Key Insights

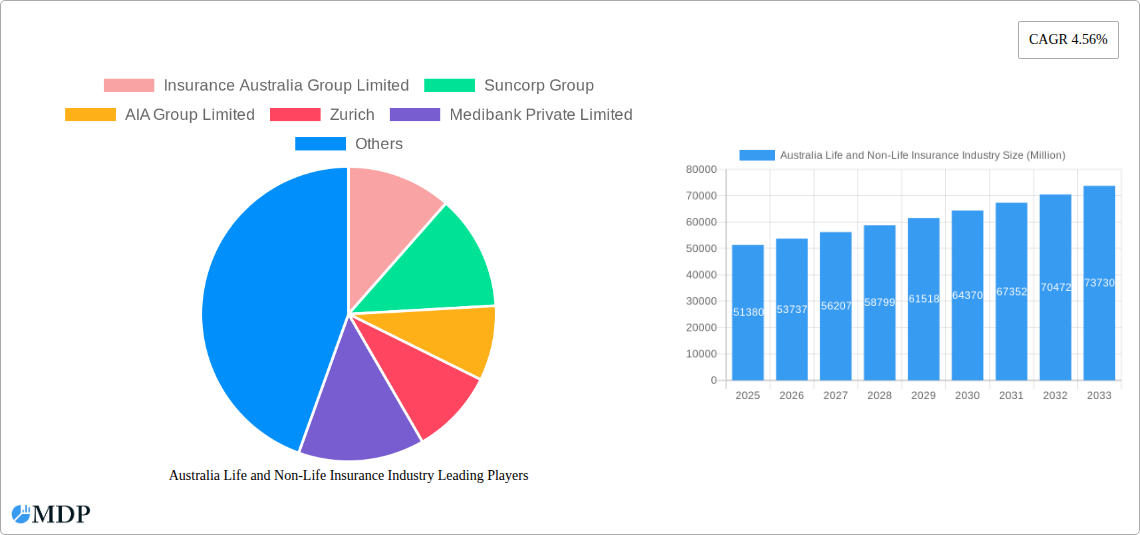

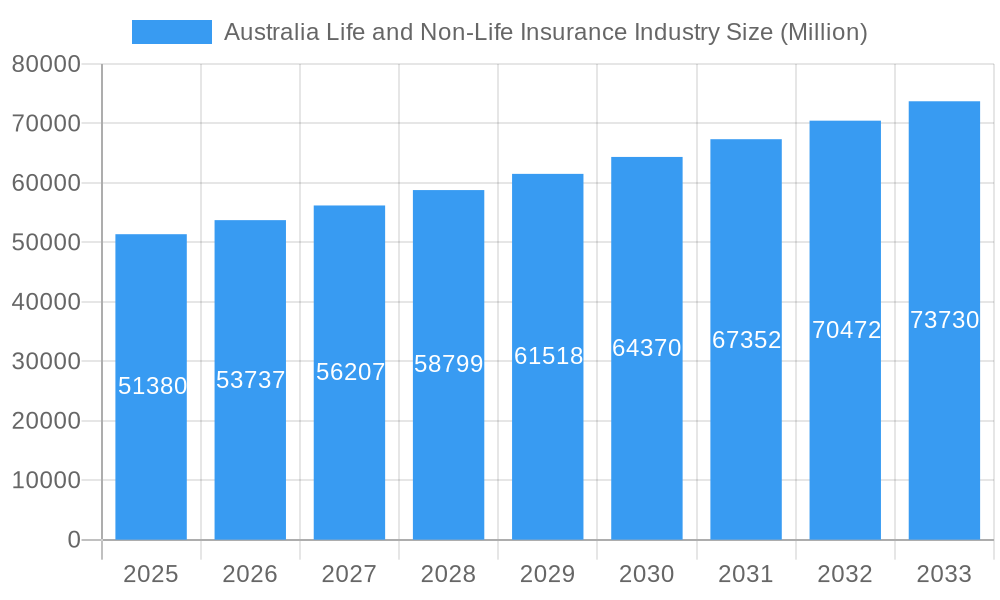

The Australian life and non-life insurance market, valued at $51.38 billion in 2025, is projected to experience steady growth, driven by a rising insured population, increasing awareness of risk mitigation, and favorable government regulations promoting financial inclusion. The Compound Annual Growth Rate (CAGR) of 4.56% from 2025 to 2033 suggests a significant expansion of the market over the forecast period. Key growth drivers include the increasing prevalence of chronic illnesses, necessitating health insurance, and a rising demand for retirement planning solutions, bolstering the life insurance segment. Technological advancements, such as digital insurance platforms and AI-powered risk assessment tools, are streamlining operations and improving customer experience, further fueling market expansion. However, challenges such as intense competition, stringent regulatory oversight, and economic fluctuations represent potential restraints. The market is segmented by product type (life, health, property, casualty), distribution channels (online, agents, brokers), and customer demographics. Major players like Insurance Australia Group, Suncorp Group, and AIA Group Limited dominate the landscape, vying for market share through product innovation and strategic partnerships.

Australia Life and Non-Life Insurance Industry Market Size (In Billion)

The forecast period of 2025-2033 anticipates continued growth, influenced by demographic shifts, economic progress, and evolving consumer preferences towards personalized insurance solutions. While economic downturns could temporarily impact market expansion, the long-term outlook remains positive, given the inherent need for risk protection in a dynamic environment. Specific regional variations are expected within Australia, with higher growth potentially observed in urban centers experiencing rapid population growth and increased economic activity. The competitive landscape is likely to remain dynamic, with existing players focused on mergers and acquisitions, diversification, and digital transformation strategies to maintain their competitive edge. Focus on customer retention through enhanced service offerings and personalized solutions will be crucial for success in this increasingly competitive and technology-driven market.

Australia Life and Non-Life Insurance Industry Company Market Share

Australia Life and Non-Life Insurance Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Australian life and non-life insurance industry, covering market dynamics, trends, leading players, and future opportunities. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an indispensable resource for industry stakeholders, investors, and strategic planners. The report leverages extensive data analysis and expert insights to offer actionable intelligence for informed decision-making. Key players analyzed include Insurance Australia Group Limited, Suncorp Group, AIA Group Limited, Zurich, Medibank Private Limited, Genworth Mortgage Insurance Australia Limited, ClearView Wealth Limited, Cover-More Limited, AMP Limited, and NIB Holdings Limited (list not exhaustive).

Australia Life and Non-Life Insurance Industry Market Dynamics & Concentration

The Australian life and non-life insurance market exhibits a moderately concentrated structure, with a few large players holding significant market share. IAG, Suncorp, and AIA Group collectively command an estimated xx% of the market (2024). Market concentration is influenced by several factors, including stringent regulatory frameworks, high barriers to entry, and economies of scale enjoyed by established players. Innovation in areas like InsurTech, particularly the growing adoption of IoT and AI-powered solutions, is driving competition and reshaping the market landscape. The increasing prevalence of online platforms and digital distribution channels is further intensifying competition. The industry has witnessed significant M&A activity in recent years, with xx major deals concluded between 2019 and 2024, primarily driven by a desire for expansion, diversification, and improved technological capabilities. Substitute products, such as self-insurance options for SMEs, are also emerging and gaining traction. Consumer trends favor personalized products, digital-first experiences, and greater transparency in pricing and claims processing.

- Market Share: IAG xx%, Suncorp xx%, AIA xx%, Others xx% (2024)

- M&A Deal Count: xx (2019-2024)

- Key Innovation Drivers: InsurTech, IoT, AI

- Regulatory Framework: APRA, ASIC

Australia Life and Non-Life Insurance Industry Industry Trends & Analysis

The Australian life and non-life insurance market demonstrates robust growth, driven by factors such as rising disposable incomes, increasing awareness of insurance products, and a growing aging population. The market is estimated to grow at a CAGR of xx% from 2025 to 2033, reaching a market size of approximately $XX Million by 2033. Technological advancements, specifically digitalization and the use of big data and analytics, are significantly influencing the industry. Consumers increasingly favor online platforms for purchasing and managing insurance policies, demanding seamless digital experiences. Competitive dynamics are shaped by price wars, product differentiation, and the emergence of InsurTech companies. Market penetration for life insurance remains comparatively lower than in other developed countries indicating potential for further growth. The increasing adoption of embedded insurance, where insurance is integrated into other products or services, is also expected to drive market expansion. Furthermore, the rise of climate change awareness is forcing a focus on climate risk underwriting and product development.

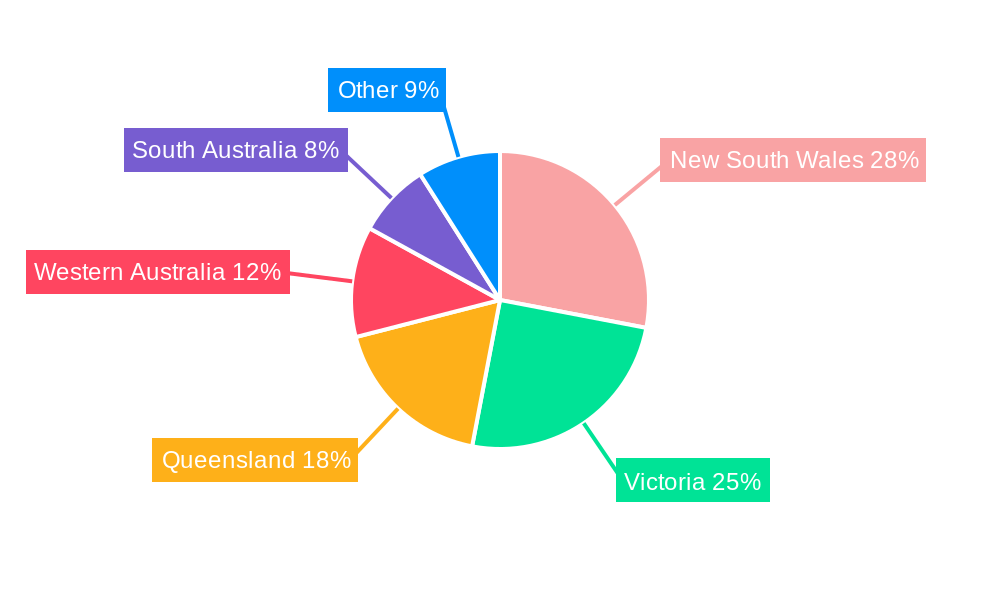

Leading Markets & Segments in Australia Life and Non-Life Insurance Industry

The Australian life and non-life insurance market is geographically diverse, with significant presence across all states and territories. However, the major metropolitan areas like Sydney, Melbourne, and Brisbane exhibit the highest concentration of insured individuals and businesses driving higher premiums and revenue. The non-life segment holds a larger share of the overall market, driven by a combination of mandatory insurance requirements, greater consumer awareness and relatively simpler and quicker digital adoption.

- Key Drivers:

- Strong economic growth in major metropolitan areas

- High population density

- Developed infrastructure and financial systems

The dominance of metropolitan areas is primarily attributed to a higher concentration of businesses and individuals with greater disposable incomes. Furthermore, regulatory frameworks, robust infrastructure, and a strong financial system contribute to a stable and conducive market environment.

Australia Life and Non-Life Insurance Industry Product Developments

Significant product innovations are transforming the Australian insurance landscape. The integration of IoT devices for risk assessment and prevention is gaining momentum, as seen in IAG's investment in Myriota. The rise of personalized insurance products, tailored to specific individual needs and risk profiles, is also enhancing customer experience and driving product differentiation. The development of online platforms simplifies the purchasing process and provides improved accessibility to insurance products. These developments leverage technological advancements, improving market fit by providing more convenient, affordable, and personalized coverage.

Key Drivers of Australia Life and Non-Life Insurance Industry Growth

Several key factors fuel the growth of the Australian life and non-life insurance industry. Technological advancements, such as AI-powered risk assessment and personalized products, enhance efficiency and customer satisfaction. Positive economic growth boosts disposable incomes, fueling demand for insurance coverage. Favorable regulatory environments promoting competition and innovation also play a significant role. The increasing awareness of financial planning and protection needs further drives growth. Finally, the rise of climate-related risks is leading to an increasing focus on related insurance products.

Challenges in the Australia Life and Non-Life Insurance Industry Market

The Australian life and non-life insurance industry faces several challenges. Stringent regulatory requirements increase compliance costs, impacting profitability. Cybersecurity threats pose significant risks to data privacy and operational security. Intense competition from both traditional and InsurTech players necessitates strategic innovation and efficient cost management to maintain market share and profitability. The challenge of climate-related risks and its impact on insurance coverage also necessitates considerable investment.

Emerging Opportunities in Australia Life and Non-Life Insurance Industry

The Australian life and non-life insurance industry presents considerable long-term growth potential. The expansion of InsurTech solutions, particularly AI and machine learning, offers opportunities for improved risk assessment and personalized product development. Strategic partnerships between traditional insurers and InsurTech companies create synergies for innovation and market expansion. Growing demand for specialized insurance products, particularly those addressing specific risks such as cyber security or climate change, creates new revenue streams. Expansion into underserved market segments further offers growth opportunities.

Leading Players in the Australia Life and Non-Life Insurance Industry Sector

- Insurance Australia Group Limited

- Suncorp Group

- AIA Group Limited

- Zurich

- Medibank Private Limited

- Genworth Mortgage Insurance Australia Limited

- ClearView Wealth Limited

- Cover-More Limited

- AMP Limited

- NIB Holdings Limited

Key Milestones in Australia Life and Non-Life Insurance Industry Industry

- September 2022: Launch of io.Insure, the world's first online marketplace for M&A insurance for SMEs.

- February 2023: IAG invests in Myriota for IoT-based risk management solutions.

Strategic Outlook for Australia Life and Non-Life Insurance Industry Market

The Australian life and non-life insurance market presents significant growth potential driven by technological advancements, evolving consumer preferences, and a focus on risk management. Strategic partnerships, product innovation, and expansion into emerging segments will be crucial for capturing market share and driving long-term success. Insurers who effectively leverage technology to enhance customer experience and optimize operations will be well-positioned for growth in the coming years. A focus on sustainability and climate change related risks will be crucial for long term viability.

Australia Life and Non-Life Insurance Industry Segmentation

-

1. Insurance Type

-

1.1. Life insurance

- 1.1.1. Individual

- 1.1.2. Group

-

1.2. Non-Life Insurance

- 1.2.1. Fire

- 1.2.2. Motor

- 1.2.3. Marine

- 1.2.4. Health

- 1.2.5. Other Non-Life Insurance

-

1.1. Life insurance

-

2. Distribution Channel

- 2.1. Direct

- 2.2. Brokers

- 2.3. Banks

- 2.4. Other Distribution Channels

Australia Life and Non-Life Insurance Industry Segmentation By Geography

- 1. Australia

Australia Life and Non-Life Insurance Industry Regional Market Share

Geographic Coverage of Australia Life and Non-Life Insurance Industry

Australia Life and Non-Life Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 5.1.1. Life insurance

- 5.1.1.1. Individual

- 5.1.1.2. Group

- 5.1.2. Non-Life Insurance

- 5.1.2.1. Fire

- 5.1.2.2. Motor

- 5.1.2.3. Marine

- 5.1.2.4. Health

- 5.1.2.5. Other Non-Life Insurance

- 5.1.1. Life insurance

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Direct

- 5.2.2. Brokers

- 5.2.3. Banks

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6. Australia Life and Non-Life Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6.1.1. Life insurance

- 6.1.1.1. Individual

- 6.1.1.2. Group

- 6.1.2. Non-Life Insurance

- 6.1.2.1. Fire

- 6.1.2.2. Motor

- 6.1.2.3. Marine

- 6.1.2.4. Health

- 6.1.2.5. Other Non-Life Insurance

- 6.1.1. Life insurance

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Direct

- 6.2.2. Brokers

- 6.2.3. Banks

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Insurance Australia Group Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Suncorp Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 AIA Group Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Zurich

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Medibank Private Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Genworth Mortgage Insurance Australia Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 ClearView Wealth Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Cover-More Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AMP Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 NIB Holdings Limited**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Insurance Australia Group Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia Life and Non-Life Insurance Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Australia Life and Non-Life Insurance Industry Share (%) by Company 2025

List of Tables

- Table 1: Australia Life and Non-Life Insurance Industry Revenue Million Forecast, by Insurance Type 2020 & 2033

- Table 2: Australia Life and Non-Life Insurance Industry Volume Billion Forecast, by Insurance Type 2020 & 2033

- Table 3: Australia Life and Non-Life Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Australia Life and Non-Life Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 5: Australia Life and Non-Life Insurance Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Australia Life and Non-Life Insurance Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 7: Australia Life and Non-Life Insurance Industry Revenue Million Forecast, by Insurance Type 2020 & 2033

- Table 8: Australia Life and Non-Life Insurance Industry Volume Billion Forecast, by Insurance Type 2020 & 2033

- Table 9: Australia Life and Non-Life Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 10: Australia Life and Non-Life Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 11: Australia Life and Non-Life Insurance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Australia Life and Non-Life Insurance Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Life and Non-Life Insurance Industry?

The projected CAGR is approximately 4.56%.

2. Which companies are prominent players in the Australia Life and Non-Life Insurance Industry?

Key companies in the market include Insurance Australia Group Limited, Suncorp Group, AIA Group Limited, Zurich, Medibank Private Limited, Genworth Mortgage Insurance Australia Limited, ClearView Wealth Limited, Cover-More Limited, AMP Limited, NIB Holdings Limited**List Not Exhaustive.

3. What are the main segments of the Australia Life and Non-Life Insurance Industry?

The market segments include Insurance Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 51.38 Million as of 2022.

5. What are some drivers contributing to market growth?

Guaranteed Protection Drives The Market.

6. What are the notable trends driving market growth?

Motor Vehicle and Household Insurance has the Largest Shares.

7. Are there any restraints impacting market growth?

Guaranteed Protection Drives The Market.

8. Can you provide examples of recent developments in the market?

February 2023: Insurance Australia Group Limited (IAG), Australia's largest general insurer, invested in Myriota, a global pioneer in low-cost and low-power satellite connectivity for the Internet of Things (IoT). This aim was to explore how IoT devices can help insurance customers manage risk and safeguard their assets.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Life and Non-Life Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Life and Non-Life Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Life and Non-Life Insurance Industry?

To stay informed about further developments, trends, and reports in the Australia Life and Non-Life Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence