Key Insights

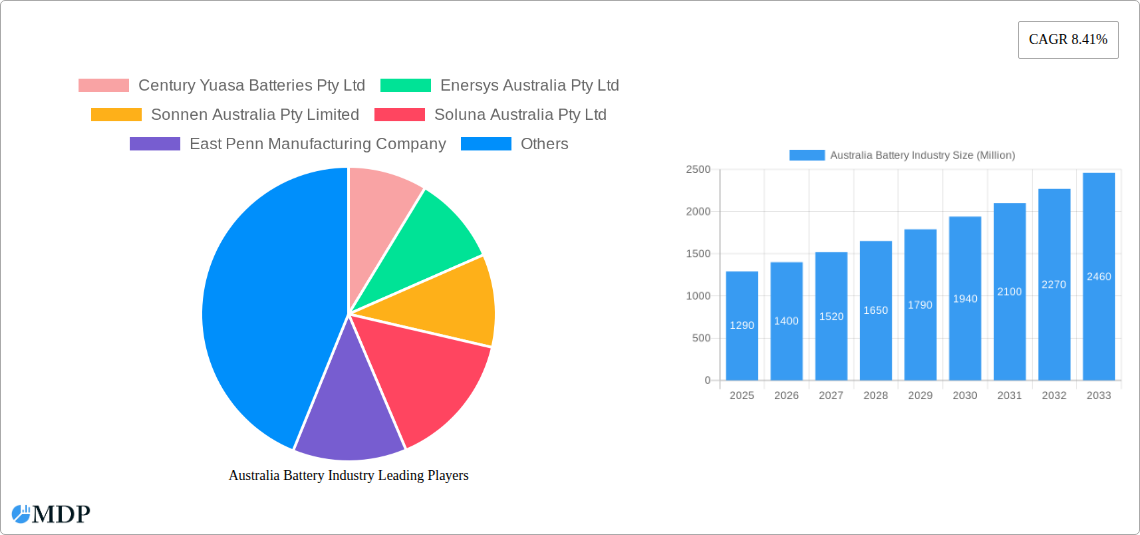

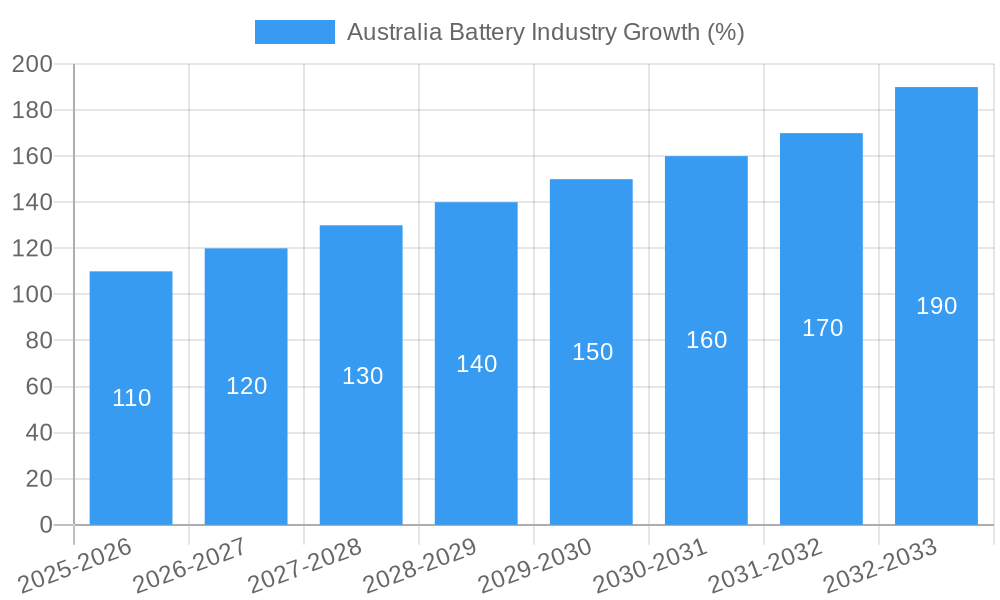

The Australian battery industry, valued at $1.29 billion in 2025, is poised for substantial growth, exhibiting a Compound Annual Growth Rate (CAGR) of 8.41% from 2025 to 2033. This expansion is fueled by several key drivers. The increasing adoption of renewable energy sources, particularly solar and wind power, necessitates efficient energy storage solutions, driving demand for stationary batteries in sectors like telecom, UPS systems, and large-scale Energy Storage Systems (ESS). Furthermore, the burgeoning electric vehicle (EV) market in Australia is significantly boosting the demand for automotive batteries, including HEV, PHEV, and EV batteries. Growth in the consumer electronics sector and industrial applications, such as motive power for forklifts and other machinery, further contributes to market expansion. While the dominance of Lithium-ion batteries is undeniable, lead-acid batteries retain a significant market share, particularly in the SLI (Starting, Lighting, Ignition) battery segment. However, technological advancements and government incentives promoting the adoption of cleaner energy technologies will likely shift the market share towards Lithium-ion and other advanced battery technologies over the forecast period. Competitive pressures from both domestic and international players, including Century Yuasa, Enersys, Sonnen, and Bosch, will shape the market landscape, driving innovation and pricing strategies. Potential regulatory changes and supply chain vulnerabilities related to raw material sourcing represent potential restraints to this growth.

The forecast period (2025-2033) anticipates continued robust growth, driven by government policies supporting renewable energy integration and the escalating demand for electric vehicles. The diversification of applications across industrial, automotive, and consumer sectors ensures a multi-faceted growth trajectory. However, achieving the projected growth will depend on overcoming challenges such as managing the rising costs of raw materials and ensuring a stable and reliable supply chain. The Australian battery industry's success will hinge on attracting investment in research and development, fostering technological innovation, and creating a supportive regulatory environment that encourages both domestic manufacturing and the adoption of advanced battery technologies. The market segmentation, encompassing various battery technologies and applications, reflects the diverse nature of the demand and the strategic positioning of different industry players.

Australia Battery Industry Market Report: 2019-2033

Dive into the comprehensive analysis of Australia's dynamic battery industry, encompassing market size, trends, leading players, and future projections (2019-2033). This report provides actionable insights for stakeholders across the value chain, from manufacturers and distributors to investors and policymakers.

This in-depth report provides a detailed analysis of the Australian battery industry, covering the period from 2019 to 2033. It features a robust forecast for 2025-2033, with 2025 serving as the base and estimated year. The historical data spans from 2019 to 2024. The report encompasses a wide range of battery technologies and applications, providing a granular understanding of the market dynamics at play.

Australia Battery Industry Market Dynamics & Concentration

This section analyzes the competitive landscape of the Australian battery market, focusing on market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user trends, and mergers and acquisitions (M&A) activities.

The Australian battery market exhibits a moderately concentrated structure, with several major players controlling significant market share. While precise market share data for individual companies is proprietary and not publicly available, estimates suggest that the top five players likely hold approximately xx% of the market in 2025. This concentration is influenced by factors such as economies of scale, technological expertise, and established distribution networks.

- Innovation Drivers: Government incentives for renewable energy integration and electric vehicle (EV) adoption are driving significant innovation in battery technologies, particularly in lithium-ion battery development.

- Regulatory Frameworks: Australia's renewable energy targets and emissions reduction policies are creating a favorable regulatory environment for battery storage solutions. Stringent safety standards and environmental regulations also play a vital role in shaping the market.

- Product Substitutes: While lithium-ion batteries are gaining dominance, lead-acid batteries continue to hold a significant share in specific applications. Emerging technologies like solid-state batteries are also anticipated to gain traction in the long term, potentially influencing market share dynamics.

- End-User Trends: The increasing adoption of EVs, renewable energy sources (solar, wind), and backup power systems (UPS, telecom) are driving demand across various battery applications. The growth in the energy storage systems (ESS) segment is particularly notable.

- M&A Activities: The number of M&A deals in the Australian battery industry has seen a steady increase, reflecting both consolidation and strategic expansion by major players. An estimated xx M&A deals were recorded between 2019 and 2024, with a projected increase in deal activity in the coming years.

Australia Battery Industry Industry Trends & Analysis

This section delves into the key trends shaping the Australian battery industry, including market growth drivers, technological disruptions, consumer preferences, and competitive dynamics.

The Australian battery market is poised for robust growth over the forecast period (2025-2033), driven primarily by the increasing adoption of renewable energy sources and the government's commitment to reducing carbon emissions. The market is expected to achieve a Compound Annual Growth Rate (CAGR) of xx% during this period. This growth will be fueled by:

- Technological Advancements: Continuous improvements in battery energy density, lifespan, and cost-effectiveness are driving higher market penetration across various segments.

- Consumer Preferences: Growing awareness of environmental sustainability and the rising popularity of electric vehicles are influencing consumer preferences toward battery-powered solutions.

- Government Policies: Australia’s focus on clean energy and its targets for renewable energy integration are providing significant tailwinds to the battery industry.

- Competitive Landscape: The market is characterized by a mix of established players and emerging companies, fostering healthy competition and driving innovation.

Leading Markets & Segments in Australia Battery Industry

This section identifies the dominant regions, countries, and segments within the Australian battery industry.

Technology:

- Lithium-ion Batteries: This segment is experiencing the most rapid growth, driven by its high energy density and suitability for applications like EVs and ESS.

- Lead-acid Batteries: Lead-acid batteries retain a significant market share, particularly in applications like SLI (starting, lighting, ignition) and industrial batteries due to their lower cost.

- Other Technologies: Emerging technologies like solid-state and flow batteries are gaining traction, but their market penetration remains relatively limited in 2025.

Application:

- Energy Storage Systems (ESS): This segment shows significant growth potential, driven by the need for grid stabilization and renewable energy integration.

- Electric Vehicles (EVs): The increasing popularity of EVs is driving demand for automotive batteries, including HEV, PHEV, and EV applications.

- Industrial Batteries: Industrial batteries (motive and stationary) constitute a significant segment due to their extensive use in various industrial processes.

- SLI Batteries: This segment remains sizable, serving the conventional automotive market. However, its growth rate is expected to slow compared to other segments.

Key Drivers:

- Government Incentives and Policies: Generous subsidies and tax incentives for renewable energy projects and EV adoption are driving the demand for batteries.

- Infrastructure Development: Significant investments in grid infrastructure to support the integration of renewable energy and storage solutions are accelerating the growth of the battery market.

The dominant segment in the Australian battery market is the ESS segment, due to the government's focus on renewable energy integration and the rising demand for grid stability.

Australia Battery Industry Product Developments

Recent advancements in battery technology have focused on enhancing energy density, lifespan, safety, and reducing costs. Improvements in lithium-ion battery chemistry, thermal management systems, and battery management systems (BMS) are prominent. These improvements are tailored to meet the specific needs of diverse applications, from EVs and ESS to portable electronics and industrial use. The competitive advantage lies in achieving optimal performance and cost-effectiveness across different applications.

Key Drivers of Australia Battery Industry Growth

The Australian battery market is fueled by a confluence of factors:

- Technological advancements: Continued improvements in battery technology, particularly in lithium-ion batteries, are lowering costs and improving performance.

- Government policies: Australia's commitment to renewable energy and its policies supporting EV adoption are strong catalysts for growth. Examples include incentives for battery manufacturing and deployment.

- Economic growth: The broader economic growth in Australia is contributing to increased demand across various battery applications.

Challenges in the Australia Battery Industry Market

The Australian battery market faces challenges:

- Supply chain disruptions: Global supply chain issues can impact the availability of raw materials and components necessary for battery manufacturing. This results in potential production delays and increased costs (estimated impact: xx Million AUD annually in 2025).

- Regulatory hurdles: Navigating complex regulations and obtaining necessary permits for battery manufacturing and deployment can pose challenges.

- Competition: The market is becoming increasingly competitive, with both established players and new entrants vying for market share.

Emerging Opportunities in Australia Battery Industry

The Australian battery industry offers promising opportunities:

- Technological breakthroughs: Continued innovation in battery technology promises to further improve performance, reduce costs, and expand applications.

- Strategic partnerships: Collaborations between battery manufacturers, energy companies, and research institutions are opening new avenues for innovation and market expansion.

- Market expansion: Growing demand for energy storage and EVs presents significant opportunities for market expansion within Australia and potentially into regional markets.

Leading Players in the Australia Battery Industry Sector

- Century Yuasa Batteries Pty Ltd

- Enersys Australia Pty Ltd

- Sonnen Australia Pty Limited

- Soluna Australia Pty Ltd

- East Penn Manufacturing Company

- Robert Bosch (Australia) Pty Ltd

- PMB Defence

- R & J Batteries Pty Ltd

- Energy Renaissance Pty Ltd

- VARTA AG

- Crystal Solar Energy

- Battery Energy Power Solutions Pty

- Exide Technologies

Key Milestones in Australia Battery Industry Industry

- June 2023: Commissioning of the Hazelwood big battery (150 MW), marking a significant milestone in large-scale battery storage deployment in Australia.

- January 2023: Recharge Industries' announcement to build a large lithium-ion battery cell factory in Australia (up to 30 GWh annual capacity), signifying a major investment in domestic battery manufacturing.

Strategic Outlook for Australia Battery Industry Market

The Australian battery industry presents significant long-term growth potential, driven by the ongoing shift towards renewable energy, increasing EV adoption, and government support for clean energy technologies. Strategic opportunities exist for companies focusing on innovation, supply chain optimization, and strategic partnerships to capitalize on this growth. The market is expected to continue expanding, with opportunities for both domestic manufacturers and international players.

Australia Battery Industry Segmentation

-

1. Technology

- 1.1. Li-Ion Battery

- 1.2. Lead-acid Battery

- 1.3. Other Technologies

-

2. Application

- 2.1. SLI Batteries

- 2.2. Industri

- 2.3. Portable Batteries (Consumer Electronics, etc.)

- 2.4. Automotive Batteries (HEV, PHEV, EV)

- 2.5. Other Applications

Australia Battery Industry Segmentation By Geography

- 1. Australia

Australia Battery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.41% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Demand from EV Sector4.; Supportive Government Policies

- 3.3. Market Restrains

- 3.3.1. 4.; Lack of Development in Battery Production Supply Chain

- 3.4. Market Trends

- 3.4.1. SLI Battery Application to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Australia Battery Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Li-Ion Battery

- 5.1.2. Lead-acid Battery

- 5.1.3. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. SLI Batteries

- 5.2.2. Industri

- 5.2.3. Portable Batteries (Consumer Electronics, etc.)

- 5.2.4. Automotive Batteries (HEV, PHEV, EV)

- 5.2.5. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Century Yuasa Batteries Pty Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Enersys Australia Pty Ltd

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Sonnen Australia Pty Limited

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Soluna Australia Pty Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 East Penn Manufacturing Company

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Robert Bosch (Australia) Pty Ltd

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 PMB Defence

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 R & J Batteries Pty Ltd

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Energy Renaissance Pty Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 VARTA AG

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Crystal Solar Energy*List Not Exhaustive

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Battery Energy Power Solutions Pty

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Exide Technologies

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.1 Century Yuasa Batteries Pty Ltd

List of Figures

- Figure 1: Australia Battery Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Australia Battery Industry Share (%) by Company 2024

List of Tables

- Table 1: Australia Battery Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Australia Battery Industry Volume Kiloton Forecast, by Region 2019 & 2032

- Table 3: Australia Battery Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 4: Australia Battery Industry Volume Kiloton Forecast, by Technology 2019 & 2032

- Table 5: Australia Battery Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 6: Australia Battery Industry Volume Kiloton Forecast, by Application 2019 & 2032

- Table 7: Australia Battery Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Australia Battery Industry Volume Kiloton Forecast, by Region 2019 & 2032

- Table 9: Australia Battery Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Australia Battery Industry Volume Kiloton Forecast, by Country 2019 & 2032

- Table 11: Australia Battery Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 12: Australia Battery Industry Volume Kiloton Forecast, by Technology 2019 & 2032

- Table 13: Australia Battery Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 14: Australia Battery Industry Volume Kiloton Forecast, by Application 2019 & 2032

- Table 15: Australia Battery Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Australia Battery Industry Volume Kiloton Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Battery Industry?

The projected CAGR is approximately 8.41%.

2. Which companies are prominent players in the Australia Battery Industry?

Key companies in the market include Century Yuasa Batteries Pty Ltd, Enersys Australia Pty Ltd, Sonnen Australia Pty Limited, Soluna Australia Pty Ltd, East Penn Manufacturing Company, Robert Bosch (Australia) Pty Ltd, PMB Defence, R & J Batteries Pty Ltd, Energy Renaissance Pty Ltd, VARTA AG, Crystal Solar Energy*List Not Exhaustive, Battery Energy Power Solutions Pty, Exide Technologies.

3. What are the main segments of the Australia Battery Industry?

The market segments include Technology, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.29 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Demand from EV Sector4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

SLI Battery Application to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Lack of Development in Battery Production Supply Chain.

8. Can you provide examples of recent developments in the market?

June 2023: Engie, Eku Energy, and Fluence commissioned the Hazelwood big battery, Australia's first large-scale battery project, at the former coal site of a power station in the state of Victoria. The 150 MW battery claims several Australian firsts in its design and operation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Kiloton.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Battery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Battery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Battery Industry?

To stay informed about further developments, trends, and reports in the Australia Battery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence