Key Insights

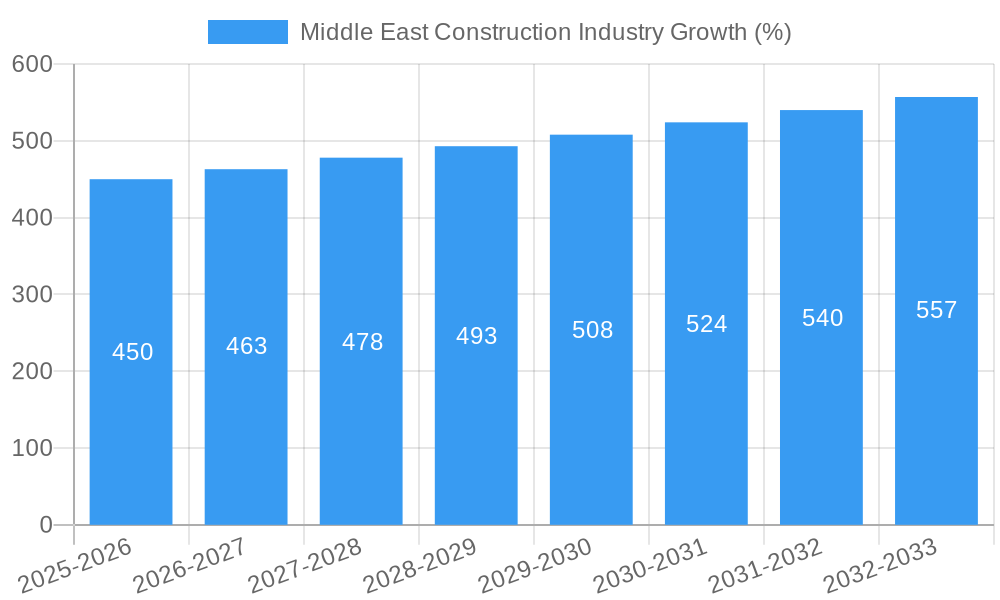

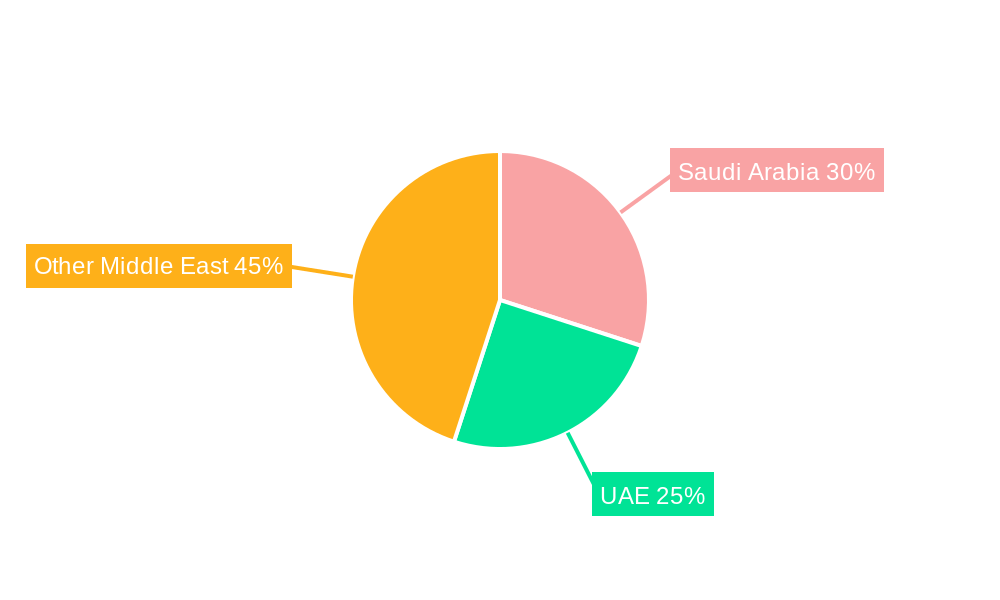

The Middle East construction industry, currently valued at approximately $XX million (assuming a reasonable figure based on regional economic activity and global construction market size), is experiencing robust growth, with a Compound Annual Growth Rate (CAGR) exceeding 3.00%. This expansion is driven by several key factors. Significant investments in infrastructure development, fueled by rising populations and urbanization across nations like Saudi Arabia and the UAE, are a primary catalyst. Furthermore, mega-projects, including large-scale residential, commercial, and industrial constructions, contribute significantly to the industry's dynamism. Government initiatives promoting sustainable building practices and technological advancements in construction materials, such as the increased adoption of polymers and improved bitumen formulations, are also shaping market trends. However, the sector faces challenges such as fluctuating oil prices, potential labor shortages, and the need for increased regulatory compliance surrounding sustainable building practices. The segmentation of the market highlights growth opportunities across various material types (bitumen, rubber, metal, polymer) and end-user sectors (residential, commercial, industrial). Specific countries like Saudi Arabia and the UAE are major contributors to the overall market size, reflecting their robust economic activity and ambitious infrastructure development plans.

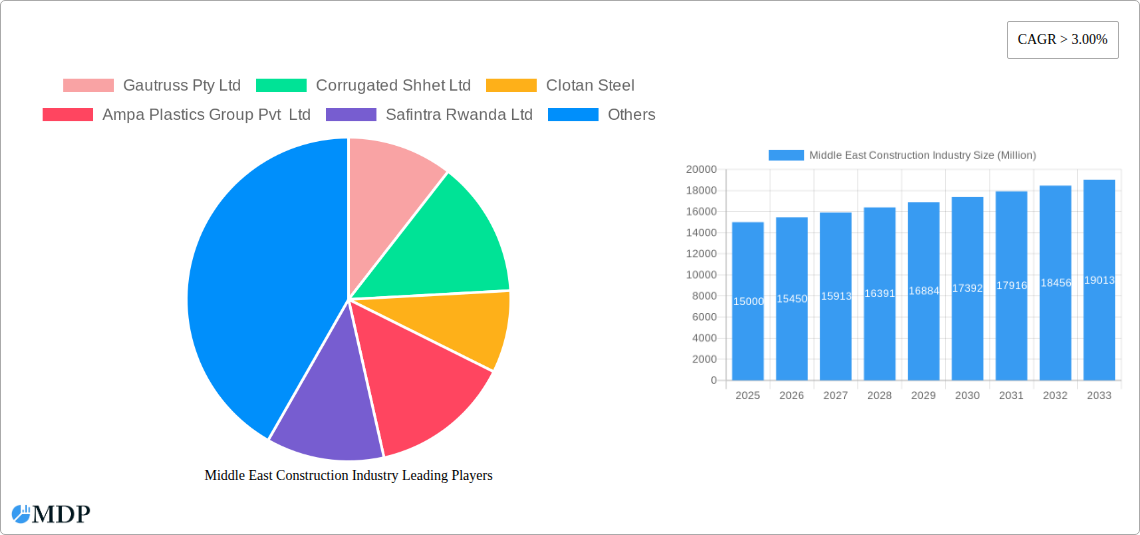

The competitive landscape is marked by a mix of both local and international players, including companies like Gautruss Pty Ltd, Corrugated Sheet Ltd, and Al Shafar Steel Engineering. While competition is fierce, opportunities exist for companies offering innovative, sustainable, and cost-effective solutions. The forecast period (2025-2033) anticipates continued growth, potentially exceeding current projections given the region's ongoing investments in infrastructure and the expanding urban landscape. Further research into specific sub-sectors, such as green building materials and smart construction technologies, will offer more granular insights into investment potential. The market's resilience is linked to the long-term vision of regional governments, suggesting continued growth and investment potential in the coming decade.

Middle East Construction Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Middle East construction industry, offering invaluable insights for stakeholders, investors, and industry professionals. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report leverages historical data (2019-2024) to project future market trends and opportunities. Discover key market drivers, challenges, and emerging opportunities within this dynamic sector. The report covers a wide geographical scope, including Saudi Arabia, the United Arab Emirates, Iran, South Africa, and the Rest of Middle East and Africa, analyzing market segments by material (bitumen, rubber, metal, polymer) and end-user (residential, commercial, industrial). The total market size is predicted to reach xx Million by 2033.

Middle East Construction Industry Market Dynamics & Concentration

The Middle East construction market exhibits a moderately concentrated landscape, with a few dominant players commanding significant market share. Market concentration is influenced by factors such as government regulations, access to capital, and technological advancements. Innovation is driven primarily by the need for sustainable building practices, improved efficiency, and enhanced safety standards. Regulatory frameworks, including building codes and environmental regulations, significantly impact market dynamics. Product substitutes, such as alternative building materials, also influence market competition. End-user trends, particularly towards sustainable and technologically advanced buildings, are reshaping market demand. The last five years have witnessed xx M&A deals, indicating a trend towards consolidation within the industry. Key players' market share fluctuations are primarily attributed to infrastructure projects and economic policies. Saudi Arabia currently holds the largest market share, with xx% in 2025, followed by the UAE with xx%.

Middle East Construction Industry Industry Trends & Analysis

The Middle East construction industry is experiencing robust growth, driven by factors such as rapid urbanization, population growth, and significant investments in infrastructure development. The Compound Annual Growth Rate (CAGR) is projected to be xx% during the forecast period (2025-2033). Technological disruptions, such as Building Information Modeling (BIM) and the adoption of prefabricated construction methods, are improving efficiency and reducing construction timelines. Consumer preferences are shifting towards sustainable and smart buildings, increasing demand for eco-friendly materials and technologies. Competitive dynamics are characterized by intense rivalry among established players and the emergence of innovative start-ups. Market penetration of sustainable building materials is gradually increasing, currently at xx%, expected to reach xx% by 2033.

Leading Markets & Segments in Middle East Construction Industry

- Dominant Region/Country: Saudi Arabia and the UAE remain the leading markets, driven by large-scale infrastructure projects, government initiatives, and robust economic growth. Iran demonstrates significant, albeit volatile, growth potential.

- Dominant Segment (By Material): Metal accounts for the largest share of the market, driven by its use in high-rise buildings and infrastructure projects. Polymer materials are experiencing rapid growth due to their lightweight and versatile nature.

- Dominant Segment (By End User): The commercial sector dominates, propelled by the growth of the hospitality, retail, and office sectors. Residential construction also displays strong growth, driven by population growth and rising urbanization.

Key Drivers:

- Saudi Arabia: Vision 2030 initiatives, substantial investments in infrastructure projects (Neom, Qiddiya), and government support for the construction sector.

- UAE: Focus on diversification of the economy beyond oil, large-scale infrastructure projects for Expo 2020 legacy, and investments in smart city initiatives.

- Iran: Despite economic sanctions, continued investment in housing and infrastructure projects fuels moderate growth.

The dominance of these markets and segments reflects sustained investment in infrastructure development and large-scale construction projects.

Middle East Construction Industry Product Developments

The industry is witnessing a surge in innovative products, including advanced building materials with enhanced durability and sustainability features, prefabricated building components, and smart building technologies. These advancements cater to the growing demand for efficient, sustainable, and technologically advanced construction solutions. The market is favoring products that offer improved performance, reduced construction time, and lower environmental impact, aligning with the region's sustainability goals.

Key Drivers of Middle East Construction Industry Growth

Several factors fuel the industry's growth. Government investments in infrastructure projects, such as new airports, roads, and railways, play a major role. Rapid urbanization and population growth necessitate increased housing and commercial development. Furthermore, supportive economic policies and a focus on sustainable development create a favorable environment for market expansion. The adoption of advanced construction technologies enhances productivity and efficiency.

Challenges in the Middle East Construction Industry Market

The industry faces significant challenges, including regulatory complexities, supply chain disruptions impacting material availability and cost, and fierce competition among numerous players. These factors create uncertainty and impact project timelines and profitability. Labor shortages and fluctuating material prices also pose significant operational challenges. Furthermore, political instability in certain regions poses a risk to project continuity. These challenges collectively contribute to a xx Million loss annually.

Emerging Opportunities in Middle East Construction Industry

The long-term growth outlook is positive. The increasing adoption of sustainable building practices, technological advancements (like BIM and 3D printing), and strategic partnerships between local and international firms present major opportunities. Expansion into emerging markets within the region and a focus on specialized construction niches (such as renewable energy infrastructure) also offer significant growth potential.

Leading Players in the Middle East Construction Industry Sector

- Gautruss Pty Ltd

- Corrugated Shhet Ltd

- Clotan Steel

- Ampa Plastics Group Pvt Ltd

- Safintra Rwanda Ltd

- Algoa Steel & Roofing

- Kirby International

- Al Shafar Steel Engineering

- Palram Industries Ltd

- Youngman

Key Milestones in Middle East Construction Industry Industry

- 2020: Launch of several large-scale infrastructure projects in Saudi Arabia under Vision 2030.

- 2021: Increased adoption of BIM technology across multiple projects in the UAE.

- 2022: Significant investment in sustainable building materials across the region.

- 2023: Several mergers and acquisitions within the construction materials sector.

Strategic Outlook for Middle East Construction Industry Market

The Middle East construction industry is poised for sustained growth, driven by ongoing infrastructure development and increasing urbanization. Strategic partnerships, investment in technological advancements, and a focus on sustainable practices will be crucial for success. Companies that can adapt to changing market dynamics and regulatory environments will be well-positioned to capitalize on the significant opportunities within this dynamic sector. The market is expected to see continuous growth and innovation in the coming years, leading to further expansion and development.

Middle East Construction Industry Segmentation

-

1. Material

- 1.1. Bitumen

- 1.2. Rubber

- 1.3. Metal

- 1.4. Polymer

-

2. End User

- 2.1. Residential

- 2.2. Commercial

- 2.3. Industrial

Middle East Construction Industry Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle East Construction Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 3.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Rapid Urabanization4.; Increasing government investments

- 3.3. Market Restrains

- 3.3.1. 4.; Increasing cost of raw materials affecting the construction industry4.; Slowdown in economic growth affecting the market

- 3.4. Market Trends

- 3.4.1. Construction Activities Playing a Significant Role in the Construction Sheets Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Middle East Construction Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Bitumen

- 5.1.2. Rubber

- 5.1.3. Metal

- 5.1.4. Polymer

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Residential

- 5.2.2. Commercial

- 5.2.3. Industrial

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. United Arab Emirates Middle East Construction Industry Analysis, Insights and Forecast, 2019-2031

- 7. Saudi Arabia Middle East Construction Industry Analysis, Insights and Forecast, 2019-2031

- 8. Qatar Middle East Construction Industry Analysis, Insights and Forecast, 2019-2031

- 9. Israel Middle East Construction Industry Analysis, Insights and Forecast, 2019-2031

- 10. Egypt Middle East Construction Industry Analysis, Insights and Forecast, 2019-2031

- 11. Oman Middle East Construction Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Middle East Middle East Construction Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Gautruss Pty Ltd

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Corrugated Shhet Ltd

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Clotan Steel

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Ampa Plastics Group Pvt Ltd

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Safintra Rwanda Ltd

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Algoa Steel & Roofing

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Kirby International**List Not Exhaustive

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Al Shafar Steel Engineering

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Palram Industries Ltd

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Youngman

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Gautruss Pty Ltd

List of Figures

- Figure 1: Middle East Construction Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Middle East Construction Industry Share (%) by Company 2024

List of Tables

- Table 1: Middle East Construction Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Middle East Construction Industry Revenue Million Forecast, by Material 2019 & 2032

- Table 3: Middle East Construction Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 4: Middle East Construction Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Middle East Construction Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United Arab Emirates Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Saudi Arabia Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Qatar Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Israel Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Egypt Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Oman Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Middle East Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Middle East Construction Industry Revenue Million Forecast, by Material 2019 & 2032

- Table 14: Middle East Construction Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 15: Middle East Construction Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Saudi Arabia Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: United Arab Emirates Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Israel Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Qatar Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Kuwait Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Oman Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Bahrain Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Jordan Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Lebanon Middle East Construction Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Construction Industry?

The projected CAGR is approximately > 3.00%.

2. Which companies are prominent players in the Middle East Construction Industry?

Key companies in the market include Gautruss Pty Ltd, Corrugated Shhet Ltd, Clotan Steel, Ampa Plastics Group Pvt Ltd, Safintra Rwanda Ltd, Algoa Steel & Roofing, Kirby International**List Not Exhaustive, Al Shafar Steel Engineering, Palram Industries Ltd, Youngman.

3. What are the main segments of the Middle East Construction Industry?

The market segments include Material, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Rapid Urabanization4.; Increasing government investments.

6. What are the notable trends driving market growth?

Construction Activities Playing a Significant Role in the Construction Sheets Market.

7. Are there any restraints impacting market growth?

4.; Increasing cost of raw materials affecting the construction industry4.; Slowdown in economic growth affecting the market.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Construction Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Construction Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Construction Industry?

To stay informed about further developments, trends, and reports in the Middle East Construction Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence