Key Insights

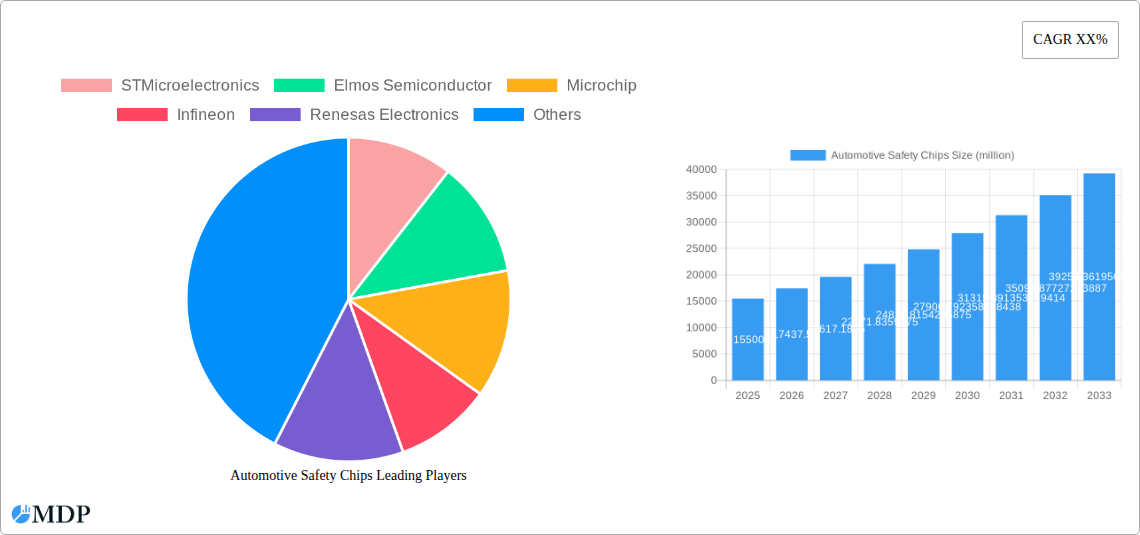

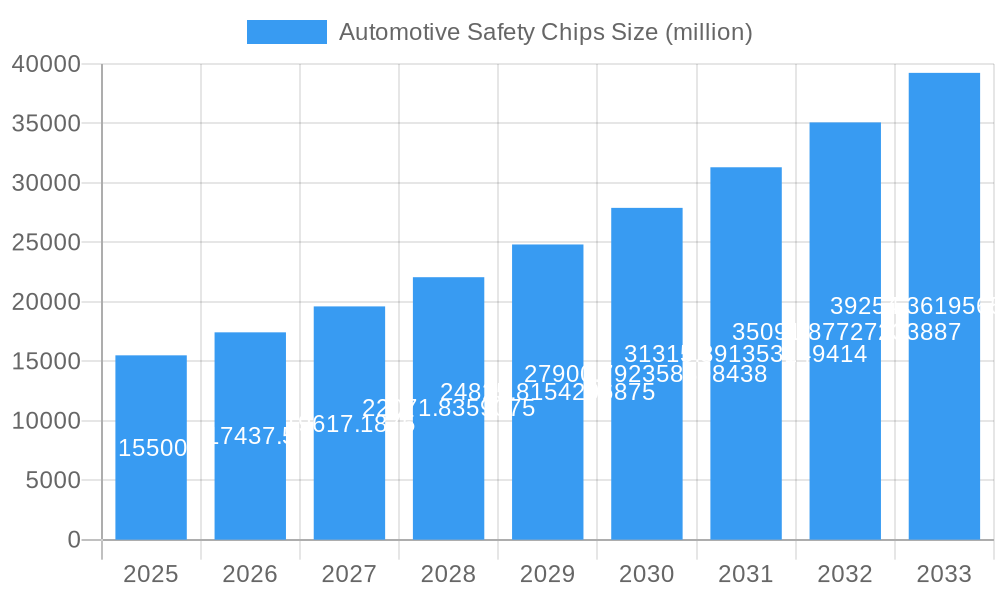

The global Automotive Safety Chips market is projected for substantial growth, expected to reach $63.1 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 14.9% through 2033. This expansion is driven by increasing demand for advanced vehicle safety features, stringent regulatory mandates, heightened consumer safety awareness, and rapid automotive technology advancements. The integration of critical systems such as Electronic Stability Control (ESC), Anti-lock Braking Systems (ABS), and advanced airbag deployment necessitates specialized safety integrated circuits (ICs). The proliferation of autonomous driving, reliant on redundant and highly reliable safety electronics, will further accelerate market growth. Evolving vehicle architectures and a growing focus on automotive cybersecurity will also boost demand for high-performance safety chips.

Automotive Safety Chips Market Size (In Billion)

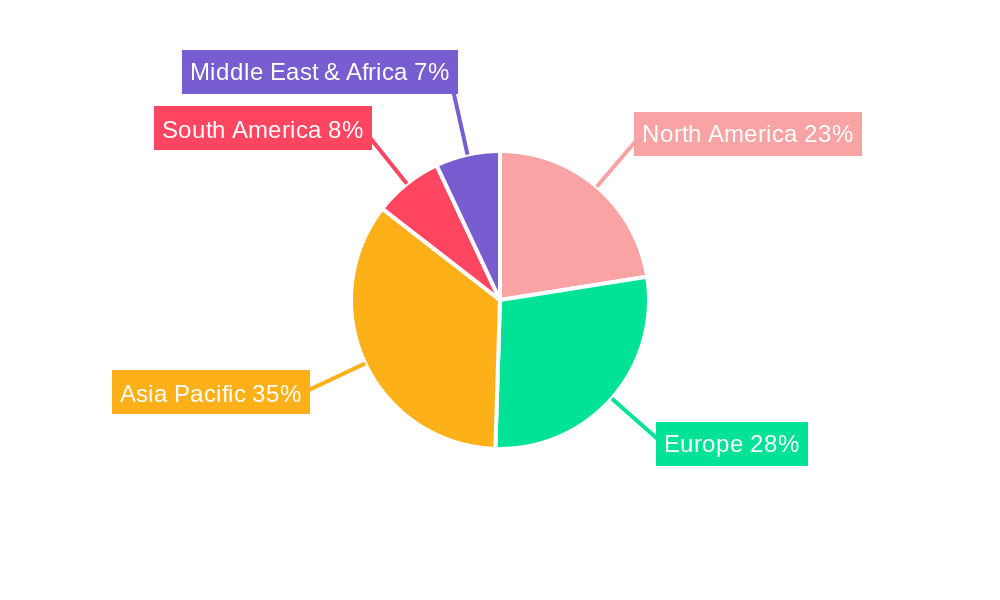

Market segmentation highlights dominance in commercial and passenger vehicle applications. Airbag ICs and Braking ICs hold significant shares due to their essential safety functions, while Steering ICs are gaining prominence with the rise of electric power steering. Leading industry players including STMicroelectronics, Infineon, NXP Semiconductors, and Texas Instruments are investing heavily in R&D to meet evolving market demands. Geographically, the Asia Pacific, particularly China, is a key growth driver owing to its vast automotive production and adoption of safety technologies. North America and Europe remain critical, mature markets driven by established safety standards and consumer preference for advanced safety features. While high development costs and complex supply chains may present challenges, the imperative for enhanced vehicular safety is expected to outweigh these constraints.

Automotive Safety Chips Company Market Share

Automotive Safety Chips Market: Navigating a Crucial Sector for Autonomous and Connected Vehicles

This comprehensive report, "Automotive Safety Chips Market: Dynamics, Trends, and Future Outlook (2019–2033)", offers an in-depth analysis of the vital automotive safety chips industry. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, this report delves into the intricate market dynamics, emerging trends, leading segments, and strategic imperatives shaping this critical sector. With a forecast period extending to 2033, it provides actionable insights for stakeholders seeking to capitalize on the burgeoning demand for advanced automotive safety solutions.

Automotive Safety Chips Market Dynamics & Concentration

The automotive safety chips market is characterized by a moderate to high concentration, with a few key players holding significant market share. Innovation is primarily driven by the relentless pursuit of enhanced vehicle safety, adherence to stringent global regulations, and the integration of advanced driver-assistance systems (ADAS) and autonomous driving technologies. Regulatory frameworks, such as Euro NCAP, NHTSA's NCAP programs, and forthcoming UNECE regulations, are pivotal in mandating the adoption of sophisticated safety features, thereby propelling demand for specialized chips. The threat of product substitutes is relatively low for core safety functionalities like airbag deployment or braking control, as these are highly specialized and critical components. However, in areas like ADAS, software-defined solutions and integrated platforms can be seen as evolving forms of substitution. End-user trends are overwhelmingly focused on achieving zero-fatality goals, improving occupant protection, and enhancing the overall driving experience through intelligent safety systems. Mergers and acquisitions (M&A) activity, while not excessively high, plays a role in consolidating market positions and acquiring specialized technological capabilities. For instance, recent M&A deals have seen larger semiconductor manufacturers acquire niche players in areas like sensor fusion or AI processing for safety applications. The market is projected to witness a compound annual growth rate (CAGR) of approximately 15%, with the total market value expected to reach xx million by 2025 and grow substantially by 2033. M&A deal counts have been steady, averaging 5-7 significant transactions annually over the historical period.

Automotive Safety Chips Industry Trends & Analysis

The automotive safety chips industry is experiencing robust growth, fueled by a confluence of technological advancements, evolving consumer expectations, and stringent regulatory mandates. The increasing sophistication of vehicles, transitioning towards connected and autonomous functionalities, necessitates a dramatic increase in the computational power and specialized processing capabilities offered by safety chips. Market growth drivers are predominantly linked to the escalating demand for ADAS features such as adaptive cruise control, lane-keeping assist, automatic emergency braking, and blind-spot detection. The global push towards reducing road fatalities is a paramount driver, with governments worldwide implementing and strengthening safety regulations, mandating the inclusion of advanced safety systems that rely heavily on these chips. Technological disruptions are constant, with advancements in AI, machine learning, and sensor fusion technologies requiring more powerful and efficient safety semiconductors. The development of ISO 26262 functional safety standards continues to shape product development, ensuring the reliability and integrity of safety-critical electronic components. Consumer preferences are increasingly leaning towards vehicles equipped with comprehensive safety suites, as evidenced by consumer surveys indicating a willingness to pay a premium for enhanced safety features. This trend is further amplified by the growing adoption of electric vehicles (EVs), which often come equipped with advanced safety systems as a standard offering. Competitive dynamics are intensifying, with established semiconductor giants competing alongside emerging players specializing in niche safety technologies. Strategic partnerships and collaborations are becoming common as companies aim to leverage each other's expertise in areas like software development, AI algorithms, and sensor integration. The market penetration of advanced safety features, once confined to premium segments, is rapidly expanding into mass-market vehicles, further accelerating the demand for automotive safety chips. The total market size, estimated at over xx million in the base year of 2025, is projected to witness a significant upward trajectory. The CAGR for the forecast period is estimated to be around 15%, indicating a sustained and rapid expansion. This growth is underpinned by the continuous introduction of new vehicle models incorporating higher levels of safety automation.

Leading Markets & Segments in Automotive Safety Chips

The automotive safety chips market is experiencing dominant growth across several key regions and segments, driven by a combination of economic policies, infrastructure development, and evolving consumer preferences. Passenger Vehicles represent the largest application segment, accounting for over 70% of the global market share. This dominance is fueled by several factors:

- Economic Policies and Consumer Demand: In developed economies, favorable economic conditions and a strong consumer demand for premium features drive the adoption of advanced safety systems in passenger cars. Government incentives and safety rating programs further encourage manufacturers to integrate these technologies.

- Technological Integration: Passenger vehicles are at the forefront of integrating sophisticated ADAS and autonomous driving features, directly translating to a higher demand for specialized safety chips.

- Global Safety Regulations: Regulations like Euro NCAP and NHTSA mandates are increasingly pushing for higher safety standards in passenger cars, making safety chips an essential component.

Within the types of automotive safety chips, the Braking IC segment holds a substantial market share, estimated at around 30% of the total market. This is due to:

- Critical Safety Function: Reliable and responsive braking systems are fundamental to vehicle safety, making braking ICs indispensable.

- Advancements in Electronic Braking Systems (EBS): The transition from traditional hydraulic braking to advanced EBS, including Anti-lock Braking Systems (ABS), Electronic Stability Control (ESC), and regenerative braking in EVs, significantly increases the complexity and demand for sophisticated braking ICs.

- ADAS Integration: Braking ICs play a crucial role in ADAS functions like automatic emergency braking and adaptive cruise control, further boosting their market penetration.

The Airbag IC segment also represents a significant portion of the market, driven by mandatory safety requirements and the increasing number of airbags in modern vehicles, including side curtain and knee airbags.

- Mandatory Safety Feature: Airbags are a universally mandated safety feature, ensuring a consistent demand for airbag control ICs.

- Advanced Deployment Systems: Modern airbag systems utilize sophisticated sensors and control units, requiring advanced ICs for precise and rapid deployment.

The Commercial Vehicles segment, while currently smaller than passenger vehicles, is experiencing a rapid growth trajectory, projected to capture a larger market share in the coming years.

- Fleet Safety Initiatives: Commercial fleet operators are increasingly investing in safety technologies to reduce accidents, improve operational efficiency, and mitigate insurance costs.

- Logistics and Autonomous Trucking: The push towards autonomous trucking and advanced driver assistance systems in long-haul transportation creates a significant demand for robust and high-performance safety chips.

- Regulatory Focus on Commercial Safety: Governments are also focusing on enhancing safety standards for commercial vehicles, further driving chip adoption.

The Steering IC segment is gaining momentum with the advent of advanced power steering systems and active steering technologies that contribute to vehicle stability and maneuverability.

Automotive Safety Chips Product Developments

Recent product developments in automotive safety chips are centered around enhanced processing power, lower power consumption, and advanced functionalities crucial for sophisticated ADAS and autonomous driving. Innovations include the introduction of specialized processors capable of real-time sensor fusion, AI inference for object recognition and prediction, and robust functional safety features adhering to ISO 26262 ASIL D standards. These advancements enable faster decision-making for critical safety actions like emergency braking and steering intervention. The integration of multiple safety functions onto single chips (SoCs) is a key trend, reducing bill of materials and complexity. Competitive advantages are being carved out through proprietary algorithms, secure boot mechanisms, and over-the-air (OTA) update capabilities for safety software. The market fit for these developments is directly aligned with the growing demand for Level 2+ and Level 3 autonomous driving capabilities, as well as the continuous improvement of existing safety features.

Key Drivers of Automotive Safety Chips Growth

The automotive safety chips market is propelled by several interconnected drivers:

- Stringent Global Safety Regulations: Mandates from bodies like NHTSA and Euro NCAP are increasingly requiring advanced safety features, directly boosting demand for sophisticated safety chips.

- Advancements in ADAS and Autonomous Driving: The continuous development and adoption of technologies like automatic emergency braking, lane keeping assist, and adaptive cruise control necessitate higher performance safety semiconductors.

- Consumer Demand for Enhanced Safety: Growing consumer awareness and preference for vehicles with comprehensive safety suites are driving manufacturers to equip vehicles with more advanced safety systems.

- Electrification of Vehicles: The integration of advanced battery management and power control systems in EVs often goes hand-in-hand with advanced safety features, creating a synergistic growth effect.

- Technological Innovation: Continuous breakthroughs in AI, machine learning, and sensor technology are enabling more capable and effective safety systems, requiring innovative chip solutions.

Challenges in the Automotive Safety Chips Market

Despite the robust growth, the automotive safety chips market faces several challenges:

- Regulatory Compliance Complexity: Adhering to diverse and evolving global safety standards (e.g., ISO 26262) requires significant investment in R&D and rigorous testing, adding to development costs and timelines.

- Supply Chain Disruptions: The automotive industry, including chip manufacturing, is susceptible to global supply chain volatilities, leading to potential shortages and price fluctuations. This can impact production volumes and market availability.

- Intensifying Competition and Price Pressure: The presence of numerous established and emerging players leads to fierce competition, which can exert downward pressure on profit margins, especially for high-volume, less differentiated components.

- Rapid Technological Obsolescence: The fast pace of technological advancement in areas like AI and ADAS can lead to the rapid obsolescence of existing chip designs, necessitating continuous investment in next-generation products.

- High Development Costs: Developing highly reliable and safety-certified automotive chips requires substantial investment in R&D, testing, and validation, posing a barrier for smaller players.

Emerging Opportunities in Automotive Safety Chips

The automotive safety chips market is ripe with emerging opportunities driven by technological breakthroughs and evolving market dynamics:

- Expansion of ADAS and Autonomous Driving Levels: The ongoing development and eventual widespread adoption of higher levels of autonomous driving (Level 4 and 5) will unlock massive demand for significantly more powerful and complex safety chip solutions, including those for AI processing and sensor fusion.

- Vehicle-to-Everything (V2X) Communication Integration: As V2X communication becomes more prevalent, safety chips will need to incorporate advanced connectivity and processing capabilities to enable inter-vehicle and vehicle-to-infrastructure safety applications, such as collision avoidance and traffic management.

- Cybersecurity for Automotive Systems: With increasing connectivity, robust in-chip cybersecurity features are becoming paramount to protect safety-critical systems from malicious attacks. This presents an opportunity for specialized security chip solutions.

- Growth in Emerging Markets: As developing economies witness an increase in vehicle ownership and a growing emphasis on safety, these regions present significant untapped market potential for automotive safety chips.

- Customization and Specialization: The increasing complexity of automotive platforms creates opportunities for chip manufacturers to offer highly specialized and customized safety solutions for specific vehicle architectures or ADAS functionalities.

Leading Players in the Automotive Safety Chips Sector

- STMicroelectronics

- Elmos Semiconductor

- Microchip

- Infineon

- Renesas Electronics

- NXP Semiconductors

- Texas Instruments

- Tongxin Micro

- Huada Semiconductor

- Black Sesame

- SemiDrive

- Thinktech

- iStarChip Semiconductor

Key Milestones in Automotive Safety Chips Industry

- 2019: Increased regulatory pressure for AEB systems adoption globally.

- 2020: Significant advancements in AI-powered sensor fusion for ADAS.

- 2021: Major automotive OEMs announce aggressive timelines for autonomous driving development.

- 2022: Introduction of next-generation braking ICs with enhanced control and diagnostics.

- 2023: Growing focus on functional safety (ISO 26262) compliance in chip design.

- 2024: Launch of advanced airbag control ICs supporting a wider range of sensor inputs.

- 2025 (Estimated): Increased integration of V2X capabilities into safety chipsets.

- 2026-2028: Anticipated rise in adoption of Level 3 autonomous driving features.

- 2029-2032: Potential commercialization of Level 4 autonomous driving solutions, demanding highly sophisticated safety silicon.

Strategic Outlook for Automotive Safety Chips Market

The strategic outlook for the automotive safety chips market is exceptionally strong, driven by the unstoppable march towards safer and more autonomous vehicles. Key growth accelerators include the continuous evolution of ADAS functionalities into higher automation levels, the increasing integration of V2X communication for enhanced situational awareness, and the growing importance of robust in-chip cybersecurity. Manufacturers that can offer highly integrated, power-efficient, and functionally safe solutions, coupled with strong software support and AI capabilities, will be best positioned to capitalize on this expanding market. Strategic opportunities lie in forging deeper partnerships with OEMs, investing in cutting-edge research and development for next-generation processing and AI inference, and expanding geographical reach into high-growth emerging markets. The future of automotive safety is intrinsically linked to the advancement of these critical semiconductor components.

Automotive Safety Chips Segmentation

-

1. Application

- 1.1. Commercial Vehicles

- 1.2. Passenger Vehicles

-

2. Types

- 2.1. Airbag IC

- 2.2. Braking IC

- 2.3. Steering IC

- 2.4. Others

Automotive Safety Chips Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Safety Chips Regional Market Share

Geographic Coverage of Automotive Safety Chips

Automotive Safety Chips REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Safety Chips Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Vehicles

- 5.1.2. Passenger Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Airbag IC

- 5.2.2. Braking IC

- 5.2.3. Steering IC

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Safety Chips Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Vehicles

- 6.1.2. Passenger Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Airbag IC

- 6.2.2. Braking IC

- 6.2.3. Steering IC

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Safety Chips Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Vehicles

- 7.1.2. Passenger Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Airbag IC

- 7.2.2. Braking IC

- 7.2.3. Steering IC

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Safety Chips Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Vehicles

- 8.1.2. Passenger Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Airbag IC

- 8.2.2. Braking IC

- 8.2.3. Steering IC

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Safety Chips Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Vehicles

- 9.1.2. Passenger Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Airbag IC

- 9.2.2. Braking IC

- 9.2.3. Steering IC

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Safety Chips Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Vehicles

- 10.1.2. Passenger Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Airbag IC

- 10.2.2. Braking IC

- 10.2.3. Steering IC

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 STMicroelectronics

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Elmos Semiconductor

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Microchip

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Infineon

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Renesas Electronics

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 NXP Semiconductors

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Texas Instruments

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Tongxin Micro

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Huada Semiconductor

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Black Sesame

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 SemiDrive

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Thinktech

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 iStarChip Semiconductor

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 STMicroelectronics

List of Figures

- Figure 1: Global Automotive Safety Chips Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive Safety Chips Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive Safety Chips Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Safety Chips Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Automotive Safety Chips Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Safety Chips Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive Safety Chips Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Safety Chips Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive Safety Chips Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Safety Chips Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Automotive Safety Chips Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Safety Chips Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive Safety Chips Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Safety Chips Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive Safety Chips Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Safety Chips Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Automotive Safety Chips Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Safety Chips Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive Safety Chips Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Safety Chips Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Safety Chips Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Safety Chips Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Safety Chips Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Safety Chips Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Safety Chips Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Safety Chips Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Safety Chips Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Safety Chips Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Safety Chips Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Safety Chips Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Safety Chips Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Safety Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Safety Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Safety Chips Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Safety Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Safety Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Safety Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Safety Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Safety Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Safety Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Safety Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Safety Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Safety Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Safety Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Safety Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Safety Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Safety Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Safety Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Safety Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Safety Chips Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Safety Chips?

The projected CAGR is approximately 14.9%.

2. Which companies are prominent players in the Automotive Safety Chips?

Key companies in the market include STMicroelectronics, Elmos Semiconductor, Microchip, Infineon, Renesas Electronics, NXP Semiconductors, Texas Instruments, Tongxin Micro, Huada Semiconductor, Black Sesame, SemiDrive, Thinktech, iStarChip Semiconductor.

3. What are the main segments of the Automotive Safety Chips?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 63.1 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Safety Chips," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Safety Chips report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Safety Chips?

To stay informed about further developments, trends, and reports in the Automotive Safety Chips, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence