Key Insights

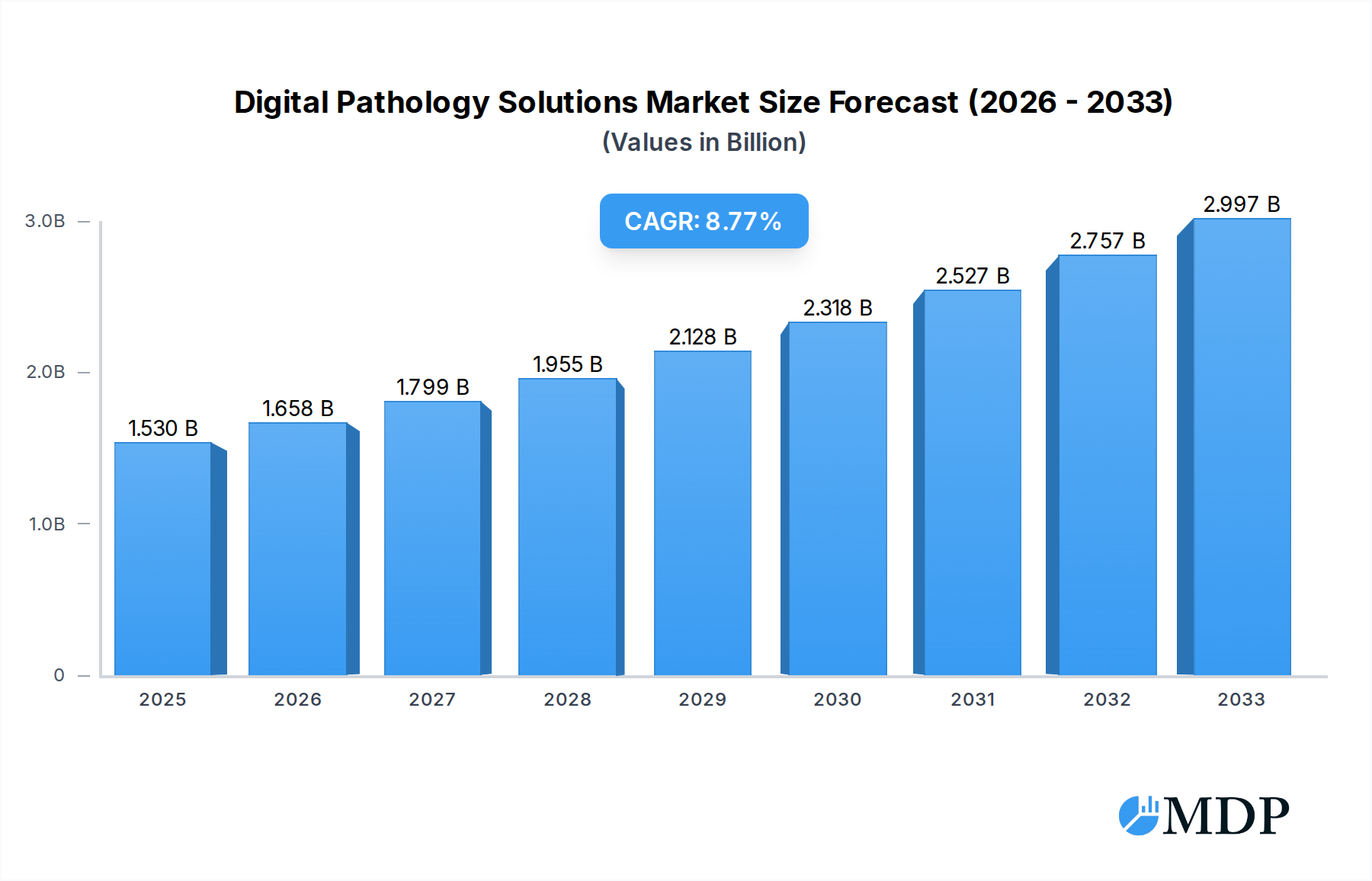

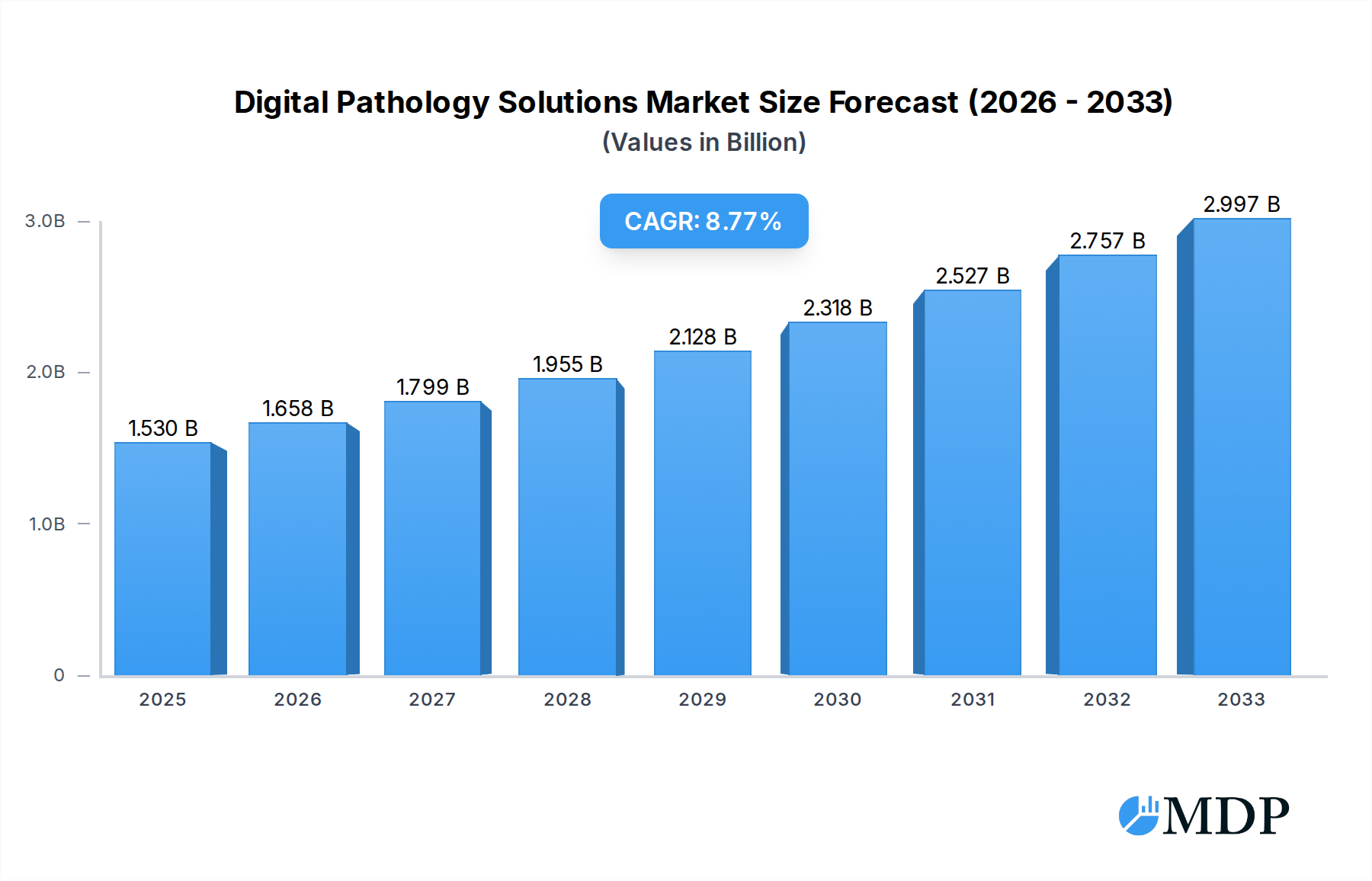

The global Digital Pathology Solutions market is poised for substantial growth, projected to reach a market size of $1.53 billion in 2025. Driven by an impressive Compound Annual Growth Rate (CAGR) of 8.6%, this sector is expected to witness sustained expansion through 2033. Key drivers fueling this surge include the increasing demand for accurate and efficient pathological diagnoses, particularly in the realm of cancer detection and treatment. The integration of artificial intelligence (AI) and machine learning (ML) algorithms is revolutionizing image analysis, enabling faster and more precise identification of disease markers. Furthermore, the growing need for streamlined workflows in clinical laboratories, coupled with the accelerating pace of drug discovery and development, are significant contributors to market expansion. The shift towards digitized archives for better data management and accessibility also plays a crucial role in driving adoption.

Digital Pathology Solutions Market Size (In Billion)

The market encompasses diverse applications, prominently featuring Pathological Diagnosis and Clinical Laboratory segments, alongside vital contributions to Drug Discovery and other related fields. In terms of types, Cytopathology and Histopathology are the primary categories witnessing significant technological advancements and market penetration. Restraints, such as the initial high cost of implementation and the need for robust IT infrastructure, are being progressively addressed through cloud-based solutions and increasing vendor support. Emerging trends like telepathology, remote consultations, and the development of advanced AI-powered diagnostic tools are further shaping the market landscape. Major industry players, including Hoffmann-La Roche AG, Philips, and Siemens, are actively investing in research and development, fostering innovation and expanding the global reach of digital pathology solutions.

Digital Pathology Solutions Company Market Share

This in-depth report provides an unparalleled analysis of the global Digital Pathology Solutions market, a rapidly evolving sector poised to revolutionize healthcare delivery. With a study period spanning from 2019 to 2033, a base and estimated year of 2025, and a robust forecast period of 2025–2033, this report offers critical insights into market dynamics, industry trends, leading segments, product innovations, growth drivers, challenges, emerging opportunities, key players, pivotal milestones, and a strategic outlook for this billion-dollar industry.

Digital Pathology Solutions Market Dynamics & Concentration

The Digital Pathology Solutions market exhibits a moderate to high concentration, with key players like Hoffmann-La Roche AG, Roche Diagnostics, Philips, and Siemens holding significant market share. Innovation drivers, fueled by advancements in AI, machine learning, and cloud computing, are continuously reshaping the landscape. Regulatory frameworks, while evolving, present a mixed bag of opportunities and hurdles, impacting adoption rates. Product substitutes, primarily traditional microscopy, are steadily being displaced by the superior efficiency and accuracy of digital solutions. End-user trends indicate a growing demand for integrated diagnostics, personalized medicine, and remote consultation capabilities, further propelling market growth. Merger and acquisition (M&A) activities are notable, with an estimated xx number of significant deals recorded in the historical period (2019–2024), indicating a strategic consolidation phase. Companies like Proscia and 3DHISTECH Ltd. are actively involved in these strategic moves, aiming to expand their technological portfolios and market reach. The overall market value is projected to surpass xx billion by 2033.

Digital Pathology Solutions Industry Trends & Analysis

The Digital Pathology Solutions industry is experiencing a transformative growth trajectory, driven by a confluence of factors that are fundamentally altering how diagnostic processes are conducted. The increasing prevalence of chronic diseases and the subsequent surge in diagnostic testing are major market growth drivers, pushing the demand for faster, more accurate, and efficient pathology workflows. Technological disruptions are at the forefront, with Artificial Intelligence (AI) and Machine Learning (ML) algorithms demonstrating remarkable capabilities in automating slide analysis, identifying complex biomarkers, and predicting disease progression, thereby enhancing diagnostic precision. Cloud-based platforms are also gaining traction, facilitating seamless data storage, retrieval, and sharing, enabling remote diagnostics and collaborative research on a global scale. Consumer preferences are shifting towards patient-centric healthcare models that emphasize early disease detection and personalized treatment plans, areas where digital pathology excels. The competitive dynamics within the industry are intensifying, with established giants like Philips and Siemens investing heavily in R&D alongside agile startups like Proscia and Tribun Health, all vying for market leadership. The market penetration of digital pathology solutions, though still nascent in some regions, is steadily increasing, with a projected Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period. This growth is underpinned by a growing understanding of the economic benefits, including reduced turnaround times, improved resource allocation, and enhanced diagnostic accuracy leading to better patient outcomes. The total market value is expected to reach an impressive xx billion by 2033.

Leading Markets & Segments in Digital Pathology Solutions

The Pathological Diagnosis application segment stands as the dominant force within the global Digital Pathology Solutions market. This leadership is primarily driven by the increasing need for accurate and timely cancer diagnoses, where digital pathology offers unparalleled advantages in visualizing and analyzing tissue samples. The Clinical Laboratory segment follows closely, as laboratories worldwide are embracing digital solutions to streamline workflows, improve efficiency, and reduce turnaround times for routine diagnostics.

Key Drivers for Dominance in Pathological Diagnosis and Clinical Laboratory Segments:

- Technological Advancements: The continuous development of high-resolution scanners, advanced image analysis software, and AI-powered diagnostic tools directly addresses the core needs of pathology labs.

- Cost-Effectiveness: While initial investments can be substantial, the long-term cost savings associated with reduced manual labor, improved efficiency, and decreased slide wastage are significant.

- Regulatory Support: As regulatory bodies increasingly approve digital pathology solutions for primary diagnosis, their adoption in clinical settings is accelerating.

- Interoperability and Integration: The ability of digital pathology systems to integrate with existing Laboratory Information Systems (LIS) and Electronic Health Records (EHRs) is crucial for seamless workflow implementation.

Dominance Analysis of Key Segments:

The Histopathology type segment is the largest contributor to the digital pathology market. This is due to the extensive use of tissue samples in the diagnosis of a wide range of diseases, particularly cancers. The detailed microscopic examination of tissue morphology is critical, and digital histopathology offers enhanced visualization, quantitative analysis, and archival capabilities. Cytopathology, while smaller, is also experiencing significant growth as advancements in digital cytology solutions improve the accuracy and efficiency of analyzing cells from various bodily fluids and fine-needle aspirations.

Leading Regions and Countries:

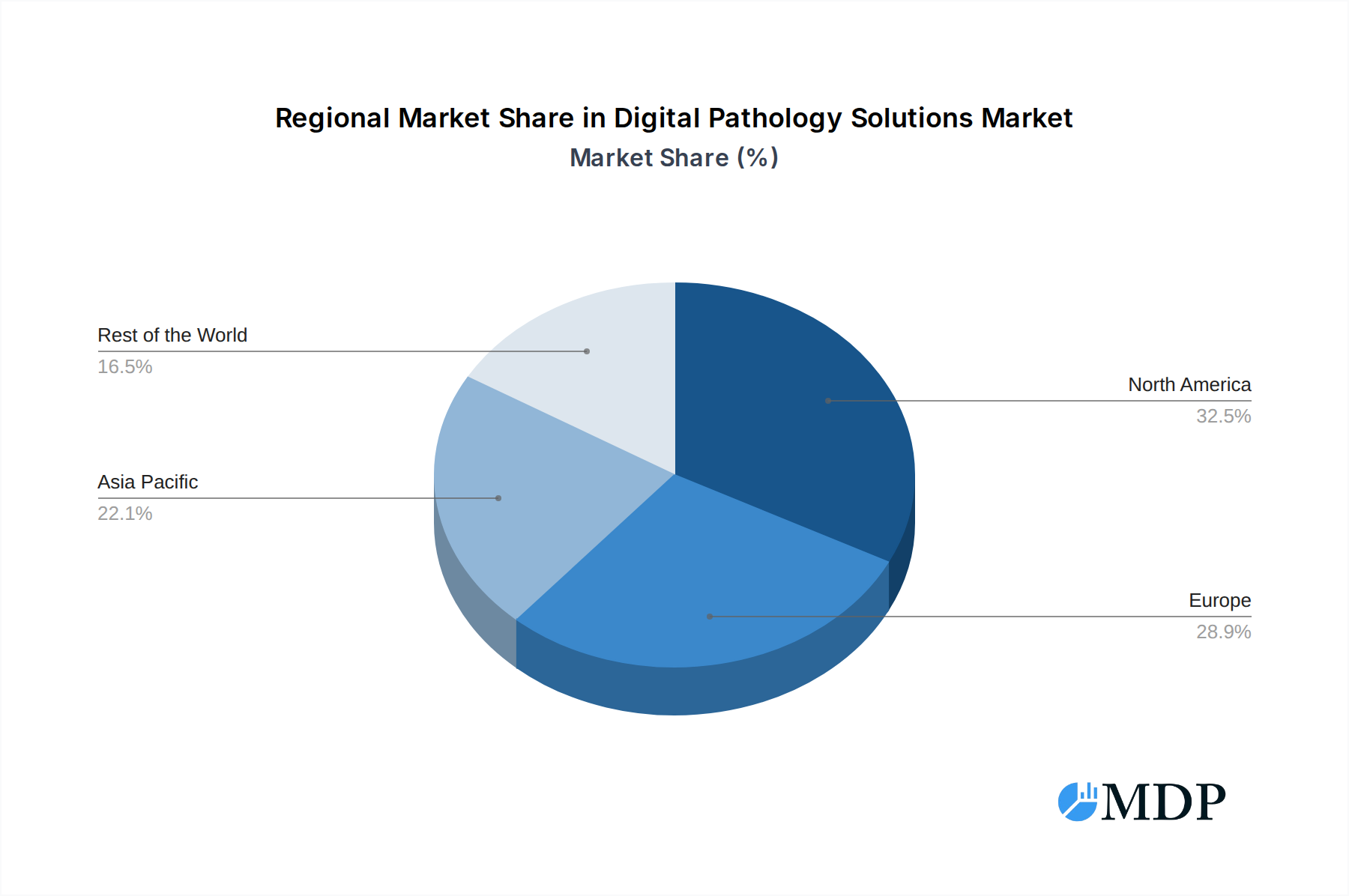

North America, particularly the United States, currently leads the market, owing to early adoption of advanced technologies, robust healthcare infrastructure, and significant investments in medical research and development. Europe, with countries like Germany and the UK, is also a major market, driven by a strong focus on innovation and increasing healthcare expenditure. The Asia-Pacific region, especially China and India, is poised for substantial growth due to rising healthcare awareness, a growing patient pool, and increasing government initiatives to modernize healthcare facilities.

Digital Pathology Solutions Product Developments

Product innovation in the Digital Pathology Solutions market is characterized by the integration of artificial intelligence (AI) and machine learning (ML) for automated slide analysis, anomaly detection, and quantitative biomarker assessment. Companies are focusing on developing high-throughput scanners for rapid slide digitization and cloud-based platforms for secure data storage, remote access, and collaborative diagnostics. These advancements offer competitive advantages by improving diagnostic accuracy, reducing turnaround times, and enabling new applications in drug discovery and personalized medicine. The market is witnessing a surge in software solutions that provide advanced image analysis, workflow automation, and predictive insights, enhancing the overall value proposition of digital pathology.

Key Drivers of Digital Pathology Solutions Growth

The growth of the Digital Pathology Solutions market is propelled by several key factors. Technologically, the rapid advancements in whole-slide imaging (WSI) scanners, coupled with the increasing sophistication of AI and machine learning algorithms for image analysis, are significant catalysts. Economically, the rising healthcare expenditure globally, coupled with the need for cost-effective and efficient diagnostic methods, is driving adoption. Regulatory frameworks are also becoming more supportive, with increasing approvals for digital pathology in primary diagnostic settings, further encouraging investment and implementation. The demand for personalized medicine and companion diagnostics also plays a crucial role, as digital pathology enables detailed analysis of biomarkers crucial for targeted therapies.

Challenges in the Digital Pathology Solutions Market

Despite its immense potential, the Digital Pathology Solutions market faces several challenges. Regulatory hurdles, particularly in obtaining approvals for AI-driven diagnostic tools and ensuring data privacy and security, can impede market entry and adoption. The high initial cost of implementing digital pathology systems, including scanners, software, and IT infrastructure, remains a significant barrier for smaller institutions. Furthermore, the need for extensive training and change management for pathologists and laboratory staff to adapt to new digital workflows can create resistance. Interoperability issues between different vendor systems and the lack of standardized data formats can also hinder seamless integration. Cybersecurity threats and the potential for data breaches necessitate robust security measures, adding to implementation costs and complexity.

Emerging Opportunities in Digital Pathology Solutions

Emerging opportunities in the Digital Pathology Solutions market are primarily driven by technological breakthroughs and strategic market expansion. The integration of AI and ML is not just about automation; it's opening doors for predictive diagnostics, enabling earlier disease detection and personalized treatment strategies. The growing demand for precision medicine in oncology, for instance, creates a significant opportunity for digital pathology to become an indispensable tool for biomarker identification and patient stratification. Strategic partnerships between technology providers, pharmaceutical companies, and research institutions are fostering innovation and accelerating the development of novel applications, particularly in drug discovery and clinical trials. Furthermore, the expanding healthcare infrastructure in emerging economies presents a substantial opportunity for market penetration, as these regions seek to leapfrog traditional technologies with advanced digital solutions. The development of telepathology services, facilitated by robust digital infrastructure, is also a burgeoning area, offering greater accessibility to expert diagnostics in remote or underserved areas.

Leading Players in the Digital Pathology Solutions Sector

- Hoffmann-La Roche AG

- Roche Diagnostics

- Proscia

- 3DHISTECH Ltd.

- Philips

- Siemens

- Q2 Solutions

- TriStar Technology Group

- Iron Mountain

- Smart In Media AG

- HealthTrust Europe

- Dedalus

- Tribun Health

- Qube scientific

- Leica Biosystems

Key Milestones in Digital Pathology Solutions Industry

- 2019: FDA clearance of the first fully digital pathology solution for primary diagnosis.

- 2020: Increased adoption of telepathology services driven by the global pandemic, accelerating remote diagnostics.

- 2021: Significant investments in AI-powered pathology platforms by major tech and healthcare companies, boosting market confidence.

- 2022: Launch of new AI algorithms for automated cancer detection and grading, improving efficiency and accuracy.

- 2023: Growing emphasis on interoperability standards for digital pathology systems, facilitating seamless integration with LIS and EHRs.

- 2024: Expansion of digital pathology solutions into new therapeutic areas beyond oncology, such as infectious diseases and neurological disorders.

Strategic Outlook for Digital Pathology Solutions Market

The strategic outlook for the Digital Pathology Solutions market is exceptionally bright, characterized by sustained growth accelerators and significant future potential. The ongoing advancements in AI and machine learning are set to further enhance diagnostic capabilities, driving the adoption of predictive and personalized medicine approaches. The increasing demand for integrated diagnostic workflows, where digital pathology seamlessly connects with other healthcare data sources, will be a key growth driver. Furthermore, the expanding penetration into emerging markets, coupled with strategic collaborations and mergers, will solidify the market's global reach. Investment in cloud-based infrastructure and cybersecurity will be paramount to ensure scalability and data integrity. The market is poised for continued innovation, leading to a more efficient, accurate, and accessible future for pathology services worldwide.

Digital Pathology Solutions Segmentation

-

1. Application

- 1.1. Pathological Diagnosis

- 1.2. Clinical Laboratory

- 1.3. Drug Discovery

- 1.4. Others

-

2. Types

- 2.1. Cytopathology

- 2.2. Histopathology

Digital Pathology Solutions Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Digital Pathology Solutions Regional Market Share

Geographic Coverage of Digital Pathology Solutions

Digital Pathology Solutions REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Digital Pathology Solutions Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pathological Diagnosis

- 5.1.2. Clinical Laboratory

- 5.1.3. Drug Discovery

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cytopathology

- 5.2.2. Histopathology

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Digital Pathology Solutions Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pathological Diagnosis

- 6.1.2. Clinical Laboratory

- 6.1.3. Drug Discovery

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cytopathology

- 6.2.2. Histopathology

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Digital Pathology Solutions Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pathological Diagnosis

- 7.1.2. Clinical Laboratory

- 7.1.3. Drug Discovery

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cytopathology

- 7.2.2. Histopathology

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Digital Pathology Solutions Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pathological Diagnosis

- 8.1.2. Clinical Laboratory

- 8.1.3. Drug Discovery

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cytopathology

- 8.2.2. Histopathology

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Digital Pathology Solutions Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pathological Diagnosis

- 9.1.2. Clinical Laboratory

- 9.1.3. Drug Discovery

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cytopathology

- 9.2.2. Histopathology

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Digital Pathology Solutions Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pathological Diagnosis

- 10.1.2. Clinical Laboratory

- 10.1.3. Drug Discovery

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cytopathology

- 10.2.2. Histopathology

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Hoffmann-La Roche AG

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Roche Diagnostics

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Proscia

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 3DHISTECH Ltd.

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Philips

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Siemens

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Q2 Solutions

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 TriStar Technology Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Iron Mountain

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Smart In Media AG

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 HealthTrust Europe

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Dedalus

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Tribun Health

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Qube scientific

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Leica Biosystems

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Hoffmann-La Roche AG

List of Figures

- Figure 1: Global Digital Pathology Solutions Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Digital Pathology Solutions Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Digital Pathology Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Digital Pathology Solutions Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Digital Pathology Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Digital Pathology Solutions Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Digital Pathology Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Digital Pathology Solutions Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Digital Pathology Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Digital Pathology Solutions Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Digital Pathology Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Digital Pathology Solutions Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Digital Pathology Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Digital Pathology Solutions Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Digital Pathology Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Digital Pathology Solutions Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Digital Pathology Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Digital Pathology Solutions Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Digital Pathology Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Digital Pathology Solutions Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Digital Pathology Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Digital Pathology Solutions Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Digital Pathology Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Digital Pathology Solutions Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Digital Pathology Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Digital Pathology Solutions Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Digital Pathology Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Digital Pathology Solutions Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Digital Pathology Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Digital Pathology Solutions Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Digital Pathology Solutions Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Digital Pathology Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Digital Pathology Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Digital Pathology Solutions Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Digital Pathology Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Digital Pathology Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Digital Pathology Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Digital Pathology Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Digital Pathology Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Digital Pathology Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Digital Pathology Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Digital Pathology Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Digital Pathology Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Digital Pathology Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Digital Pathology Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Digital Pathology Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Digital Pathology Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Digital Pathology Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Digital Pathology Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Digital Pathology Solutions Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Digital Pathology Solutions?

The projected CAGR is approximately 8.6%.

2. Which companies are prominent players in the Digital Pathology Solutions?

Key companies in the market include Hoffmann-La Roche AG, Roche Diagnostics, Proscia, 3DHISTECH Ltd., Philips, Siemens, Q2 Solutions, TriStar Technology Group, Iron Mountain, Smart In Media AG, HealthTrust Europe, Dedalus, Tribun Health, Qube scientific, Leica Biosystems.

3. What are the main segments of the Digital Pathology Solutions?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.53 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Digital Pathology Solutions," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Digital Pathology Solutions report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Digital Pathology Solutions?

To stay informed about further developments, trends, and reports in the Digital Pathology Solutions, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence