Key Insights

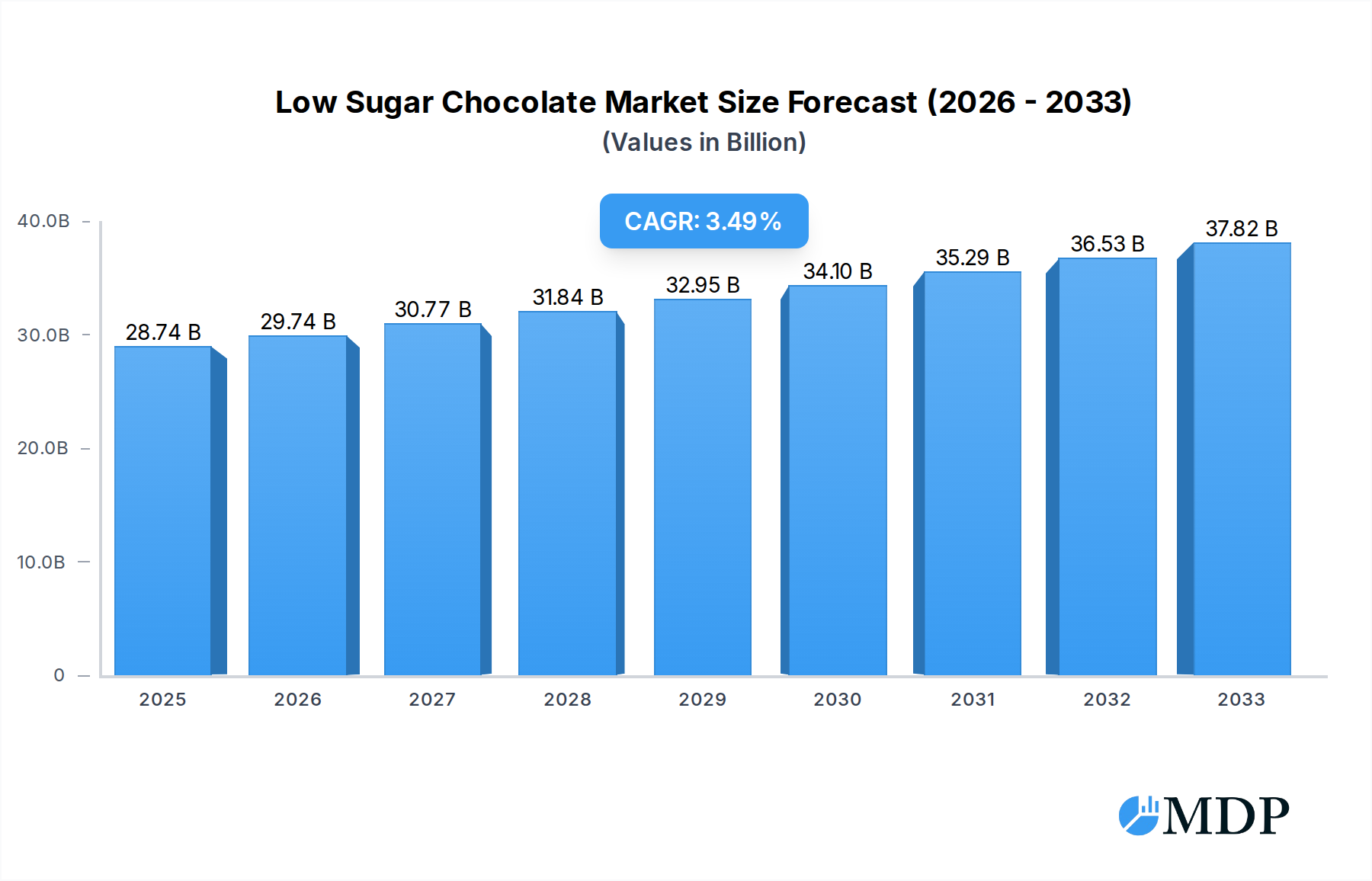

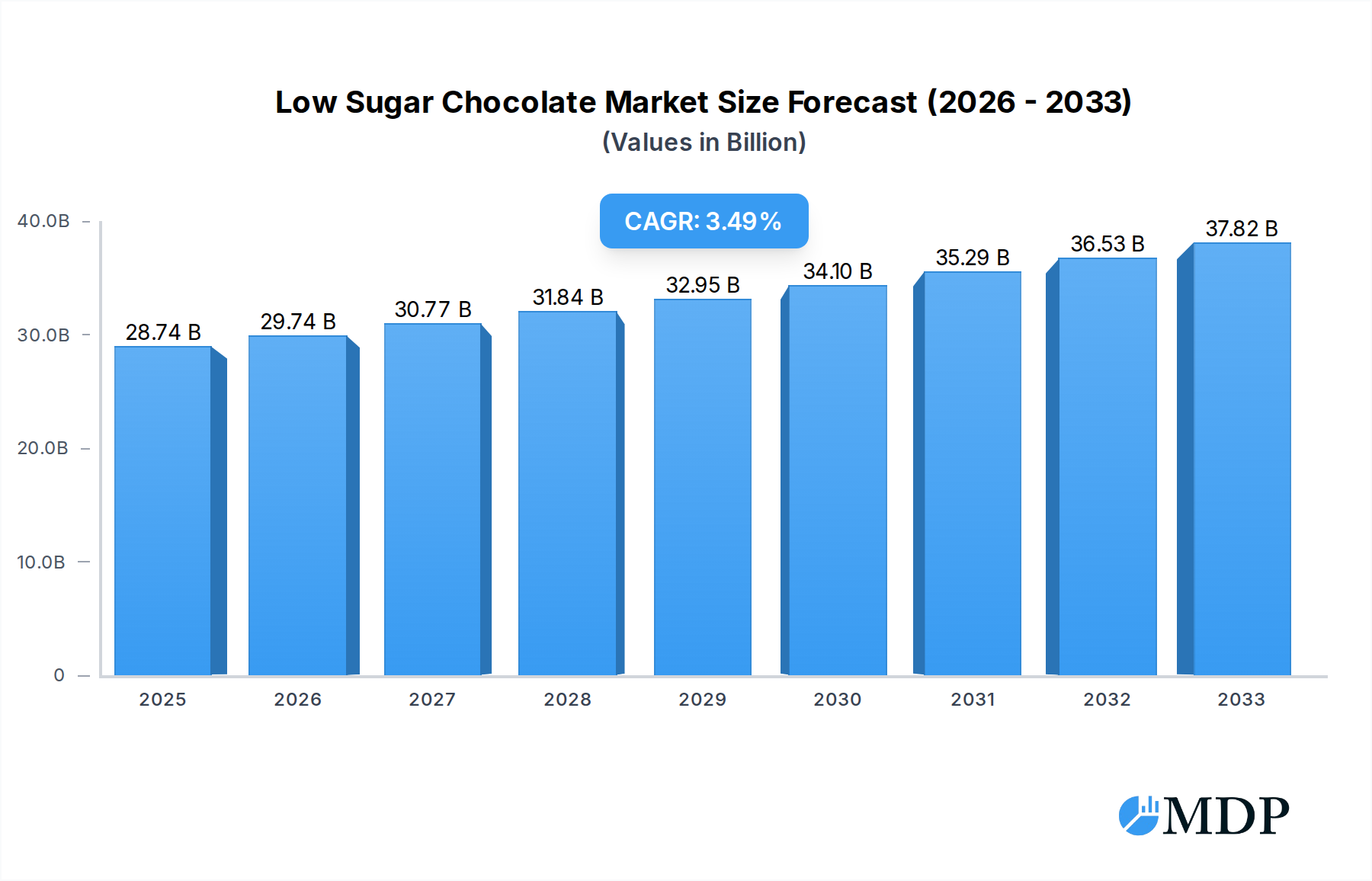

The global Low Sugar Chocolate market is poised for significant expansion, projected to reach $28.74 billion by 2025. This robust growth is underpinned by a projected Compound Annual Growth Rate (CAGR) of 3.4% from 2019 to 2033. The primary driver behind this upward trajectory is a growing consumer consciousness regarding health and wellness, leading to an increased demand for confectionery products with reduced sugar content. This shift is further amplified by dietary trends such as ketogenic and paleo diets, which actively favor low-sugar alternatives. The market's expansion is also fueled by innovation in sugar-alternative technologies and a wider availability of appealing low-sugar chocolate formulations, addressing taste and texture concerns that previously hindered adoption.

Low Sugar Chocolate Market Size (In Billion)

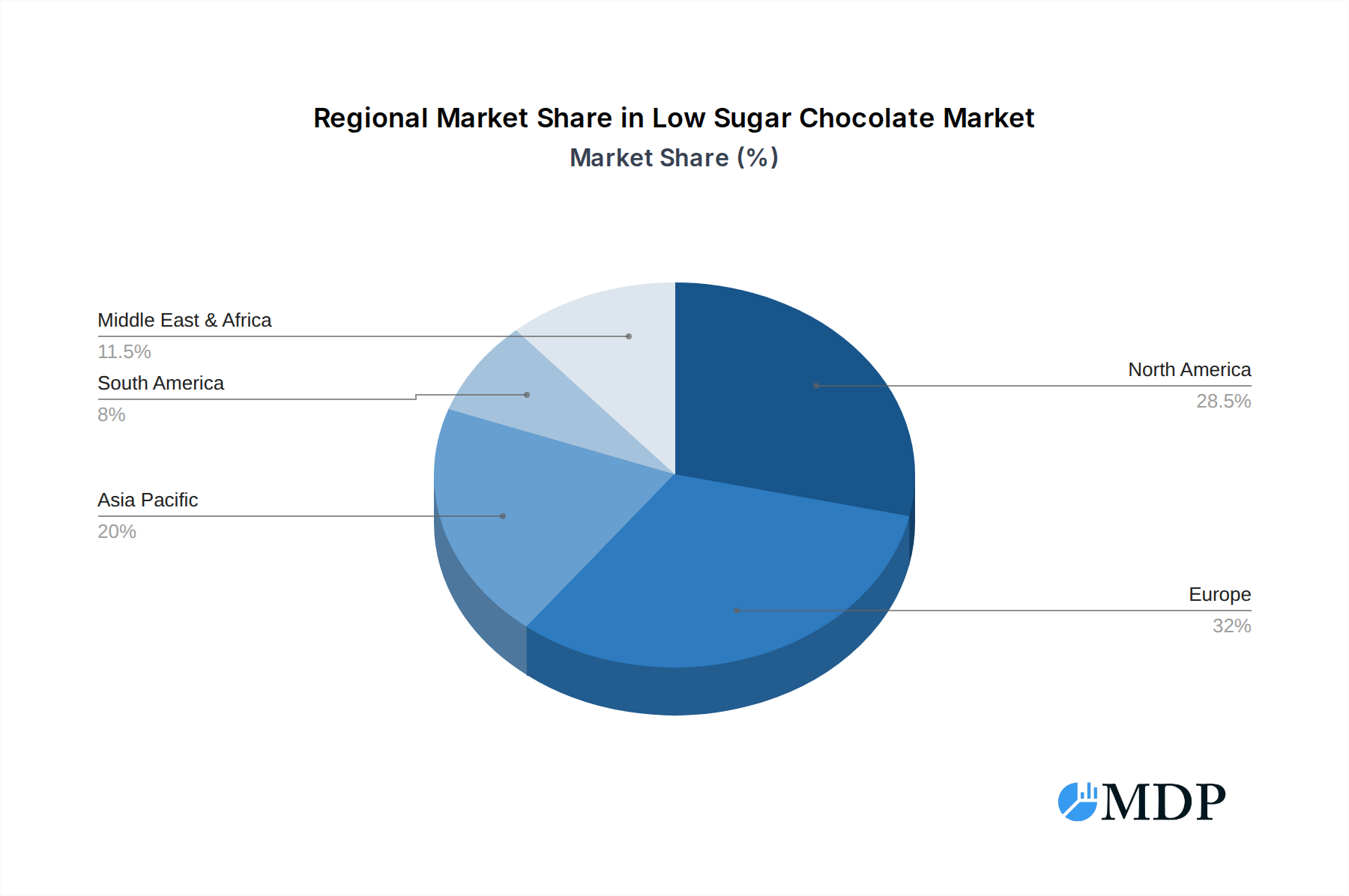

Further diversifying the market landscape, the application segment is witnessing strong performance in both chocolate bars and flavoring ingredients, indicating a dual demand for direct consumption and incorporation into other food products. The prevalence of dark chocolate within the low-sugar segment highlights its inherent lower sugar profile and perceived health benefits. Geographically, North America and Europe are leading the charge, driven by established health trends and higher disposable incomes. However, the Asia Pacific region presents a substantial untapped potential, with rapid urbanization and a burgeoning middle class increasingly adopting healthier lifestyle choices. Key industry players are actively investing in research and development to expand their product portfolios and cater to evolving consumer preferences, solidifying the market's dynamic and promising future.

Low Sugar Chocolate Company Market Share

This comprehensive Low Sugar Chocolate Market report offers an in-depth analysis of a rapidly expanding global industry. With a study period spanning 2019–2033, a base year of 2025, and a forecast period from 2025–2033, this report provides invaluable insights for industry stakeholders, including manufacturers, ingredient suppliers, and market analysts. Delving into high-traffic keywords such as "sugar-free chocolate," "healthy indulgence," "dietary chocolate," and "reduced sugar confectionery," this report is optimized to maximize search visibility and attract relevant audiences. We project the global Low Sugar Chocolate market to reach billions by the end of the forecast period, driven by escalating consumer demand for healthier alternatives and significant industry innovation.

Low Sugar Chocolate Market Dynamics & Concentration

The Low Sugar Chocolate market exhibits a dynamic and evolving landscape, characterized by increasing competition and a strong focus on innovation. Market concentration remains moderate, with a few dominant players holding significant market share, while a growing number of agile companies are carving out niches. Innovation drivers are primarily centered around novel sweeteners, improved taste profiles that mimic traditional sugar-sweetened chocolate, and the development of functional low-sugar variants. Regulatory frameworks are becoming increasingly stringent regarding sugar content labeling and health claims, pushing manufacturers towards cleaner ingredient lists and transparent communication. Product substitutes, such as other low-sugar snacks and sugar-free confectionery alternatives, pose a competitive threat, necessitating continuous product development. End-user trends are overwhelmingly skewed towards health-conscious consumers seeking guilt-free indulgence, leading to a surge in demand for dark chocolate and other varieties with lower sugar content. Mergers and acquisitions (M&A) activities are expected to remain active as larger players seek to acquire innovative technologies or expand their presence in this lucrative segment. With an estimated billions in M&A deal counts over the forecast period, strategic consolidation will shape the future market structure.

- Market Share Concentration: Moderate, with leading companies holding substantial but not entirely dominant positions.

- Innovation Drivers: Natural sweeteners, advanced flavor technologies, functional ingredient integration.

- Regulatory Frameworks: Increasing focus on clear labeling, health claims verification, and sugar reduction initiatives.

- Product Substitutes: Sugar-free candies, low-calorie snacks, fruit-based desserts.

- End-User Trends: Health and wellness focus, demand for natural ingredients, desire for indulgent yet guilt-free options.

- M&A Activities: Expected to rise as companies seek strategic partnerships and market consolidation.

Low Sugar Chocolate Industry Trends & Analysis

The Low Sugar Chocolate industry is poised for significant expansion, driven by a confluence of powerful market growth drivers. A primary catalyst is the escalating global health and wellness trend, where consumers are actively seeking to reduce their sugar intake due to concerns about obesity, diabetes, and other chronic diseases. This shift in consumer consciousness directly translates into a robust demand for low sugar chocolate bars, sugar-free dark chocolate, and dietary chocolate options. Technological disruptions are playing a crucial role, with advancements in natural sweetener technologies, such as stevia, erythritol, and monk fruit, enabling manufacturers to create products that are not only lower in sugar but also offer improved taste and texture profiles, closely replicating the sensory experience of traditional chocolate. The development of innovative flavoring ingredients that enhance sweetness perception without added sugar further fuels this trend. Market penetration for low sugar chocolate is steadily increasing, moving beyond niche health food stores to mainstream retail channels. The CAGR for the global low sugar chocolate market is projected to be approximately billions over the forecast period. Competitive dynamics are intensifying, with established confectionery giants and agile startups alike vying for market share. Companies are investing heavily in research and development to create novel formulations, appealing packaging, and targeted marketing campaigns. The increasing availability of reduced sugar confectionery options across various product formats, including chocolate bars, truffles, and baking ingredients, is broadening the market's appeal. Furthermore, the growing understanding of the role of sugar in various health conditions is creating a sustained demand for healthy indulgence options. The market is witnessing a rise in premium and artisanal low sugar chocolates, catering to consumers willing to pay a premium for quality ingredients and sophisticated flavor profiles. The global market size is anticipated to reach billions by 2025.

Leading Markets & Segments in Low Sugar Chocolate

The Low Sugar Chocolate market demonstrates significant regional and segmental dominance, driven by distinct consumer preferences and regulatory landscapes. North America currently leads the market, propelled by a highly health-conscious consumer base and a strong emphasis on dietary management. The United States, in particular, showcases robust demand for sugar-free dark chocolate and low sugar chocolate bars, influenced by widespread awareness of diabetes and obesity. Economic policies supporting healthier food options and the presence of major confectionery manufacturers actively investing in this segment contribute to this leadership. Europe follows closely, with countries like Germany and the United Kingdom exhibiting a growing appetite for reduced sugar confectionery, driven by stringent sugar taxes and public health campaigns.

Within the Application segment, Chocolate Bars command the largest market share, accounting for an estimated billions in sales, as they represent a convenient and popular format for consumers seeking a healthier treat. The demand for Flavoring Ingredient applications, used in a wide array of food and beverage products, is also significant and projected to grow steadily, reaching an estimated billions. The Others segment, encompassing products like chocolate chips, confectionery coatings, and specialty items, represents a developing but promising area.

In terms of Type, Dark Chocolate dominates the low sugar segment, with its inherent lower sugar content and perceived health benefits resonating strongly with consumers. Its market share is estimated to be billions. The Others segment, which includes low sugar milk chocolate, white chocolate, and other variations, is experiencing rapid growth as manufacturers develop innovative formulations to cater to a broader range of taste preferences, projected to reach billions.

- Dominant Region: North America, particularly the United States, driven by health consciousness and supportive economic policies.

- Leading Application: Chocolate Bars, offering convenience and widespread appeal.

- Key Drivers for Chocolate Bars: On-the-go consumption, diverse flavor options, and accessible pricing.

- Dominant Type: Dark Chocolate, due to its natural lower sugar content and health associations.

- Emerging Growth Segment (Type): Low Sugar Milk and White Chocolate, as formulation advancements improve taste and texture.

- Significant Application Growth: Flavoring Ingredients, supporting broader food and beverage innovation.

Low Sugar Chocolate Product Developments

The Low Sugar Chocolate sector is witnessing a wave of innovation focused on enhancing taste, texture, and health benefits. Leading companies like Barry Callebaut and Lindt are at the forefront, developing proprietary sweetener blends and advanced processing techniques to minimize sugar without compromising on the rich, decadent experience consumers expect from chocolate. Innovations include the use of natural, low-glycemic sweeteners like allulose and monk fruit, alongside improved cocoa bean sourcing and roasting methods to amplify natural sweetness. Product developments are increasingly emphasizing functional benefits, such as added fiber, probiotics, or antioxidants, transforming indulgence into a health-conscious choice. This strategic focus on superior taste profiles and added nutritional value provides a significant competitive advantage, capturing the growing segment of consumers actively seeking healthier alternatives.

Key Drivers of Low Sugar Chocolate Growth

The growth of the Low Sugar Chocolate market is primarily propelled by evolving consumer health consciousness, with an increasing global awareness of the detrimental effects of excessive sugar consumption. This has led to a sustained demand for healthier confectionery alternatives, pushing manufacturers to innovate and cater to this trend. Technological advancements in natural sweetener technologies and flavor masking are crucial, enabling the creation of low-sugar chocolates with taste profiles comparable to their traditional counterparts. Regulatory support, through initiatives promoting sugar reduction and clear labeling, further encourages the development and adoption of low-sugar options.

- Health & Wellness Trend: Rising consumer focus on reducing sugar intake for better health.

- Technological Innovation: Advancements in natural sweeteners and flavor enhancement.

- Regulatory Initiatives: Government policies encouraging sugar reduction and transparent labeling.

- Product Diversification: Expansion of low-sugar options across various formats and types.

Challenges in the Low Sugar Chocolate Market

Despite its promising growth, the Low Sugar Chocolate market faces several challenges. The primary hurdle is the inherent difficulty in replicating the exact taste and texture of traditional sugar-laden chocolate using alternative sweeteners, leading to potential compromises in sensory experience for some consumers. High ingredient costs for natural sweeteners and specialty ingredients can result in premium pricing, limiting affordability and market penetration for a broader consumer base. Supply chain complexities for novel ingredients and stringent regulatory approvals for new food additives can also pose significant challenges. Furthermore, intense competition from established confectionery brands and the ever-evolving consumer preferences require continuous investment in research and development to maintain a competitive edge.

- Taste & Texture Compromise: Difficulty in perfectly replicating traditional chocolate's sensory profile.

- High Ingredient Costs: Premium pricing for natural sweeteners and specialized ingredients.

- Supply Chain Complexity: Sourcing and availability of novel ingredients.

- Regulatory Hurdles: Approval processes for new food additives and health claims.

Emerging Opportunities in Low Sugar Chocolate

The Low Sugar Chocolate market is ripe with emerging opportunities, driven by unmet consumer needs and continuous innovation. The development of functional low-sugar chocolates, fortified with ingredients like probiotics, prebiotics, or adaptogens, presents a significant avenue for growth, catering to the increasing demand for holistic wellness products. Strategic partnerships between confectionery manufacturers and ingredient technology companies can accelerate the development of novel sweeteners and flavor profiles. Furthermore, the expansion into emerging markets with a growing middle class and increasing health awareness offers substantial untapped potential. The rise of direct-to-consumer (DTC) models allows brands to directly engage with health-conscious consumers, fostering loyalty and gathering valuable market insights.

Leading Players in the Low Sugar Chocolate Sector

- Barry Callebaut

- Stella Bernrain

- Lindt

- Chocolat Frey

- Chocolats Halba

- Läderach

- Felchlin

- Pfister Chocolatier

- Favarger

- Camillebloch

- Alprose

- Gysi

- Cailler (Nestle)

- Villars

- Mondelēz International

- Maestrani Schweizer Schokoladen

- Confiserie Sprüngli

Key Milestones in Low Sugar Chocolate Industry

- 2019: Increased consumer awareness regarding sugar's health impact drives initial demand for low sugar options.

- 2020: Major confectionery companies begin investing in R&D for sugar reduction technologies.

- 2021: Launch of innovative stevia-sweetened chocolate bars by several key players.

- 2022: Growing popularity of monk fruit and allulose as primary sweeteners in chocolate formulations.

- 2023: Expansion of low sugar dark chocolate offerings and introduction of functional low sugar chocolate products.

- 2024: Increased regulatory scrutiny on sugar content and health claims in confectionery.

- 2025: Projected significant market growth as consumer adoption of low sugar chocolate reaches new heights.

- 2026-2033: Anticipated further innovation in sweetener technology, expanded product portfolios, and increased market penetration globally.

Strategic Outlook for Low Sugar Chocolate Market

The strategic outlook for the Low Sugar Chocolate Market is overwhelmingly positive, with significant growth accelerators in place. The persistent global shift towards healthier lifestyles and preventative healthcare will continue to fuel demand for reduced-sugar alternatives. Manufacturers are advised to focus on innovation in natural sweetener technology and flavor science to overcome taste perception barriers. Strategic partnerships with ingredient suppliers and research institutions are crucial for staying ahead of the curve. Expanding product portfolios to include a wider variety of low-sugar options, including milk and white chocolate, will broaden consumer appeal. Furthermore, leveraging digital marketing and e-commerce platforms to reach and engage health-conscious consumers directly presents a key opportunity for market expansion and brand building. The market is projected to witness continued robust growth and evolving consumer preferences.

Low Sugar Chocolate Segmentation

-

1. Application

- 1.1. Chocolate Bars

- 1.2. Flavoring Ingredient

- 1.3. Others

-

2. Type

- 2.1. Dark Chocolate

- 2.2. Others

Low Sugar Chocolate Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Low Sugar Chocolate Regional Market Share

Geographic Coverage of Low Sugar Chocolate

Low Sugar Chocolate REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Chocolate Bars

- 5.1.2. Flavoring Ingredient

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Dark Chocolate

- 5.2.2. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Low Sugar Chocolate Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Chocolate Bars

- 6.1.2. Flavoring Ingredient

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Dark Chocolate

- 6.2.2. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Low Sugar Chocolate Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Chocolate Bars

- 7.1.2. Flavoring Ingredient

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Dark Chocolate

- 7.2.2. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Low Sugar Chocolate Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Chocolate Bars

- 8.1.2. Flavoring Ingredient

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Dark Chocolate

- 8.2.2. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Low Sugar Chocolate Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Chocolate Bars

- 9.1.2. Flavoring Ingredient

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Dark Chocolate

- 9.2.2. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Low Sugar Chocolate Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Chocolate Bars

- 10.1.2. Flavoring Ingredient

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Dark Chocolate

- 10.2.2. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Low Sugar Chocolate Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Chocolate Bars

- 11.1.2. Flavoring Ingredient

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Dark Chocolate

- 11.2.2. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Barry Callebaut

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Stella Bernrain

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Lindt

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Chocolat Frey

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Chocolats Halba

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Läderach

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Felchlin

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Pfister Chocolatier

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Favarger

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Camillebloch

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Alprose

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Gysi

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Cailler (Nestle)

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Villars

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Mondelēz International

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Maestrani Schweizer Schokoladen

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Confiserie Sprüngli

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 Barry Callebaut

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Low Sugar Chocolate Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Low Sugar Chocolate Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Low Sugar Chocolate Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Low Sugar Chocolate Volume (K), by Application 2025 & 2033

- Figure 5: North America Low Sugar Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Low Sugar Chocolate Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Low Sugar Chocolate Revenue (billion), by Type 2025 & 2033

- Figure 8: North America Low Sugar Chocolate Volume (K), by Type 2025 & 2033

- Figure 9: North America Low Sugar Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Low Sugar Chocolate Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Low Sugar Chocolate Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Low Sugar Chocolate Volume (K), by Country 2025 & 2033

- Figure 13: North America Low Sugar Chocolate Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Low Sugar Chocolate Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Low Sugar Chocolate Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Low Sugar Chocolate Volume (K), by Application 2025 & 2033

- Figure 17: South America Low Sugar Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Low Sugar Chocolate Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Low Sugar Chocolate Revenue (billion), by Type 2025 & 2033

- Figure 20: South America Low Sugar Chocolate Volume (K), by Type 2025 & 2033

- Figure 21: South America Low Sugar Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Low Sugar Chocolate Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Low Sugar Chocolate Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Low Sugar Chocolate Volume (K), by Country 2025 & 2033

- Figure 25: South America Low Sugar Chocolate Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Low Sugar Chocolate Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Low Sugar Chocolate Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Low Sugar Chocolate Volume (K), by Application 2025 & 2033

- Figure 29: Europe Low Sugar Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Low Sugar Chocolate Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Low Sugar Chocolate Revenue (billion), by Type 2025 & 2033

- Figure 32: Europe Low Sugar Chocolate Volume (K), by Type 2025 & 2033

- Figure 33: Europe Low Sugar Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Low Sugar Chocolate Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Low Sugar Chocolate Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Low Sugar Chocolate Volume (K), by Country 2025 & 2033

- Figure 37: Europe Low Sugar Chocolate Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Low Sugar Chocolate Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Low Sugar Chocolate Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Low Sugar Chocolate Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Low Sugar Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Low Sugar Chocolate Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Low Sugar Chocolate Revenue (billion), by Type 2025 & 2033

- Figure 44: Middle East & Africa Low Sugar Chocolate Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Low Sugar Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Low Sugar Chocolate Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Low Sugar Chocolate Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Low Sugar Chocolate Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Low Sugar Chocolate Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Low Sugar Chocolate Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Low Sugar Chocolate Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Low Sugar Chocolate Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Low Sugar Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Low Sugar Chocolate Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Low Sugar Chocolate Revenue (billion), by Type 2025 & 2033

- Figure 56: Asia Pacific Low Sugar Chocolate Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Low Sugar Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Low Sugar Chocolate Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Low Sugar Chocolate Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Low Sugar Chocolate Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Low Sugar Chocolate Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Low Sugar Chocolate Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Low Sugar Chocolate Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Low Sugar Chocolate Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Low Sugar Chocolate Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global Low Sugar Chocolate Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Low Sugar Chocolate Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Low Sugar Chocolate Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Low Sugar Chocolate Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Low Sugar Chocolate Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Low Sugar Chocolate Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Low Sugar Chocolate Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Low Sugar Chocolate Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Low Sugar Chocolate Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Low Sugar Chocolate Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Low Sugar Chocolate Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Low Sugar Chocolate Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Low Sugar Chocolate Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Low Sugar Chocolate Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Low Sugar Chocolate Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Low Sugar Chocolate Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Low Sugar Chocolate Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Low Sugar Chocolate Revenue billion Forecast, by Type 2020 & 2033

- Table 34: Global Low Sugar Chocolate Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Low Sugar Chocolate Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Low Sugar Chocolate Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Low Sugar Chocolate Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Low Sugar Chocolate Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Low Sugar Chocolate Revenue billion Forecast, by Type 2020 & 2033

- Table 58: Global Low Sugar Chocolate Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Low Sugar Chocolate Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Low Sugar Chocolate Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Low Sugar Chocolate Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Low Sugar Chocolate Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Low Sugar Chocolate Revenue billion Forecast, by Type 2020 & 2033

- Table 76: Global Low Sugar Chocolate Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Low Sugar Chocolate Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Low Sugar Chocolate Volume K Forecast, by Country 2020 & 2033

- Table 79: China Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Low Sugar Chocolate Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Low Sugar Chocolate Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Low Sugar Chocolate?

The projected CAGR is approximately 3.4%.

2. Which companies are prominent players in the Low Sugar Chocolate?

Key companies in the market include Barry Callebaut, Stella Bernrain, Lindt, Chocolat Frey, Chocolats Halba, Läderach, Felchlin, Pfister Chocolatier, Favarger, Camillebloch, Alprose, Gysi, Cailler (Nestle), Villars, Mondelēz International, Maestrani Schweizer Schokoladen, Confiserie Sprüngli.

3. What are the main segments of the Low Sugar Chocolate?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 28.74 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Low Sugar Chocolate," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Low Sugar Chocolate report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Low Sugar Chocolate?

To stay informed about further developments, trends, and reports in the Low Sugar Chocolate, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence