Key Insights

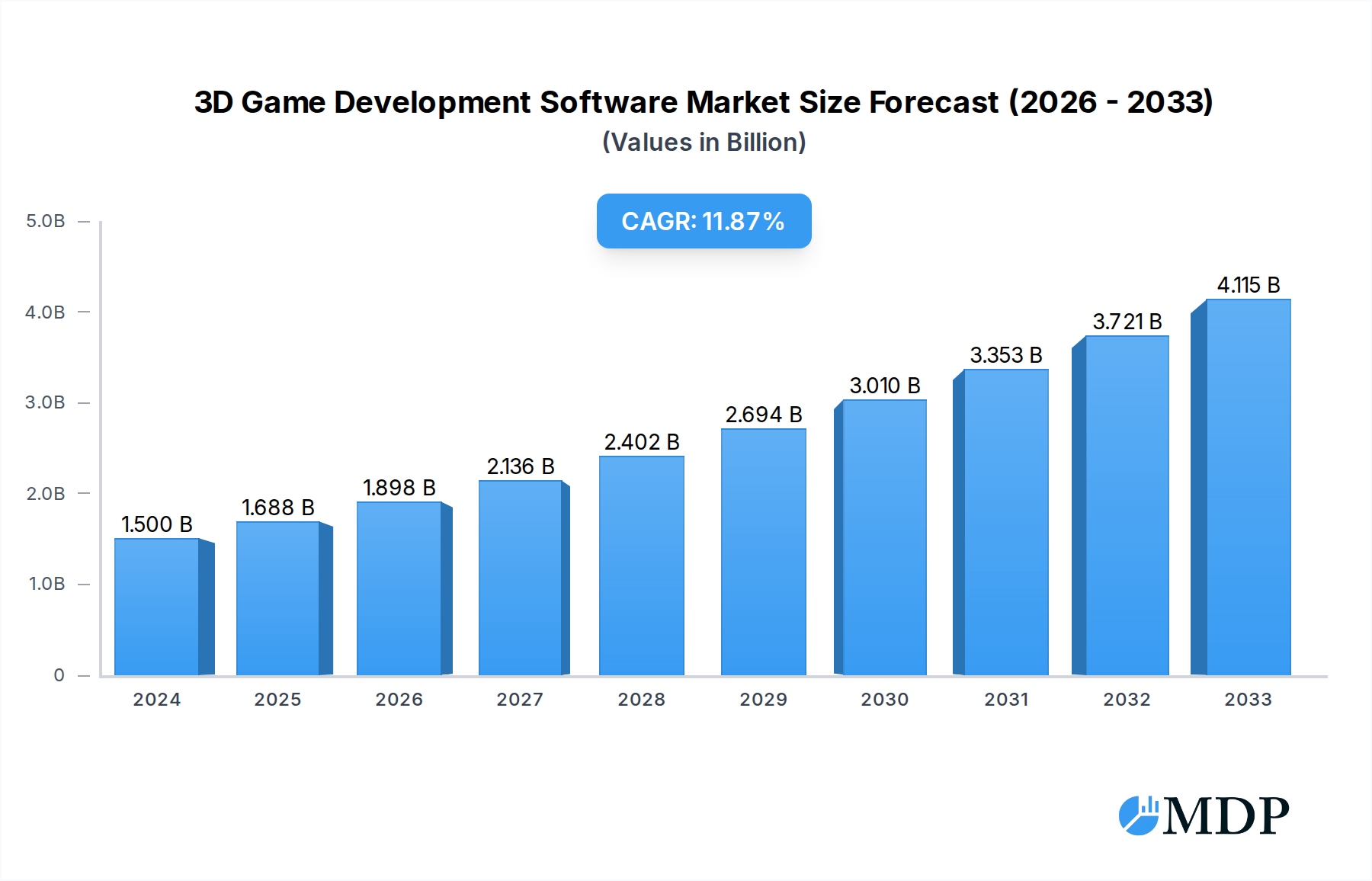

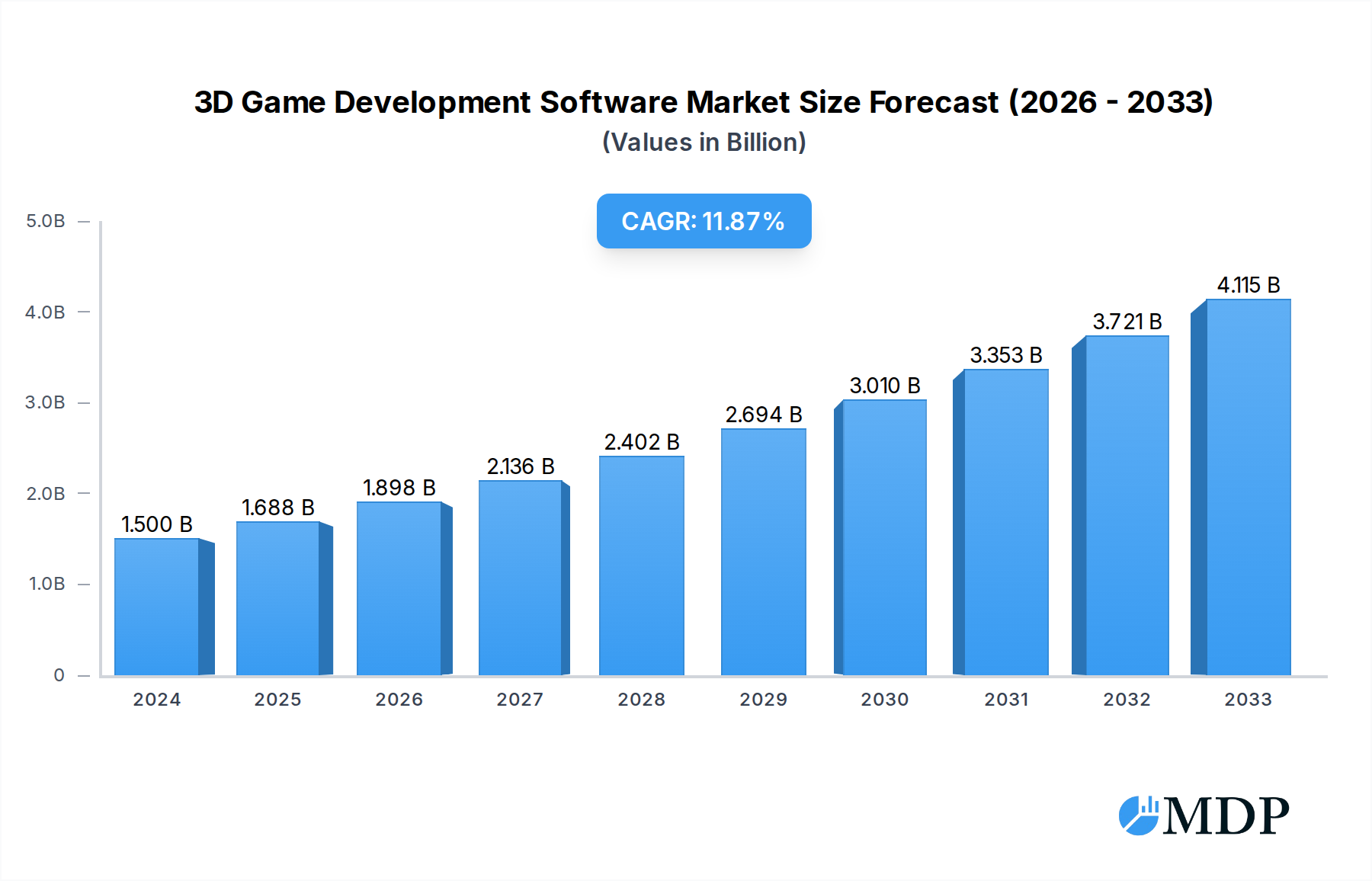

The global 3D game development software market is poised for robust expansion, projected to reach a substantial $1.5 billion in 2024. This growth is underpinned by an impressive Compound Annual Growth Rate (CAGR) of 12.3% over the forecast period from 2025 to 2033. Several key drivers are fueling this upward trajectory, including the increasing demand for immersive gaming experiences, the proliferation of advanced graphics technologies, and the growing accessibility of game development tools for both independent developers and large enterprises. The rise of mobile gaming and the continuous innovation in virtual reality (VR) and augmented reality (AR) technologies are also significant contributors, opening up new avenues for 3D game creation and consumption. Furthermore, the ongoing digital transformation across various industries, beyond gaming, is driving the adoption of 3D modeling and development tools for simulations, architectural visualization, and product design, indirectly bolstering the overall market.

3D Game Development Software Market Size (In Billion)

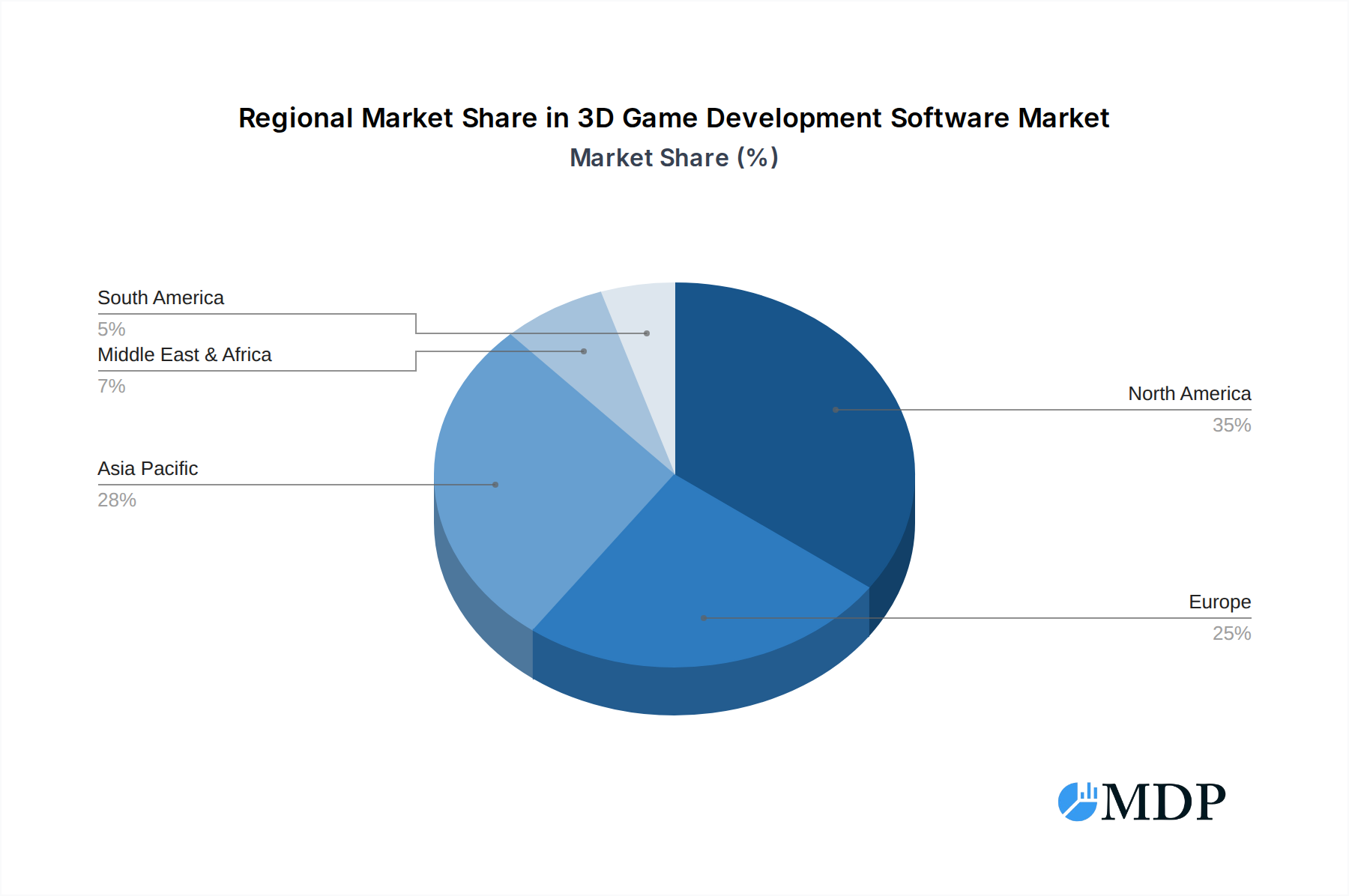

The market is segmented across various applications, with Small and Medium-sized Enterprises (SMEs) representing a rapidly growing segment due to increasingly user-friendly and affordable software solutions, while Large Enterprises continue to dominate in terms of complex, high-fidelity game production. On the technology front, both On-cloud and On-premise deployment models are witnessing adoption, with cloud solutions offering scalability and flexibility, and on-premise solutions providing enhanced control and security for specific enterprise needs. Key players like Autodesk, Epic Games (Unreal Engine), and Unity Technologies are continuously innovating, offering comprehensive suites of tools that empower developers to create sophisticated 3D game environments. Emerging restraints, such as the increasing complexity of game development pipelines and the evolving landscape of intellectual property rights, are being addressed through platform advancements and evolving business models. The market's dynamic nature is further evident in the regional distribution, with North America and Asia Pacific expected to lead in both consumption and development, driven by strong technological infrastructure and a burgeoning gaming culture.

3D Game Development Software Company Market Share

3D Game Development Software Market Dynamics & Concentration

The 3D game development software market is characterized by a dynamic interplay of innovation, competition, and evolving end-user demands. Market concentration is moderately high, with a few dominant players holding substantial market share. For instance, Unity Technologies and Epic Games (Unreal Engine) collectively command an estimated market share exceeding eighty billion dollars in 2025. Innovation drivers are primarily fueled by advancements in rendering technologies, AI-powered tools for asset creation and animation, and the increasing demand for cross-platform compatibility. Regulatory frameworks, while less stringent in this sector compared to others, focus on intellectual property rights and content moderation, impacting development workflows and distribution strategies. Product substitutes, though limited in terms of direct feature parity, include specialized indie development tools and open-source engines, which offer niche solutions for specific project needs. End-user trends reveal a growing preference for intuitive, user-friendly interfaces that lower the barrier to entry for both small and large development teams. Mergers and acquisitions (M&A) activities, while not at a billion-dollar peak, have seen several strategic acquisitions in the historical period (2019-2024) amounting to over five billion dollars in combined deal value, aimed at consolidating market presence and acquiring specialized talent or technologies. These include acquisitions of smaller asset creation studios and specialized AI solution providers by larger entities.

3D Game Development Software Industry Trends & Analysis

The 3D game development software industry is poised for substantial growth, driven by a confluence of technological breakthroughs and escalating consumer engagement with immersive digital experiences. Over the forecast period (2025–2033), the market is anticipated to witness a Compound Annual Growth Rate (CAGR) of approximately fifteen percent, propelling its valuation to an estimated three hundred billion dollars by 2033. This robust expansion is underpinned by significant technological disruptions, including the widespread adoption of real-time rendering pipelines, the integration of artificial intelligence (AI) and machine learning (ML) into asset generation and character animation, and the burgeoning influence of cloud-based development platforms that enhance collaboration and scalability. Consumer preferences are increasingly shifting towards photorealistic graphics, complex physics simulations, and interactive narratives, demanding more sophisticated and efficient development tools. This trend is particularly evident in the rapid market penetration of engines supporting virtual reality (VR) and augmented reality (AR) development, which are expected to reach over sixty percent market penetration among dedicated game studios by 2028. The competitive landscape is intensely dynamic, with established players like Autodesk, Epic Games (Unreal Engine), and Unity Technologies continuously innovating to maintain their leadership positions. They are investing heavily in R&D to offer more streamlined workflows, advanced visual fidelity options, and expanded platform support. Emerging players such as Crytek, GameSalad, Buildbox, and Delta Engine are carving out niches by focusing on specific market segments, such as mobile game development or low-code/no-code solutions, fostering a competitive environment that benefits developers through enhanced toolsets and diversified choices. The industry is also witnessing a growing convergence of game development with other digital content creation sectors, such as film, architectural visualization, and industrial design, further broadening the application and market scope of 3D game development software. This cross-pollination of technologies and applications is a key catalyst for sustained innovation and market expansion, ensuring a dynamic and evolving industry for years to come. The historical period (2019–2024) saw market growth of over one hundred billion dollars, laying a strong foundation for future expansion.

Leading Markets & Segments in 3D Game Development Software

The global 3D game development software market exhibits significant regional and segment-specific dominance, driven by a complex interplay of economic policies, technological infrastructure, and market demand. North America currently represents the largest regional market, accounting for an estimated forty-five percent of the global market share in 2025, with the United States as the primary driver due to its robust gaming industry, significant venture capital investments, and a large pool of skilled developers. Key drivers for this dominance include favorable economic policies that encourage technological innovation and entrepreneurship, a well-developed digital infrastructure supporting high-speed internet and cloud computing, and a substantial consumer base with a high disposable income for entertainment.

Within the segmentation by Application, the Large Enterprise segment is currently the dominant force, contributing over seventy percent to the total market revenue in 2025, valued at approximately two hundred billion dollars. This dominance is attributed to the substantial budgets that large game studios can allocate to advanced software, custom development tools, and extensive licensing, enabling them to create AAA titles with cutting-edge graphics and complex gameplay. The continuous need for high-fidelity visuals and intricate game mechanics in blockbuster releases necessitates the comprehensive feature sets offered by premium 3D game development software.

Conversely, the SME segment, while smaller in individual transaction value, is experiencing rapid growth and is projected to outpace the enterprise segment in terms of CAGR over the forecast period. This growth is fueled by the increasing accessibility of powerful yet more affordable development tools, the rise of indie game development as a viable career path, and the growing demand for specialized game experiences. The proliferation of accessible game engines and asset marketplaces is democratizing game creation, enabling smaller teams to compete effectively.

In terms of Types, the On-cloud segment is rapidly gaining traction and is projected to become the dominant type by 2030, currently holding an estimated fifty-five percent market share. The shift towards cloud-based solutions is driven by numerous advantages: enhanced collaboration capabilities for distributed development teams, scalable computing resources for rendering and simulation, reduced upfront hardware costs, and seamless integration with CI/CD pipelines. Cloud platforms offer flexibility and agility, allowing developers to adapt quickly to project needs and leverage powerful processing power on demand. This is particularly beneficial for SMEs and startups that may lack the capital for extensive on-premise infrastructure.

The On-premise segment, while historically dominant, is expected to see a slower growth trajectory, although it will remain a significant contributor to the market. Large enterprises with existing, robust IT infrastructures and stringent security requirements may continue to favor on-premise solutions for their perceived control and data security. However, the trend towards hybrid cloud models, combining the benefits of both on-premise and cloud solutions, is also gaining momentum, offering a balanced approach for organizations with diverse needs and legacy systems. The estimated market value for cloud-based solutions is projected to reach over one hundred and fifty billion dollars by 2033, significantly outpacing the on-premise segment's growth.

3D Game Development Software Product Developments

Recent product developments in 3D game development software are sharply focused on enhancing realism, streamlining workflows, and expanding creative possibilities. Innovations in real-time ray tracing and global illumination are pushing the boundaries of visual fidelity, enabling developers to create incredibly lifelike environments and character models. The integration of AI-powered tools for procedural content generation, animation rigging, and asset optimization is significantly reducing development time and costs. Furthermore, the expansion of cross-platform compatibility, with robust support for PC, consoles, mobile, and emerging XR devices, is a key competitive advantage. These advancements are not only empowering large studios to produce more visually stunning and immersive experiences but are also making sophisticated development tools more accessible to independent developers and smaller teams, fostering a more vibrant and diverse game development ecosystem.

Key Drivers of 3D Game Development Software Growth

The growth of the 3D game development software market is primarily propelled by several key factors. Technological advancements, particularly in real-time rendering, AI for asset creation, and VR/AR integration, are continuously enhancing the capabilities and appeal of these tools. The burgeoning demand for immersive gaming experiences across diverse platforms, from consoles and PCs to mobile and XR devices, fuels the need for sophisticated development software. Economic factors, including increasing disposable incomes globally and significant investment in the gaming industry, create a fertile ground for market expansion. Regulatory factors, such as intellectual property protection and content standards, while not always direct drivers, shape the development landscape and can influence software adoption. The continuous evolution of consumer preferences towards higher visual fidelity and interactive narratives further accentuates the need for advanced 3D game development solutions.

Challenges in the 3D Game Development Software Market

Despite its robust growth, the 3D game development software market faces several challenges. High software licensing costs can be a barrier, particularly for independent developers and small studios with limited budgets, potentially exceeding ten thousand dollars per user annually for premium licenses. The steep learning curve associated with advanced features and complex workflows requires significant training and expertise, impacting developer productivity. Intense market competition leads to rapid obsolescence of older versions, necessitating continuous investment in software updates and training, with upgrade costs sometimes reaching twenty percent of the initial purchase price. Furthermore, the increasing complexity of game development projects, coupled with evolving platform requirements and the need for cross-platform compatibility, can strain development resources and timelines. Supply chain issues for high-end development hardware, though less prevalent for software itself, can indirectly impact project timelines and budgets.

Emerging Opportunities in 3D Game Development Software

Emerging opportunities in the 3D game development software market are largely driven by technological breakthroughs and strategic market expansion. The continued advancement and adoption of Artificial Intelligence (AI) present significant opportunities for automating asset creation, character animation, and even game design processes, potentially reducing development cycles by as much as thirty percent. The expanding market for Augmented Reality (AR) and Virtual Reality (VR) experiences, projected to reach over one hundred billion dollars by 2030, offers a substantial growth avenue for software that supports these immersive platforms. Strategic partnerships between software developers and hardware manufacturers, as well as collaborations with emerging technologies like the metaverse, can unlock new revenue streams and market penetration. Furthermore, the increasing demand for real-time 3D content beyond gaming, in sectors like virtual production, architectural visualization, and digital twins, opens up vast new application areas for existing and adapted game development software.

Leading Players in the 3D Game Development Software Sector

- Autodesk

- Epic Games (Unreal Engine)

- Unity Technologies

- GameSalad

- Crytek

- Buildbox

- Delta Engine

Key Milestones in 3D Game Development Software Industry

- 2019: Release of Unreal Engine 4.23, introducing significant rendering enhancements and workflow improvements.

- 2020: Unity Technologies announces its IPO, highlighting the strong market demand for game development tools, raising over one billion dollars.

- 2020: Autodesk releases Maya 2020, focusing on animation and rigging tools, integrated with its broader creative suite.

- 2021: Epic Games launches Unreal Engine 5, showcasing groundbreaking features like Nanite and Lumen, revolutionizing real-time rendering capabilities.

- 2021: Unity introduces its DOTS (Data-Oriented Technology Stack) to improve performance and scalability for complex projects.

- 2022: GameSalad introduces significant updates to its visual scripting interface, making it more accessible for mobile game development.

- 2022: Buildbox releases new tools for rapid prototyping and monetization, targeting the casual and hyper-casual game markets.

- 2023: Crytek's CryEngine receives updates focusing on cross-platform development and enhanced visual realism.

- 2023: Delta Engine releases a new version with improved networking capabilities for multiplayer game development.

- 2024: Significant advancements in AI-driven asset generation tools are integrated into leading game engines, reducing manual creation effort by up to forty percent.

Strategic Outlook for 3D Game Development Software Market

The strategic outlook for the 3D game development software market is exceptionally positive, driven by sustained innovation and expanding applications. The increasing integration of AI and machine learning will continue to democratize development, enabling more complex and visually rich experiences to be created with greater efficiency. The burgeoning XR market presents a significant growth accelerator, with software vendors focusing on robust tools for VR and AR content creation. Furthermore, the convergence of game development with other real-time 3D industries, such as virtual production and the metaverse, offers substantial diversification and revenue opportunities. Companies that can adapt to these evolving technological landscapes, foster strong developer communities, and provide scalable, accessible solutions are poised for significant success in the coming years, with market projections indicating growth exceeding five hundred billion dollars by 2033.

3D Game Development Software Segmentation

-

1. Application

- 1.1. SME

- 1.2. Large Enterprise

-

2. Types

- 2.1. On-cloud

- 2.2. On-premise

3D Game Development Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

3D Game Development Software Regional Market Share

Geographic Coverage of 3D Game Development Software

3D Game Development Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global 3D Game Development Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. SME

- 5.1.2. Large Enterprise

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. On-cloud

- 5.2.2. On-premise

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America 3D Game Development Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. SME

- 6.1.2. Large Enterprise

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. On-cloud

- 6.2.2. On-premise

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America 3D Game Development Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. SME

- 7.1.2. Large Enterprise

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. On-cloud

- 7.2.2. On-premise

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe 3D Game Development Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. SME

- 8.1.2. Large Enterprise

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. On-cloud

- 8.2.2. On-premise

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa 3D Game Development Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. SME

- 9.1.2. Large Enterprise

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. On-cloud

- 9.2.2. On-premise

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific 3D Game Development Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. SME

- 10.1.2. Large Enterprise

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. On-cloud

- 10.2.2. On-premise

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Autodesk

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Epic Games (Unreal Engine)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Unity Technologies

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 GameSalad

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Crytek

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Buildbox

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Delta Engine

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.1 Autodesk

List of Figures

- Figure 1: Global 3D Game Development Software Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America 3D Game Development Software Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America 3D Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America 3D Game Development Software Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America 3D Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America 3D Game Development Software Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America 3D Game Development Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America 3D Game Development Software Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America 3D Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America 3D Game Development Software Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America 3D Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America 3D Game Development Software Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America 3D Game Development Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe 3D Game Development Software Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe 3D Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe 3D Game Development Software Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe 3D Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe 3D Game Development Software Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe 3D Game Development Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa 3D Game Development Software Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa 3D Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa 3D Game Development Software Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa 3D Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa 3D Game Development Software Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa 3D Game Development Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific 3D Game Development Software Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific 3D Game Development Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific 3D Game Development Software Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific 3D Game Development Software Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific 3D Game Development Software Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific 3D Game Development Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global 3D Game Development Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global 3D Game Development Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global 3D Game Development Software Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global 3D Game Development Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global 3D Game Development Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global 3D Game Development Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global 3D Game Development Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global 3D Game Development Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global 3D Game Development Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global 3D Game Development Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global 3D Game Development Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global 3D Game Development Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global 3D Game Development Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global 3D Game Development Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global 3D Game Development Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global 3D Game Development Software Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global 3D Game Development Software Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global 3D Game Development Software Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific 3D Game Development Software Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the 3D Game Development Software?

The projected CAGR is approximately 12.3%.

2. Which companies are prominent players in the 3D Game Development Software?

Key companies in the market include Autodesk, Epic Games (Unreal Engine), Unity Technologies, GameSalad, Crytek, Buildbox, Delta Engine.

3. What are the main segments of the 3D Game Development Software?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "3D Game Development Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the 3D Game Development Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the 3D Game Development Software?

To stay informed about further developments, trends, and reports in the 3D Game Development Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence