Key Insights

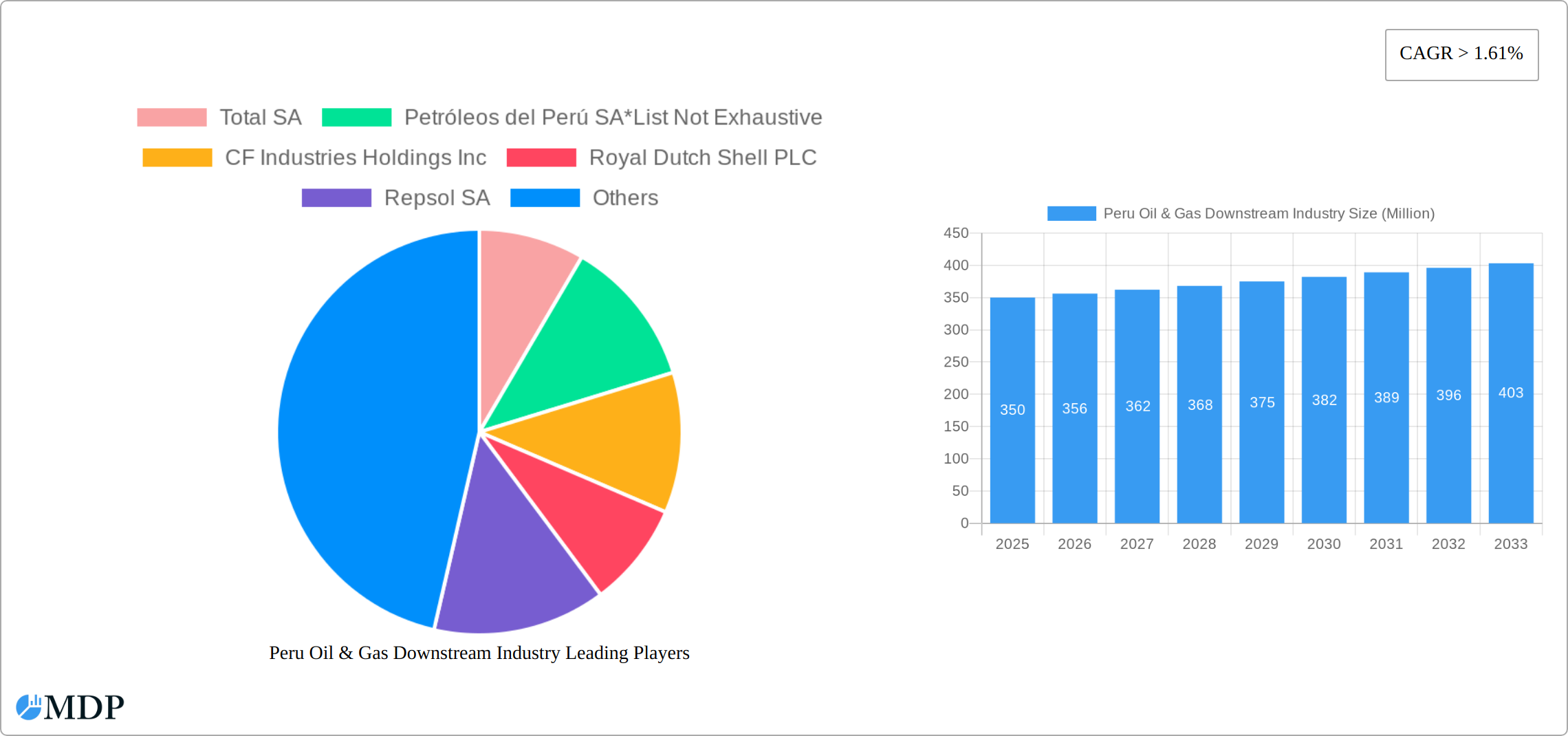

The Peruvian oil and gas downstream industry, encompassing refineries and petrochemical plants, presents a compelling investment landscape characterized by steady growth. While the precise market size for 2025 is unavailable, considering a CAGR of 1.61% from a base year (likely representing a historical average), and acknowledging the presence of significant players like Total SA, Petróleos del Perú SA, and Repsol SA, we can reasonably infer a market valuation in the hundreds of millions of USD for 2025. Key drivers include increasing domestic energy demand fueled by population growth and economic development, coupled with government initiatives to improve infrastructure and attract foreign investment in the energy sector. However, the sector also faces constraints, such as dependence on fluctuating global oil prices and potential challenges related to environmental regulations and sustainability concerns. The segment breakdown between refineries and petrochemical plants is likely weighted towards refineries given Peru's current energy consumption patterns. Growth will likely be driven by investments in refinery modernization and expansion to meet the country's growing energy demands. Looking ahead to 2033, strategic investments in downstream infrastructure and diversification of energy sources are crucial to ensure sustained growth and resilience against external economic shocks. The presence of multinational companies suggests a high level of international engagement in Peru’s oil and gas market, which should underpin future growth.

The forecast period (2025-2033) anticipates continued expansion, though the rate of growth may be influenced by geopolitical factors and global energy transitions. The inclusion of companies like CF Industries Holdings Inc, which is predominantly focused on fertilizers and chemicals, indicates potential opportunities for integration and expansion in related industries. Regional analysis focusing solely on Peru highlights the localized nature of this market study, although downstream operations are frequently linked to broader global energy markets and supply chains. The period 2019-2024 serves as a valuable baseline, providing insights into historical market trends and informing future projections. Further granular data regarding production capacity, consumption patterns, and regulatory frameworks would enhance the precision of future analyses.

Peru Oil & Gas Downstream Industry: 2019-2033 Market Report

Unlocking Growth Potential in Peru's Dynamic Downstream Energy Sector

This comprehensive report provides an in-depth analysis of Peru's oil & gas downstream industry, offering invaluable insights for stakeholders seeking to navigate this evolving market. The study covers the period 2019-2033, with a focus on the forecast period 2025-2033 and a base year of 2025. Benefit from detailed market sizing, segmentation, competitive analysis, and growth projections to inform strategic decision-making. Key players like Total SA, Petróleos del Perú SA, CF Industries Holdings Inc, Royal Dutch Shell PLC, and Repsol SA are analyzed, but the list is not exhaustive.

Peru Oil & Gas Downstream Industry Market Dynamics & Concentration

This section analyzes the competitive landscape, focusing on market concentration, innovation, regulation, substitutes, end-user trends, and mergers & acquisitions (M&A) activity within Peru's downstream oil & gas sector. The market share of key players is assessed, alongside the number of M&A deals throughout the historical period (2019-2024).

- Market Concentration: The Peruvian downstream market exhibits a moderately concentrated structure, with a few dominant players controlling a significant portion (estimated at xx%) of the refinery and petrochemical plant capacity. This concentration is largely driven by significant investments from international players and the relatively high capital expenditure required for refinery operations and petrochemical plant constructions.

- Innovation Drivers: Technological advancements in refining processes and petrochemical production are pushing efficiency and yield improvements. Government support and regulatory incentives for cleaner fuels and reduced emissions contribute to environmentally conscious innovation.

- Regulatory Frameworks: Stringent environmental regulations, aimed at reducing pollution and greenhouse gas emissions, are shaping industry practices and driving investment in cleaner technologies. Furthermore, policies focused on energy security and diversification are impacting investment decisions and market strategies.

- Product Substitutes: The emergence of renewable energy sources and biofuels represents a growing threat of substitution, particularly in the transportation sector. This requires market players to adopt strategies to enhance market competitiveness through product diversification and innovation of more sustainable products.

- End-User Trends: The growing demand for refined petroleum products from transportation, industrial, and residential sectors significantly influence market dynamics. This demand is expected to increase alongside population growth and economic development. However, shifts in consumer preferences towards electric vehicles and other sustainable transportation options present challenges.

- M&A Activities: The historical period (2019-2024) witnessed xx M&A deals, primarily driven by companies aiming to enhance market share, expand their geographic footprint, and gain access to crucial infrastructure. This is likely to continue, fueled by the dynamic nature of the market and opportunities arising from consolidation.

Peru Oil & Gas Downstream Industry Industry Trends & Analysis

This section provides a comprehensive analysis of the major trends shaping the growth trajectory of Peru's oil & gas downstream sector from 2019 to 2033. We delve into technological advancements, evolving consumer preferences, competitive dynamics, and the projected Compound Annual Growth Rate (CAGR) and market penetration. The analysis incorporates both quantitative data and qualitative insights to offer a holistic view of the market's evolution.

The Peruvian downstream oil & gas market is projected to experience a CAGR of [Insert Projected CAGR]% during the forecast period (2025-2033). This growth is fueled by several interconnected factors: a burgeoning energy demand driven by sustained economic expansion; a significant increase in transportation fuel consumption, reflecting Peru's growing vehicle fleet and improved infrastructure; and the robust expansion of industrial activity across various sectors. Furthermore, technological disruptions are playing a pivotal role. The adoption of advanced refining technologies, including those focused on enhanced efficiency and reduced emissions, is transforming the industry landscape. The integration of sophisticated digital solutions for process optimization, predictive maintenance, and improved operational efficiency further contributes to this positive growth trajectory. Finally, the evolving consumer preferences, including a growing demand for cleaner and more sustainable fuels, and increasingly stringent environmental regulations, are prompting significant shifts in product development and market positioning strategies. This dynamic environment necessitates innovative competitive strategies for both established and emerging players, focusing on operational efficiency, technological innovation, and strategic partnerships.

Leading Markets & Segments in Peru Oil & Gas Downstream Industry

This section details the dominant segments within Peru's downstream industry, specifically focusing on Refineries and Petrochemicals Plants. A detailed analysis highlights the leading regions, key growth drivers, and factors contributing to their dominance.

- Refineries: The Lima metropolitan area holds the largest refining capacity, driven by its proximity to major consumption centers and existing infrastructure. This location benefits from ease of logistics, transportation, and access to major markets.

- Petrochemicals Plants: While the petrochemical sector remains relatively smaller compared to refining, it's anticipated to witness growth, driven by the increasing demand for petrochemical products in the manufacturing and construction sectors. Furthermore, government incentives targeting industrial development and industrial diversification are anticipated to encourage further growth in this segment.

- Key Drivers: Favorable government policies encouraging domestic production, investment in infrastructure (such as pipelines and storage facilities), and the proximity to major markets significantly contribute to the dominance of specific regions and segments. The overall economic growth and increasing urbanization of the population fuel demand for products from these segments.

Peru Oil & Gas Downstream Industry Product Developments

Recent innovations in Peru's downstream oil & gas sector are primarily focused on enhancing fuel quality to meet increasingly stringent environmental regulations. Significant advancements in refining processes are leading to improved efficiency, higher yields, and a reduced environmental footprint. There is a strong emphasis on the production of cleaner fuels, including the exploration of alternative feedstocks and the growing development of biofuels. This trend aligns with the global shift towards more sustainable energy sources and responds to both regulatory pressures and changing consumer demands. These developments are fostering a highly competitive landscape that rewards innovation, technological leadership, and efficient operations.

Key Drivers of Peru Oil & Gas Downstream Industry Growth

The robust growth of Peru's downstream oil & gas sector is underpinned by several key drivers. Strong economic growth consistently fuels increased energy demand across various sectors, including transportation, industry, and residential consumption. Government initiatives focused on infrastructure development, particularly in transportation and energy, play a crucial supporting role, enhancing the sector's overall efficiency and capacity. The continuous rise in urbanization and industrial activity, coupled with steady population growth, has created a significant and sustained demand for refined petroleum products. Finally, the adoption and implementation of modern and efficient refining technologies further amplifies the sector's growth potential by maximizing resource utilization and minimizing environmental impact.

Challenges in the Peru Oil & Gas Downstream Industry Market

The Peruvian downstream oil & gas market faces challenges such as fluctuating global oil prices, which affect profitability and investment decisions. Infrastructure limitations, particularly in pipeline capacity and storage facilities, create logistical bottlenecks. Environmental regulations, while necessary, increase operational costs and compliance burdens. Moreover, intense competition among existing players, and the potential entry of new competitors, necessitates constant adaptation and innovation to maintain market share. These factors combined can significantly impact the overall growth and sustainability of the industry.

Emerging Opportunities in Peru Oil & Gas Downstream Industry

Significant long-term growth opportunities exist for Peru's downstream oil & gas industry. Strategic partnerships focused on technological advancements and infrastructure development are vital to unlock this potential. The exploration and development of renewable energy sources and biofuels offer crucial avenues for diversification and the achievement of sustainable growth. Investing in cutting-edge refining technologies and expanding the petrochemical sector to meet the growing demand for petrochemical products across multiple industries will further bolster the sector's long-term prospects. These opportunities require a balanced approach, combining innovation with responsible environmental stewardship.

Leading Players in the Peru Oil & Gas Downstream Industry Sector

- Total SA

- Petróleos del Perú SA

- CF Industries Holdings Inc

- Royal Dutch Shell PLC

- Repsol SA

Key Milestones in Peru Oil & Gas Downstream Industry Industry

- 2020-Q2: Implementation of new environmental regulations impacting refinery operations.

- 2021-Q4: Completion of a major pipeline expansion project enhancing transportation capabilities.

- 2022-Q1: Launch of a new, higher-quality gasoline blend.

- 2023-Q3: Announcement of a significant investment in a new petrochemical plant. (Further details not available, xx Million investment anticipated.)

Strategic Outlook for Peru Oil & Gas Downstream Industry Market

The future of Peru's downstream oil & gas market remains positive, driven by persistent economic growth and steadily increasing energy demand. Strategic investments in infrastructure modernization, the widespread adoption of cleaner and more efficient technologies, and calculated diversification into related sectors like biofuels and petrochemicals will be instrumental in unlocking further growth and ensuring the long-term sustainability of the industry. The market presents substantial and attractive opportunities for both established players and new entrants eager to capitalize on rising energy demands and the government's commitment to creating a modern and efficient energy sector.

Peru Oil & Gas Downstream Industry Segmentation

-

1. Refineries

-

1.1. Overview

- 1.1.1. Existing Infrastructure

- 1.1.2. Projects in Pipeline

- 1.1.3. Upcoming Projects

-

1.1. Overview

-

2. Petrochemicals Plants

-

2.1. Overview

- 2.1.1. Existing Infrastructure

- 2.1.2. Projects in Pipeline

- 2.1.3. Upcoming Projects

-

2.1. Overview

Peru Oil & Gas Downstream Industry Segmentation By Geography

- 1. Peru

Peru Oil & Gas Downstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 1.61% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Declining Solar Panel Costs4.; Supportive Government Policies

- 3.3. Market Restrains

- 3.3.1. 4.; High Upfront Cost

- 3.4. Market Trends

- 3.4.1. Oil Refining Capacity to Witness Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Peru Oil & Gas Downstream Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 5.1.1. Overview

- 5.1.1.1. Existing Infrastructure

- 5.1.1.2. Projects in Pipeline

- 5.1.1.3. Upcoming Projects

- 5.1.1. Overview

- 5.2. Market Analysis, Insights and Forecast - by Petrochemicals Plants

- 5.2.1. Overview

- 5.2.1.1. Existing Infrastructure

- 5.2.1.2. Projects in Pipeline

- 5.2.1.3. Upcoming Projects

- 5.2.1. Overview

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Peru

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Total SA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Petróleos del Perú SA*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 CF Industries Holdings Inc

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Royal Dutch Shell PLC

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Repsol SA

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.1 Total SA

List of Figures

- Figure 1: Peru Oil & Gas Downstream Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Peru Oil & Gas Downstream Industry Share (%) by Company 2024

List of Tables

- Table 1: Peru Oil & Gas Downstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Peru Oil & Gas Downstream Industry Revenue Million Forecast, by Refineries 2019 & 2032

- Table 3: Peru Oil & Gas Downstream Industry Revenue Million Forecast, by Petrochemicals Plants 2019 & 2032

- Table 4: Peru Oil & Gas Downstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Peru Oil & Gas Downstream Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Peru Oil & Gas Downstream Industry Revenue Million Forecast, by Refineries 2019 & 2032

- Table 7: Peru Oil & Gas Downstream Industry Revenue Million Forecast, by Petrochemicals Plants 2019 & 2032

- Table 8: Peru Oil & Gas Downstream Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Peru Oil & Gas Downstream Industry?

The projected CAGR is approximately > 1.61%.

2. Which companies are prominent players in the Peru Oil & Gas Downstream Industry?

Key companies in the market include Total SA, Petróleos del Perú SA*List Not Exhaustive, CF Industries Holdings Inc, Royal Dutch Shell PLC, Repsol SA.

3. What are the main segments of the Peru Oil & Gas Downstream Industry?

The market segments include Refineries, Petrochemicals Plants.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Declining Solar Panel Costs4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Oil Refining Capacity to Witness Growth.

7. Are there any restraints impacting market growth?

4.; High Upfront Cost.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Peru Oil & Gas Downstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Peru Oil & Gas Downstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Peru Oil & Gas Downstream Industry?

To stay informed about further developments, trends, and reports in the Peru Oil & Gas Downstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence