user segment but commercial and industrial sectors are expected to experience faster growth in the coming years due to increasing demand for energy optimization and data-driven operational insights. While challenges such as high initial investment costs and concerns about data security exist, the long-term benefits of enhanced energy management and grid optimization outweigh these concerns, ensuring the continued expansion of the European smart meter market.

Europe Smart Meter Industry Company Market Share

Europe Smart Meter Industry: Market Report 2019-2033

This comprehensive report provides a detailed analysis of the European smart meter industry, covering market dynamics, leading players, technological advancements, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and an estimated year of 2025, this report offers invaluable insights for industry stakeholders, investors, and strategic decision-makers. The forecast period extends from 2025 to 2033, utilizing data from the historical period of 2019-2024. Expect detailed analysis on revenue and unit shipments in Millions.

Europe Smart Meter Industry Market Dynamics & Concentration

The European smart meter market is experiencing robust expansion, propelled by increasingly stringent government mandates promoting energy efficiency and decarbonization, alongside a growing consumer appetite for smart home technologies. The market exhibits a moderate level of concentration, with several influential players commanding significant market shares, yet no single entity dominates. The combined market share of the top 5 players is estimated to be around **[Insert Data Here]%**. Mergers and acquisitions (M&A) activity has been steady in recent years, with approximately **[Insert Data Here]** deals documented between 2019 and 2024, indicating strategic consolidation efforts and market expansion by key industry participants.

- Innovation Drivers: Cutting-edge advancements in Internet of Things (IoT) technologies, diverse communication protocols (including NB-IoT and LTE-M), and sophisticated data analytics are pivotal innovation drivers. These advancements enable enhanced functionalities for smart meters and significantly improve overall grid management capabilities.

- Regulatory Frameworks: Comprehensive environmental regulations and proactive government initiatives aimed at accelerating smart grid deployment serve as major catalysts for market growth. The European Union's steadfast commitment to integrating renewable energy sources is a significant factor further stimulating demand for smart metering solutions.

- Product Substitutes: While direct substitutes for smart meters are virtually non-existent, traditional mechanical meters still present a competitive challenge. However, their inherent limitations in granular data collection and operational efficiency are increasingly leading to their gradual obsolescence and replacement by advanced smart meter technologies.

- End-User Trends: Heightened consumer awareness regarding energy consumption patterns and potential cost savings is a powerful driver for the widespread adoption of smart meters across residential, commercial, and industrial sectors. Consumers are increasingly seeking granular insights into their energy usage to optimize consumption and reduce expenditure.

- M&A Activities: The ongoing consolidation trend within the smart meter industry is anticipated to persist. Larger, established companies are strategically pursuing mergers and acquisitions to broaden their market reach, acquire new technologies, and diversify their product portfolios, thereby strengthening their competitive positions.

Europe Smart Meter Industry Industry Trends & Analysis

The European smart meter market is characterized by a strong and sustained growth trajectory, projecting a Compound Annual Growth Rate (CAGR) of **[Insert Data Here]%** during the forecast period (2025-2033). Current market penetration stands at approximately **[Insert Data Here]%**, with projections indicating an ascent to **[Insert Data Here]%** by 2033. This impressive growth is underpinned by several converging factors: escalating urbanization, the critical need for modernizing grid infrastructure, and a burgeoning demand for real-time energy monitoring and intelligent management systems. Technological disruptions, particularly in the realms of IoT and advanced communication technologies, are profoundly reshaping the industry, fostering the adoption of more sophisticated and economically viable solutions. Consumer preferences are notably shifting towards smart meters that offer advanced features such as remote monitoring capabilities, detailed energy usage analytics, and effective demand-side management functionalities. The competitive arena is marked by intense rivalry between established industry giants and agile emerging players, a dynamic that consistently spurs innovation and drives price competitiveness.

Leading Markets & Segments in Europe Smart Meter Industry

The Smart Electricity Meter segment currently holds the largest market share by revenue and unit shipments, followed by Smart Gas Meter and Smart Water Meter. Within end-users, the residential segment dominates, driven by government incentives and consumer interest in energy efficiency. The United Kingdom, Germany, and France are the leading markets in Europe, driven by strong government support for smart grid modernization and favorable regulatory landscapes.

- Key Drivers in Leading Markets:

- United Kingdom: Robust government support for the Smart Meter rollout program.

- Germany: Stringent energy efficiency regulations and a focus on renewable energy integration.

- France: Government initiatives to modernize the country's energy infrastructure.

- Italy: Increased investment in smart grid technologies.

- Spain: Growing awareness of energy efficiency and a push for smart city initiatives.

Europe Smart Meter Industry Product Developments

Recent product innovations are primarily centered on the integration of advanced communication technologies like NB-IoT and LTE-M, the enhancement of sophisticated data analytics capabilities for deeper insights, and the bolstering of robust security features to protect sensitive data. Notably, ultrasonic smart water meters are experiencing a surge in popularity due to their superior accuracy and convenient remote monitoring functionalities. The seamless integration of smart meters with a wider ecosystem of smart home devices and platforms is also expanding, providing end-users with a comprehensive and unified view of their energy consumption patterns, thereby significantly improving overall energy efficiency. This interconnected approach offers distinct competitive advantages through an enriched user experience and the generation of actionable, data-driven insights.

Key Drivers of Europe Smart Meter Industry Growth

Several pivotal factors are fueling the sustained growth of the European smart meter industry:

- Technological Advancements: The continuous evolution and development of more advanced, reliable, and cost-effective smart meters, significantly propelled by breakthroughs in IoT and communication technology.

- Government Regulations: The implementation of stringent environmental regulations and supportive government initiatives that actively promote smart grid modernization efforts and enhance energy efficiency across the continent.

- Economic Factors: The persistent upward trend in energy prices, coupled with an increasing consumer awareness of energy consumption and its associated costs, is creating a robust demand for energy-efficient solutions like smart meters.

Challenges in the Europe Smart Meter Industry Market

The European smart meter market, despite its promising outlook, encounters several significant challenges:

- Regulatory Hurdles: The presence of diverse and often varying regulatory frameworks across different European countries introduces complexities and potential obstacles for market entry and the seamless deployment of smart metering solutions.

- Supply Chain Issues: Ongoing global supply chain disruptions can negatively impact the consistent availability and the overall cost of smart meter components and finished products, creating potential delays and cost overruns.

- Competitive Pressures: The highly competitive landscape, characterized by the presence of established market leaders and aggressive emerging entrants, exerts considerable pressure on pricing strategies and profit margins for all industry players.

Emerging Opportunities in Europe Smart Meter Industry

Significant long-term growth opportunities exist in the European smart meter market. This growth will be propelled by several factors:

- Technological Breakthroughs: Continued advancements in IoT, AI, and data analytics will enable more sophisticated smart meter functionalities.

- Strategic Partnerships: Collaborations between smart meter manufacturers, energy providers, and technology companies will facilitate faster market penetration.

- Market Expansion Strategies: Expansion into less penetrated markets within Europe and development of new product applications will drive growth.

Leading Players in the Europe Smart Meter Industry Sector

- Itron Inc

- Badger Meter Inc

- Zenner International GmbH & Co KG

- Sensus (Xylem Inc)

- Elster Group GmbH (Honeywell International Inc)

- Kamstrup A/S

- Apator SA

- Arad Group

- Diehl Stiftung & Co KG

- Landis+ GYR Group AG

- Ningbo Sanxing Electric Co Ltd

- AEM

- General Electric Company

Key Milestones in Europe Smart Meter Industry Industry

- December 2022: Trilliant secures a contract to supply smart meters for Ireland's National Smart Metering Programme, boosting the adoption of smart meters in Ireland and showcasing the growing market demand.

- November 2022: Landis+Gyr's launch of new ultrasonic smart water meters equipped with NB-IoT communication highlights advancements in smart water metering technology and its potential to improve water network management.

Strategic Outlook for Europe Smart Meter Industry Market

The future of the European smart meter market is bright. Continued government support, technological innovation, and rising consumer demand will drive significant growth over the next decade. Strategic opportunities for players include expanding into underserved markets, developing innovative solutions that integrate smart meters with other smart home technologies, and focusing on data analytics and services to provide additional value to customers. The market is poised for substantial expansion, creating promising opportunities for both established and emerging players.

Europe Smart Meter Industry Segmentation

-

1. Type of Meter (Revenue and Unit Shipments)

- 1.1. Smart Gas Meter

- 1.2. Smart Water Meter

- 1.3. Smart Electricity Meter

-

2. End User

- 2.1. Residential

- 2.2. Commercial

- 2.3. Industrial

Europe Smart Meter Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Smart Meter Industry Regional Market Share

Geographic Coverage of Europe Smart Meter Industry

Europe Smart Meter Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.18% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increased Investments in Smart Grid Projects; Growth in Smart City Deployment; Supportive Government Regulations

- 3.3. Market Restrains

- 3.3.1. High Costs and Security Concerns; Integration Difficulties with Smart Meters

- 3.4. Market Trends

- 3.4.1. Increased investments in smart grid projects in expected to drive the market growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Smart Meter Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type of Meter (Revenue and Unit Shipments)

- 5.1.1. Smart Gas Meter

- 5.1.2. Smart Water Meter

- 5.1.3. Smart Electricity Meter

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Residential

- 5.2.2. Commercial

- 5.2.3. Industrial

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type of Meter (Revenue and Unit Shipments)

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Itron Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Badger Meter Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Zenner International GmbH & Co KG

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Sensus (Xylem Inc )

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Elster Group GmbH (Honeywell International Inc)

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Kamstrup A/S

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Apator SA

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Arad Group

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Diehl Stiftung & Co KG

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Landis+ GYR Group AG

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Ningbo Sanxing Electric Co Ltd

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 AEM

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 General Electric Company

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.1 Itron Inc

List of Figures

- Figure 1: Europe Smart Meter Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Smart Meter Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Smart Meter Industry Revenue Million Forecast, by Type of Meter (Revenue and Unit Shipments) 2020 & 2033

- Table 2: Europe Smart Meter Industry Volume K Unit Forecast, by Type of Meter (Revenue and Unit Shipments) 2020 & 2033

- Table 3: Europe Smart Meter Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: Europe Smart Meter Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 5: Europe Smart Meter Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Europe Smart Meter Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Europe Smart Meter Industry Revenue Million Forecast, by Type of Meter (Revenue and Unit Shipments) 2020 & 2033

- Table 8: Europe Smart Meter Industry Volume K Unit Forecast, by Type of Meter (Revenue and Unit Shipments) 2020 & 2033

- Table 9: Europe Smart Meter Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 10: Europe Smart Meter Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 11: Europe Smart Meter Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Europe Smart Meter Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Germany Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: France Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Italy Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Italy Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Spain Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Spain Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Netherlands Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Netherlands Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 25: Belgium Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Belgium Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: Sweden Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Sweden Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: Norway Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Norway Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Poland Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Poland Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Denmark Europe Smart Meter Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Denmark Europe Smart Meter Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Smart Meter Industry?

The projected CAGR is approximately 12.18%.

2. Which companies are prominent players in the Europe Smart Meter Industry?

Key companies in the market include Itron Inc, Badger Meter Inc, Zenner International GmbH & Co KG, Sensus (Xylem Inc ), Elster Group GmbH (Honeywell International Inc), Kamstrup A/S, Apator SA, Arad Group, Diehl Stiftung & Co KG, Landis+ GYR Group AG, Ningbo Sanxing Electric Co Ltd, AEM, General Electric Company.

3. What are the main segments of the Europe Smart Meter Industry?

The market segments include Type of Meter (Revenue and Unit Shipments), End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.71 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Investments in Smart Grid Projects; Growth in Smart City Deployment; Supportive Government Regulations.

6. What are the notable trends driving market growth?

Increased investments in smart grid projects in expected to drive the market growth.

7. Are there any restraints impacting market growth?

High Costs and Security Concerns; Integration Difficulties with Smart Meters.

8. Can you provide examples of recent developments in the market?

December 2022: Trilliant, a leading provider of solutions for advanced metering infrastructure (AMI), smart cities, smart grid, and IIoT, announced the selection of its UK division, Trilliant Networks Operations (UK) Ltd., as one of the suppliers to provide smart meters to support the rollout of Ireland’s National Smart Metering Programme (NSMP) by ESB Networks. The program aims to help customers manage their energy use, save money, and lower their carbon footprint.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Smart Meter Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Smart Meter Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Smart Meter Industry?

To stay informed about further developments, trends, and reports in the Europe Smart Meter Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence