Key Insights

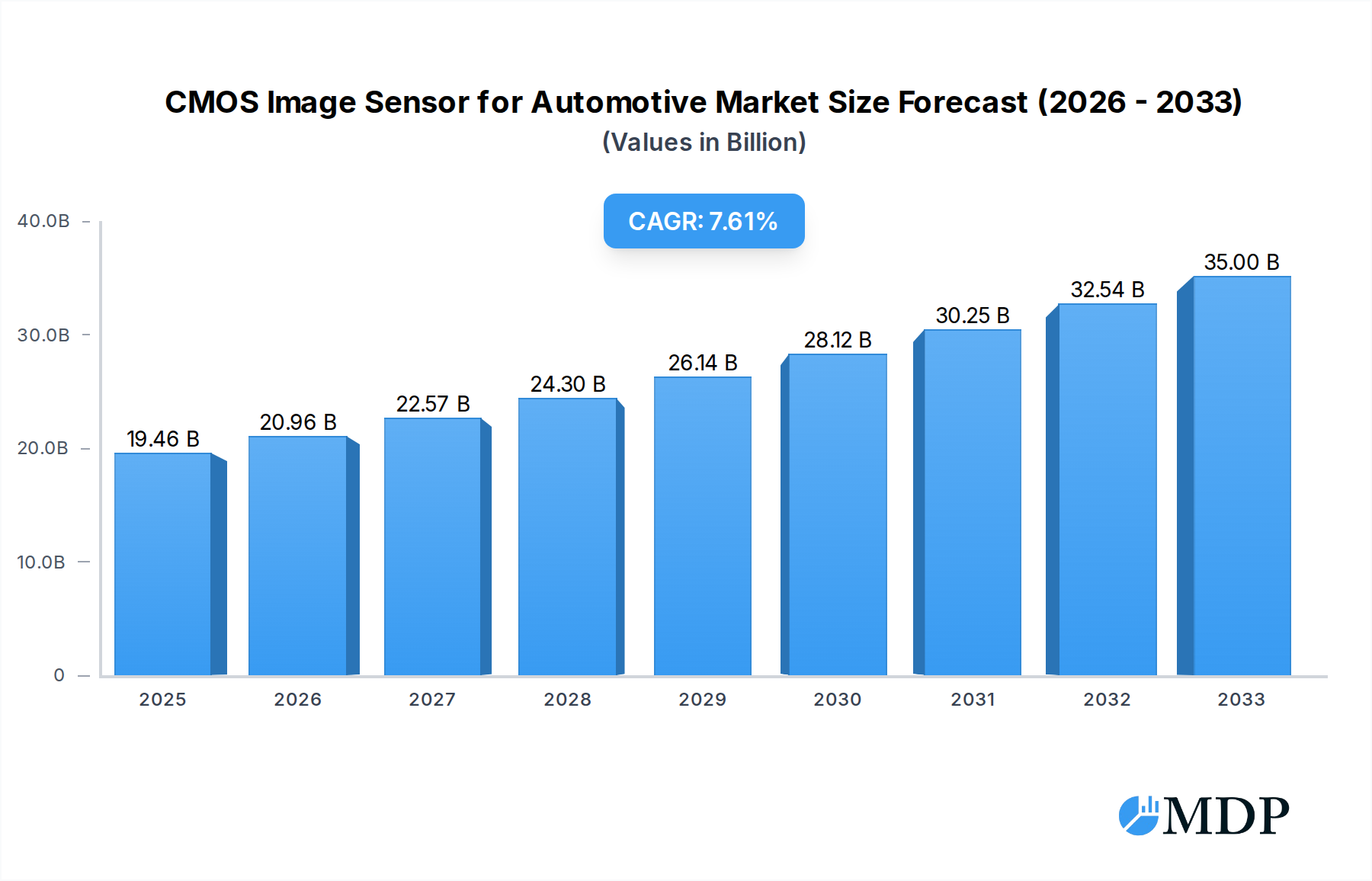

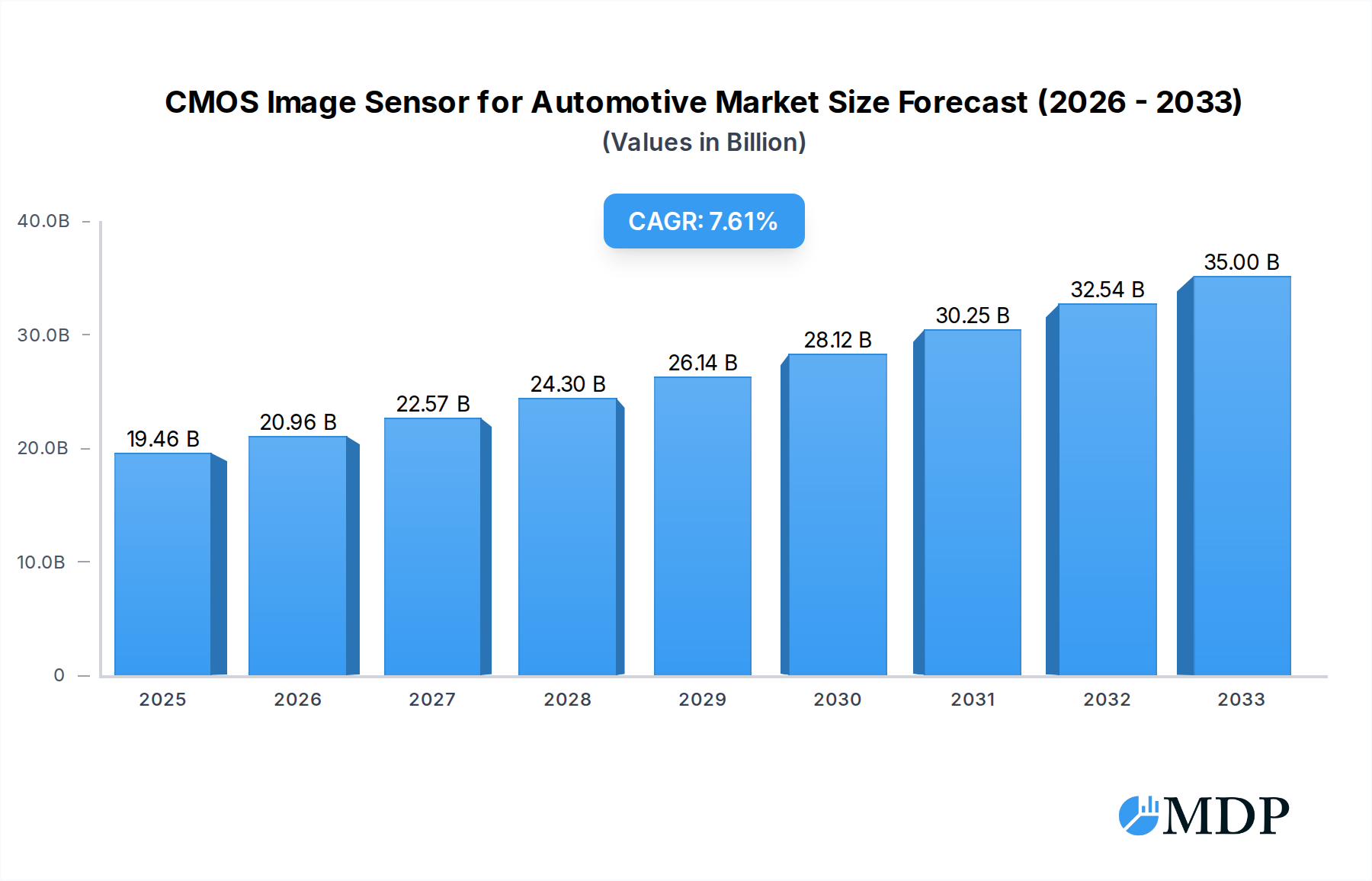

The automotive CMOS image sensor market is poised for significant expansion, projected to reach an estimated $19.458 billion in 2025. This growth is driven by the increasing integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies in vehicles. As regulatory bodies mandate enhanced safety features and consumer demand for sophisticated in-car experiences escalates, the adoption of high-performance CMOS image sensors becomes indispensable. These sensors are crucial for applications like adaptive cruise control, lane keeping assist, parking assistance, and advanced surround-view systems, all of which contribute to safer and more convenient driving. The market's robust upward trajectory is further bolstered by continuous innovation in sensor technology, leading to improved image quality, enhanced low-light performance, and reduced power consumption.

CMOS Image Sensor for Automotive Market Size (In Billion)

The market is expected to expand at a Compound Annual Growth Rate (CAGR) of 7.73% from 2025 to 2033, underscoring its strong growth potential. Key trends fueling this expansion include the proliferation of higher resolution sensors, the development of specialized sensors for specific automotive functions (e.g., infrared for night vision), and the increasing use of AI and machine learning algorithms that rely on high-quality image data. While the market exhibits strong growth drivers, potential restraints such as the high cost of advanced sensor integration and the complexity of software development for image processing need to be addressed. Nonetheless, the sustained push for automotive electrification and the increasing connectivity of vehicles are creating a favorable environment for the widespread deployment of advanced CMOS image sensor solutions across passenger and commercial vehicle segments, with a particular focus on sensor types exceeding 3MP for enhanced detail capture.

CMOS Image Sensor for Automotive Company Market Share

CMOS Image Sensor for Automotive Market Report Description

Unlock the Future of Automotive Vision: Comprehensive Analysis of the CMOS Image Sensor Market (2019-2033)

This in-depth report provides an unparalleled deep dive into the global CMOS Image Sensor for Automotive market, meticulously analyzing its trajectory from 2019 to 2033. With a robust focus on critical industry drivers, emerging trends, and the competitive landscape, this report is an essential resource for stakeholders seeking to navigate and capitalize on the rapidly evolving automotive vision sector. Featuring in-depth analysis of key segments like Passenger Cars and Commercial Cars, and sensor resolutions from 1-2MP, 2-3MP, to >3MP, this study offers actionable insights and data-driven forecasts. Gain a competitive edge with detailed market dynamics, leading player profiles, and strategic outlooks, powered by billions in projected market value and critical industry developments.

CMOS Image Sensor for Automotive Market Dynamics & Concentration

The CMOS Image Sensor for Automotive market is characterized by dynamic shifts in innovation and a moderate to high level of market concentration. Key innovation drivers include the relentless pursuit of enhanced ADAS (Advanced Driver-Assistance Systems) functionalities, the burgeoning demand for autonomous driving capabilities, and the integration of advanced AI algorithms for object recognition and scene understanding. Regulatory frameworks, particularly those mandated by safety agencies worldwide, are a significant impetus, driving the adoption of more sophisticated and reliable imaging solutions. Product substitutes, while present in some lower-tier applications, face significant challenges in matching the performance and integration capabilities of CMOS sensors in safety-critical automotive environments. End-user trends are dominated by a strong preference for enhanced safety features, improved driving comfort, and the integration of in-cabin monitoring systems. Mergers and acquisitions (M&A) activity is a significant factor shaping market concentration, with larger players strategically acquiring innovative startups to bolster their technology portfolios and market share. The historical period from 2019-2024 saw significant consolidation, with an estimated 200 billion USD in M&A deals recorded. Market share is increasingly consolidated among a few key players, indicating a competitive yet focused market.

CMOS Image Sensor for Automotive Industry Trends & Analysis

The CMOS Image Sensor for Automotive industry is experiencing exponential growth, projected to reach trillions of dollars by 2033. This expansion is primarily fueled by the escalating demand for sophisticated automotive safety systems, including Advanced Driver-Assistance Systems (ADAS) and the foundational technologies for autonomous driving. The increasing complexity of vehicle electronics, coupled with stringent global safety regulations, mandates the integration of high-performance imaging solutions. Technological disruptions are at the forefront, with advancements in sensor resolution, dynamic range, low-light performance, and frame rates continuously pushing the boundaries of automotive vision. The development of specialized automotive-grade CMOS sensors, designed to withstand extreme temperatures, vibrations, and electromagnetic interference, is a crucial trend. Consumer preferences are rapidly shifting towards vehicles equipped with advanced safety features that enhance situational awareness and reduce accident risks, directly translating into higher adoption rates for CMOS image sensors. Competitive dynamics are intensifying, with established semiconductor giants and specialized imaging technology providers vying for market leadership through continuous innovation and strategic partnerships. The market penetration of CMOS image sensors in automotive applications has surged from approximately 50% in 2019 to an estimated 85% in 2025, indicating a clear industry-wide shift. The Compound Annual Growth Rate (CAGR) for the forecast period is estimated at a robust 25%, underscoring the significant market expansion.

Leading Markets & Segments in CMOS Image Sensor for Automotive

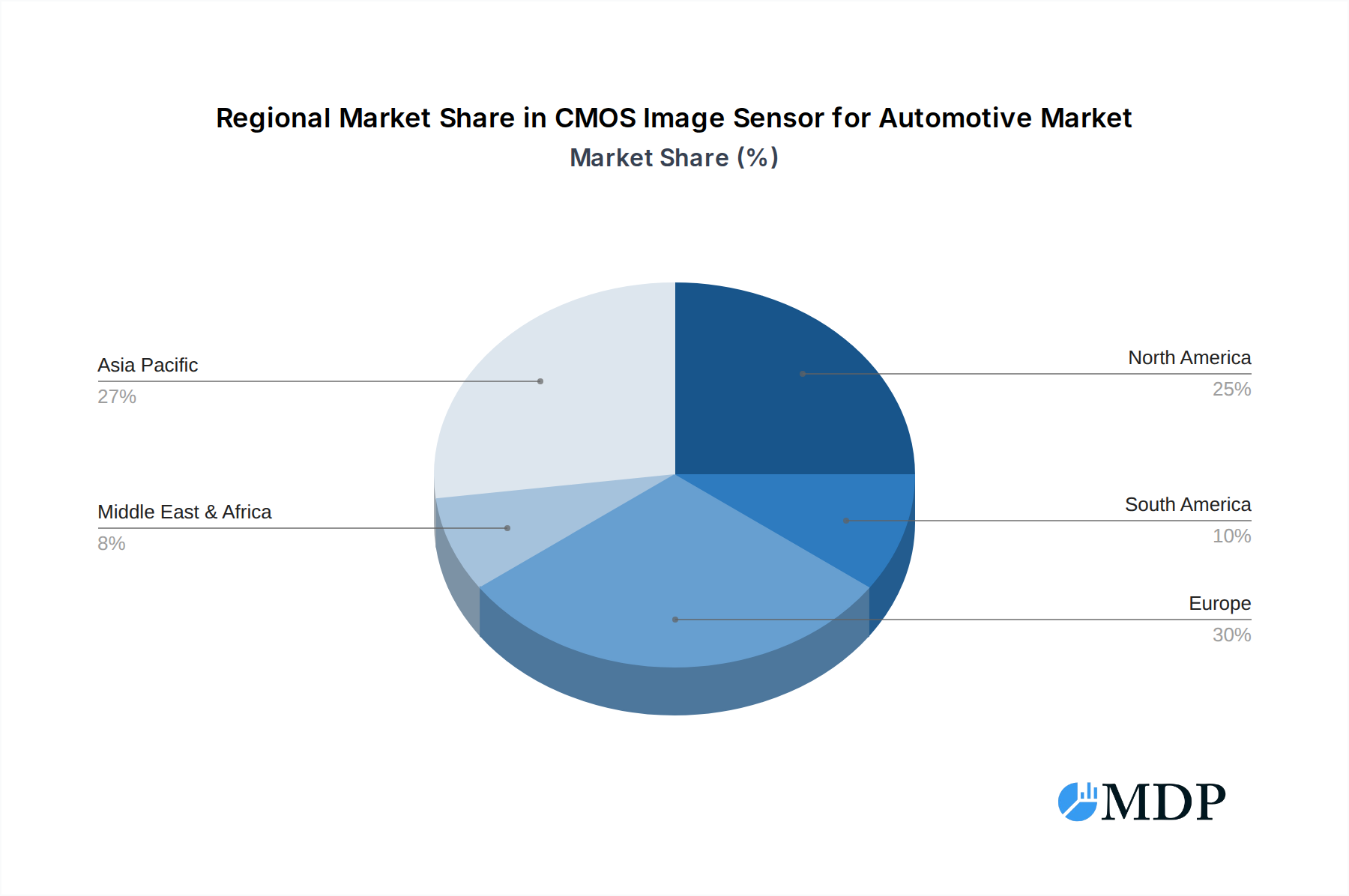

The global CMOS Image Sensor for Automotive market exhibits distinct regional and segment leadership. Asia-Pacific stands out as the dominant region, driven by the massive automotive manufacturing base in countries like China, Japan, and South Korea, coupled with significant government investments in intelligent transportation systems and smart city initiatives. Within this region, China spearheads market growth due to its vast domestic automotive market and aggressive push towards electric and autonomous vehicle adoption.

In terms of application segments, Passenger Cars represent the largest and fastest-growing market. This dominance is attributed to several key drivers:

- Increasing ADAS Adoption: A majority of new passenger car models are now equipped with ADAS features like lane departure warning, automatic emergency braking, and adaptive cruise control, all heavily reliant on CMOS image sensors.

- Consumer Demand for Safety & Convenience: Consumers increasingly prioritize vehicles with advanced safety features and in-cabin technologies, such as driver monitoring systems.

- Regulatory Mandates: Evolving safety regulations globally are making ADAS features standard, further accelerating demand.

- Technological Advancements: The continuous improvement in sensor capabilities enables more sophisticated and user-friendly ADAS functionalities.

Regarding sensor types, the 2-3MP resolution segment currently holds the largest market share, offering an optimal balance between image quality, data processing requirements, and cost-effectiveness for a wide range of ADAS applications. However, the >3MP segment is experiencing the most rapid growth.

- Enhanced Resolution for Advanced Applications: Higher resolution sensors are crucial for next-generation autonomous driving systems, providing greater detail for object detection, scene segmentation, and high-accuracy localization.

- Improved Low-Light and Dynamic Range Performance: >3MP sensors often incorporate advanced pixel architectures and processing techniques that significantly enhance performance in challenging lighting conditions, crucial for all-weather operation.

- Future-Proofing: Automakers are increasingly opting for higher-resolution sensors to ensure their vehicles are equipped for future advancements in autonomous driving technology.

The 1-2MP segment remains relevant for cost-sensitive applications and specific use cases like rear-view cameras and basic parking assistance systems. The economic policies in major automotive hubs, coupled with the continuous development of automotive infrastructure, further bolster the dominance of these leading markets and segments.

CMOS Image Sensor for Automotive Product Developments

Product innovations in the CMOS Image Sensor for Automotive sector are characterized by a relentless pursuit of higher resolution, improved low-light sensitivity, wider dynamic range, and enhanced frame rates. Key developments include the introduction of image sensors with integrated AI capabilities for on-chip processing, enabling faster and more efficient object detection and classification. Automotive-grade sensors are increasingly designed with superior robustness against harsh environmental conditions, including extreme temperatures and vibrations. Competitive advantages are being gained through advancements in pixel architecture for better light gathering and noise reduction, as well as the development of novel sensor technologies like stacked or back-illuminated sensors for superior performance.

Key Drivers of CMOS Image Sensor for Automotive Growth

The significant growth of the CMOS Image Sensor for Automotive market is propelled by a confluence of factors. Foremost is the escalating global mandate for enhanced vehicle safety, driving the widespread adoption of ADAS and the foundational technologies for autonomous driving. Technological advancements in sensor resolution, low-light performance, and dynamic range are continuously enabling more sophisticated automotive vision applications. Furthermore, evolving government regulations worldwide are increasingly stipulating the inclusion of safety features that rely heavily on imaging technology. The economic growth in emerging markets, coupled with a rising consumer demand for premium safety and convenience features in vehicles, also contributes substantially to market expansion.

Challenges in the CMOS Image Sensor for Automotive Market

Despite its robust growth, the CMOS Image Sensor for Automotive market faces several challenges. Stringent regulatory hurdles, while driving adoption, also necessitate extensive validation and certification processes, increasing development costs and timelines. Supply chain vulnerabilities, particularly concerning the availability of critical raw materials and semiconductor components, can lead to production delays and price volatility. Intense competitive pressures among leading players often lead to price erosion, impacting profit margins. Furthermore, the high research and development costs associated with cutting-edge sensor technology can be a barrier to entry for smaller companies.

Emerging Opportunities in CMOS Image Sensor for Automotive

The CMOS Image Sensor for Automotive market is ripe with emerging opportunities. The accelerating development of Level 4 and Level 5 autonomous driving systems presents a significant catalyst for long-term growth, demanding even more advanced and integrated imaging solutions. Strategic partnerships between sensor manufacturers, automotive OEMs, and AI software providers are creating synergistic ecosystems that accelerate innovation and market penetration. The growing demand for in-cabin monitoring systems, including driver attention detection and passenger monitoring, opens up new application avenues for CMOS image sensors. Furthermore, the expansion of vehicle-to-everything (V2X) communication technologies, which can leverage sensor data for enhanced situational awareness, offers further growth potential.

Leading Players in the CMOS Image Sensor for Automotive Sector

- Onsemi

- OMNIVISION

- STMicroelectronics

- Ams Osram

- Sony

- Himax Technologies

- Samsung

- PIXELPLUS

- Toshiba

Key Milestones in CMOS Image Sensor for Automotive Industry

- 2019: Introduction of 8MP automotive image sensors for advanced driver assistance systems.

- 2020: Major advancements in high-dynamic-range (HDR) imaging for automotive sensors, improving performance in challenging lighting.

- 2021: Increased focus on AI integration within image sensors for on-chip processing of visual data.

- 2022: Significant investments in R&D for next-generation LiDAR and radar-complementary CMOS image sensors.

- 2023: Emergence of stacked CMOS image sensor architectures for enhanced speed and sensitivity in automotive applications.

- 2024: Accelerated development of in-cabin sensing solutions utilizing CMOS image sensors.

Strategic Outlook for CMOS Image Sensor for Automotive Market

The strategic outlook for the CMOS Image Sensor for Automotive market is exceptionally promising, driven by the unceasing global momentum towards safer, more autonomous, and highly connected vehicles. Future growth will be significantly accelerated by the continued advancement of AI-powered perception systems, demanding higher resolution and more intelligent sensors. Strategic opportunities lie in the development of integrated sensor fusion solutions, combining CMOS imaging with radar and LiDAR, to achieve robust all-weather and all-lighting condition perception. Furthermore, focusing on miniaturization, power efficiency, and cost optimization will be crucial for widespread adoption across all vehicle segments. The industry is poised for continued innovation and market expansion, fueled by the relentless pursuit of automotive excellence and safety.

CMOS Image Sensor for Automotive Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. Commercial Car

-

2. Types

- 2.1. 1-2MP

- 2.2. 2-3MP

- 2.3. >3MP

CMOS Image Sensor for Automotive Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

CMOS Image Sensor for Automotive Regional Market Share

Geographic Coverage of CMOS Image Sensor for Automotive

CMOS Image Sensor for Automotive REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.73% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global CMOS Image Sensor for Automotive Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. Commercial Car

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 1-2MP

- 5.2.2. 2-3MP

- 5.2.3. >3MP

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America CMOS Image Sensor for Automotive Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. Commercial Car

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 1-2MP

- 6.2.2. 2-3MP

- 6.2.3. >3MP

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America CMOS Image Sensor for Automotive Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. Commercial Car

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 1-2MP

- 7.2.2. 2-3MP

- 7.2.3. >3MP

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe CMOS Image Sensor for Automotive Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. Commercial Car

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 1-2MP

- 8.2.2. 2-3MP

- 8.2.3. >3MP

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa CMOS Image Sensor for Automotive Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. Commercial Car

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 1-2MP

- 9.2.2. 2-3MP

- 9.2.3. >3MP

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific CMOS Image Sensor for Automotive Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. Commercial Car

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 1-2MP

- 10.2.2. 2-3MP

- 10.2.3. >3MP

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Onsemi

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 OMNIVISION

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 STMicroelectronics

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Ams Osram

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Sony

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Himax Technologies

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Samsung

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 PIXELPLUS

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Toshiba

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Onsemi

List of Figures

- Figure 1: Global CMOS Image Sensor for Automotive Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global CMOS Image Sensor for Automotive Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America CMOS Image Sensor for Automotive Revenue (billion), by Application 2025 & 2033

- Figure 4: North America CMOS Image Sensor for Automotive Volume (K), by Application 2025 & 2033

- Figure 5: North America CMOS Image Sensor for Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America CMOS Image Sensor for Automotive Volume Share (%), by Application 2025 & 2033

- Figure 7: North America CMOS Image Sensor for Automotive Revenue (billion), by Types 2025 & 2033

- Figure 8: North America CMOS Image Sensor for Automotive Volume (K), by Types 2025 & 2033

- Figure 9: North America CMOS Image Sensor for Automotive Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America CMOS Image Sensor for Automotive Volume Share (%), by Types 2025 & 2033

- Figure 11: North America CMOS Image Sensor for Automotive Revenue (billion), by Country 2025 & 2033

- Figure 12: North America CMOS Image Sensor for Automotive Volume (K), by Country 2025 & 2033

- Figure 13: North America CMOS Image Sensor for Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America CMOS Image Sensor for Automotive Volume Share (%), by Country 2025 & 2033

- Figure 15: South America CMOS Image Sensor for Automotive Revenue (billion), by Application 2025 & 2033

- Figure 16: South America CMOS Image Sensor for Automotive Volume (K), by Application 2025 & 2033

- Figure 17: South America CMOS Image Sensor for Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America CMOS Image Sensor for Automotive Volume Share (%), by Application 2025 & 2033

- Figure 19: South America CMOS Image Sensor for Automotive Revenue (billion), by Types 2025 & 2033

- Figure 20: South America CMOS Image Sensor for Automotive Volume (K), by Types 2025 & 2033

- Figure 21: South America CMOS Image Sensor for Automotive Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America CMOS Image Sensor for Automotive Volume Share (%), by Types 2025 & 2033

- Figure 23: South America CMOS Image Sensor for Automotive Revenue (billion), by Country 2025 & 2033

- Figure 24: South America CMOS Image Sensor for Automotive Volume (K), by Country 2025 & 2033

- Figure 25: South America CMOS Image Sensor for Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America CMOS Image Sensor for Automotive Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe CMOS Image Sensor for Automotive Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe CMOS Image Sensor for Automotive Volume (K), by Application 2025 & 2033

- Figure 29: Europe CMOS Image Sensor for Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe CMOS Image Sensor for Automotive Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe CMOS Image Sensor for Automotive Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe CMOS Image Sensor for Automotive Volume (K), by Types 2025 & 2033

- Figure 33: Europe CMOS Image Sensor for Automotive Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe CMOS Image Sensor for Automotive Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe CMOS Image Sensor for Automotive Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe CMOS Image Sensor for Automotive Volume (K), by Country 2025 & 2033

- Figure 37: Europe CMOS Image Sensor for Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe CMOS Image Sensor for Automotive Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa CMOS Image Sensor for Automotive Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa CMOS Image Sensor for Automotive Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa CMOS Image Sensor for Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa CMOS Image Sensor for Automotive Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa CMOS Image Sensor for Automotive Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa CMOS Image Sensor for Automotive Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa CMOS Image Sensor for Automotive Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa CMOS Image Sensor for Automotive Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa CMOS Image Sensor for Automotive Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa CMOS Image Sensor for Automotive Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa CMOS Image Sensor for Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa CMOS Image Sensor for Automotive Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific CMOS Image Sensor for Automotive Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific CMOS Image Sensor for Automotive Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific CMOS Image Sensor for Automotive Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific CMOS Image Sensor for Automotive Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific CMOS Image Sensor for Automotive Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific CMOS Image Sensor for Automotive Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific CMOS Image Sensor for Automotive Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific CMOS Image Sensor for Automotive Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific CMOS Image Sensor for Automotive Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific CMOS Image Sensor for Automotive Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific CMOS Image Sensor for Automotive Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific CMOS Image Sensor for Automotive Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global CMOS Image Sensor for Automotive Volume K Forecast, by Application 2020 & 2033

- Table 3: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global CMOS Image Sensor for Automotive Volume K Forecast, by Types 2020 & 2033

- Table 5: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global CMOS Image Sensor for Automotive Volume K Forecast, by Region 2020 & 2033

- Table 7: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global CMOS Image Sensor for Automotive Volume K Forecast, by Application 2020 & 2033

- Table 9: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global CMOS Image Sensor for Automotive Volume K Forecast, by Types 2020 & 2033

- Table 11: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global CMOS Image Sensor for Automotive Volume K Forecast, by Country 2020 & 2033

- Table 13: United States CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global CMOS Image Sensor for Automotive Volume K Forecast, by Application 2020 & 2033

- Table 21: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global CMOS Image Sensor for Automotive Volume K Forecast, by Types 2020 & 2033

- Table 23: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global CMOS Image Sensor for Automotive Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global CMOS Image Sensor for Automotive Volume K Forecast, by Application 2020 & 2033

- Table 33: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global CMOS Image Sensor for Automotive Volume K Forecast, by Types 2020 & 2033

- Table 35: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global CMOS Image Sensor for Automotive Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global CMOS Image Sensor for Automotive Volume K Forecast, by Application 2020 & 2033

- Table 57: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global CMOS Image Sensor for Automotive Volume K Forecast, by Types 2020 & 2033

- Table 59: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global CMOS Image Sensor for Automotive Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global CMOS Image Sensor for Automotive Volume K Forecast, by Application 2020 & 2033

- Table 75: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global CMOS Image Sensor for Automotive Volume K Forecast, by Types 2020 & 2033

- Table 77: Global CMOS Image Sensor for Automotive Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global CMOS Image Sensor for Automotive Volume K Forecast, by Country 2020 & 2033

- Table 79: China CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific CMOS Image Sensor for Automotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific CMOS Image Sensor for Automotive Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the CMOS Image Sensor for Automotive?

The projected CAGR is approximately 7.73%.

2. Which companies are prominent players in the CMOS Image Sensor for Automotive?

Key companies in the market include Onsemi, OMNIVISION, STMicroelectronics, Ams Osram, Sony, Himax Technologies, Samsung, PIXELPLUS, Toshiba.

3. What are the main segments of the CMOS Image Sensor for Automotive?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.458 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "CMOS Image Sensor for Automotive," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the CMOS Image Sensor for Automotive report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the CMOS Image Sensor for Automotive?

To stay informed about further developments, trends, and reports in the CMOS Image Sensor for Automotive, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence