Key Insights

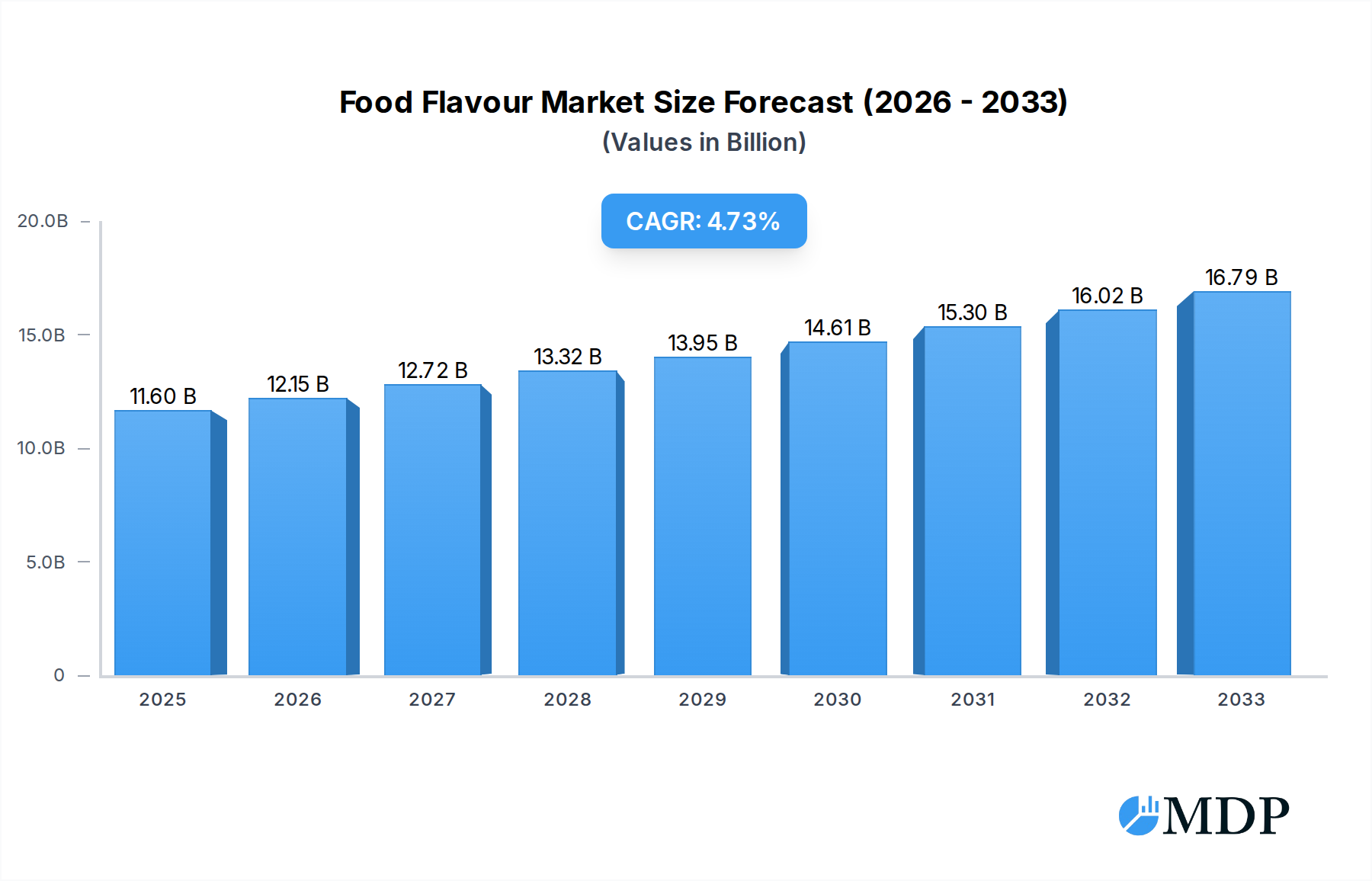

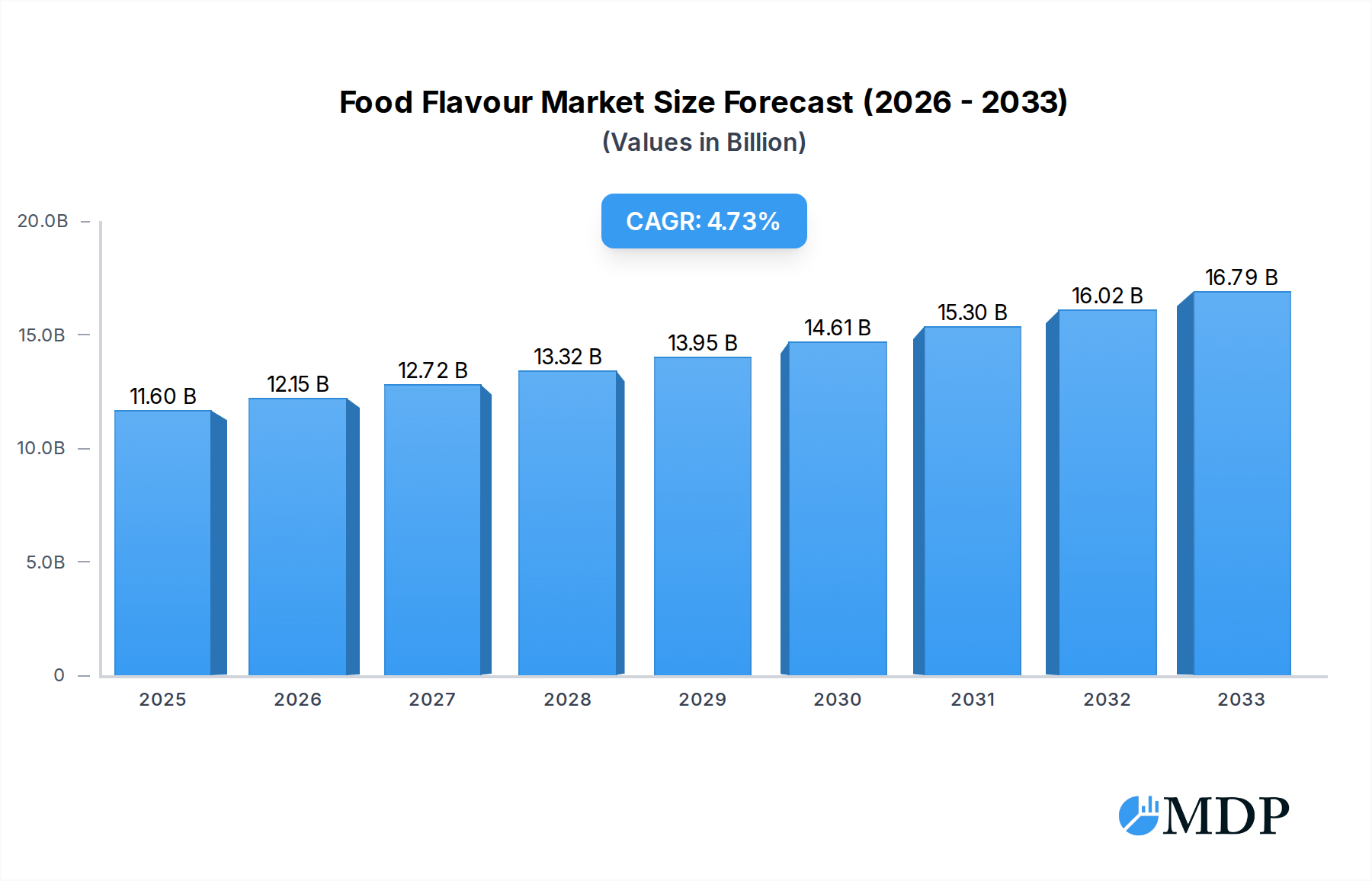

The global food flavour market is poised for significant expansion, with an estimated USD 11.6 billion valuation in 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 4.7% projected over the forecast period of 2025-2033. The increasing consumer demand for innovative and diverse taste experiences is a primary driver, pushing manufacturers to develop novel flavour profiles that cater to evolving palates. Furthermore, a growing awareness of natural ingredients and a preference for healthier, clean-label products are steering the market towards natural food flavours, although synthetic options continue to hold a substantial share due to cost-effectiveness and versatility. The expanding food and beverage industry, particularly in emerging economies, coupled with the growing processed food sector, directly fuels the demand for a wide array of flavourings.

Food Flavour Market Size (In Billion)

The market's trajectory is also influenced by prevailing consumer trends, such as the rise of convenience foods, the demand for exotic and ethnic flavours, and the incorporation of flavours in functional foods and beverages aimed at specific health benefits. However, certain factors, including stringent regulatory frameworks concerning food additives and the fluctuating prices of raw materials, particularly for natural flavour compounds, present potential restraints. Nevertheless, technological advancements in flavour encapsulation and extraction techniques, alongside strategic collaborations and acquisitions among key players, are expected to mitigate these challenges and propel sustained market development. The competitive landscape is dominated by major global players, indicating a mature yet dynamic market characterized by innovation and strategic market penetration.

Food Flavour Company Market Share

Food Flavour Market Research Report: Unlocking Billion-Dollar Opportunities

This comprehensive report delves into the global Food Flavour market, a dynamic and rapidly evolving industry projected to reach billions in value. With a deep dive into market dynamics, trends, leading segments, and key players, this analysis provides invaluable insights for industry stakeholders, from manufacturers and ingredient suppliers to investors and policymakers. The study spans from 2019–2033, with a base year of 2025 and an estimated year also of 2025, covering a detailed historical period of 2019–2024 and a robust forecast period of 2025–2033. This report is your definitive guide to navigating the complexities and capitalizing on the immense opportunities within the food flavour sector.

Food Flavour Market Dynamics & Concentration

The global Food Flavour market exhibits a moderate to high concentration, with a significant portion of market share held by a few dominant players. Key innovation drivers include the ever-growing consumer demand for novel taste experiences, the increasing preference for natural and clean-label ingredients, and advancements in extraction and synthesis technologies. Regulatory frameworks, such as those governed by the FDA and EFSA, play a crucial role in shaping product development and market access, ensuring consumer safety and ingredient authenticity. Product substitutes, primarily arising from the "free-from" trend (e.g., sugar-free, artificial flavour-free alternatives), are increasingly influencing ingredient choices. End-user trends are strongly leaning towards healthier, sustainable, and ethically sourced food products, directly impacting flavour ingredient selection. Mergers and acquisitions (M&A) activities have been a strategic tool for market expansion and portfolio diversification. In the historical period 2019–2024, notable M&A deals across the sector reached an estimated count of xx billion in value, signifying a robust consolidation phase. Major companies like Givaudan and Firmenich have consistently pursued strategic acquisitions to bolster their product offerings and geographic reach. The market share of the top five players in 2025 is estimated to be xx billion, indicating a significant but not entirely monopolistic landscape.

Food Flavour Industry Trends & Analysis

The global Food Flavour market is experiencing robust growth, propelled by several interconnected trends that are reshaping consumer preferences and industry practices. A significant CAGR of xx% is projected over the forecast period 2025–2033, demonstrating sustained expansion. One of the primary market growth drivers is the escalating demand for natural and organic food flavours, fueled by consumer awareness regarding health and wellness. This trend is leading to a substantial shift away from synthetic additives towards plant-derived and fermentation-based flavour solutions. Technological disruptions are also playing a pivotal role. Advancements in biotechnological processes, such as precision fermentation and enzymatic synthesis, are enabling the cost-effective production of complex and desirable natural flavour compounds. This innovation not only expands the palette of available flavours but also offers more sustainable alternatives to traditional extraction methods. Consumer preferences are increasingly sophisticated, with a growing appetite for exotic, ethnic, and artisanal flavour profiles. The "experiential dining" trend, even within home consumption, is driving demand for authentic and immersive taste experiences. Furthermore, the "clean label" movement continues to gain traction, pushing manufacturers to simplify ingredient lists and avoid artificial colours, preservatives, and flavours. Competitive dynamics are characterized by intense R&D efforts, strategic partnerships, and a growing emphasis on sustainability and transparency throughout the supply chain. Market penetration of natural food flavours is estimated to reach xx% by 2025, a testament to their growing consumer acceptance. The impact of these trends is creating a fertile ground for both established multinational corporations and agile niche players to innovate and capture market share. The ongoing evolution of food processing techniques and packaging technologies also influences flavour stability and delivery, necessitating continuous adaptation from flavour manufacturers.

Leading Markets & Segments in Food Flavour

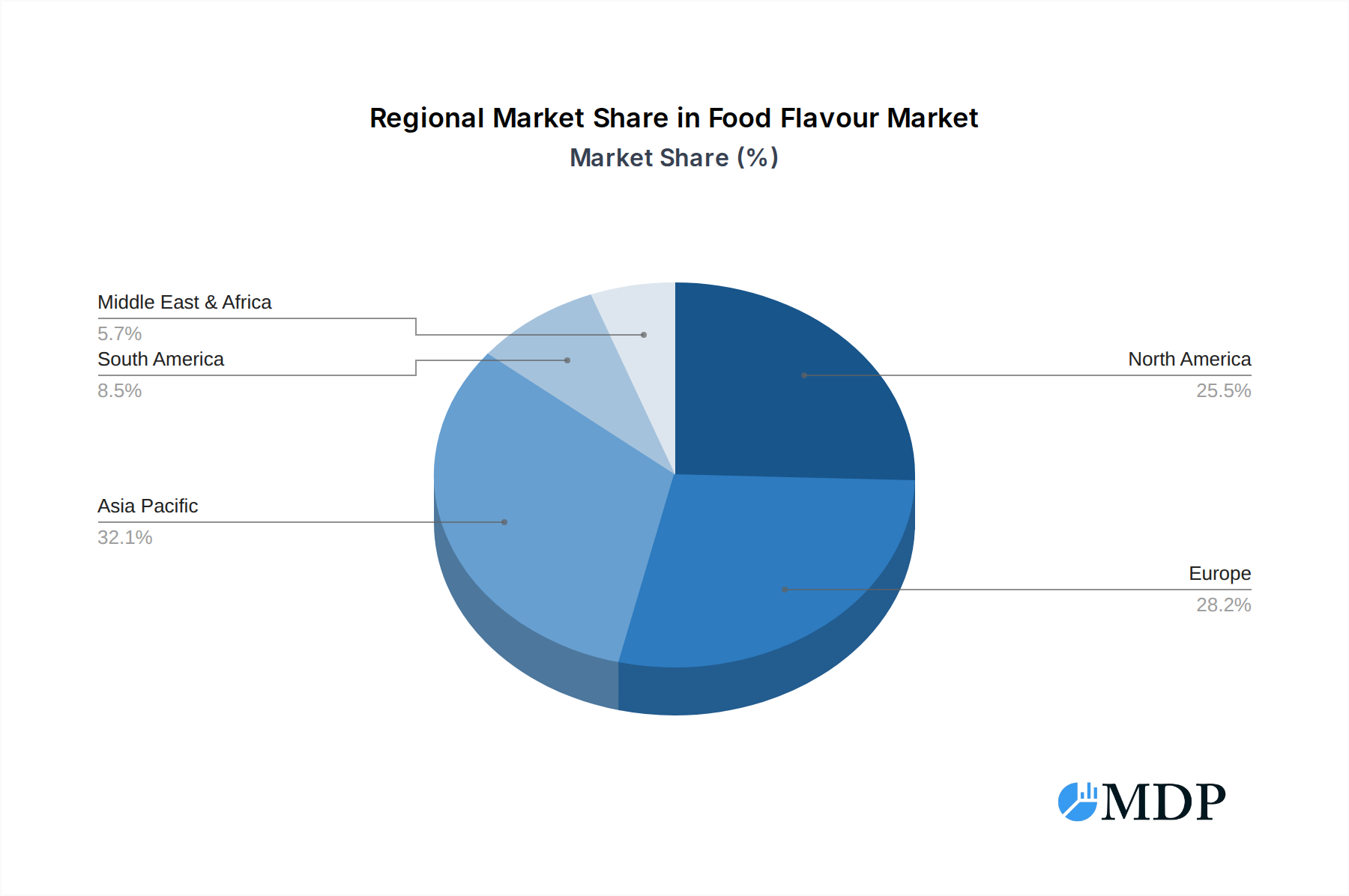

The global Food Flavour market's dominance is influenced by regional economic strength, regulatory landscapes, and consumer demographics. North America and Europe currently lead the market, driven by high disposable incomes, a strong preference for processed foods, and a mature consumer base that actively seeks innovative flavour experiences. However, the Asia Pacific region is emerging as a powerhouse of growth, propelled by rapid urbanization, a burgeoning middle class, and an increasing adoption of Western dietary habits, which often incorporate a wider variety of processed foods and beverages. Within the application segment, Beverage currently holds the largest market share, estimated at xx billion in 2025. This dominance is attributed to the widespread use of flavourings in carbonated drinks, juices, dairy beverages, and alcoholic beverages, where taste is a primary purchase driver. The Snacks segment also commands a significant market share, estimated at xx billion in 2025, driven by the popularity of savory and sweet snacks that rely heavily on appealing flavour profiles.

Dominance Drivers in Beverage:

- Economic Policies: Favorable trade policies and industrial growth in key Asia Pacific economies are boosting beverage production and consumption.

- Infrastructure: Well-developed distribution networks ensure efficient product availability across vast geographic areas.

- Consumer Preferences: A constant demand for novel and refreshing taste profiles in an increasingly competitive beverage market.

- Innovation: Continuous introduction of new beverage categories and flavour combinations.

Dominance Drivers in Snacks:

- Consumer Lifestyles: Busy lifestyles and the demand for convenient, on-the-go food options fuel snack consumption.

- Product Diversification: The vast array of snack types, from potato chips to extruded snacks and confectionery, allows for extensive flavour application.

- Flavor Innovation: The snack industry thrives on introducing bold and unique flavour profiles to capture consumer attention.

- Affordability: Snacks often represent an accessible indulgence for a broad consumer base.

In terms of flavour type, Natural Food Flavour is experiencing a surge in demand and is projected to outpace the growth of synthetic counterparts. The market share for natural food flavours is estimated to reach xx% by 2025, with a projected market value of xx billion. This shift is primarily driven by stringent government regulations on artificial additives and a growing consumer consciousness regarding health and well-being. The Desserts and Dairy Products segments are also significant contributors to market growth, with increasing demand for premium and indulgence-oriented flavourings.

Food Flavour Product Developments

Recent product developments in the Food Flavour market are characterized by a strong emphasis on natural sourcing, sustainability, and enhanced sensory experiences. Companies are investing heavily in proprietary extraction technologies to isolate rare and potent natural flavour compounds, leading to innovations in fruit, botanical, and savory profiles. The demand for plant-based flavours is also driving research into novel ingredients and flavour combinations that mimic traditional animal-derived tastes. These advancements aim to provide food manufacturers with clean-label solutions that do not compromise on taste or performance. Competitive advantages are being built through proprietary ingredient formulations, advanced encapsulation techniques for improved flavour stability and controlled release, and certifications that guarantee ethical sourcing and environmental responsibility. For instance, the introduction of specific umami-rich natural extracts and the development of low-calorie, high-impact sweetness enhancers are key trends.

Key Drivers of Food Flavour Growth

The Food Flavour market's growth is underpinned by a confluence of powerful drivers. Technologically, advancements in biotechnology and extraction methods are unlocking new possibilities for natural and authentic flavour creation, making previously inaccessible or costly flavour compounds commercially viable. Economically, rising disposable incomes in emerging economies are fueling increased consumption of processed foods and beverages, directly translating to higher demand for flavourings. The growing global population also contributes significantly to this expanding market. Regulatory shifts, such as the increasing scrutiny and restriction of artificial additives, are creating a strong tailwind for natural and clean-label flavour solutions, encouraging manufacturers to reformulate their products. For example, the EU's ban on certain artificial colours has spurred innovation in natural colouring and flavouring solutions.

Challenges in the Food Flavour Market

Despite its robust growth, the Food Flavour market faces several significant challenges. Stringent and evolving regulatory frameworks across different regions can create complex compliance hurdles for global manufacturers, requiring extensive testing and documentation. Supply chain volatility, particularly for natural ingredients susceptible to climate change and geopolitical factors, can lead to price fluctuations and availability issues. Competitive pressures are immense, with a fragmented market and the constant need for innovation to stay ahead of consumer trends. The cost of developing and sourcing natural ingredients can also be higher than synthetic alternatives, impacting profit margins. Quantifiable impacts include an estimated xx% increase in R&D expenditure needed to meet regulatory demands and secure sustainable natural ingredient sourcing.

Emerging Opportunities in Food Flavour

Catalysts driving long-term growth in the Food Flavour market are numerous and exciting. Technological breakthroughs in precision fermentation are poised to revolutionize the production of complex natural flavours, offering scalability and reduced environmental impact. Strategic partnerships between flavour houses and food manufacturers are becoming crucial for co-creating innovative products and gaining early market access. The expanding global middle class, particularly in developing nations, presents a vast untapped market for diverse and appealing flavour solutions. Furthermore, the growing interest in personalized nutrition and functional foods creates opportunities for specialized flavour formulations that complement health benefits. The increasing demand for plant-based and meat-alternative products is also a significant opportunity for developing realistic and satisfying flavour profiles.

Leading Players in the Food Flavour Sector

- Givaudan

- Firmenich

- Symrise

- IFF (International Flavors & Fragrances)

- Robertet

- Frutarom (now part of IFF)

- Sensient Technologies Corporation

- WILD Flavors (now part of Archer Daniels Midland Company)

- T. Hasegawa Co., Ltd.

- Takasago International Corporation

- Mane

- Huabao Flavours & Fragrances Co., Ltd.

- Boton Corporation

- Zhonghua Chemical

- SinoLion (part of WACKER Chemie AG)

Key Milestones in Food Flavour Industry

- 2019: Increased investment in natural flavour extraction technologies by leading players.

- 2020: Growing consumer demand for plant-based alternatives spurs innovation in savory flavours.

- 2021: Enhanced regulatory scrutiny on artificial additives in major markets.

- 2022: Significant M&A activity as larger companies acquire specialized natural flavour ingredient providers.

- 2023: Advancements in precision fermentation technologies begin to offer scalable natural flavour solutions.

- 2024: Growing emphasis on sustainability and ethical sourcing throughout the flavour supply chain.

Strategic Outlook for Food Flavour Market

The strategic outlook for the Food Flavour market is overwhelmingly positive, characterized by sustained growth fueled by evolving consumer preferences and technological advancements. Key growth accelerators include the continued shift towards natural and clean-label ingredients, the expansion of plant-based food markets, and the increasing demand for exotic and artisanal flavour profiles. Companies that focus on sustainable sourcing, invest in innovative biotechnological solutions, and forge strong strategic partnerships will be well-positioned to capitalize on future market potential. The exploration of novel flavour delivery systems and the integration of flavour development with functional food attributes also represent significant strategic opportunities for differentiation and market leadership.

Food Flavour Segmentation

-

1. Application

- 1.1. Snacks

- 1.2. Beverage

- 1.3. Dairy Products

- 1.4. Desserts

- 1.5. Others

-

2. Type

- 2.1. Synthetic Food Flavour

- 2.2. Natural Food Flavour

Food Flavour Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Food Flavour Regional Market Share

Geographic Coverage of Food Flavour

Food Flavour REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Snacks

- 5.1.2. Beverage

- 5.1.3. Dairy Products

- 5.1.4. Desserts

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Synthetic Food Flavour

- 5.2.2. Natural Food Flavour

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Food Flavour Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Snacks

- 6.1.2. Beverage

- 6.1.3. Dairy Products

- 6.1.4. Desserts

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Synthetic Food Flavour

- 6.2.2. Natural Food Flavour

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Food Flavour Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Snacks

- 7.1.2. Beverage

- 7.1.3. Dairy Products

- 7.1.4. Desserts

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Synthetic Food Flavour

- 7.2.2. Natural Food Flavour

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Food Flavour Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Snacks

- 8.1.2. Beverage

- 8.1.3. Dairy Products

- 8.1.4. Desserts

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Synthetic Food Flavour

- 8.2.2. Natural Food Flavour

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Food Flavour Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Snacks

- 9.1.2. Beverage

- 9.1.3. Dairy Products

- 9.1.4. Desserts

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Synthetic Food Flavour

- 9.2.2. Natural Food Flavour

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Food Flavour Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Snacks

- 10.1.2. Beverage

- 10.1.3. Dairy Products

- 10.1.4. Desserts

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Synthetic Food Flavour

- 10.2.2. Natural Food Flavour

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Food Flavour Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Snacks

- 11.1.2. Beverage

- 11.1.3. Dairy Products

- 11.1.4. Desserts

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Synthetic Food Flavour

- 11.2.2. Natural Food Flavour

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Givaudan

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Firmenich

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Symrise

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 IFF

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Roberte

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Frutarom

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Sensien

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 WILD Flavors

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 T-Hasegawa

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Takasago Inter

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Mane

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Huabao Flavours & Fragrances

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Boton

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Zhonghua Chemical

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Givaudan

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Food Flavour Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Food Flavour Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Food Flavour Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Food Flavour Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Food Flavour Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Food Flavour Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Food Flavour Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Food Flavour Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Food Flavour Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Food Flavour Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Food Flavour Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Food Flavour Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Food Flavour Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Food Flavour Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Food Flavour Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Food Flavour Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Food Flavour Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Food Flavour Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Food Flavour Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Food Flavour Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Food Flavour Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Food Flavour Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Food Flavour Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Food Flavour Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Food Flavour Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Food Flavour Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Food Flavour Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Food Flavour Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Food Flavour Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Food Flavour Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Food Flavour Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Food Flavour Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Food Flavour Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Food Flavour Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Food Flavour Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Food Flavour Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Food Flavour Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Food Flavour Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Food Flavour Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Food Flavour Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Food Flavour Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Food Flavour Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Food Flavour Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Food Flavour Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Food Flavour Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Food Flavour Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Food Flavour Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Food Flavour Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Food Flavour Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Food Flavour Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Flavour?

The projected CAGR is approximately 4.7%.

2. Which companies are prominent players in the Food Flavour?

Key companies in the market include Givaudan, Firmenich, Symrise, IFF, Roberte, Frutarom, Sensien, WILD Flavors, T-Hasegawa, Takasago Inter, Mane, Huabao Flavours & Fragrances, Boton, Zhonghua Chemical.

3. What are the main segments of the Food Flavour?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.6 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Food Flavour," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Food Flavour report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Food Flavour?

To stay informed about further developments, trends, and reports in the Food Flavour, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence