Key Insights

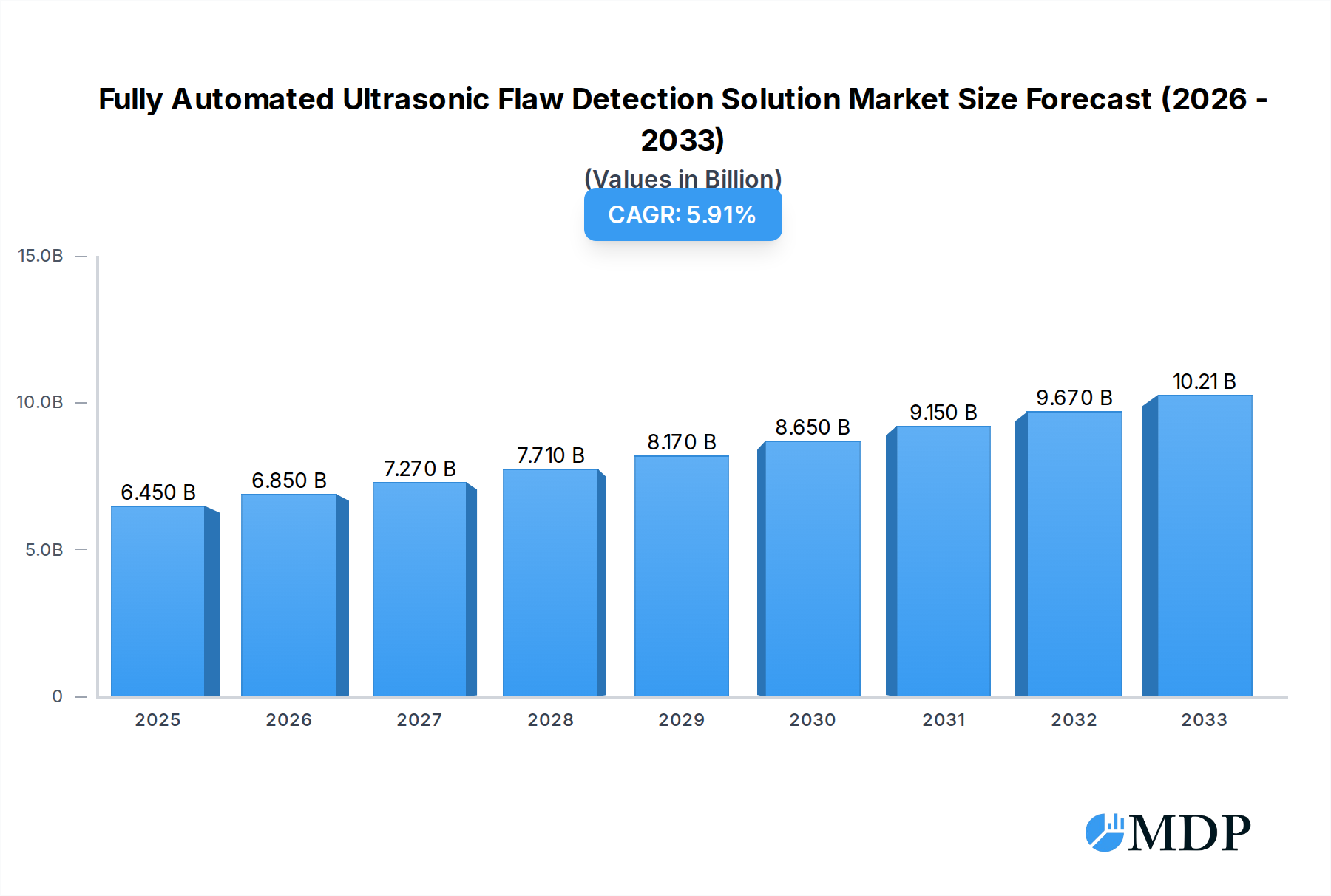

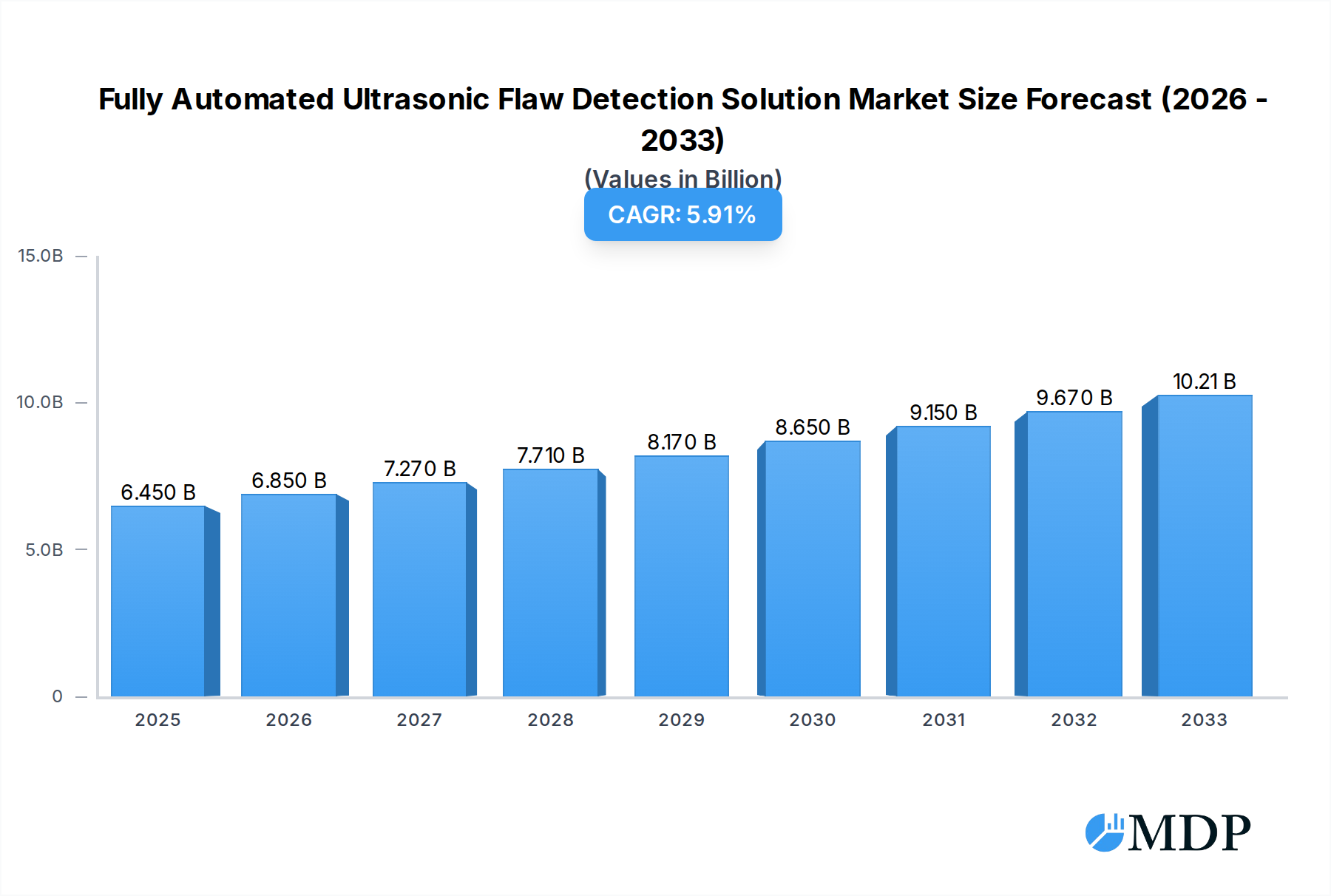

The Fully Automated Ultrasonic Flaw Detection Solution market is poised for significant expansion, with an estimated market size of $6.45 billion in 2025. This robust growth trajectory is underpinned by a projected Compound Annual Growth Rate (CAGR) of 6.29% throughout the forecast period, indicating a sustained and healthy increase in market value. The increasing demand for enhanced safety regulations, coupled with the need for improved efficiency and accuracy in quality control processes across various industries, serves as a primary catalyst for this market's ascent. The automotive sector, in particular, is a key driver, with stringent standards for vehicle integrity necessitating advanced flaw detection methods. Furthermore, the aerospace industry's relentless pursuit of lightweight yet robust materials, coupled with the critical safety requirements, fuels the adoption of automated ultrasonic testing. As manufacturing processes become more complex and the tolerance for defects diminishes, the inherent precision and speed offered by fully automated solutions become indispensable.

Fully Automated Ultrasonic Flaw Detection Solution Market Size (In Billion)

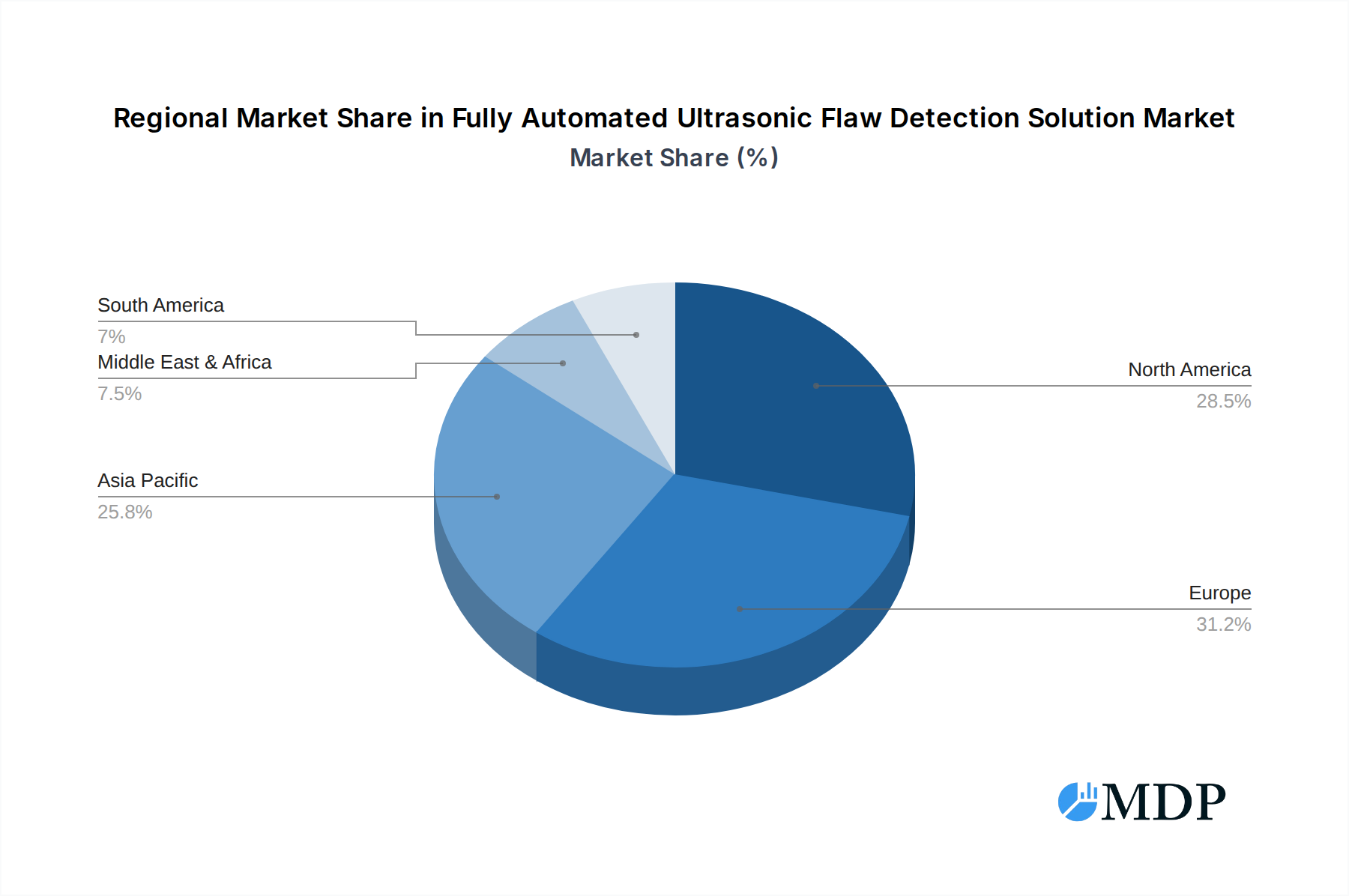

The market is characterized by a dynamic interplay of technological advancements and evolving industry needs. While the adoption of phased array ultrasonic testing services and time-of-flight diffraction services are key segments, the overarching trend is towards greater automation and integration of these technologies. This automation not only minimizes human error but also significantly reduces inspection times, thereby boosting overall productivity. However, the market is not without its challenges. High initial investment costs for sophisticated automated systems can act as a restraint, particularly for smaller enterprises. Additionally, the need for skilled personnel to operate and maintain these advanced systems, along with the requirement for standardization across different applications, are areas that warrant continued attention. Despite these hurdles, the compelling benefits of enhanced reliability, cost-effectiveness in the long run, and improved safety outcomes are expected to propel the Fully Automated Ultrasonic Flaw Detection Solution market to new heights, with substantial opportunities in regions like North America and Europe, followed by Asia Pacific.

Fully Automated Ultrasonic Flaw Detection Solution Company Market Share

Fully Automated Ultrasonic Flaw Detection Solution Market Dynamics & Concentration

The fully automated ultrasonic flaw detection solution market exhibits a moderately concentrated landscape, with key players like Applus+, Ashtead Technology, Bureau Veritas, FORCE Technology, GE Measurement and Control, MME Group, Olympus, Sentinel Integrity Solutions, SHAWCOR, and TÜV Rheinland holding significant market share. Innovation drivers are predominantly centered on enhanced detection accuracy, reduced inspection times, and the integration of artificial intelligence and machine learning for predictive maintenance insights. Regulatory frameworks, particularly in sectors like aerospace and oil & gas, are increasingly mandating stringent quality control, thus fueling the demand for automated solutions. While direct product substitutes are limited, advancements in other non-destructive testing (NDT) methods pose indirect competition. End-user trends lean towards a preference for real-time data, improved safety standards, and cost optimization through reduced downtime. Merger and acquisition (M&A) activities are expected to shape market concentration further, with an estimated 7 M&A deals anticipated during the forecast period of 2025–2033, aimed at consolidating market presence and expanding technological portfolios. Market share distribution is dynamic, with leading companies vying for dominance through strategic partnerships and advanced technological offerings.

Fully Automated Ultrasonic Flaw Detection Solution Industry Trends & Analysis

The fully automated ultrasonic flaw detection solution market is poised for robust growth, driven by an escalating demand for advanced NDT technologies across critical industries. The projected Compound Annual Growth Rate (CAGR) for the market is estimated at 8.5 billion during the forecast period of 2025–2033. This growth is propelled by several key factors. Firstly, the increasing emphasis on safety and reliability in sectors such as Automobiles, Airplanes, and Ships necessitates more efficient and accurate flaw detection systems. Traditional manual inspection methods are proving inadequate to meet the stringent quality standards and high throughput requirements of modern manufacturing and infrastructure maintenance. Automated ultrasonic systems offer unparalleled precision, repeatability, and the ability to inspect complex geometries, thereby reducing the risk of failures and enhancing operational safety.

Secondly, technological disruptions are playing a pivotal role. The integration of artificial intelligence (AI) and machine learning (ML) algorithms is transforming the way ultrasonic data is analyzed. These advanced technologies enable faster and more accurate interpretation of flaw signals, reducing human error and allowing for predictive maintenance strategies. Companies are investing heavily in research and development to create smarter, more autonomous inspection systems that can identify even minute defects and predict potential failures before they occur. This shift from reactive to proactive maintenance significantly reduces downtime and operational costs for end-users, making automated solutions highly attractive.

Thirdly, evolving consumer preferences, particularly within the industrial sectors, are driving the adoption of these sophisticated technologies. Industries are increasingly seeking solutions that not only ensure product integrity but also provide comprehensive data analytics and reporting capabilities. The demand for real-time monitoring and remote inspection is also on the rise, facilitated by the connectivity and data-handling capabilities of automated ultrasonic systems. This allows for continuous assessment of asset health, even in hazardous or inaccessible environments.

The competitive dynamics within the market are characterized by intense innovation and strategic collaborations. Companies are differentiating themselves through the development of specialized probes, advanced software platforms, and integrated inspection workflows. The market penetration of fully automated solutions is expected to rise significantly, driven by the demonstrable return on investment and the increasing need for efficient, data-driven inspection processes. The historical period (2019–2024) has laid a strong foundation, with initial adoption driven by high-risk industries, and the base year of 2025 marks a significant inflection point for widespread market expansion. The estimated market size for 2025 is valued at approximately 15 billion.

Leading Markets & Segments in Fully Automated Ultrasonic Flaw Detection Solution

The global market for Fully Automated Ultrasonic Flaw Detection Solutions is experiencing significant growth, with particular dominance observed in regions and segments that prioritize advanced manufacturing, stringent safety regulations, and extensive infrastructure development.

Dominant Region: North America and Europe currently lead the market, driven by their advanced aerospace and automotive industries, respectively. The stringent regulatory environments in these regions, coupled with a high adoption rate of cutting-edge technologies, create a fertile ground for automated NDT solutions. For instance, in the Automobiles segment, the increasing complexity of vehicle components and the push for enhanced safety features necessitate highly accurate and efficient flaw detection. The automotive industry in North America, with its substantial manufacturing base and focus on electric vehicle (EV) development, is a key driver. Similarly, European nations’ commitment to industrial innovation and adherence to rigorous quality standards in their automotive and aerospace sectors contribute to this regional dominance. The United States, in particular, benefits from substantial investment in infrastructure modernization and a strong aerospace manufacturing ecosystem.

Dominant Segments by Application:

- Airplanes: This segment is a major consumer due to the critical safety requirements and complex material structures in aerospace. The continuous need for rigorous inspection of aircraft components throughout their lifecycle, from manufacturing to in-service maintenance, drives the demand for automated ultrasonic solutions. The global commercial aviation fleet is projected to expand significantly, further bolstering demand.

- Automobiles: As automotive manufacturing becomes more automated and complex, especially with the rise of electric vehicles and advanced driver-assistance systems (ADAS), the need for precise and rapid flaw detection in components like battery packs, chassis, and structural elements is paramount. The trend towards lighter, stronger materials also necessitates advanced inspection techniques.

- Ships: The maritime industry, with its large-scale structures and demanding operational environments, also presents a substantial market. Automated ultrasonic testing is crucial for inspecting welds, hull integrity, and critical components on vessels, ensuring safety and longevity. The growing global trade and the need for efficient shipping operations indirectly fuel this demand.

Dominant Segments by Type:

- Phased Array Ultrasonic Testing (PAUT) Services: PAUT is a cornerstone of automated ultrasonic flaw detection. Its ability to steer ultrasonic beams electronically allows for faster scanning of complex geometries and the detection of smaller defects with higher resolution. The widespread adoption of PAUT technology in critical industries for its versatility and precision makes it the leading segment within automated solutions.

- Time of Flight Diffraction (TOFD) Services: TOFD is highly effective for detecting and sizing flaws, particularly cracks, in welds. Its accuracy and reliability in characterizing defect depth make it an indispensable tool in industries where weld integrity is paramount, such as shipbuilding and pressure vessel manufacturing.

The economic policies supporting advanced manufacturing, significant investments in infrastructure projects worldwide, and the continuous drive for enhanced product reliability and safety across these sectors are key enablers for the dominance of these markets and segments. The base year of 2025 represents a strong point for these segments, with significant market penetration and anticipated growth. The estimated market value for PAUT services within this sector is approximately 7 billion.

Fully Automated Ultrasonic Flaw Detection Solution Product Developments

Recent product developments in fully automated ultrasonic flaw detection solutions are characterized by a significant leap in AI integration, enhanced portability, and multi-modal data fusion. Innovations like smart probes with embedded processing capabilities are reducing inspection times and improving data accuracy. The development of cloud-based platforms allows for remote monitoring and data analysis, enabling predictive maintenance insights and real-time decision-making. These advancements offer competitive advantages by providing faster, more reliable, and cost-effective inspection solutions, aligning with market demands for efficiency and safety in critical applications.

Key Drivers of Fully Automated Ultrasonic Flaw Detection Solution Growth

The growth of the Fully Automated Ultrasonic Flaw Detection Solution market is primarily propelled by the escalating demand for enhanced safety and reliability across industries like aerospace and automotive. Technological advancements, particularly the integration of AI and machine learning for faster and more accurate defect detection and analysis, are significant growth accelerators. Stringent regulatory mandates for quality control and the need to reduce operational downtime and maintenance costs through predictive analytics also contribute substantially to market expansion. The increasing complexity of manufactured components further necessitates sophisticated automated inspection capabilities.

Challenges in the Fully Automated Ultrasonic Flaw Detection Solution Market

Despite robust growth, the Fully Automated Ultrasonic Flaw Detection Solution market faces several challenges. High initial investment costs for advanced automated systems can be a barrier for small and medium-sized enterprises. The need for skilled personnel to operate and maintain these sophisticated technologies presents a talent gap. Furthermore, standardization and interoperability issues between different vendor systems can hinder widespread adoption. Cybersecurity concerns related to data handling in cloud-based solutions also require careful consideration, potentially impacting market penetration.

Emerging Opportunities in Fully Automated Ultrasonic Flaw Detection Solution

Emerging opportunities in the Fully Automated Ultrasonic Flaw Detection Solution market lie in the expanding applications within the renewable energy sector, particularly in wind turbine blade inspection and infrastructure integrity monitoring. The growing trend towards Industry 4.0 and smart manufacturing environments presents a significant catalyst for integrated automated inspection solutions. Strategic partnerships between NDT equipment manufacturers and software developers to create comprehensive, end-to-end solutions will unlock new market potential. Furthermore, the development of miniaturized and more robust systems for inspecting complex and hard-to-reach areas will open up new application frontiers.

Leading Players in the Fully Automated Ultrasonic Flaw Detection Solution Sector

- Applus+

- Ashtead Technology

- Bureau Veritas

- FORCE Technology

- GE Measurement and Control

- MME Group

- Olympus

- Sentinel Integrity Solutions

- SHAWCOR

- TÜV Rheinland

Key Milestones in Fully Automated Ultrasonic Flaw Detection Solution Industry

- 2019: Increased adoption of AI algorithms for data analysis in ultrasonic testing.

- 2020: Introduction of portable and highly integrated phased array ultrasonic systems.

- 2021: Expansion of cloud-based platforms for remote monitoring and data management.

- 2022: Development of advanced probes for inspecting composite materials in aerospace.

- 2023: Focus on AI-driven predictive maintenance solutions becoming mainstream.

- 2024: Enhanced sensor technologies for improved flaw characterization and sizing.

- 2025: Significant market growth driven by widespread adoption in automotive and aerospace.

- 2026-2033: Continued innovation in AI, robotics integration, and expansion into new industry verticals.

Strategic Outlook for Fully Automated Ultrasonic Flaw Detection Solution Market

The strategic outlook for the Fully Automated Ultrasonic Flaw Detection Solution market is exceptionally promising, driven by an increasing imperative for industrial safety, operational efficiency, and quality assurance. The market is set to expand significantly as automation becomes a standard in manufacturing and maintenance. Key growth accelerators will include the continued integration of advanced AI and ML for smarter, more autonomous inspection, and the development of IoT-enabled solutions for real-time monitoring and data analytics. Strategic partnerships and M&A activities are expected to consolidate the market and foster innovation, paving the way for more comprehensive and integrated NDT solutions across diverse industries.

Fully Automated Ultrasonic Flaw Detection Solution Segmentation

-

1. Application

- 1.1. Automobiles

- 1.2. Airplanes

- 1.3. Ships

- 1.4. Others

-

2. Types

- 2.1. Phased Array Ultrasonic Testing Services

- 2.2. Time of Flight Diffraction Services

Fully Automated Ultrasonic Flaw Detection Solution Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fully Automated Ultrasonic Flaw Detection Solution Regional Market Share

Geographic Coverage of Fully Automated Ultrasonic Flaw Detection Solution

Fully Automated Ultrasonic Flaw Detection Solution REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.29% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Fully Automated Ultrasonic Flaw Detection Solution Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automobiles

- 5.1.2. Airplanes

- 5.1.3. Ships

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Phased Array Ultrasonic Testing Services

- 5.2.2. Time of Flight Diffraction Services

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Fully Automated Ultrasonic Flaw Detection Solution Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automobiles

- 6.1.2. Airplanes

- 6.1.3. Ships

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Phased Array Ultrasonic Testing Services

- 6.2.2. Time of Flight Diffraction Services

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Fully Automated Ultrasonic Flaw Detection Solution Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automobiles

- 7.1.2. Airplanes

- 7.1.3. Ships

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Phased Array Ultrasonic Testing Services

- 7.2.2. Time of Flight Diffraction Services

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Fully Automated Ultrasonic Flaw Detection Solution Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automobiles

- 8.1.2. Airplanes

- 8.1.3. Ships

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Phased Array Ultrasonic Testing Services

- 8.2.2. Time of Flight Diffraction Services

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Fully Automated Ultrasonic Flaw Detection Solution Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automobiles

- 9.1.2. Airplanes

- 9.1.3. Ships

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Phased Array Ultrasonic Testing Services

- 9.2.2. Time of Flight Diffraction Services

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Fully Automated Ultrasonic Flaw Detection Solution Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automobiles

- 10.1.2. Airplanes

- 10.1.3. Ships

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Phased Array Ultrasonic Testing Services

- 10.2.2. Time of Flight Diffraction Services

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Applus+

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Ashtead Technology

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Bureau Veritas

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 FORCE Technology

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 GE Measurement and Control

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 MME Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Olympus

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sentinel Integrity Solutions

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 SHAWCOR

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 TÜV Rheinland

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Applus+

List of Figures

- Figure 1: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Fully Automated Ultrasonic Flaw Detection Solution Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Fully Automated Ultrasonic Flaw Detection Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Fully Automated Ultrasonic Flaw Detection Solution Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fully Automated Ultrasonic Flaw Detection Solution?

The projected CAGR is approximately 6.29%.

2. Which companies are prominent players in the Fully Automated Ultrasonic Flaw Detection Solution?

Key companies in the market include Applus+, Ashtead Technology, Bureau Veritas, FORCE Technology, GE Measurement and Control, MME Group, Olympus, Sentinel Integrity Solutions, SHAWCOR, TÜV Rheinland.

3. What are the main segments of the Fully Automated Ultrasonic Flaw Detection Solution?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.45 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fully Automated Ultrasonic Flaw Detection Solution," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fully Automated Ultrasonic Flaw Detection Solution report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fully Automated Ultrasonic Flaw Detection Solution?

To stay informed about further developments, trends, and reports in the Fully Automated Ultrasonic Flaw Detection Solution, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence