Key Insights

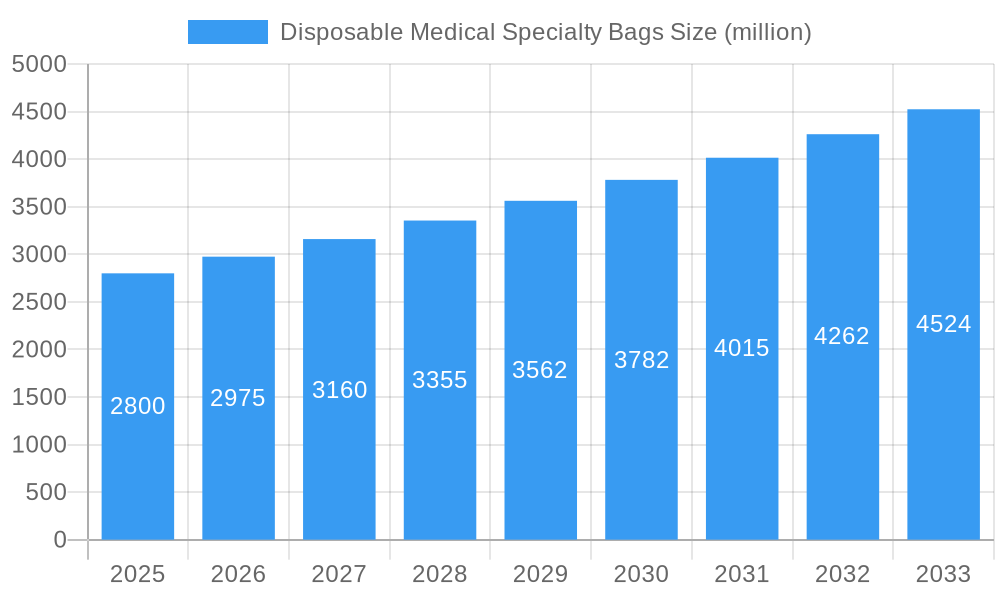

The global Disposable Medical Specialty Bags market is projected for significant expansion, estimated to reach $10.4 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 4.52% anticipated through 2033. This growth is driven by escalating global healthcare expenditure, the increasing prevalence of chronic diseases, and a heightened focus on infection control and patient safety, leading to greater adoption of single-use products in hospitals and home care settings. Advances in material science are enhancing bag functionality, sterility, and patient comfort. Emerging economies with expanding healthcare infrastructure also offer substantial market opportunities.

Disposable Medical Specialty Bags Market Size (In Billion)

The market offers a diverse range of products, including anesthesia breathing bags, blood bags, IV bags, and ostomy bags. Innovations in leak-proof designs and user-friendly interfaces are improving market penetration. Key restraints include stringent regulatory compliance and raw material price volatility. However, sustained demand from an aging global population and the need for advanced patient care solutions will drive healthy market growth. Key industry players are investing in research and development to leverage these market dynamics.

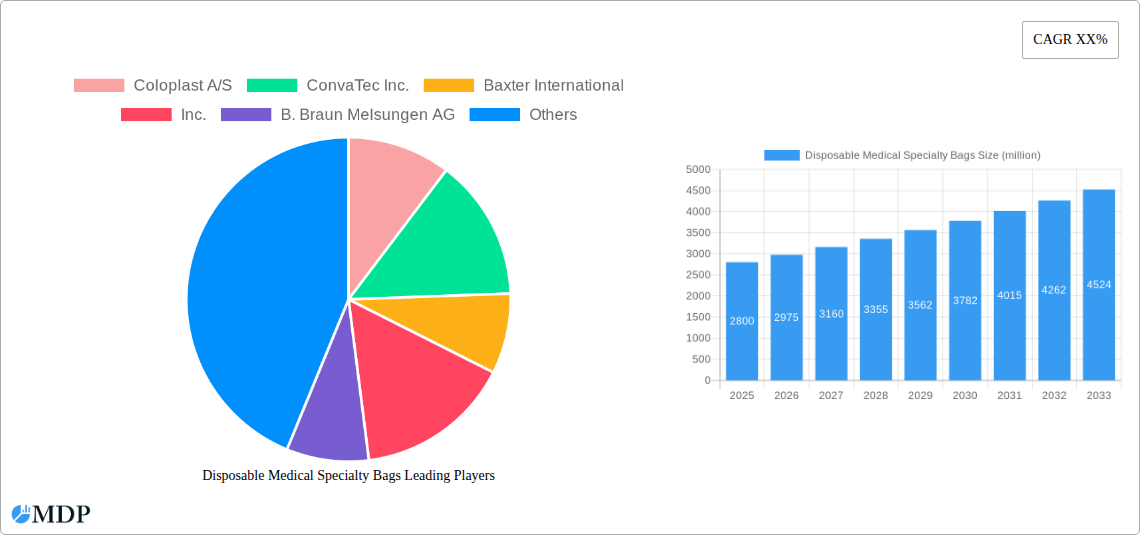

Disposable Medical Specialty Bags Company Market Share

Disposable Medical Specialty Bags Market: Comprehensive Analysis & Future Outlook (2019-2033)

This in-depth report provides a detailed examination of the global disposable medical specialty bags market, offering critical insights for industry stakeholders, manufacturers, suppliers, and investors. Covering a comprehensive study period from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033, this analysis delves into market dynamics, key trends, leading segments, product innovations, growth drivers, challenges, opportunities, and the competitive landscape. With an estimated market value exceeding several million USD in the base year of 2025, the market is poised for significant expansion driven by rising healthcare expenditures, increasing prevalence of chronic diseases, and advancements in medical technology.

Disposable Medical Specialty Bags Market Dynamics & Concentration

The disposable medical specialty bags market is characterized by a moderate to high concentration, with a few key players dominating a substantial portion of the market share. Leading companies like Coloplast A/S, ConvaTec Inc., and Baxter International, Inc. consistently invest in research and development to introduce innovative products that enhance patient care and safety. The primary innovation drivers include the development of advanced materials for improved biocompatibility and durability, as well as the integration of smart features for enhanced monitoring and administration. Regulatory frameworks, such as those established by the FDA and EMA, play a crucial role in ensuring product quality, safety, and efficacy, albeit sometimes posing challenges for market entry for smaller players. Product substitutes are limited, given the specialized nature of these bags, though advancements in reusable medical devices could present a long-term threat. End-user trends are heavily influenced by the growing demand for home healthcare solutions and the increasing preference for single-use products to minimize infection risks. Mergers and acquisitions (M&A) activities are a notable aspect of market dynamics, with an estimated hundreds of M&A deals recorded during the historical period, aimed at consolidating market share, expanding product portfolios, and gaining access to new technologies and geographical regions. For instance, in 2023 alone, there were approximately 50 M&A transactions focused on specialty medical disposables.

Disposable Medical Specialty Bags Industry Trends & Analysis

The disposable medical specialty bags industry is experiencing robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 6.5% from 2025 to 2033. This expansion is primarily fueled by the escalating global demand for advanced healthcare solutions, a direct consequence of the increasing incidence of chronic diseases such as diabetes, cardiovascular conditions, and gastrointestinal disorders. The aging global population further amplifies this trend, as elderly individuals typically require more frequent and specialized medical interventions, including the use of disposable bags for various medical procedures. Technological disruptions are also playing a pivotal role. Innovations in material science are leading to the development of lighter, more flexible, and biocompatible bags, enhancing patient comfort and reducing the risk of adverse reactions. Furthermore, the integration of smart technologies, such as sensors for fluid level monitoring and integrated drug delivery systems within bags like IV bags and enteral feeding bags, is revolutionizing patient care and empowering healthcare professionals with real-time data. Consumer preferences are increasingly leaning towards disposable products due to heightened awareness regarding infection control and the convenience offered by single-use items, particularly in home care settings. This shift is evident in the growing market penetration of ostomy bags and urinary collection bags in ambulatory care. Competitive dynamics within the market are intense, with established players focusing on product differentiation through superior quality, innovative features, and strategic partnerships, while new entrants often aim to capture niche markets with specialized offerings. The overall market penetration for basic disposable medical bags stands at an estimated 70% in developed economies, with significant room for growth in emerging markets. The market value is projected to reach an estimated over 20 million USD by 2033.

Leading Markets & Segments in Disposable Medical Specialty Bags

The hospitals segment continues to be the dominant application in the disposable medical specialty bags market, driven by their high volume of patient admissions and the extensive range of medical procedures performed. Within this segment, IV bags represent the largest type, followed closely by blood bags, owing to their critical role in fluid management and transfusion services, respectively. The widespread adoption of advanced medical technologies and the continuous need for sterile, single-use products in hospital settings are key drivers. Furthermore, economic policies in developed nations that prioritize healthcare infrastructure development and increased government spending on public health initiatives further bolster the demand from hospitals.

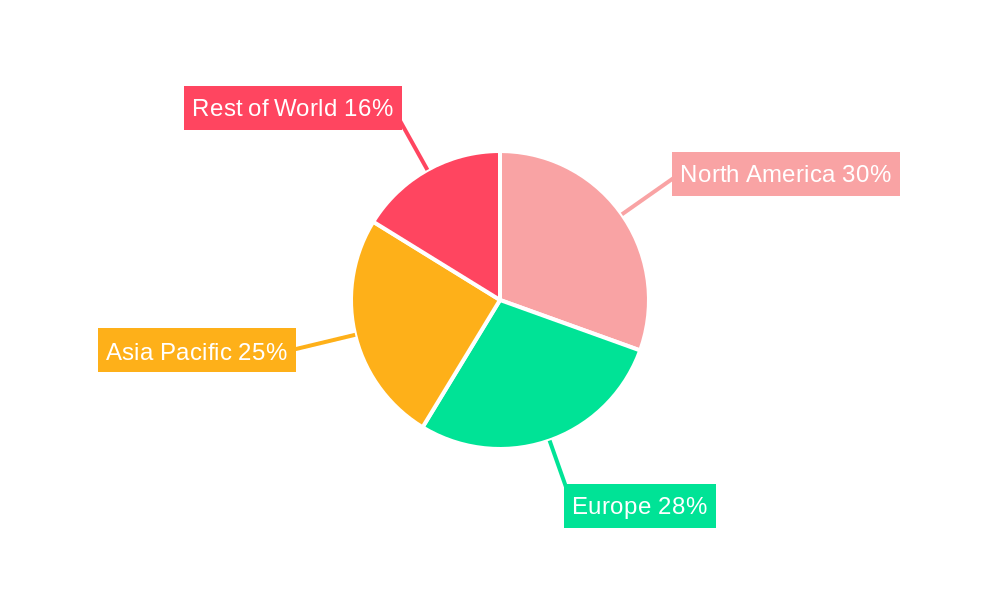

In terms of geographical dominance, North America (specifically the United States) and Europe (led by Germany and the UK) are the leading markets. This is attributed to factors such as high per capita healthcare expenditure, advanced healthcare infrastructure, a significant patient population with chronic diseases, and stringent regulatory standards that encourage the adoption of high-quality disposable medical products.

Key drivers contributing to the dominance of these regions and segments include:

Hospitals:

- High Volume of Procedures: Hospitals perform a vast array of surgical, diagnostic, and therapeutic procedures requiring disposable medical bags.

- Infection Control Protocols: Strict protocols necessitate the use of sterile, single-use items to prevent healthcare-associated infections (HAIs).

- Technological Advancements: Integration of advanced medical devices and equipment in hospitals drives demand for compatible specialty bags.

- Reimbursement Policies: Favorable reimbursement policies for disposable medical supplies in many countries incentivize their use.

IV Bags:

- Ubiquitous Use: Essential for drug administration, hydration, and nutritional support across various medical conditions.

- Growth in Biologics and Chemotherapy: Increasing use of complex injectable drugs fuels demand for specialized IV bags.

Blood Bags:

- Surgical Procedures and Trauma Care: Crucial for blood transfusions in surgeries, accidents, and medical emergencies.

- Blood Donation Drives: Continuous efforts to maintain blood banks drive consistent demand.

North America & Europe:

- High Healthcare Spending: Significant investment in healthcare infrastructure and patient care.

- Aging Population: A larger elderly demographic with increased healthcare needs.

- Advanced Medical Technology Adoption: Early and widespread adoption of innovative medical devices.

- Stringent Quality Standards: Robust regulatory frameworks ensure demand for high-quality, certified products.

The home care segment is emerging as a significant growth area, driven by the shift towards outpatient care and the increasing prevalence of chronic diseases managed in home environments. In this setting, ostomy bags and urinary collection bags are particularly important, reflecting the growing number of individuals managing long-term conditions at home.

Disposable Medical Specialty Bags Product Developments

Recent product developments in the disposable medical specialty bags market are focused on enhancing patient safety, comfort, and usability. Innovations include the introduction of bags made from advanced, biocompatible polymers that minimize allergic reactions and improve flexibility. Smart technologies are being integrated, such as ostomy bags with odor control features and IV bags with integrated dose-monitoring capabilities. Enhanced sterile packaging techniques are also a key focus, ensuring product integrity and reducing the risk of contamination. These developments offer competitive advantages by addressing unmet clinical needs, improving patient adherence to treatment, and streamlining healthcare workflows, ultimately leading to better patient outcomes.

Key Drivers of Disposable Medical Specialty Bags Growth

The disposable medical specialty bags market is propelled by several key growth drivers. Firstly, the rising global prevalence of chronic diseases, including diabetes, cardiovascular ailments, and gastrointestinal disorders, necessitates the continuous use of specialized bags for treatment and management. Secondly, the growing aging population worldwide contributes significantly to market expansion, as elderly individuals often require more frequent and long-term medical interventions. Thirdly, technological advancements in material science are leading to the development of superior, more user-friendly, and safer disposable bags. Lastly, increasing healthcare expenditure and government initiatives promoting better healthcare access and infection control protocols globally are crucial accelerators for market growth.

Challenges in the Disposable Medical Specialty Bags Market

Despite its robust growth, the disposable medical specialty bags market faces several challenges. Stringent and evolving regulatory frameworks across different regions can pose significant hurdles for product approvals and market entry, increasing development costs and time. Supply chain disruptions, exacerbated by geopolitical events or unforeseen global crises, can lead to material shortages and price volatility, impacting manufacturing and delivery. Furthermore, intense competitive pressures among established players and emerging manufacturers drive down profit margins. The high initial investment required for advanced manufacturing facilities and R&D also presents a barrier for smaller companies.

Emerging Opportunities in Disposable Medical Specialty Bags

Emerging opportunities in the disposable medical specialty bags market are primarily driven by technological breakthroughs and strategic market expansion. The growing demand for personalized medicine is creating a niche for custom-designed specialty bags catering to specific patient needs and therapeutic regimens. Furthermore, the increasing adoption of telehealth and home-based care models presents a significant opportunity for advanced disposable bags that facilitate remote patient monitoring and self-administration of treatments. Strategic partnerships between medical device manufacturers and technology companies can lead to the development of innovative, connected disposable bag systems. Expansion into underdeveloped and emerging markets, where healthcare infrastructure is rapidly improving, also offers substantial growth potential.

Leading Players in the Disposable Medical Specialty Bags Sector

- Coloplast A/S

- ConvaTec Inc.

- Baxter International, Inc.

- B. Braun Melsungen AG

- Hollister Incorporated

- Medline Industries, Inc.

- Terumo Corporation

- Nolato AB

- Smiths Medical

- acopharma

Key Milestones in Disposable Medical Specialty Bags Industry

- 2019: Introduction of biodegradable materials for ostomy bags, enhancing sustainability.

- 2020: Increased demand for specialized COVID-19 related respiratory support bags (e.g., anesthesia breathing bags, resuscitation bags).

- 2021: FDA approval for advanced smart IV bags with integrated dispensing technology.

- 2022: Significant M&A activity focused on consolidating the CAPD bags market.

- 2023: Launch of novel antimicrobial coatings for urinary collection bags to reduce infection rates.

- 2024: Expansion of home care product lines by key manufacturers to meet growing demand.

- 2025: Anticipated launch of next-generation enteral feeding bags with enhanced nutrient delivery systems.

Strategic Outlook for Disposable Medical Specialty Bags Market

The strategic outlook for the disposable medical specialty bags market is highly optimistic, driven by sustained demand from an aging global population and the persistent rise in chronic diseases. Future growth will be accelerated by ongoing innovations in smart packaging and material science, which are set to enhance product functionality and patient convenience. Strategic opportunities lie in expanding product portfolios to include a wider range of niche specialty bags and in penetrating emerging markets with tailored solutions. Collaborations with healthcare providers and technology firms will be crucial for developing integrated medical solutions that leverage the capabilities of advanced disposable bags, thereby solidifying market leadership and driving long-term value.

Disposable Medical Specialty Bags Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Clinics

- 1.3. Home Care

-

2. Types

- 2.1. Anesthesia Breathing Bags

- 2.2. Bile Collection Bags

- 2.3. Ostomy Bags

- 2.4. Resuscitation Bags

- 2.5. Blood Bags

- 2.6. CAPD Bags

- 2.7. Enema Bags

- 2.8. Enteral Feeding Bags

- 2.9. IV Bags

- 2.10. Urinary Collection Bags

Disposable Medical Specialty Bags Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Disposable Medical Specialty Bags Regional Market Share

Geographic Coverage of Disposable Medical Specialty Bags

Disposable Medical Specialty Bags REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.52% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Clinics

- 5.1.3. Home Care

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Anesthesia Breathing Bags

- 5.2.2. Bile Collection Bags

- 5.2.3. Ostomy Bags

- 5.2.4. Resuscitation Bags

- 5.2.5. Blood Bags

- 5.2.6. CAPD Bags

- 5.2.7. Enema Bags

- 5.2.8. Enteral Feeding Bags

- 5.2.9. IV Bags

- 5.2.10. Urinary Collection Bags

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Disposable Medical Specialty Bags Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Clinics

- 6.1.3. Home Care

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Anesthesia Breathing Bags

- 6.2.2. Bile Collection Bags

- 6.2.3. Ostomy Bags

- 6.2.4. Resuscitation Bags

- 6.2.5. Blood Bags

- 6.2.6. CAPD Bags

- 6.2.7. Enema Bags

- 6.2.8. Enteral Feeding Bags

- 6.2.9. IV Bags

- 6.2.10. Urinary Collection Bags

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Disposable Medical Specialty Bags Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Clinics

- 7.1.3. Home Care

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Anesthesia Breathing Bags

- 7.2.2. Bile Collection Bags

- 7.2.3. Ostomy Bags

- 7.2.4. Resuscitation Bags

- 7.2.5. Blood Bags

- 7.2.6. CAPD Bags

- 7.2.7. Enema Bags

- 7.2.8. Enteral Feeding Bags

- 7.2.9. IV Bags

- 7.2.10. Urinary Collection Bags

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Disposable Medical Specialty Bags Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Clinics

- 8.1.3. Home Care

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Anesthesia Breathing Bags

- 8.2.2. Bile Collection Bags

- 8.2.3. Ostomy Bags

- 8.2.4. Resuscitation Bags

- 8.2.5. Blood Bags

- 8.2.6. CAPD Bags

- 8.2.7. Enema Bags

- 8.2.8. Enteral Feeding Bags

- 8.2.9. IV Bags

- 8.2.10. Urinary Collection Bags

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Disposable Medical Specialty Bags Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Clinics

- 9.1.3. Home Care

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Anesthesia Breathing Bags

- 9.2.2. Bile Collection Bags

- 9.2.3. Ostomy Bags

- 9.2.4. Resuscitation Bags

- 9.2.5. Blood Bags

- 9.2.6. CAPD Bags

- 9.2.7. Enema Bags

- 9.2.8. Enteral Feeding Bags

- 9.2.9. IV Bags

- 9.2.10. Urinary Collection Bags

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Disposable Medical Specialty Bags Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Clinics

- 10.1.3. Home Care

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Anesthesia Breathing Bags

- 10.2.2. Bile Collection Bags

- 10.2.3. Ostomy Bags

- 10.2.4. Resuscitation Bags

- 10.2.5. Blood Bags

- 10.2.6. CAPD Bags

- 10.2.7. Enema Bags

- 10.2.8. Enteral Feeding Bags

- 10.2.9. IV Bags

- 10.2.10. Urinary Collection Bags

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Disposable Medical Specialty Bags Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Clinics

- 11.1.3. Home Care

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Anesthesia Breathing Bags

- 11.2.2. Bile Collection Bags

- 11.2.3. Ostomy Bags

- 11.2.4. Resuscitation Bags

- 11.2.5. Blood Bags

- 11.2.6. CAPD Bags

- 11.2.7. Enema Bags

- 11.2.8. Enteral Feeding Bags

- 11.2.9. IV Bags

- 11.2.10. Urinary Collection Bags

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Coloplast A/S

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ConvaTec Inc.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Baxter International

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Inc.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 B. Braun Melsungen AG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Hollister Incorporated

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Medline Industries

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Inc.

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Terumo Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Nolato AB

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Smiths Medical

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 acopharma

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Coloplast A/S

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Disposable Medical Specialty Bags Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Disposable Medical Specialty Bags Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Disposable Medical Specialty Bags Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Disposable Medical Specialty Bags Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Disposable Medical Specialty Bags Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Disposable Medical Specialty Bags Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Disposable Medical Specialty Bags Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Disposable Medical Specialty Bags Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Disposable Medical Specialty Bags Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Disposable Medical Specialty Bags Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Disposable Medical Specialty Bags Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Disposable Medical Specialty Bags Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Disposable Medical Specialty Bags Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Disposable Medical Specialty Bags Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Disposable Medical Specialty Bags Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Disposable Medical Specialty Bags Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Disposable Medical Specialty Bags Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Disposable Medical Specialty Bags Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Disposable Medical Specialty Bags Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Disposable Medical Specialty Bags Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Disposable Medical Specialty Bags Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Disposable Medical Specialty Bags Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Disposable Medical Specialty Bags Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Disposable Medical Specialty Bags Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Disposable Medical Specialty Bags Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Disposable Medical Specialty Bags Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Disposable Medical Specialty Bags Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Disposable Medical Specialty Bags Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Disposable Medical Specialty Bags Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Disposable Medical Specialty Bags Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Disposable Medical Specialty Bags Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Disposable Medical Specialty Bags Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Disposable Medical Specialty Bags Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Disposable Medical Specialty Bags?

The projected CAGR is approximately 4.52%.

2. Which companies are prominent players in the Disposable Medical Specialty Bags?

Key companies in the market include Coloplast A/S, ConvaTec Inc., Baxter International, Inc., B. Braun Melsungen AG, Hollister Incorporated, Medline Industries, Inc., Terumo Corporation, Nolato AB, Smiths Medical, acopharma.

3. What are the main segments of the Disposable Medical Specialty Bags?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.4 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Disposable Medical Specialty Bags," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Disposable Medical Specialty Bags report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Disposable Medical Specialty Bags?

To stay informed about further developments, trends, and reports in the Disposable Medical Specialty Bags, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence