Key Insights

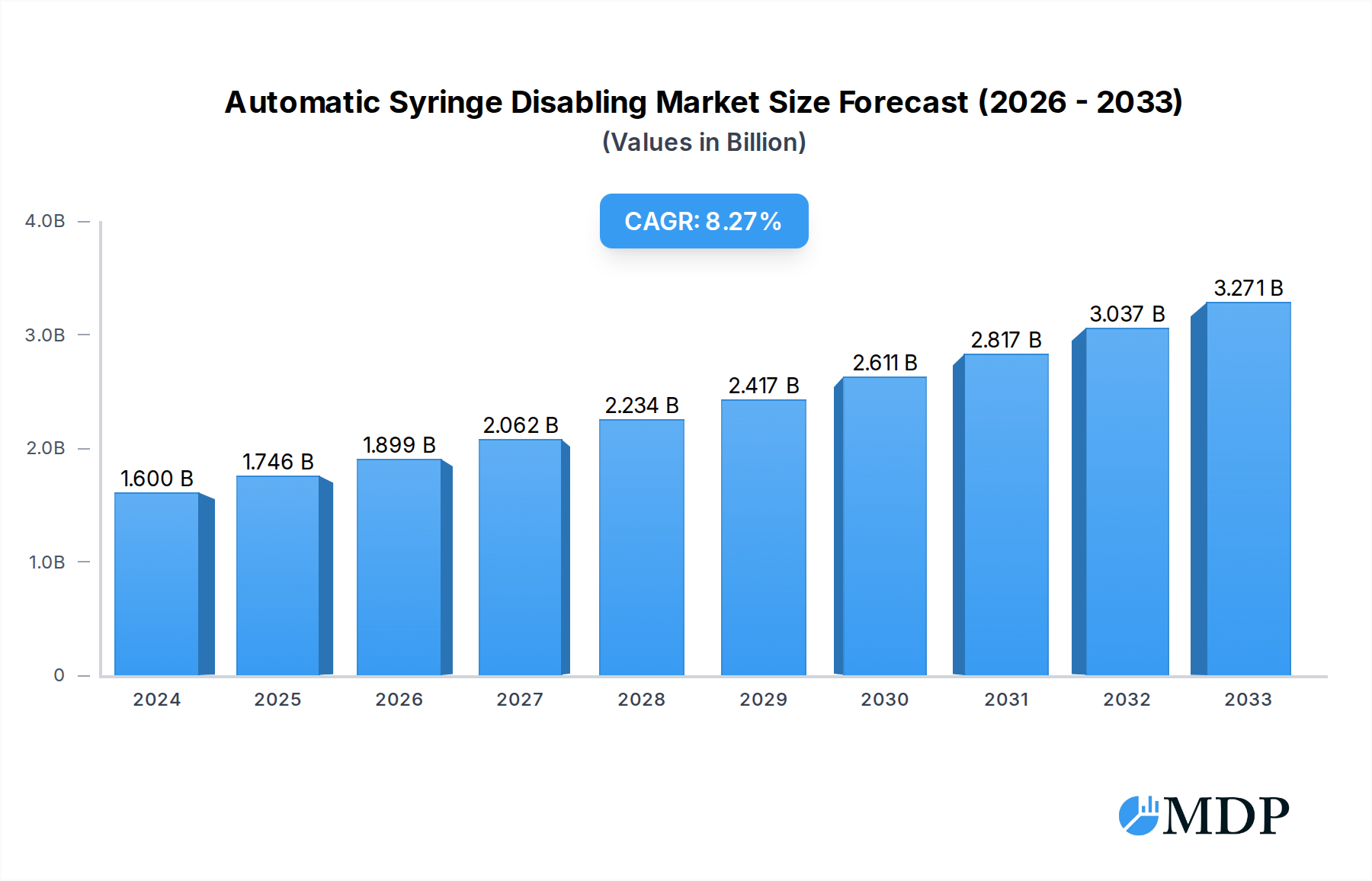

The Automatic Syringe Disabling market is poised for significant expansion, driven by an increasing global emphasis on patient safety and the prevention of needlestick injuries. With an estimated market size of $1.6 billion in 2024, this sector is projected to experience a robust Compound Annual Growth Rate (CAGR) of 9.1% through 2033. This upward trajectory is fueled by stringent healthcare regulations mandating safer medical practices, particularly in hospital and clinic settings, which represent the primary application segments. The growing adoption of advanced healthcare technologies and the rising prevalence of chronic diseases necessitating regular injections further bolster market demand. Moreover, the increasing awareness among healthcare professionals and institutions regarding the severe consequences of improperly disposed syringes, including the transmission of infectious diseases, acts as a powerful catalyst for the adoption of automatic disabling devices.

Automatic Syringe Disabling Market Size (In Billion)

The market's growth is further supported by continuous innovation in syringe designs and disabling mechanisms, leading to more efficient and user-friendly products. The demand spans various types of syringes, including 1ML, 2ML, 3ML, 5ML, and 10ML, catering to diverse medical needs. While the market is characterized by strong growth, potential restraints include the initial cost of implementing these safety devices in resource-limited healthcare facilities and the need for comprehensive training for healthcare personnel. However, the long-term benefits of reduced infection rates, lower healthcare-associated costs, and enhanced occupational safety are expected to outweigh these challenges. Key players are actively engaged in research and development to introduce next-generation disabling technologies, ensuring sustained market development and meeting the evolving demands of the global healthcare industry.

Automatic Syringe Disabling Company Market Share

This in-depth report provides an exhaustive analysis of the global Automatic Syringe Disabling market, a critical segment within medical device technology focused on preventing needlestick injuries and ensuring safe medical practices. Covering the historical period of 2019–2024, base year 2025, estimated year 2025, and a comprehensive forecast period from 2025–2033, this research offers unparalleled insights into market dynamics, industry trends, leading segments, product developments, growth drivers, challenges, and emerging opportunities. Stakeholders can leverage this report to understand the competitive landscape, identify strategic growth avenues, and make informed decisions in this rapidly evolving sector. The market is projected to reach significant valuations, driven by increasing healthcare expenditures, stringent safety regulations, and a growing emphasis on healthcare worker safety. Key companies such as BD, Terumo, and Vogt Medical are at the forefront of innovation and market penetration.

Automatic Syringe Disabling Market Dynamics & Concentration

The global Automatic Syringe Disabling market exhibits a moderate to high level of concentration, with a few key players holding substantial market share. This concentration is driven by the significant R&D investment required for product development and the stringent regulatory approvals necessary for market entry. Innovation is primarily fueled by advancements in materials science, miniaturization of technology, and the integration of smart features for enhanced usability and safety. Regulatory frameworks, particularly in developed economies, are increasingly mandating the adoption of safety-engineered sharps disposal devices, acting as a significant market driver. Product substitutes, while present in the form of manual disabling methods, are gradually being phased out due to their inherent risks. End-user trends strongly favor devices that offer superior protection against needlestick injuries, ease of use, and compatibility with existing medical workflows. Merger and acquisition (M&A) activities are expected to play a crucial role in consolidating the market further, with an estimated XX M&A deals anticipated over the forecast period. Key players like BD and Terumo are actively engaged in strategic acquisitions to expand their product portfolios and geographical reach. The market share of leading players is estimated to be around XX billion in the base year 2025.

Automatic Syringe Disabling Industry Trends & Analysis

The Automatic Syringe Disabling industry is experiencing robust growth, underpinned by a confluence of potent market growth drivers. A primary catalyst is the escalating global awareness and regulatory imperative surrounding the prevention of needlestick injuries (NSIs). NSIs pose a significant occupational hazard for healthcare professionals, leading to the transmission of serious infections such as HIV, Hepatitis B, and Hepatitis C. Consequently, governments worldwide are enacting and enforcing legislation that mandates the use of safety-engineered medical devices, including automatic syringe disabling mechanisms. The global market penetration of these devices is projected to witness a significant surge from XX% in the historical period to XX% by the end of the forecast period.

Technological disruptions are continuously reshaping the market landscape. Innovations in materials science are leading to lighter, more durable, and cost-effective disabling mechanisms. Furthermore, the integration of smart technologies, such as passive safety features that activate automatically upon use and active safety features that require deliberate user engagement, is enhancing the overall safety profile of syringes. The development of single-use syringes with integrated disabling features is a notable trend, reducing the risk of device reuse and accidental sharps exposure.

Consumer preferences are increasingly leaning towards user-friendly and intuitive designs that minimize the learning curve for healthcare professionals. The demand for syringes that offer a seamless integration into existing clinical practices without compromising efficiency is paramount. This includes features like one-handed operation and clear visual indicators of activation.

The competitive dynamics within the Automatic Syringe Disabling market are characterized by intense R&D efforts and strategic collaborations. Companies are investing heavily in developing next-generation safety syringes that offer enhanced protection and address specific clinical needs. The market CAGR is estimated to be XX% for the forecast period. The market is projected to reach a valuation of approximately $XX billion by 2033.

Leading Markets & Segments in Automatic Syringe Disabling

The Hospital application segment stands as the dominant force in the global Automatic Syringe Disabling market. This leadership is attributed to several interconnected factors. Firstly, hospitals are the primary sites for complex medical procedures, surgeries, and the administration of a vast array of injectable medications, leading to a consistently high volume of syringe usage. The inherent risk of needlestick injuries is amplified in busy hospital environments, where the pace of work can sometimes compromise safety protocols. Consequently, hospitals are mandated to adhere to the strictest safety regulations and are early adopters of advanced safety-engineered medical devices. The financial capacity of hospitals, coupled with their commitment to patient and staff safety, makes them a significant market for automatic syringe disabling technologies.

The Clinic segment represents another substantial and growing market for automatic syringe disabling devices. As healthcare systems increasingly shift towards outpatient care and specialized treatment centers, clinics are witnessing a rise in the number of minor surgical procedures, diagnostic tests, and chronic disease management programs that involve injections. The need for safe disposal of sharps in these settings is equally critical, driving the adoption of these devices.

The 1ML and 5ML syringe types are expected to capture the largest market share within their respective categories. The widespread use of 1ML syringes for vaccinations, insulin delivery, and precise medication dosing in pediatric and neonatal care, as well as for various diagnostic tests, makes them a high-volume product. Similarly, 5ML syringes are extensively used for a broad range of therapeutic injections, fluid administration, and aspiration procedures across diverse medical specialties. The demand for these specific volumes is driven by their ubiquitous application in routine medical practice.

The economic policies in developed nations, characterized by robust healthcare spending and proactive occupational safety regulations, significantly bolster the demand for automatic syringe disabling devices in hospitals and clinics. Furthermore, the infrastructure within these healthcare settings, encompassing sterile environments and established waste disposal protocols, facilitates the seamless integration and effective utilization of these safety syringes. The growing emphasis on preventive healthcare and occupational health and safety standards across the globe further solidifies the dominance of the hospital segment and the demand for commonly used syringe types.

Automatic Syringe Disabling Product Developments

Product developments in the Automatic Syringe Disabling market are characterized by a relentless focus on enhancing safety, usability, and affordability. Innovations include the introduction of passive safety mechanisms that automatically retract the needle post-injection, minimizing user intervention and reducing the risk of accidental exposure. Active safety features, requiring a deliberate user action to engage the disabling mechanism, offer an additional layer of control and customization. Furthermore, advancements in materials science are leading to the development of syringes with improved breakage resistance and lighter construction. The integration of color-coded designs for easier identification and the development of dual-purpose syringes that can be used for both injection and blood collection are also emerging trends, offering enhanced convenience and efficiency in clinical settings. These developments aim to provide healthcare professionals with reliable and intuitive solutions for preventing needlestick injuries and ensuring a safer healthcare environment.

Key Drivers of Automatic Syringe Disabling Growth

The Automatic Syringe Disabling market is propelled by several significant growth drivers. Stringent regulatory mandates globally, enforcing the use of safety-engineered sharps disposal devices to prevent needlestick injuries, are a primary accelerator. Increasing healthcare expenditure, particularly in emerging economies, translates to greater access to advanced medical devices and a heightened focus on patient and healthcare worker safety. Growing awareness of occupational hazards associated with healthcare professionals, leading to a higher demand for protective equipment and safer medical practices, is another key factor. Technological advancements in syringe design, incorporating passive and active disabling features, are enhancing product efficacy and adoption. The rising incidence of infectious diseases transmitted through needlestick injuries further underscores the critical need for these safety devices.

Challenges in the Automatic Syringe Disabling Market

Despite its promising growth, the Automatic Syringe Disabling market faces several challenges. High initial manufacturing costs associated with advanced safety features can lead to higher product prices, potentially limiting adoption in cost-sensitive regions. Inconsistent regulatory enforcement across different countries can create market fragmentation and hinder widespread adoption. User resistance to change and the need for adequate training on new safety mechanisms can also pose a barrier. Supply chain disruptions, particularly in the wake of global events, can impact the availability and affordability of raw materials and finished products. The availability of cheaper, non-safety-engineered alternatives in certain markets continues to pose a competitive threat.

Emerging Opportunities in Automatic Syringe Disabling

Emerging opportunities in the Automatic Syringe Disabling market are substantial and offer significant long-term growth potential. The increasing focus on preventive healthcare and public health initiatives worldwide creates a continuous demand for safety devices. Technological breakthroughs in miniaturization and the integration of smart features, such as embedded sensors for tracking usage and compliance, present avenues for product differentiation and value-added services. Strategic partnerships and collaborations between medical device manufacturers and healthcare institutions can facilitate wider market penetration and the development of customized solutions. Expansion into emerging markets with growing healthcare infrastructure and increasing awareness of occupational safety standards offers considerable untapped potential. Furthermore, the development of environmentally sustainable disabling mechanisms aligns with growing global environmental consciousness.

Leading Players in the Automatic Syringe Disabling Sector

- BD

- Terumo

- Vogt Medical

- SPM Medical

- Azur Medical

- HELMJECT

- Pricon

- SRS Meditech

- Alshifa Medical

- Hindustan Syringes & Medical Devices

- Hamilton

- Avapezeshk

Key Milestones in Automatic Syringe Disabling Industry

- 2019: Increased global regulatory scrutiny and implementation of stricter sharps safety laws in key markets.

- 2020: Launch of next-generation automatic disabling syringes with enhanced passive safety features by leading manufacturers.

- 2021: Growing emphasis on healthcare worker safety due to the COVID-19 pandemic, accelerating adoption of safety-engineered devices.

- 2022: Introduction of syringes with integrated smart technology for compliance tracking and data management.

- 2023: Significant investments in R&D for biodegradable and sustainable materials for syringe manufacturing.

- 2024: Expansion of automatic syringe disabling product portfolios into emerging economies through strategic partnerships.

Strategic Outlook for Automatic Syringe Disabling Market

The strategic outlook for the Automatic Syringe Disabling market remains exceptionally positive, driven by a confluence of escalating safety imperatives and continuous innovation. Future growth accelerators will stem from further regulatory tightening, compelling healthcare providers to invest in the safest available technologies. The market is poised for significant expansion through the development of advanced, user-centric designs that integrate seamlessly into clinical workflows. Opportunities lie in capturing market share in underserved regions and in offering value-added services beyond the core product. Collaborative efforts between industry players and regulatory bodies will be crucial in standardizing safety protocols and fostering a global culture of sharps safety. Strategic acquisitions and mergers are expected to consolidate the market further, creating stronger entities capable of driving larger-scale innovation and market penetration. The continued integration of digital technologies for enhanced traceability and data analytics will also shape the future competitive landscape.

Automatic Syringe Disabling Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Others

-

2. Types

- 2.1. 1ML

- 2.2. 2ML

- 2.3. 3ML

- 2.4. 5ML

- 2.5. 10ML

- 2.6. Others

Automatic Syringe Disabling Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

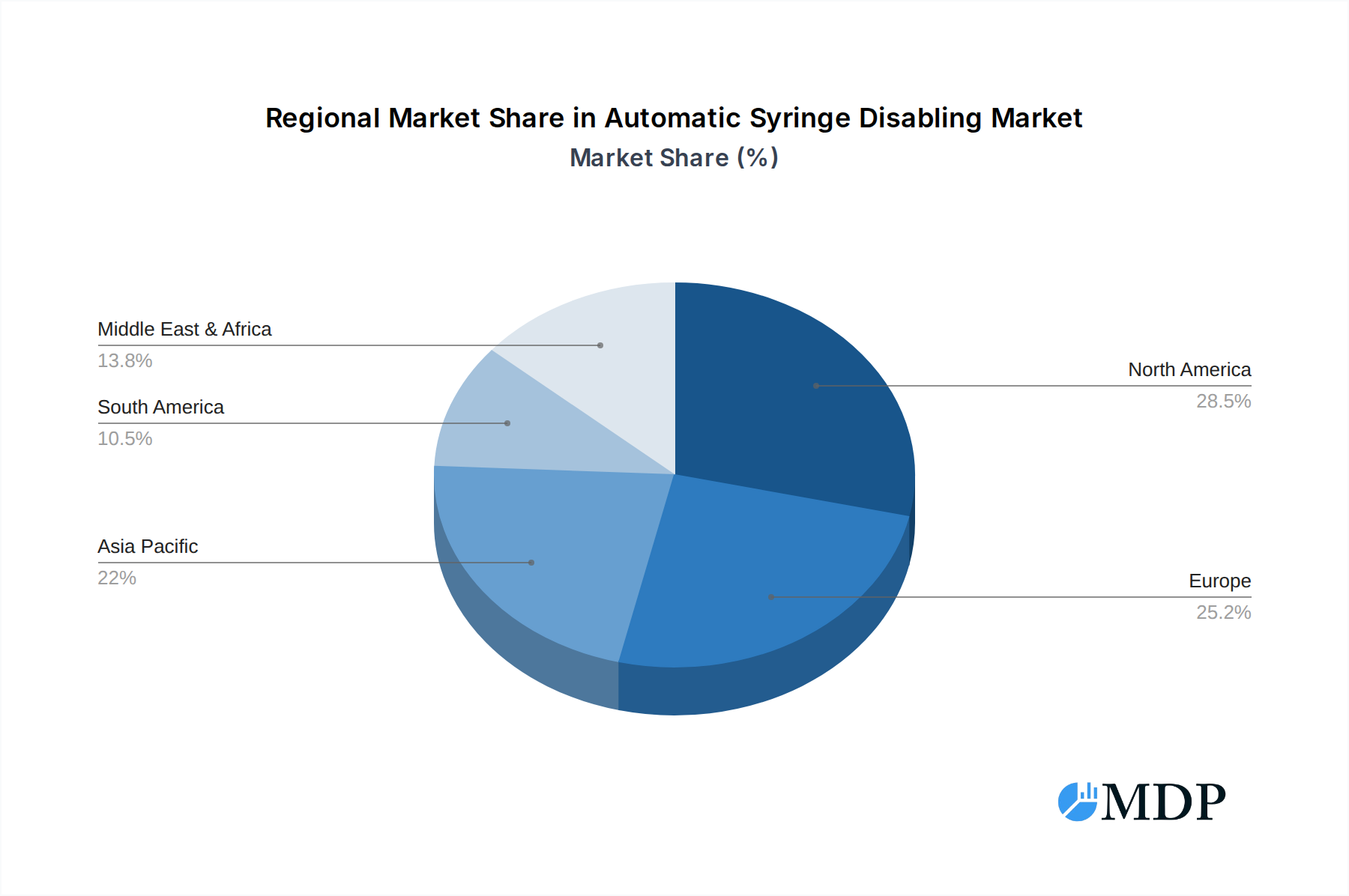

Automatic Syringe Disabling Regional Market Share

Geographic Coverage of Automatic Syringe Disabling

Automatic Syringe Disabling REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 1ML

- 5.2.2. 2ML

- 5.2.3. 3ML

- 5.2.4. 5ML

- 5.2.5. 10ML

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automatic Syringe Disabling Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 1ML

- 6.2.2. 2ML

- 6.2.3. 3ML

- 6.2.4. 5ML

- 6.2.5. 10ML

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automatic Syringe Disabling Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 1ML

- 7.2.2. 2ML

- 7.2.3. 3ML

- 7.2.4. 5ML

- 7.2.5. 10ML

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automatic Syringe Disabling Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 1ML

- 8.2.2. 2ML

- 8.2.3. 3ML

- 8.2.4. 5ML

- 8.2.5. 10ML

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automatic Syringe Disabling Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 1ML

- 9.2.2. 2ML

- 9.2.3. 3ML

- 9.2.4. 5ML

- 9.2.5. 10ML

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automatic Syringe Disabling Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 1ML

- 10.2.2. 2ML

- 10.2.3. 3ML

- 10.2.4. 5ML

- 10.2.5. 10ML

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automatic Syringe Disabling Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospital

- 11.1.2. Clinic

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. 1ML

- 11.2.2. 2ML

- 11.2.3. 3ML

- 11.2.4. 5ML

- 11.2.5. 10ML

- 11.2.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BD

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Terumo

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Vogt Medical

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 SPM Medical

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Azur Medical

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 HELMJECT

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Pricon

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 SRS Meditech

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Alshifa Medical

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Hindustan Syringes & Medical Devices

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Hamilton

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Avapezeshk

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 BD

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automatic Syringe Disabling Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Automatic Syringe Disabling Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Automatic Syringe Disabling Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automatic Syringe Disabling Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Automatic Syringe Disabling Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automatic Syringe Disabling Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Automatic Syringe Disabling Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automatic Syringe Disabling Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Automatic Syringe Disabling Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automatic Syringe Disabling Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Automatic Syringe Disabling Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automatic Syringe Disabling Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Automatic Syringe Disabling Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automatic Syringe Disabling Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Automatic Syringe Disabling Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automatic Syringe Disabling Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Automatic Syringe Disabling Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automatic Syringe Disabling Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Automatic Syringe Disabling Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automatic Syringe Disabling Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automatic Syringe Disabling Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automatic Syringe Disabling Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automatic Syringe Disabling Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automatic Syringe Disabling Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automatic Syringe Disabling Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automatic Syringe Disabling Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Automatic Syringe Disabling Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automatic Syringe Disabling Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Automatic Syringe Disabling Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automatic Syringe Disabling Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Automatic Syringe Disabling Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automatic Syringe Disabling Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Automatic Syringe Disabling Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Automatic Syringe Disabling Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Automatic Syringe Disabling Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Automatic Syringe Disabling Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Automatic Syringe Disabling Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Automatic Syringe Disabling Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Automatic Syringe Disabling Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Automatic Syringe Disabling Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Automatic Syringe Disabling Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Automatic Syringe Disabling Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Automatic Syringe Disabling Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Automatic Syringe Disabling Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Automatic Syringe Disabling Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Automatic Syringe Disabling Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Automatic Syringe Disabling Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Automatic Syringe Disabling Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Automatic Syringe Disabling Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automatic Syringe Disabling Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automatic Syringe Disabling?

The projected CAGR is approximately 9.1%.

2. Which companies are prominent players in the Automatic Syringe Disabling?

Key companies in the market include BD, Terumo, Vogt Medical, SPM Medical, Azur Medical, HELMJECT, Pricon, SRS Meditech, Alshifa Medical, Hindustan Syringes & Medical Devices, Hamilton, Avapezeshk.

3. What are the main segments of the Automatic Syringe Disabling?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automatic Syringe Disabling," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automatic Syringe Disabling report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automatic Syringe Disabling?

To stay informed about further developments, trends, and reports in the Automatic Syringe Disabling, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence