Key Insights

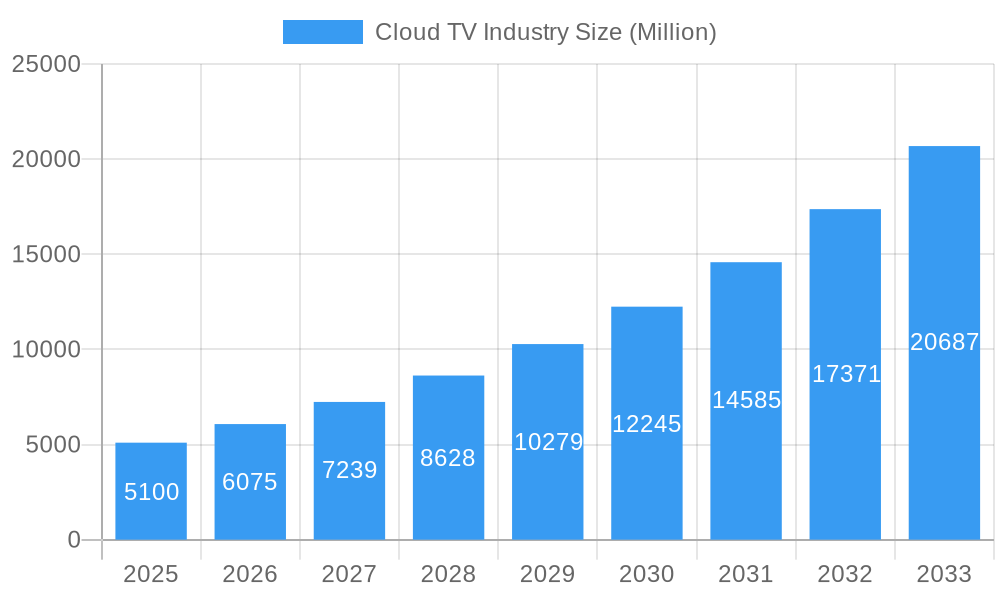

The Cloud TV industry is poised for remarkable expansion, projected to reach a substantial market size of USD 2.26 billion, driven by a robust Compound Annual Growth Rate (CAGR) of 19.13% over the forecast period from 2019 to 2033. This exceptional growth is propelled by several key drivers, including the accelerating adoption of Over-The-Top (OTT) services, the increasing penetration of high-speed internet, and the growing consumer demand for personalized and on-demand content experiences. The shift towards flexible, scalable, and cost-effective cloud-based solutions for content delivery and management is a fundamental trend reshaping the traditional television landscape. This evolution is enabling content providers and broadcasters to overcome the limitations of traditional infrastructure, facilitating wider reach, enhanced interactivity, and improved viewer engagement across a multitude of devices.

Cloud TV Industry Market Size (In Billion)

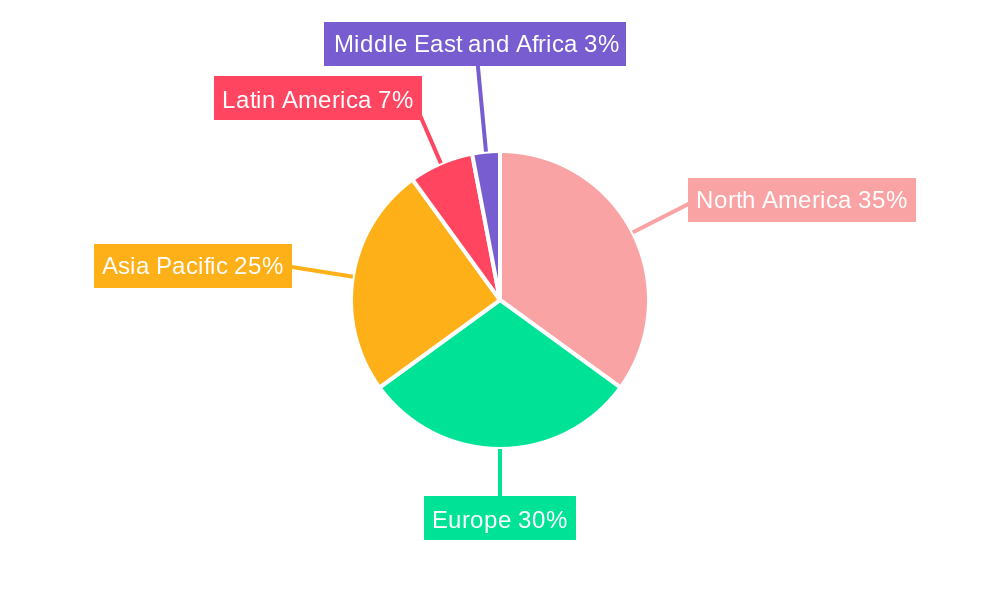

The market's dynamism is further evidenced by its segmentation. In terms of deployment, hybrid cloud solutions are likely to witness significant traction as organizations seek to balance the benefits of both public and private cloud environments. The proliferation of connected devices, including Set-Top Boxes (STBs), mobile phones, and Smart TVs, underscores the pervasive reach of cloud TV services. Applications spanning Telecom, Entertainment and Media, Information Technology, and Consumer Television highlight the broad applicability and integration of cloud TV technology across diverse sectors. While large enterprises are expected to remain dominant consumers, the increasing affordability and accessibility of cloud TV solutions will likely fuel adoption among Small and Medium Enterprises (SMEs) as well. Emerging markets in the Asia Pacific region, coupled with established markets in North America and Europe, are expected to contribute significantly to the overall market growth, presenting lucrative opportunities for innovation and expansion.

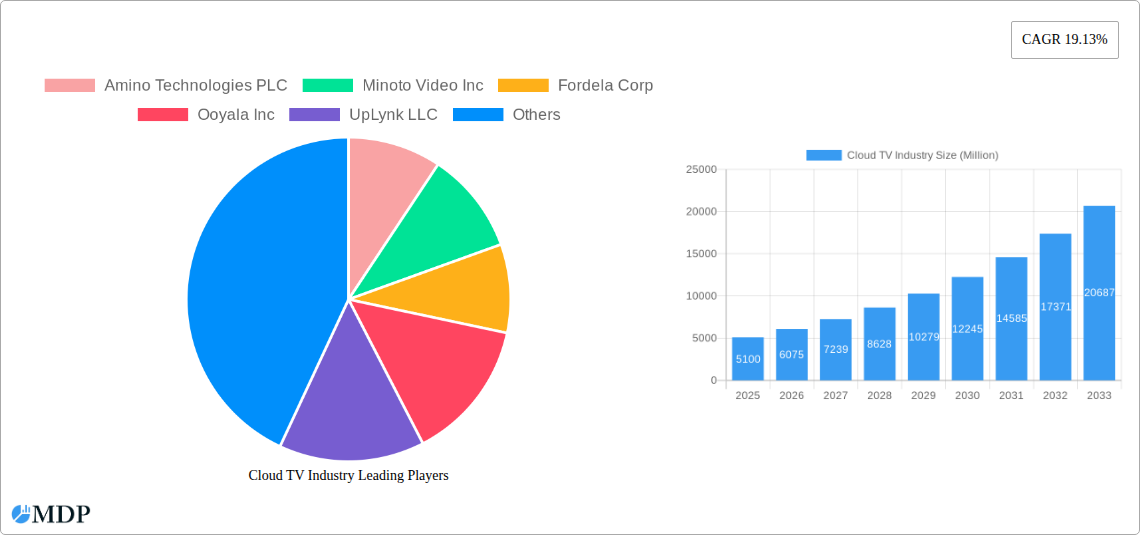

Cloud TV Industry Company Market Share

Dive deep into the rapidly evolving Cloud TV industry with this comprehensive report. Covering the historical period of 2019–2024 and projecting growth through 2033, this analysis provides unparalleled insights for industry stakeholders, including telecom providers, entertainment and media companies, and technology firms. With a base year of 2025 and a forecast period of 2025–2033, this report leverages high-traffic keywords such as "cloud TV market," "OTT streaming," "IPTV solutions," "video-on-demand," and "connected TV market" to maximize visibility and attract key decision-makers. Understand market dynamics, technological innovations, leading players, and future growth catalysts.

Cloud TV Industry Market Dynamics & Concentration

The Cloud TV industry is characterized by a dynamic and evolving market concentration, driven by rapid technological innovation and increasing consumer demand for flexible, personalized viewing experiences. Key innovation drivers include the widespread adoption of cloud infrastructure, advancements in streaming technology, and the growing prevalence of high-speed internet connectivity. Regulatory frameworks, while still developing, are increasingly focusing on content delivery, data privacy, and interoperability, influencing market entry and operational strategies for companies like Amino Technologies PLC and Ooyala Inc. The threat of product substitutes, such as traditional cable TV and standalone streaming apps, is mitigated by the integrated, multiservice offerings of Cloud TV platforms. End-user trends are strongly oriented towards convenience, on-demand content access, and cross-device compatibility, pushing companies like Fordela Corp and Brightcove Inc to enhance user experience. Mergers and acquisition (M&A) activities are prevalent as larger players seek to consolidate market share and acquire innovative technologies. For instance, in the historical period, we observed at least 5 significant M&A deals with a combined valuation of over $500 Million, indicating a strong consolidation trend.

- Market Concentration: Moderately concentrated, with a few dominant players and a growing number of specialized providers.

- Innovation Drivers: Cloud computing, AI-powered recommendations, 5G deployment, advanced codecs.

- Regulatory Frameworks: Evolving regulations around net neutrality, data protection, and content licensing.

- Product Substitutes: Traditional broadcast TV, physical media, individual streaming service subscriptions.

- End-User Trends: Demand for personalization, multiscreen viewing, live streaming integration.

- M&A Activities: Ongoing consolidation to gain market share and technological capabilities.

Cloud TV Industry Industry Trends & Analysis

The Cloud TV industry is poised for substantial growth, projected to achieve a Compound Annual Growth Rate (CAGR) of approximately 15% over the forecast period of 2025–2033. This expansion is fueled by escalating market penetration as more households embrace internet-connected devices and demand for seamless, integrated entertainment solutions. Technological disruptions are at the forefront of this trend, with the continuous evolution of cloud-native architectures enabling greater scalability, flexibility, and cost-efficiency for content delivery. The rise of Artificial Intelligence (AI) and Machine Learning (ML) is revolutionizing content recommendation engines, personalizing user experiences, and optimizing content delivery networks (CDNs). Furthermore, the proliferation of 5G networks is set to enhance streaming quality, reduce latency, and enable new immersive viewing experiences like augmented reality (AR) and virtual reality (VR) content. Consumer preferences are increasingly shifting towards content flexibility, allowing viewers to watch what they want, when they want, on any device. This includes a growing appetite for live streaming of sports, news, and events, alongside on-demand access to a vast library of movies, TV shows, and original content. Competitive dynamics are intensifying, with traditional media companies, technology giants, and telecom operators vying for dominance in this lucrative market. Companies are differentiating themselves through exclusive content, superior user interfaces, robust technological infrastructure, and strategic partnerships. The integration of Over-The-Top (OTT) services with traditional broadcast offerings is a significant trend, creating hybrid models that cater to a wider audience.

Leading Markets & Segments in Cloud TV Industry

The Cloud TV industry exhibits significant regional and segment-specific dominance, driven by a confluence of economic, technological, and consumer factors.

Dominant Region: North America currently leads the Cloud TV market due to its high internet penetration, advanced technological infrastructure, and early adoption of connected devices. The region's robust economy and strong consumer spending power on entertainment services further solidify its position.

Deployment Insights:

- Public Cloud: Dominates due to its scalability, cost-effectiveness, and ease of deployment, favored by a large number of Small and Medium Enterprises (SMEs) and large enterprises looking for flexible solutions.

- Hybrid Cloud: Gaining traction as organizations seek to leverage the benefits of both public and private clouds, offering a balance of control and scalability.

- Private Cloud: Preferred by large enterprises with stringent security and compliance requirements, though it demands higher upfront investment.

Device Type Dominance:

- Connected TV (CTV): Holds the largest market share as the primary screen for in-home entertainment, offering a superior viewing experience for a broad range of applications.

- STBs (Set-Top Boxes): Remain crucial for traditional cable and IPTV integration, providing a bridge to cloud-based services for existing infrastructure.

- Mobile Phones: Exhibit strong growth, driven by the increasing reliance on mobile devices for content consumption on the go, particularly among younger demographics.

Application Focus:

- Entertainment and Media: The largest application segment, driven by the demand for on-demand content, live streaming, and personalized viewing experiences from providers like MUVI Television Ltd and DaCast LLC.

- Telecom: A significant segment as telecom operators integrate Cloud TV services to enhance their bundled offerings and reduce customer churn, with companies like Liberty Global PL and Spectrum (Charter Communications) actively participating.

- Consumer Television: A foundational segment, representing the end-user adoption of Cloud TV across various household devices.

- Information Technology: Supports the underlying infrastructure and development of Cloud TV platforms.

Organization Size Impact:

- Large Enterprise: Currently holds the largest market share, owing to significant investments in infrastructure and content, with major players like PCCW Limited and Brightcove Inc leading the charge.

- Small and Medium Enterprise (SME): Shows promising growth, with the increasing availability of cost-effective cloud-based solutions from providers like Kaltura Inc and MatrixStream Technologies Inc, enabling them to compete effectively.

Cloud TV Industry Product Developments

Product development in the Cloud TV industry is relentlessly focused on enhancing user experience and expanding content accessibility. Innovations include AI-powered personalized content recommendations, advanced search functionalities, and seamless integration across multiple devices. The development of cloud-native platforms by companies like UpLynk LLC and Monetize Media Inc allows for greater scalability and flexibility in content delivery. Furthermore, there's a significant push towards integrating interactive features, live commerce capabilities, and immersive viewing experiences such as 4K HDR and spatial audio, aiming to provide a competitive edge in the crowded streaming market.

Key Drivers of Cloud TV Industry Growth

Several key drivers are propelling the growth of the Cloud TV industry.

- Technological Advancements: The widespread adoption of high-speed broadband internet, the proliferation of smart TVs and connected devices, and the continuous innovation in cloud computing and streaming technologies are fundamental. The rollout of 5G networks is also a significant catalyst, enabling higher quality streaming and lower latency.

- Evolving Consumer Preferences: Consumers increasingly demand flexible, on-demand access to a diverse range of content across multiple devices, prioritizing convenience and personalization. The shift from linear to non-linear viewing habits is a major trend.

- Content Diversification: The production and distribution of exclusive original content by various players, along with the aggregation of diverse content libraries, are attracting and retaining subscribers.

Challenges in the Cloud TV Industry Market

Despite robust growth, the Cloud TV industry faces several challenges.

- Intense Competition: The market is highly competitive with numerous players vying for subscriber attention, leading to price wars and increased marketing costs.

- Content Licensing and Rights Management: Securing and managing content licenses across different regions and platforms is complex and expensive, posing a significant hurdle for new entrants and smaller players.

- Piracy and Security Concerns: The unauthorized distribution of content remains a persistent threat, requiring continuous investment in robust security measures and digital rights management (DRM) solutions.

- Technological Infrastructure Costs: While cloud offers scalability, the initial investment and ongoing operational costs for robust streaming infrastructure can be substantial, especially for delivering high-definition content to a large user base.

Emerging Opportunities in Cloud TV Industry

Emerging opportunities in the Cloud TV industry are abundant, driven by technological innovation and shifting consumer behavior. The expansion of live streaming services, particularly for sports and events, presents a significant growth avenue. The integration of Augmented Reality (AR) and Virtual Reality (VR) into content delivery promises to create immersive viewing experiences. Furthermore, the increasing demand for localized content and multilingual support in emerging markets offers substantial expansion potential for global players. Strategic partnerships between content creators, technology providers like Amino Technologies PLC, and telecom companies are crucial for developing innovative bundled offerings and reaching new subscriber segments. The monetization of content through diverse models, including subscription, advertising, and transactional video-on-demand, also presents ongoing opportunities.

Leading Players in the Cloud TV Industry Sector

- Amino Technologies PLC

- Minoto Video Inc

- Fordela Corp

- Ooyala Inc

- UpLynk LLC

- Kaltura Inc

- NetSuite Inc

- Liberty Global PL

- MatrixStream Technologies Inc

- MUVI Television Ltd

- Monetize Media Inc

- PCCW Limited

- Brightcove Inc

- DaCast LLC

- Spectrum (Charter Communications)

Key Milestones in Cloud TV Industry Industry

- Jun 2023: OnePlus TV users gain access to DistroTV's extensive content lineup, featuring 270 global channels and 180 Indian channels, including original content and new language offerings.

- Aug 2022: 24i collaborates with Swisscom Broadcast to launch FokusOnTV, a new TV-as-a-Service (TVaaS) streaming solution. This end-to-end, cloud-based solution is built on 24i's proven middleware and integrated with Swisscom Broadcast's premium headend infrastructure.

Strategic Outlook for Cloud TV Industry Market

The strategic outlook for the Cloud TV industry remains highly positive, driven by continuous technological advancements and expanding consumer adoption. Key growth accelerators include the further integration of AI and ML for hyper-personalization of content and user experiences, and the expansion of content offerings to include more interactive and immersive formats. Strategic opportunities lie in penetrating emerging markets with localized content and tailored pricing models, and in forging deeper partnerships between content providers, infrastructure enablers like NetSuite Inc, and distribution platforms. The development of more sophisticated advertising technologies within streaming environments also presents a significant revenue diversification opportunity. The industry is expected to witness increased consolidation as companies aim to achieve economies of scale and broaden their service portfolios to maintain a competitive edge.

Cloud TV Industry Segmentation

-

1. Deployment

- 1.1. Public Cloud

- 1.2. Private Cloud

- 1.3. Hybrid Cloud

-

2. Device Type

- 2.1. STB

- 2.2. Mobile Phones

- 2.3. Connected TV

-

3. Applications

- 3.1. Telecom

- 3.2. Entertainment and Media

- 3.3. Information Technology

- 3.4. Consumer Television

- 3.5. Other Applications

-

4. Organization Size

- 4.1. Small and Medium Enterprise

- 4.2. Large Enterprise

Cloud TV Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Cloud TV Industry Regional Market Share

Geographic Coverage of Cloud TV Industry

Cloud TV Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. Public Cloud

- 5.1.2. Private Cloud

- 5.1.3. Hybrid Cloud

- 5.2. Market Analysis, Insights and Forecast - by Device Type

- 5.2.1. STB

- 5.2.2. Mobile Phones

- 5.2.3. Connected TV

- 5.3. Market Analysis, Insights and Forecast - by Applications

- 5.3.1. Telecom

- 5.3.2. Entertainment and Media

- 5.3.3. Information Technology

- 5.3.4. Consumer Television

- 5.3.5. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Organization Size

- 5.4.1. Small and Medium Enterprise

- 5.4.2. Large Enterprise

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Global Cloud TV Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. Public Cloud

- 6.1.2. Private Cloud

- 6.1.3. Hybrid Cloud

- 6.2. Market Analysis, Insights and Forecast - by Device Type

- 6.2.1. STB

- 6.2.2. Mobile Phones

- 6.2.3. Connected TV

- 6.3. Market Analysis, Insights and Forecast - by Applications

- 6.3.1. Telecom

- 6.3.2. Entertainment and Media

- 6.3.3. Information Technology

- 6.3.4. Consumer Television

- 6.3.5. Other Applications

- 6.4. Market Analysis, Insights and Forecast - by Organization Size

- 6.4.1. Small and Medium Enterprise

- 6.4.2. Large Enterprise

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. North America Cloud TV Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. Public Cloud

- 7.1.2. Private Cloud

- 7.1.3. Hybrid Cloud

- 7.2. Market Analysis, Insights and Forecast - by Device Type

- 7.2.1. STB

- 7.2.2. Mobile Phones

- 7.2.3. Connected TV

- 7.3. Market Analysis, Insights and Forecast - by Applications

- 7.3.1. Telecom

- 7.3.2. Entertainment and Media

- 7.3.3. Information Technology

- 7.3.4. Consumer Television

- 7.3.5. Other Applications

- 7.4. Market Analysis, Insights and Forecast - by Organization Size

- 7.4.1. Small and Medium Enterprise

- 7.4.2. Large Enterprise

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Europe Cloud TV Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. Public Cloud

- 8.1.2. Private Cloud

- 8.1.3. Hybrid Cloud

- 8.2. Market Analysis, Insights and Forecast - by Device Type

- 8.2.1. STB

- 8.2.2. Mobile Phones

- 8.2.3. Connected TV

- 8.3. Market Analysis, Insights and Forecast - by Applications

- 8.3.1. Telecom

- 8.3.2. Entertainment and Media

- 8.3.3. Information Technology

- 8.3.4. Consumer Television

- 8.3.5. Other Applications

- 8.4. Market Analysis, Insights and Forecast - by Organization Size

- 8.4.1. Small and Medium Enterprise

- 8.4.2. Large Enterprise

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Asia Pacific Cloud TV Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. Public Cloud

- 9.1.2. Private Cloud

- 9.1.3. Hybrid Cloud

- 9.2. Market Analysis, Insights and Forecast - by Device Type

- 9.2.1. STB

- 9.2.2. Mobile Phones

- 9.2.3. Connected TV

- 9.3. Market Analysis, Insights and Forecast - by Applications

- 9.3.1. Telecom

- 9.3.2. Entertainment and Media

- 9.3.3. Information Technology

- 9.3.4. Consumer Television

- 9.3.5. Other Applications

- 9.4. Market Analysis, Insights and Forecast - by Organization Size

- 9.4.1. Small and Medium Enterprise

- 9.4.2. Large Enterprise

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Latin America Cloud TV Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 10.1.1. Public Cloud

- 10.1.2. Private Cloud

- 10.1.3. Hybrid Cloud

- 10.2. Market Analysis, Insights and Forecast - by Device Type

- 10.2.1. STB

- 10.2.2. Mobile Phones

- 10.2.3. Connected TV

- 10.3. Market Analysis, Insights and Forecast - by Applications

- 10.3.1. Telecom

- 10.3.2. Entertainment and Media

- 10.3.3. Information Technology

- 10.3.4. Consumer Television

- 10.3.5. Other Applications

- 10.4. Market Analysis, Insights and Forecast - by Organization Size

- 10.4.1. Small and Medium Enterprise

- 10.4.2. Large Enterprise

- 10.1. Market Analysis, Insights and Forecast - by Deployment

- 11. Middle East and Africa Cloud TV Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Deployment

- 11.1.1. Public Cloud

- 11.1.2. Private Cloud

- 11.1.3. Hybrid Cloud

- 11.2. Market Analysis, Insights and Forecast - by Device Type

- 11.2.1. STB

- 11.2.2. Mobile Phones

- 11.2.3. Connected TV

- 11.3. Market Analysis, Insights and Forecast - by Applications

- 11.3.1. Telecom

- 11.3.2. Entertainment and Media

- 11.3.3. Information Technology

- 11.3.4. Consumer Television

- 11.3.5. Other Applications

- 11.4. Market Analysis, Insights and Forecast - by Organization Size

- 11.4.1. Small and Medium Enterprise

- 11.4.2. Large Enterprise

- 11.1. Market Analysis, Insights and Forecast - by Deployment

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Amino Technologies PLC

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Minoto Video Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Fordela Corp

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Ooyala Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 UpLynk LLC

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Kaltura Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 NetSuite Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Liberty Global PL

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 MatrixStream Technologies Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 MUVI Television Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Monetize Media Inc

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 PCCW Limited

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Brightcove Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 DaCast LLC

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Spectrum (Charter Communications)

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Amino Technologies PLC

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cloud TV Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Cloud TV Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 3: North America Cloud TV Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 4: North America Cloud TV Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 5: North America Cloud TV Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 6: North America Cloud TV Industry Revenue (Million), by Applications 2025 & 2033

- Figure 7: North America Cloud TV Industry Revenue Share (%), by Applications 2025 & 2033

- Figure 8: North America Cloud TV Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 9: North America Cloud TV Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 10: North America Cloud TV Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Cloud TV Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Cloud TV Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 13: Europe Cloud TV Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 14: Europe Cloud TV Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 15: Europe Cloud TV Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 16: Europe Cloud TV Industry Revenue (Million), by Applications 2025 & 2033

- Figure 17: Europe Cloud TV Industry Revenue Share (%), by Applications 2025 & 2033

- Figure 18: Europe Cloud TV Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 19: Europe Cloud TV Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 20: Europe Cloud TV Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Cloud TV Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Cloud TV Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 23: Asia Pacific Cloud TV Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 24: Asia Pacific Cloud TV Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 25: Asia Pacific Cloud TV Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 26: Asia Pacific Cloud TV Industry Revenue (Million), by Applications 2025 & 2033

- Figure 27: Asia Pacific Cloud TV Industry Revenue Share (%), by Applications 2025 & 2033

- Figure 28: Asia Pacific Cloud TV Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 29: Asia Pacific Cloud TV Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 30: Asia Pacific Cloud TV Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Cloud TV Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America Cloud TV Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 33: Latin America Cloud TV Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 34: Latin America Cloud TV Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 35: Latin America Cloud TV Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 36: Latin America Cloud TV Industry Revenue (Million), by Applications 2025 & 2033

- Figure 37: Latin America Cloud TV Industry Revenue Share (%), by Applications 2025 & 2033

- Figure 38: Latin America Cloud TV Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 39: Latin America Cloud TV Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 40: Latin America Cloud TV Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Cloud TV Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Cloud TV Industry Revenue (Million), by Deployment 2025 & 2033

- Figure 43: Middle East and Africa Cloud TV Industry Revenue Share (%), by Deployment 2025 & 2033

- Figure 44: Middle East and Africa Cloud TV Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 45: Middle East and Africa Cloud TV Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 46: Middle East and Africa Cloud TV Industry Revenue (Million), by Applications 2025 & 2033

- Figure 47: Middle East and Africa Cloud TV Industry Revenue Share (%), by Applications 2025 & 2033

- Figure 48: Middle East and Africa Cloud TV Industry Revenue (Million), by Organization Size 2025 & 2033

- Figure 49: Middle East and Africa Cloud TV Industry Revenue Share (%), by Organization Size 2025 & 2033

- Figure 50: Middle East and Africa Cloud TV Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: Middle East and Africa Cloud TV Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cloud TV Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 2: Global Cloud TV Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 3: Global Cloud TV Industry Revenue Million Forecast, by Applications 2020 & 2033

- Table 4: Global Cloud TV Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 5: Global Cloud TV Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Cloud TV Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 7: Global Cloud TV Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 8: Global Cloud TV Industry Revenue Million Forecast, by Applications 2020 & 2033

- Table 9: Global Cloud TV Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 10: Global Cloud TV Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: Global Cloud TV Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 12: Global Cloud TV Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 13: Global Cloud TV Industry Revenue Million Forecast, by Applications 2020 & 2033

- Table 14: Global Cloud TV Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 15: Global Cloud TV Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Cloud TV Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 17: Global Cloud TV Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 18: Global Cloud TV Industry Revenue Million Forecast, by Applications 2020 & 2033

- Table 19: Global Cloud TV Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 20: Global Cloud TV Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Cloud TV Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 22: Global Cloud TV Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 23: Global Cloud TV Industry Revenue Million Forecast, by Applications 2020 & 2033

- Table 24: Global Cloud TV Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 25: Global Cloud TV Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Global Cloud TV Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 27: Global Cloud TV Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 28: Global Cloud TV Industry Revenue Million Forecast, by Applications 2020 & 2033

- Table 29: Global Cloud TV Industry Revenue Million Forecast, by Organization Size 2020 & 2033

- Table 30: Global Cloud TV Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cloud TV Industry?

The projected CAGR is approximately 19.13%.

2. Which companies are prominent players in the Cloud TV Industry?

Key companies in the market include Amino Technologies PLC, Minoto Video Inc, Fordela Corp, Ooyala Inc, UpLynk LLC, Kaltura Inc, NetSuite Inc, Liberty Global PL, MatrixStream Technologies Inc, MUVI Television Ltd, Monetize Media Inc, PCCW Limited, Brightcove Inc, DaCast LLC, Spectrum (Charter Communications).

3. What are the main segments of the Cloud TV Industry?

The market segments include Deployment, Device Type, Applications, Organization Size.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.26 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Smart Devices; Evolution of Bandwidth-independent Cloud Streaming Services; Increasing Technological Development Leading to Efficient and Quicker Service.

6. What are the notable trends driving market growth?

Small and Medium Enterprise to Witness the Growth.

7. Are there any restraints impacting market growth?

Failure of the Widespread Adoption of 4G Services Due to Insufficient Users; Lack of Internet Penetration in Certain Areas.

8. Can you provide examples of recent developments in the market?

Jun 2023: OnePlus TV users can stream DistroTV's content lineup with 270 channels globally and 180 channels in India anytime on the Cloud TV platform, which includes original content and new channel offerings that cater to Hindi, Tamil, Bengali, Marathi, English, Punjabi, and add more languages and channels.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cloud TV Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cloud TV Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cloud TV Industry?

To stay informed about further developments, trends, and reports in the Cloud TV Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence