Key Insights

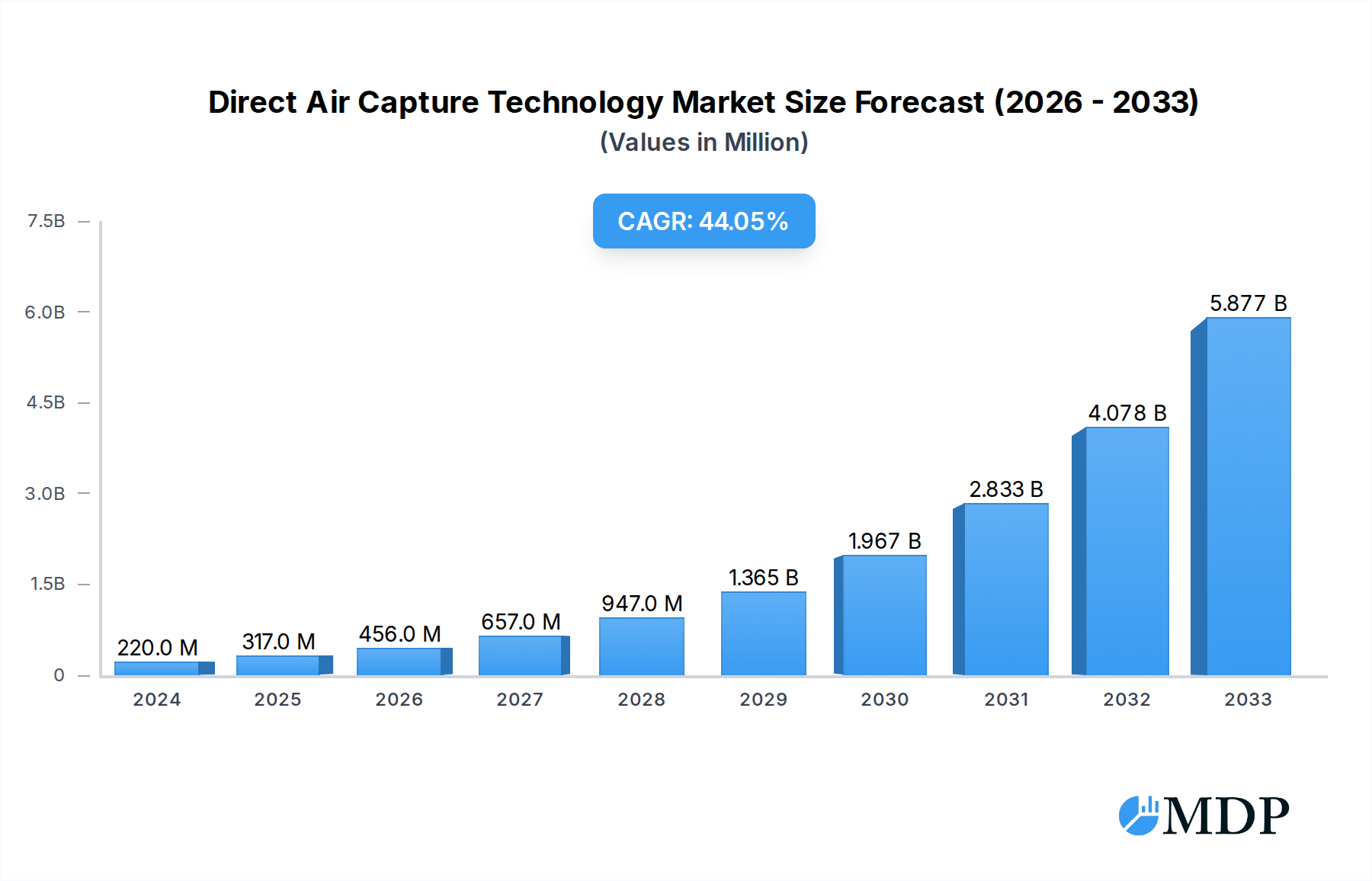

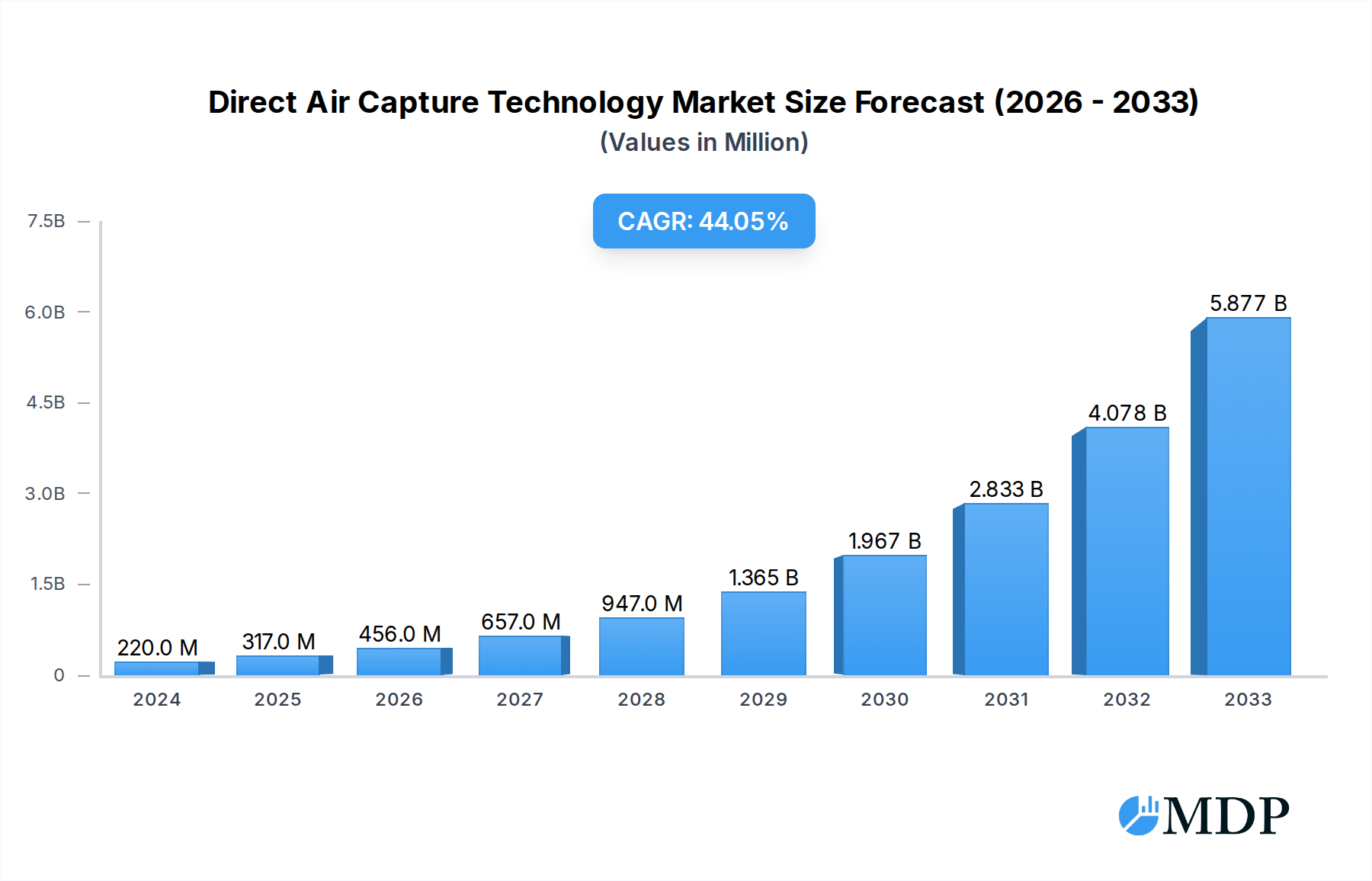

The Direct Air Capture (DAC) Technology market is experiencing phenomenal growth, projected to reach a staggering USD 220 million in 2024. This rapid expansion is driven by a CAGR of 43.8%, indicating a highly dynamic and rapidly evolving sector. The urgency to combat climate change and achieve net-zero emissions is the primary catalyst, propelling investments and innovation in DAC solutions. Key drivers include increasingly stringent environmental regulations worldwide, growing corporate sustainability initiatives, and the rising demand for carbon credits. Furthermore, advancements in DAC technologies, making them more efficient and cost-effective, are also significantly fueling market penetration. The sector is segmented into various applications, with Food and Beverage, Greenhouse, Energy, and Fuel emerging as significant adopters, leveraging DAC for carbon removal and utilization. The 'Physical Absorption in Liquid Media' and 'Adsorption on Solid Media' represent the dominant technological types currently employed. Prominent companies like Carbon Engineering, ClimeWorks, and Global Thermostat are at the forefront, developing and deploying innovative DAC solutions.

Direct Air Capture Technology Market Size (In Million)

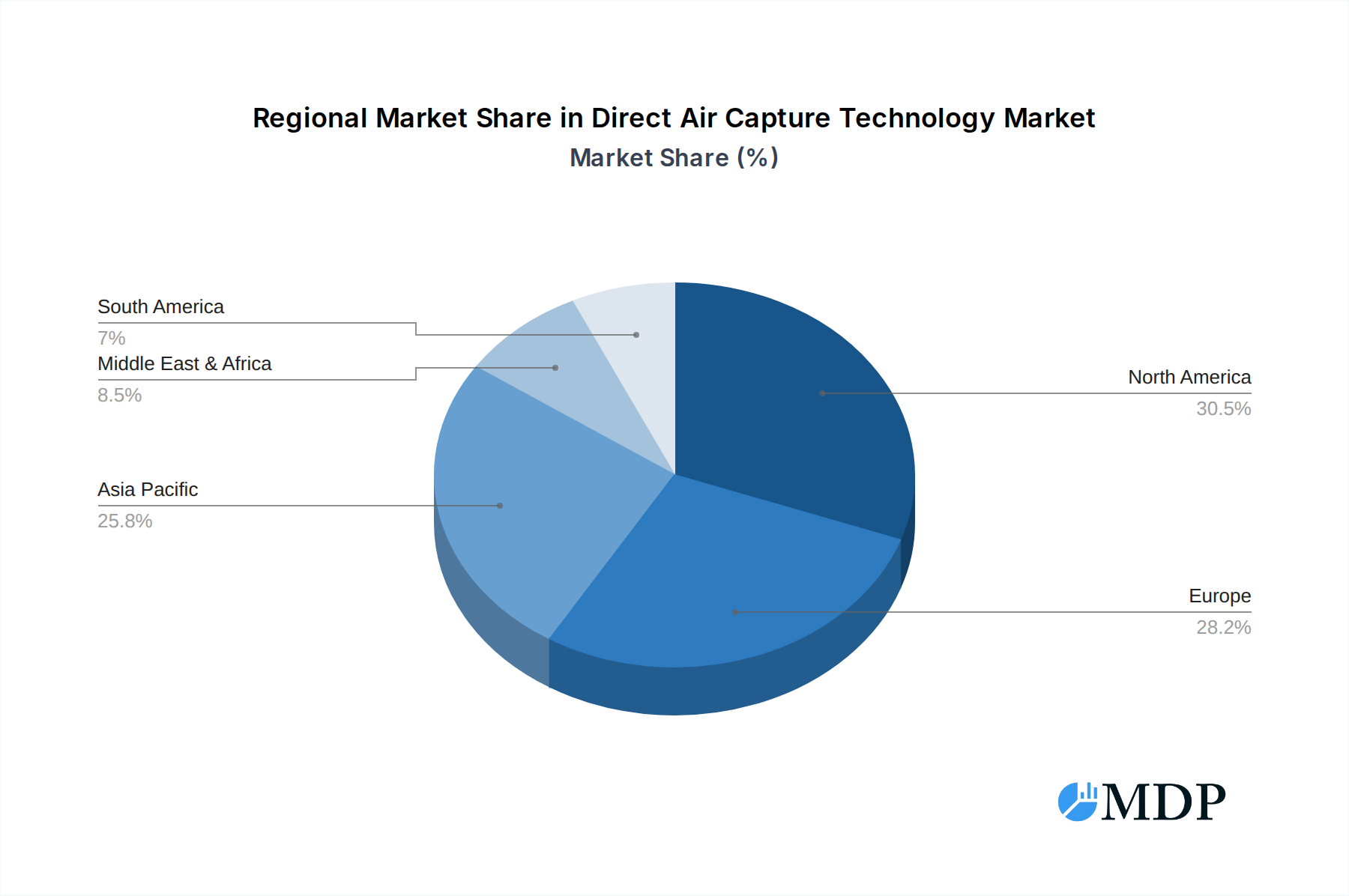

Looking ahead, the market is poised for sustained, robust growth throughout the forecast period of 2025-2033. While the initial market size for 2024 is estimated at USD 220 million, the projected CAGR suggests a significant upward trajectory. This expansion is expected to be supported by ongoing research and development, leading to improved capture efficiencies and reduced operational costs. The global push for decarbonization is creating a fertile ground for DAC technologies to scale, moving from pilot projects to large-scale commercial deployments. Restraints such as high initial capital investment and energy intensity are being addressed through technological innovations and supportive policy frameworks. Emerging trends like the integration of DAC with renewable energy sources for a truly low-carbon footprint and the development of carbon utilization pathways are further shaping the market's future. The Asia Pacific region, with its rapidly growing economies and increasing focus on environmental concerns, is expected to witness substantial growth, alongside established markets in North America and Europe.

Direct Air Capture Technology Company Market Share

Here is the SEO-optimized and engaging report description for Direct Air Capture Technology, structured as requested:

Direct Air Capture Technology Market Dynamics & Concentration

The Direct Air Capture (DAC) technology market is experiencing dynamic shifts, characterized by increasing innovation, evolving regulatory frameworks, and a growing awareness of climate change mitigation solutions. Market concentration is moderate, with key players like Carbon Engineering, ClimeWorks, and Global Thermostat leading the charge in developing and deploying DAC solutions. Innovation drivers are primarily technological advancements in sorbent materials, energy efficiency, and integration with renewable energy sources. Regulatory frameworks are nascent but rapidly developing, with governments worldwide introducing incentives and mandates to support carbon removal technologies. Product substitutes, such as nature-based solutions, are present but DAC offers unique advantages in terms of scalability and precise carbon removal. End-user trends show a strong demand from industries seeking to offset their carbon footprint, including those in the Food and Beverage, Greenhouse, Energy, and Fuel sectors. Mergers and acquisitions (M&A) activities are on the rise as larger entities recognize the strategic importance of DAC. We project an increase in M&A deal counts by over 50% within the forecast period. While market share is fragmented, the leading companies are steadily increasing their penetration, with a projected collective market share of over 60% by 2033. The pursuit of cost reduction and scalability remains a central theme, influencing investment and partnership strategies across the ecosystem.

Direct Air Capture Technology Industry Trends & Analysis

The Direct Air Capture (DAC) technology industry is on an upward trajectory, driven by an urgent global imperative to achieve net-zero emissions. The market growth drivers are multifaceted, encompassing robust policy support, significant investments from both public and private sectors, and a growing corporate commitment to sustainability. Technological disruptions are at the forefront, with continuous advancements in sorbent efficiency, modular plant designs, and integration with renewable energy sources to minimize the energy footprint of DAC operations. Consumer preferences, particularly within industrial and governmental purchasing, are increasingly favoring verifiable carbon removal solutions, making DAC a compelling option. Competitive dynamics are intensifying, with new entrants and established players vying for market dominance through innovation and strategic partnerships. The industry is witnessing a substantial increase in operational capacity and pilot projects worldwide. The estimated market penetration of DAC technology is expected to grow exponentially, with a projected Compound Annual Growth Rate (CAGR) of over 35% during the forecast period. This growth is fueled by the increasing cost-effectiveness of DAC systems and the rising price of carbon credits. The strategic positioning of DAC as a crucial tool for addressing residual emissions and historical carbon burdens further amplifies its market significance. The industry is also observing a trend towards hybrid DAC solutions that combine different capture mechanisms to optimize performance and cost across various environmental conditions. The commitment to climate targets is driving substantial R&D investments, promising further breakthroughs in the coming years.

Leading Markets & Segments in Direct Air Capture Technology

North America currently stands as the dominant region for Direct Air Capture (DAC) technology implementation and investment, driven by supportive governmental policies, significant private sector funding, and a strong focus on technological innovation. Within North America, the United States leads in terms of operational plants and research initiatives, spurred by initiatives like the U.S. Department of Energy's Carbon Negative Shot.

Dominant Application Segments:

- Energy: This segment is a primary driver due to the significant carbon footprint of fossil fuel-based energy production. DAC offers a pathway for energy companies to achieve carbon neutrality and explore carbon-neutral fuel production. Key drivers include stringent emissions regulations and the demand for sustainable energy solutions.

- Fuel: The production of synthetic fuels, often referred to as e-fuels or synthetic hydrocarbons, directly utilizes captured CO2. This is a crucial application for decarbonizing sectors like aviation and heavy transport. Economic policies promoting renewable fuels and the need for drop-in replacement fuels are significant drivers.

- Greenhouse: DAC technology is being adopted in greenhouse operations to provide concentrated CO2 for enhanced plant growth, leading to improved yields and resource efficiency. This application benefits from the direct economic advantages of increased agricultural productivity.

- Food and Beverage: While a smaller segment currently, the food and beverage industry is exploring DAC for carbon offsetting and for using captured CO2 in beverage carbonation and food preservation, driven by consumer demand for sustainable products.

Dominant Technology Types:

- Adsorption on Solid Media: This type of DAC, often championed by companies like ClimeWorks, is gaining traction due to its potential for modularity, lower energy requirements in certain configurations, and operational flexibility. The development of advanced solid sorbents with higher CO2 capture capacities and faster regeneration cycles is a key driver of its dominance.

- Physical Absorption in Liquid Media: Technologies such as those developed by Carbon Engineering utilize liquid solvents. This approach is notable for its scalability and potential for large-scale industrial deployment. Continuous improvements in solvent efficiency and the integration of waste heat for regeneration are strengthening its market position.

The dominance of these segments and types is underpinned by ongoing research and development, strategic partnerships, and the increasing economic viability of DAC solutions as carbon pricing mechanisms become more widespread.

Direct Air Capture Technology Product Developments

Product developments in Direct Air Capture (DAC) are focused on enhancing efficiency, reducing costs, and expanding deployment versatility. Innovations in sorbent materials, particularly solid adsorbents and advanced liquid solvents, are leading to higher CO2 capture rates and lower energy consumption during regeneration. Companies are also developing more modular and scalable DAC plant designs, enabling deployment in diverse locations and capacities. Competitive advantages are being realized through improved system integration with renewable energy sources, optimizing operational costs and minimizing the carbon footprint of the capture process itself. Furthermore, advancements in CO2 utilization pathways, such as conversion into synthetic fuels or building materials, are creating new market opportunities and enhancing the economic attractiveness of DAC technology.

Key Drivers of Direct Air Capture Technology Growth

The growth of Direct Air Capture (DAC) technology is propelled by a confluence of potent factors. Technological advancements in sorbent materials, energy efficiency, and process optimization are continuously driving down costs and improving capture rates. Economic factors, including the increasing price of carbon credits and growing investor confidence, are making DAC projects more financially viable. Regulatory frameworks worldwide are becoming more supportive, with governments implementing policies, incentives, and carbon pricing mechanisms that favor carbon removal solutions. The growing urgency to meet climate targets and the corporate push for net-zero commitments are creating a substantial demand for scalable carbon removal technologies like DAC, particularly for industries with hard-to-abate emissions.

Challenges in the Direct Air Capture Technology Market

Despite its promise, the Direct Air Capture (DAC) market faces significant hurdles. High capital and operational costs remain a primary challenge, though they are declining. Energy intensity for some DAC processes, even when powered by renewables, requires careful consideration of the overall carbon footprint. Scalability to meet global climate goals demands massive investment and rapid industrialization. Regulatory uncertainty and the lack of standardized carbon accounting methodologies can hinder project development and investment. Supply chain limitations for specialized materials and components can also pose bottlenecks. Competition from other carbon removal solutions, while not always direct substitutes, can influence market dynamics. The projected impact of these challenges on market growth is estimated to be a potential reduction of 15-20% in the pace of adoption without continued innovation and supportive policies.

Emerging Opportunities in Direct Air Capture Technology

The Direct Air Capture (DAC) landscape is ripe with emerging opportunities that promise to accelerate long-term growth. Technological breakthroughs in novel sorbent materials and energy-efficient regeneration processes are continuously improving performance and reducing costs. Strategic partnerships between DAC technology providers, renewable energy developers, and industrial emitters are creating integrated solutions and de-risking large-scale deployments. The expansion of CO2 utilization pathways, such as the production of sustainable aviation fuels, concrete, and chemicals, offers new revenue streams and enhances the economic case for DAC. Furthermore, the growing demand for verified carbon removal credits from corporations and governments seeking to achieve ambitious climate targets presents a significant market opportunity, driving investment and the scaling of DAC infrastructure globally.

Leading Players in the Direct Air Capture Technology Sector

- Carbon Engineering

- ClimeWorks

- Global Thermostat

- Heliogen

- Mitsubishi Heavy Industries

- Pacific Gas and Electric Company

- SygnoSphere

- Twelve

Key Milestones in Direct Air Capture Technology Industry

- 2019: ClimeWorks establishes its Orca DAC plant in Iceland, a significant milestone for large-scale operational capacity.

- 2020: Carbon Engineering announces plans for its first commercial-scale DAC facility in Texas, USA.

- 2021: The U.S. Department of Energy launches its Carbon Negative Shot initiative, aiming to reduce the cost of carbon removal.

- 2022: Global Thermostat secures significant funding for scaling its DAC technology.

- 2023: Twelve successfully demonstrates the production of sustainable jet fuel from captured CO2.

- 2024: Increased governmental funding and private sector investments signal accelerated project development and deployment.

Strategic Outlook for Direct Air Capture Technology Market

The strategic outlook for the Direct Air Capture (DAC) technology market is overwhelmingly positive, characterized by accelerating growth and expanding opportunities. Key growth accelerators include continued advancements in technology leading to further cost reductions, robust governmental support through incentives and carbon pricing, and increasing corporate demand for credible carbon removal solutions. The development of integrated DAC facilities coupled with renewable energy sources and CO2 utilization pathways will be crucial for economic viability. Strategic opportunities lie in expanding global deployment, fostering standardization in carbon accounting, and cultivating strong partnerships across the value chain to drive innovation and scale. The market is poised for significant expansion as it becomes a cornerstone of global climate mitigation strategies.

Direct Air Capture Technology Segmentation

-

1. Application

- 1.1. Food and Beverage

- 1.2. Greenhouse

- 1.3. Energy, Fuel, etc.

-

2. Types

- 2.1. Physical Absorption in Liquid Media

- 2.2. Adsorption on Solid Media

Direct Air Capture Technology Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Direct Air Capture Technology Regional Market Share

Geographic Coverage of Direct Air Capture Technology

Direct Air Capture Technology REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 43.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Direct Air Capture Technology Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food and Beverage

- 5.1.2. Greenhouse

- 5.1.3. Energy, Fuel, etc.

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Physical Absorption in Liquid Media

- 5.2.2. Adsorption on Solid Media

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Direct Air Capture Technology Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food and Beverage

- 6.1.2. Greenhouse

- 6.1.3. Energy, Fuel, etc.

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Physical Absorption in Liquid Media

- 6.2.2. Adsorption on Solid Media

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Direct Air Capture Technology Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food and Beverage

- 7.1.2. Greenhouse

- 7.1.3. Energy, Fuel, etc.

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Physical Absorption in Liquid Media

- 7.2.2. Adsorption on Solid Media

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Direct Air Capture Technology Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food and Beverage

- 8.1.2. Greenhouse

- 8.1.3. Energy, Fuel, etc.

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Physical Absorption in Liquid Media

- 8.2.2. Adsorption on Solid Media

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Direct Air Capture Technology Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food and Beverage

- 9.1.2. Greenhouse

- 9.1.3. Energy, Fuel, etc.

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Physical Absorption in Liquid Media

- 9.2.2. Adsorption on Solid Media

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Direct Air Capture Technology Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food and Beverage

- 10.1.2. Greenhouse

- 10.1.3. Energy, Fuel, etc.

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Physical Absorption in Liquid Media

- 10.2.2. Adsorption on Solid Media

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Carbon Engineering

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 ClimeWorks

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Global Thermostat

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.1 Carbon Engineering

List of Figures

- Figure 1: Global Direct Air Capture Technology Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Direct Air Capture Technology Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Direct Air Capture Technology Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Direct Air Capture Technology Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Direct Air Capture Technology Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Direct Air Capture Technology Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Direct Air Capture Technology Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Direct Air Capture Technology Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Direct Air Capture Technology Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Direct Air Capture Technology Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Direct Air Capture Technology Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Direct Air Capture Technology Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Direct Air Capture Technology Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Direct Air Capture Technology Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Direct Air Capture Technology Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Direct Air Capture Technology Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Direct Air Capture Technology Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Direct Air Capture Technology Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Direct Air Capture Technology Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Direct Air Capture Technology Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Direct Air Capture Technology Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Direct Air Capture Technology Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Direct Air Capture Technology Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Direct Air Capture Technology Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Direct Air Capture Technology Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Direct Air Capture Technology Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Direct Air Capture Technology Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Direct Air Capture Technology Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Direct Air Capture Technology Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Direct Air Capture Technology Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Direct Air Capture Technology Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Direct Air Capture Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Direct Air Capture Technology Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Direct Air Capture Technology Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Direct Air Capture Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Direct Air Capture Technology Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Direct Air Capture Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Direct Air Capture Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Direct Air Capture Technology Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Direct Air Capture Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Direct Air Capture Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Direct Air Capture Technology Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Direct Air Capture Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Direct Air Capture Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Direct Air Capture Technology Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Direct Air Capture Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Direct Air Capture Technology Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Direct Air Capture Technology Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Direct Air Capture Technology Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Direct Air Capture Technology Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Direct Air Capture Technology?

The projected CAGR is approximately 43.8%.

2. Which companies are prominent players in the Direct Air Capture Technology?

Key companies in the market include Carbon Engineering, ClimeWorks, Global Thermostat.

3. What are the main segments of the Direct Air Capture Technology?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Direct Air Capture Technology," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Direct Air Capture Technology report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Direct Air Capture Technology?

To stay informed about further developments, trends, and reports in the Direct Air Capture Technology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence