Key Insights

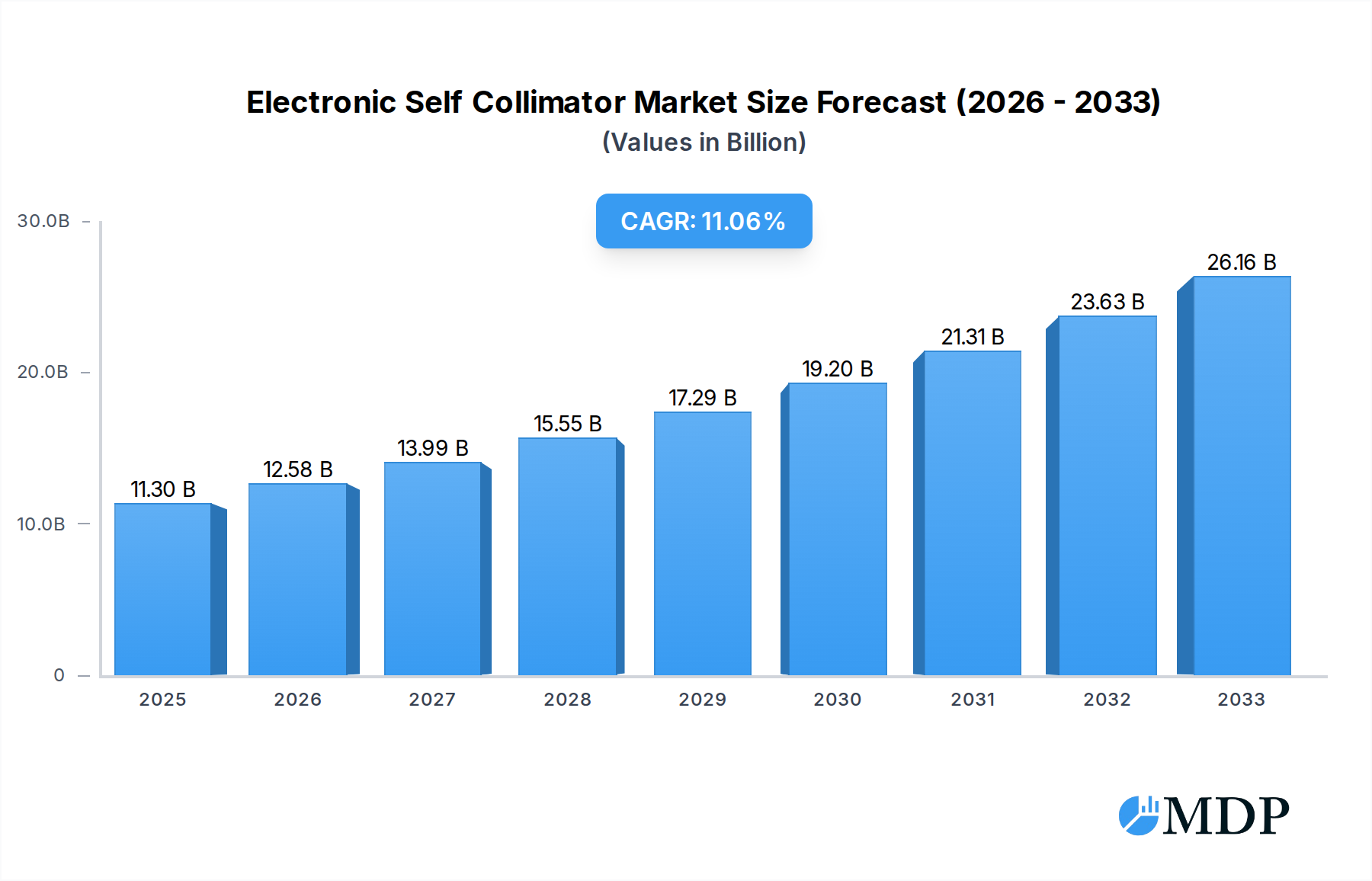

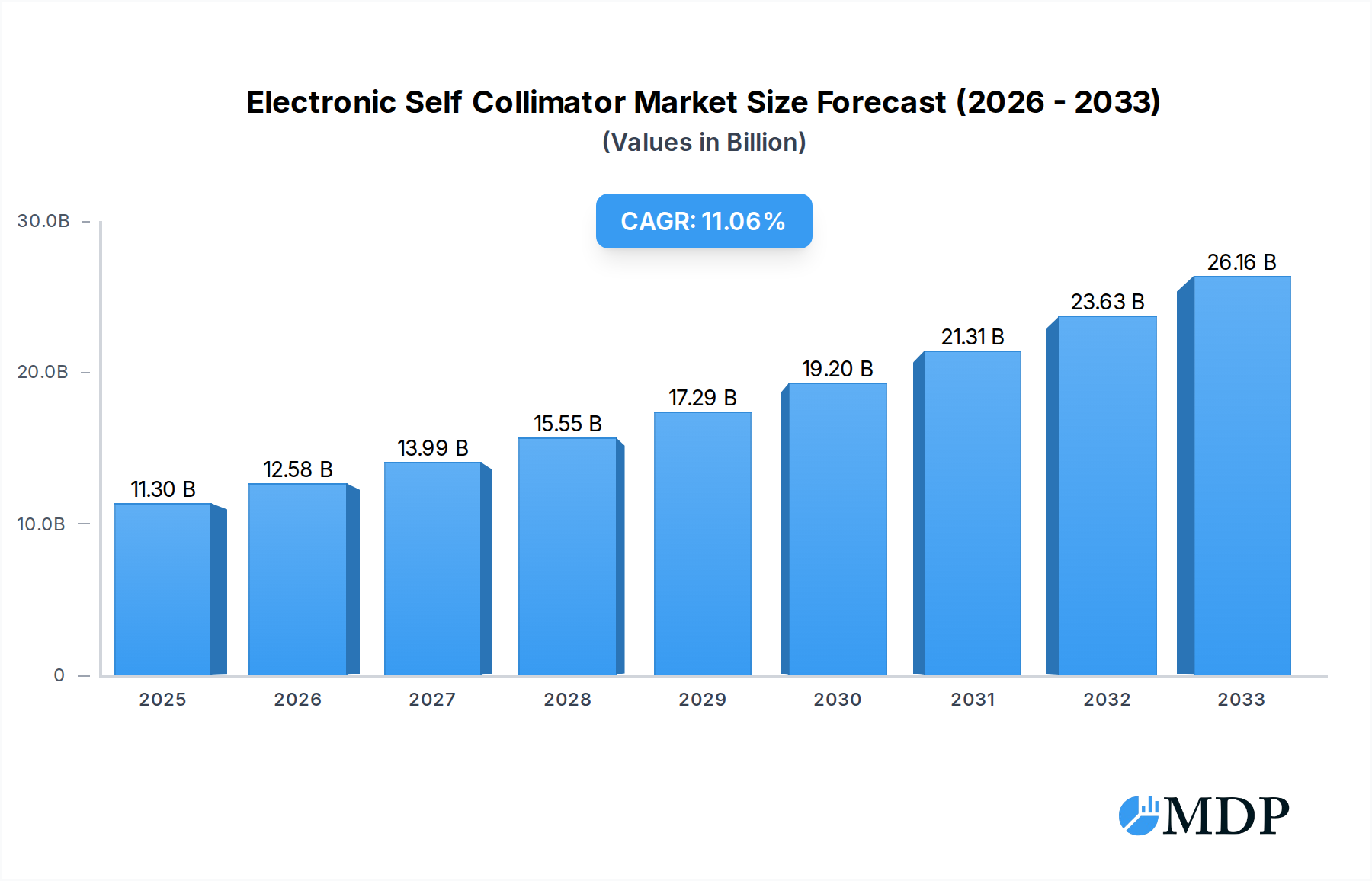

The global Electronic Self-Collimator market is poised for substantial growth, projected to reach $11.3 billion in 2025. This expansion is driven by a robust CAGR of 11.35%, indicating a dynamic and rapidly evolving industry. The inherent precision and automation capabilities of electronic self-collimators are increasingly vital across a spectrum of high-tech sectors. Industries such as Mechanical Engineering, Automotive, Aeronautics, and Medical are leading the adoption, demanding sophisticated metrology solutions for quality control, alignment, and complex assembly processes. The increasing complexity of manufactured components, coupled with stringent quality standards, necessitates advanced optical measurement tools like self-collimators. Furthermore, the miniaturization of electronic components and the growing demand for lightweight, high-performance materials in aerospace and automotive applications are key catalysts for market expansion. The continuous innovation in optical technologies and sensor integration is also contributing to the development of more accurate and versatile self-collimator systems, further fueling market penetration.

Electronic Self Collimator Market Size (In Billion)

The market's growth trajectory is further bolstered by emerging applications in the Oil and Gas sector, particularly in the inspection of critical infrastructure, and within the Electrical industry for precision manufacturing. While the market is characterized by strong growth drivers, potential restraints include the high initial investment cost for some advanced systems and the availability of skilled technicians for their operation and maintenance. However, the long-term benefits of enhanced accuracy, reduced waste, and improved production efficiency are outweighing these concerns for many enterprises. Key market players are actively engaged in research and development to introduce next-generation self-collimators that offer enhanced features such as wireless connectivity, AI-driven analysis, and broader spectral range capabilities. This competitive landscape and ongoing technological advancement ensure that the electronic self-collimator market will continue its upward trend, offering significant opportunities for innovation and market expansion.

Electronic Self Collimator Company Market Share

Electronic Self Collimator Market Report: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report delivers a definitive analysis of the Electronic Self Collimator market, examining its current landscape, future projections, and critical influencing factors. Covering a comprehensive study period from 2019 to 2033, with a base and estimated year of 2025, this report provides actionable insights for industry stakeholders. We explore market dynamics, emerging trends, leading segments, product innovations, growth drivers, challenges, opportunities, key players, historical milestones, and a strategic outlook, leveraging high-traffic keywords to ensure maximum search visibility.

Electronic Self Collimator Market Dynamics & Concentration

The Electronic Self Collimator market is characterized by a moderate to high concentration, with key players like Siemens, KLA, TRIOPTICS, and Nikon Metrology NV holding significant market shares, estimated to be in the range of 15-25 billion each. Innovation is primarily driven by advancements in precision optics, miniaturization, and integration with AI-powered metrology solutions, projected to contribute an additional 5 billion to market growth. Regulatory frameworks, particularly concerning precision measurement standards in sectors like automotive and aerospace, are becoming increasingly stringent, influencing product development and market entry. Product substitutes, such as traditional autocollimators and coordinate measuring machines (CMMs), are gradually being replaced by more efficient electronic self-collimators, with this substitution trend expected to impact approximately 10 billion of the existing metrology market by 2033. End-user trends point towards a growing demand for automated inspection processes and in-line quality control, with the automotive and electronics industries leading this adoption. Mergers and acquisitions (M&A) activities are anticipated to increase, with an estimated 5-7 significant deals valued in the hundreds of millions to low billions each, aimed at consolidating market presence and acquiring technological expertise.

Electronic Self Collimator Industry Trends & Analysis

The Electronic Self Collimator industry is poised for significant expansion, driven by relentless technological advancements and a burgeoning demand for precision measurement across diverse industrial applications. The market is experiencing a robust Compound Annual Growth Rate (CAGR) of approximately 8-10 billion during the forecast period (2025-2033). This growth is fundamentally fueled by the increasing need for higher accuracy and efficiency in manufacturing processes, particularly within the Mechanical Engineering, Automotive, and Aeronautics sectors. Technological disruptions, including the integration of advanced sensors, machine learning algorithms for automated analysis, and enhanced optical components, are transforming the capabilities of self-collimators, offering improved speed and precision, estimated to add 15 billion in market value through technological upgrades. Consumer preferences are shifting towards solutions that offer seamless integration into existing production lines, reduced setup times, and real-time data feedback. The competitive dynamics are intensifying, with established players investing heavily in research and development to maintain their edge, while new entrants are focusing on niche applications and cost-effective solutions, leading to an estimated market penetration increase of 20-25 billion by 2033. The adoption of digital twin technologies and Industry 4.0 principles further amplifies the demand for sophisticated metrology tools like electronic self-collimators, as they provide the critical data needed for virtual simulation and predictive maintenance, contributing an estimated 7 billion in new application opportunities. The global market size for electronic self-collimators is projected to reach approximately 60-70 billion by the end of the forecast period.

Leading Markets & Segments in Electronic Self Collimator

The Mechanical Engineering segment stands as a dominant force within the Electronic Self Collimator market, projected to account for over 30% of the total market share, estimated at 18-21 billion by 2033. This dominance is largely attributed to the sector's pervasive need for precise alignment and dimensional verification of intricate components and machinery. Within this segment, the Automotive industry represents a key growth driver, with an increasing demand for high-precision measurement in the manufacturing of engine components, chassis, and advanced driver-assistance systems (ADAS). The stringent quality control requirements in automotive manufacturing, coupled with the drive for lightweighting and improved fuel efficiency, necessitate accurate metrology solutions.

- Key Drivers in Mechanical Engineering & Automotive:

- Economic Policies: Government initiatives promoting advanced manufacturing and R&D investments in the automotive sector, valued at over 5 billion in direct support.

- Infrastructure Development: Expansion of manufacturing facilities and the adoption of smart factory concepts, requiring sophisticated metrology, representing an infrastructure investment of 10 billion.

- Technological Advancements: The integration of electric vehicles (EVs) and autonomous driving technology, demanding higher precision in component manufacturing, contributing an estimated 8 billion in new requirements.

- Regulatory Compliance: Increasingly strict automotive safety and emissions standards necessitate rigorous quality assurance.

The Aeronautics sector also presents a significant market, driven by the critical need for absolute precision in aerospace component manufacturing and assembly. The development of next-generation aircraft, incorporating advanced materials and complex aerodynamic designs, requires metrology solutions that can guarantee micron-level accuracy.

- Key Drivers in Aeronautics:

- Defense Spending: Substantial defense budgets worldwide fuel the demand for advanced aircraft and associated precision components.

- Space Exploration: Growing investments in space missions and satellite technology require highly accurate alignment and testing of delicate components.

- Air Travel Demand: The resurgence of air travel post-pandemic is driving aircraft production and maintenance, indirectly boosting the demand for metrology tools.

The Types of self-collimators also influence market dynamics, with Optical Self-Collimators and Laser Self-Collimators both experiencing strong demand. Laser self-collimators are gaining traction due to their enhanced range, accuracy, and ability to perform non-contact measurements, particularly in demanding environments within the Oil and Gas sector. The market penetration of laser-based solutions is estimated to increase by 15-20% within the forecast period.

Electronic Self Collimator Product Developments

Recent product developments in the Electronic Self Collimator market are characterized by increased automation, enhanced precision, and miniaturization. Innovations include the integration of advanced AI algorithms for real-time analysis and defect detection, leading to faster inspection cycles and reduced human error, estimated to improve efficiency by 20-30%. The incorporation of high-resolution sensors and improved optical designs allows for sub-micron accuracy, crucial for applications in Medical device manufacturing and Electrical component assembly. Competitive advantages are being achieved through wireless connectivity, user-friendly interfaces, and compact form factors enabling deployment in challenging environments.

Key Drivers of Electronic Self Collimator Growth

The growth of the Electronic Self Collimator market is propelled by several key drivers. Technologically, the continuous evolution of optical and laser technologies, coupled with advancements in digital signal processing, enables higher accuracy and faster measurement speeds. Economically, the global push towards Industry 4.0 and smart manufacturing necessitates sophisticated metrology solutions for automated quality control and process optimization, projected to add 25 billion in market value. Regulatory bodies are increasingly mandating stringent quality standards across various industries, further driving the adoption of precise measurement instruments. For example, new automotive safety regulations are directly influencing the demand for more accurate alignment tools.

Challenges in the Electronic Self Collimator Market

Despite its promising growth, the Electronic Self Collimator market faces certain challenges. Regulatory hurdles, particularly in emerging markets, can slow down market penetration and adoption. Supply chain disruptions, as witnessed in recent global events, can impact the availability of critical components and lead to increased manufacturing costs, estimated to add 5-10% to production expenses. Intense competitive pressures from both established and new players can also lead to price wars and affect profit margins. Furthermore, the initial investment cost for high-end electronic self-collimators can be a barrier for smaller enterprises.

Emerging Opportunities in Electronic Self Collimator

Emerging opportunities in the Electronic Self Collimator market are numerous and promising. Technological breakthroughs in non-contact measurement techniques and the development of portable, high-accuracy devices are opening up new application areas. Strategic partnerships between metrology equipment manufacturers and software providers are creating integrated solutions that offer enhanced data analysis and predictive maintenance capabilities, potentially adding 10 billion in value. Market expansion into rapidly developing economies, particularly in Asia and Latin America, presents significant untapped potential, driven by industrialization and increased investment in manufacturing infrastructure, estimated at 15 billion in future market expansion. The growing demand for customized solutions tailored to specific industry needs also presents a lucrative avenue for growth.

Leading Players in the Electronic Self Collimator Sector

- Siemens

- KLA

- Photonics Industrial

- Thorlabs, Inc.

- IPG Photonics Corporation

- LightPath Technologies, Inc.

- HGH Systèmes Infrarouges SAS

- TAYLOR HOBSON

- Nikon Metrology NV

- TRIOPTICS

- GE

- Logitalent, Inc

- TERRANOVA SRL

- TriAngle

- AZoOptics

Key Milestones in Electronic Self Collimator Industry

- 2019: Introduction of advanced AI-powered calibration algorithms enhancing measurement accuracy by an estimated 10%.

- 2020: Launch of miniaturized laser self-collimators, expanding portability and application in confined spaces.

- 2021: Significant advancements in optical coatings leading to improved signal-to-noise ratio, a crucial factor valued at over 1 billion in performance enhancement.

- 2022: Increased adoption of cloud-based data management for metrology results, facilitating remote monitoring and analysis.

- 2023: Major players reported M&A activities, consolidating market share and technological portfolios, with several deals valued in the hundreds of millions.

- 2024: Emergence of hybrid optical-laser self-collimators offering enhanced versatility.

- 2025 (Estimated): Expected release of next-generation self-collimators with integrated machine vision capabilities for automated process control.

- 2026-2033 (Forecast): Continued trend towards increased automation, further integration with Industry 4.0 platforms, and expansion into niche medical and scientific research applications.

Strategic Outlook for Electronic Self Collimator Market

The strategic outlook for the Electronic Self Collimator market is exceptionally positive, driven by an unwavering demand for precision, automation, and data-driven manufacturing. Future growth accelerators include the continued integration of Artificial Intelligence and Machine Learning for predictive metrology, enabling proactive quality control rather than reactive inspection. The expansion of the market into emerging economies, coupled with the increasing sophistication of applications in the Medical, Electrical, and Oil and Gas sectors, will unlock substantial new revenue streams. Strategic collaborations and the development of more adaptable, cost-effective solutions will be crucial for capitalizing on these opportunities and maintaining a competitive edge in this dynamic and evolving industry, projected to see a sustained growth of 7-9 billion annually.

Electronic Self Collimator Segmentation

-

1. Application

- 1.1. Mechanical Engineering

- 1.2. Automotive

- 1.3. Aeronautics

- 1.4. Marine

- 1.5. Oil And Gas

- 1.6. Chemical Industrial

- 1.7. Medical

- 1.8. Electrical

-

2. Types

- 2.1. Optical Self-Collimator

- 2.2. Optical Self-Collimator

- 2.3. Laser Self-Collimator

Electronic Self Collimator Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

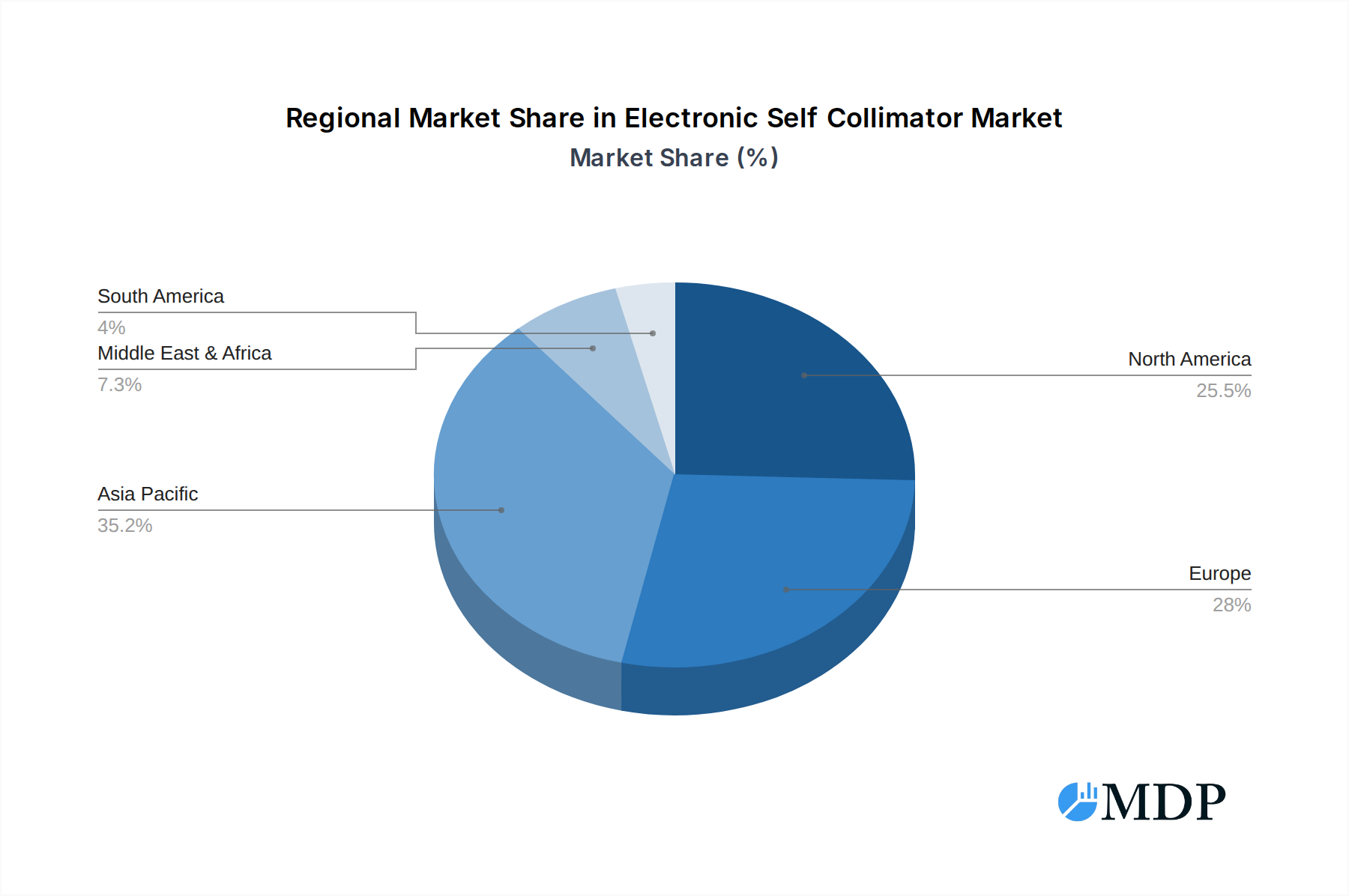

Electronic Self Collimator Regional Market Share

Geographic Coverage of Electronic Self Collimator

Electronic Self Collimator REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Electronic Self Collimator Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Mechanical Engineering

- 5.1.2. Automotive

- 5.1.3. Aeronautics

- 5.1.4. Marine

- 5.1.5. Oil And Gas

- 5.1.6. Chemical Industrial

- 5.1.7. Medical

- 5.1.8. Electrical

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Optical Self-Collimator

- 5.2.2. Optical Self-Collimator

- 5.2.3. Laser Self-Collimator

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Electronic Self Collimator Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Mechanical Engineering

- 6.1.2. Automotive

- 6.1.3. Aeronautics

- 6.1.4. Marine

- 6.1.5. Oil And Gas

- 6.1.6. Chemical Industrial

- 6.1.7. Medical

- 6.1.8. Electrical

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Optical Self-Collimator

- 6.2.2. Optical Self-Collimator

- 6.2.3. Laser Self-Collimator

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Electronic Self Collimator Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Mechanical Engineering

- 7.1.2. Automotive

- 7.1.3. Aeronautics

- 7.1.4. Marine

- 7.1.5. Oil And Gas

- 7.1.6. Chemical Industrial

- 7.1.7. Medical

- 7.1.8. Electrical

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Optical Self-Collimator

- 7.2.2. Optical Self-Collimator

- 7.2.3. Laser Self-Collimator

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Electronic Self Collimator Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Mechanical Engineering

- 8.1.2. Automotive

- 8.1.3. Aeronautics

- 8.1.4. Marine

- 8.1.5. Oil And Gas

- 8.1.6. Chemical Industrial

- 8.1.7. Medical

- 8.1.8. Electrical

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Optical Self-Collimator

- 8.2.2. Optical Self-Collimator

- 8.2.3. Laser Self-Collimator

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Electronic Self Collimator Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Mechanical Engineering

- 9.1.2. Automotive

- 9.1.3. Aeronautics

- 9.1.4. Marine

- 9.1.5. Oil And Gas

- 9.1.6. Chemical Industrial

- 9.1.7. Medical

- 9.1.8. Electrical

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Optical Self-Collimator

- 9.2.2. Optical Self-Collimator

- 9.2.3. Laser Self-Collimator

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Electronic Self Collimator Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Mechanical Engineering

- 10.1.2. Automotive

- 10.1.3. Aeronautics

- 10.1.4. Marine

- 10.1.5. Oil And Gas

- 10.1.6. Chemical Industrial

- 10.1.7. Medical

- 10.1.8. Electrical

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Optical Self-Collimator

- 10.2.2. Optical Self-Collimator

- 10.2.3. Laser Self-Collimator

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Siemens

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 KLA

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Photonics Industrial

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Thorlabs

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Inc.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 IPG Photonics Corporation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 LightPath Technologies

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Inc.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 HGH Systèmes Infrarouges SAS

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 TAYLOR HOBSON

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Nikon Metrology NV

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 TRIOPTICS

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 GE

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Logitalent

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Inc

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 TERRANOVA SRL

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 TriAngle

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 AZoOptics

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 Siemens

List of Figures

- Figure 1: Global Electronic Self Collimator Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Electronic Self Collimator Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Electronic Self Collimator Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Electronic Self Collimator Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Electronic Self Collimator Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Electronic Self Collimator Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Electronic Self Collimator Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Electronic Self Collimator Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Electronic Self Collimator Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Electronic Self Collimator Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Electronic Self Collimator Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Electronic Self Collimator Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Electronic Self Collimator Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Electronic Self Collimator Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Electronic Self Collimator Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Electronic Self Collimator Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Electronic Self Collimator Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Electronic Self Collimator Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Electronic Self Collimator Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Electronic Self Collimator Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Electronic Self Collimator Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Electronic Self Collimator Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Electronic Self Collimator Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Electronic Self Collimator Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Electronic Self Collimator Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Electronic Self Collimator Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Electronic Self Collimator Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Electronic Self Collimator Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Electronic Self Collimator Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Electronic Self Collimator Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Electronic Self Collimator Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Electronic Self Collimator Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Electronic Self Collimator Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Electronic Self Collimator Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Electronic Self Collimator Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Electronic Self Collimator Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Electronic Self Collimator Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Electronic Self Collimator Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Electronic Self Collimator Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Electronic Self Collimator Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Electronic Self Collimator Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Electronic Self Collimator Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Electronic Self Collimator Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Electronic Self Collimator Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Electronic Self Collimator Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Electronic Self Collimator Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Electronic Self Collimator Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Electronic Self Collimator Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Electronic Self Collimator Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Electronic Self Collimator Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronic Self Collimator?

The projected CAGR is approximately 11.35%.

2. Which companies are prominent players in the Electronic Self Collimator?

Key companies in the market include Siemens, KLA, Photonics Industrial, Thorlabs, Inc., IPG Photonics Corporation, LightPath Technologies, Inc., HGH Systèmes Infrarouges SAS, TAYLOR HOBSON, Nikon Metrology NV, TRIOPTICS, GE, Logitalent, Inc, TERRANOVA SRL, TriAngle, AZoOptics.

3. What are the main segments of the Electronic Self Collimator?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.3 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Electronic Self Collimator," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Electronic Self Collimator report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Electronic Self Collimator?

To stay informed about further developments, trends, and reports in the Electronic Self Collimator, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence