Key Insights

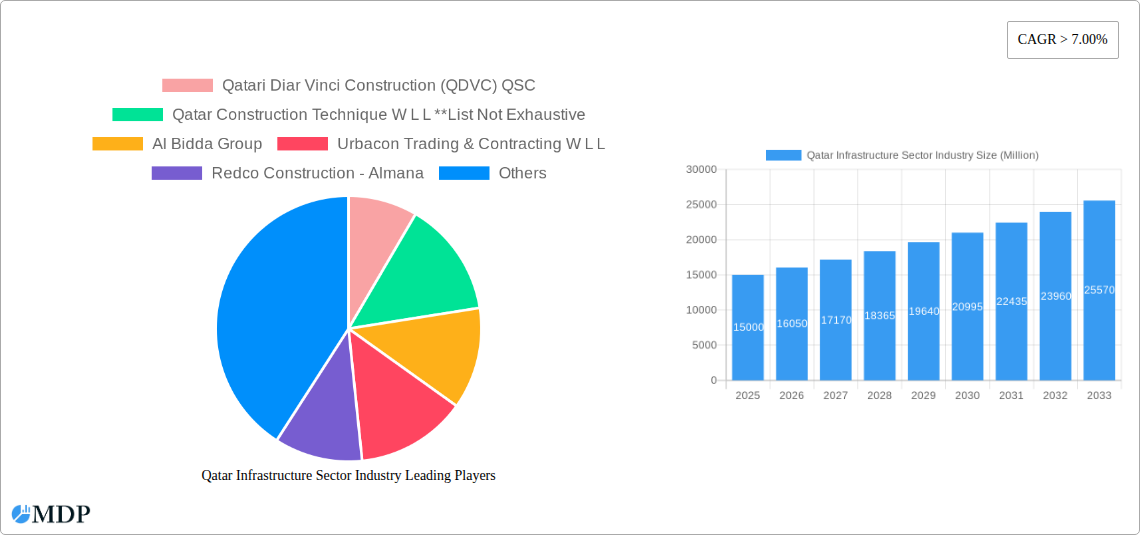

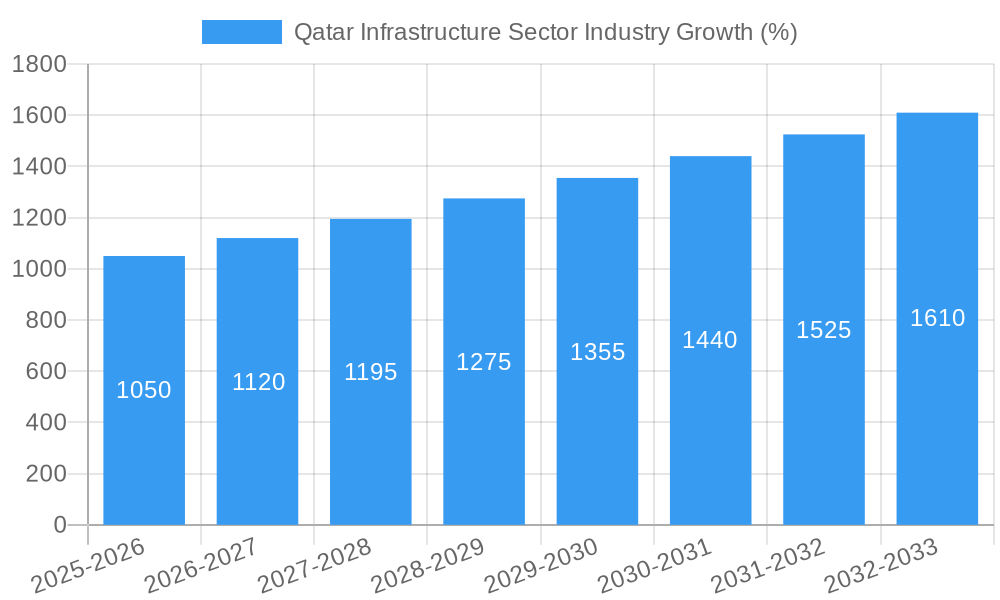

The Qatari infrastructure sector is experiencing robust growth, projected to maintain a Compound Annual Growth Rate (CAGR) exceeding 7% from 2025 to 2033. This expansion is fueled by significant government investments in mega-projects related to the FIFA World Cup 2022 legacy and the country's long-term vision for diversification and sustainable development. Key drivers include the ongoing development of transportation infrastructure (roads, railways, airports, and seaports), social infrastructure (housing, healthcare, and education facilities), and the expansion of energy and industrial sectors requiring robust extraction and manufacturing infrastructure. The market is segmented into Social, Transportation, Extraction, and Manufacturing infrastructure, each contributing significantly to the overall growth. Leading companies like Qatari Diar Vinci Construction (QDVC) QSC, Qatar Construction Technique, Al Bidda Group, and others play a crucial role in shaping this dynamic landscape. The sector's growth trajectory is influenced by factors such as consistent government spending, a strong private sector involvement, and a commitment to utilizing innovative technologies.

However, challenges exist. Potential restraints include fluctuations in global commodity prices, the availability of skilled labor, and the need to balance rapid development with environmental sustainability. To mitigate these risks, proactive strategies are needed to enhance project management efficiency, improve workforce training programs, and ensure responsible resource allocation and environmentally friendly construction practices. The significant investment in infrastructure projects makes Qatar an attractive market for both local and international players seeking opportunities in the construction and related industries. Continued diversification of the economy beyond hydrocarbons will further boost demand for sophisticated infrastructure development and enhance long-term sustainability. The foreseeable future points towards continued expansion and a strengthening position of Qatar as a regional leader in infrastructure development.

Qatar Infrastructure Sector Industry: 2019-2033 Market Report - A Comprehensive Analysis

This comprehensive report provides an in-depth analysis of the Qatar Infrastructure Sector Industry, covering market dynamics, trends, leading players, and future opportunities from 2019 to 2033. The study period encompasses historical data (2019-2024), a base year (2025), and a forecast period (2025-2033), offering a complete picture of the sector's evolution and future trajectory. The report is essential for industry stakeholders, investors, and government agencies seeking to understand and capitalize on the significant growth potential in Qatar's infrastructure development. Key players like Qatari Diar Vinci Construction (QDVC) QSC, Qatar Construction Technique W L L, Al Bidda Group, Urbacon Trading & Contracting W L L, Redco Construction - Almana, Arabian Construction Engineering Company, ALEC, Al Jaber Engineering Co, United Construction Est W L L, and Gulf Housing & Construction Co are analyzed within the context of market trends.

Qatar Infrastructure Sector Industry Market Dynamics & Concentration

The Qatar infrastructure sector exhibits a moderately concentrated market structure, with several large players commanding significant market share. While precise figures for market share are unavailable publicly and require extensive primary research, we estimate that the top 5 companies hold approximately xx% of the overall market in 2025, reflecting a trend towards consolidation in recent years. Innovation in the sector is driven by government initiatives promoting sustainable development, technological advancements (e.g., BIM, IoT), and the demand for efficient and resilient infrastructure solutions. The regulatory framework, while generally supportive of investment, involves complex permitting processes and stringent environmental regulations. Product substitutes are limited; however, increased focus on cost-effectiveness and lifecycle considerations introduces competitive pressure. End-user trends favour sustainable and smart infrastructure, shaping technological choices and material selection. M&A activity has been moderate, with an estimated xx number of deals completed between 2019 and 2024. This signifies a potential for further consolidation as companies seek scale and expertise.

- Market Concentration: Estimated top 5 company market share: xx% in 2025

- M&A Activity: Approximately xx deals between 2019-2024

- Key Drivers of Innovation: Sustainable development initiatives, technological advancements (BIM, IoT), demand for resilient infrastructure

- Regulatory Landscape: Supportive but involves complex processes and stringent environmental regulations

Qatar Infrastructure Sector Industry Industry Trends & Analysis

The Qatar infrastructure sector is projected to experience robust growth over the forecast period, driven by substantial government investment in mega-projects related to the FIFA World Cup and the nation's long-term vision. The compound annual growth rate (CAGR) is estimated at xx% from 2025 to 2033, fuelled by expanding urbanization, population growth, and diversification of the economy. Technological disruptions, including the adoption of Building Information Modeling (BIM), digital twins, and smart city technologies, are transforming project design, construction, and management. Consumer preferences shift towards sustainable infrastructure solutions, promoting environmentally friendly materials and construction methods. The competitive landscape is dynamic, with both local and international companies vying for market share. Market penetration of advanced construction technologies remains relatively low, presenting opportunities for early adopters to gain a competitive edge.

Leading Markets & Segments in Qatar Infrastructure Sector Industry

The Transportation Infrastructure segment currently dominates the Qatar infrastructure market, accounting for the largest share of investment and construction activity. This dominance stems from ongoing major projects related to road networks, rail expansion, and airport upgrades. The Social Infrastructure segment, encompassing healthcare facilities, educational institutions, and housing, is also experiencing strong growth, driven by the nation’s focus on improving living standards and quality of life. Extraction and Manufacturing infrastructure segments contribute significantly, aligning with the country's economic diversification efforts and industrial development strategy.

- Transportation Infrastructure: Key Drivers: FIFA World Cup legacy projects, expansion of Doha Metro, Hamad International Airport upgrades, Road network improvements.

- Social Infrastructure: Key Drivers: Increasing population, focus on improving living standards, government investment in education and healthcare facilities.

- Extraction Infrastructure: Key Drivers: Expansion of the energy sector, focus on gas and oil infrastructure development.

- Manufacturing Infrastructure: Key Drivers: Industrial diversification strategy, focus on building industrial zones and supporting manufacturing operations.

Qatar Infrastructure Sector Industry Product Developments

Recent product innovations focus on prefabricated construction methods, modular designs, and the integration of smart technologies for improved efficiency and sustainability. These advancements are enhancing project speed, reducing waste, and improving overall asset lifecycle performance. The market is witnessing a growing demand for environmentally friendly construction materials and sustainable building practices. This trend is strongly driven by government policies and consumer preference.

Key Drivers of Qatar Infrastructure Sector Industry Growth

Several factors drive the growth of Qatar's infrastructure sector: substantial government spending, particularly on mega-projects; a growing population requiring increased infrastructure capacity; the diversification of the economy, necessitating industrial and logistics infrastructure; the increasing adoption of sustainable construction practices, and technological advancements that improve efficiency and productivity. The continued commitment to large-scale developments, including the expansion of transportation networks and the development of new city districts, promises sustained growth.

Challenges in the Qatar Infrastructure Sector Industry Market

The sector faces challenges such as securing skilled labor, navigating complex regulatory procedures, and managing supply chain risks, particularly concerning material availability and cost fluctuations. Extreme weather conditions can also impact project timelines and budgets. Furthermore, intense competition from international contractors requires local firms to demonstrate expertise and efficiency. These factors can impact project delivery timelines and budgets, necessitating careful planning and risk management.

Emerging Opportunities in Qatar Infrastructure Sector Industry

Significant opportunities exist in the adoption of advanced technologies such as BIM, IoT, and AI, enabling efficient project management, improved safety, and sustainable infrastructure development. Strategic partnerships between international and local companies can foster knowledge transfer and technological advancements. Government initiatives promoting sustainable practices provide lucrative opportunities for firms focusing on green infrastructure solutions. Expanding into new infrastructure segments, such as smart city technologies and renewable energy infrastructure, presents further avenues for growth.

Leading Players in the Qatar Infrastructure Sector Industry Sector

- Qatari Diar Vinci Construction (QDVC) QSC

- Qatar Construction Technique W L L

- Al Bidda Group

- Urbacon Trading & Contracting W L L

- Redco Construction - Almana

- Arabian Construction Engineering Company

- ALEC

- Al Jaber Engineering Co

- United Construction Est W L L

- Gulf Housing & Construction Co

Key Milestones in Qatar Infrastructure Sector Industry Industry

- 2019-2024: Significant investment in transportation infrastructure projects related to the FIFA World Cup.

- 2022: Completion of key World Cup stadium projects and related transportation infrastructure.

- 2023: Launch of several smart city initiatives.

- 2025 (Ongoing): Continued investment in large-scale infrastructure projects across various segments.

Strategic Outlook for Qatar Infrastructure Sector Industry Market

The long-term outlook for Qatar's infrastructure sector is positive, with projected sustained growth driven by ongoing government investment, economic diversification, and population growth. The focus on sustainable development and technological advancements presents significant opportunities for innovative companies to capture market share and contribute to the nation's ambitious development goals. The sector is well-positioned for continued expansion and a strong contribution to Qatar's long-term economic prosperity.

Qatar Infrastructure Sector Industry Segmentation

-

1. Infrastructure segment

- 1.1. Social Infrastructure

- 1.2. Transportation Infrastructure

- 1.3. Extraction Infrastructure

- 1.4. Manufacturing Infrastructure

Qatar Infrastructure Sector Industry Segmentation By Geography

- 1. Qatar

Qatar Infrastructure Sector Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 7.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Rapid Urabanization4.; Increasing government investments

- 3.3. Market Restrains

- 3.3.1. 4.; Increasing cost of raw materials affecting the construction industry4.; Slowdown in economic growth affecting the market

- 3.4. Market Trends

- 3.4.1. The Government's Focus on the Construction Industry Boosting the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Qatar Infrastructure Sector Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Infrastructure segment

- 5.1.1. Social Infrastructure

- 5.1.2. Transportation Infrastructure

- 5.1.3. Extraction Infrastructure

- 5.1.4. Manufacturing Infrastructure

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Qatar

- 5.1. Market Analysis, Insights and Forecast - by Infrastructure segment

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Qatari Diar Vinci Construction (QDVC) QSC

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Qatar Construction Technique W L L **List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Al Bidda Group

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Urbacon Trading & Contracting W L L

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Redco Construction - Almana

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Arabian Construction Engineering Company

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 ALEC

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Al Jaber Engineering Co

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 United Construction Est W L L

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Gulf Housing & Construction Co

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Qatari Diar Vinci Construction (QDVC) QSC

List of Figures

- Figure 1: Qatar Infrastructure Sector Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Qatar Infrastructure Sector Industry Share (%) by Company 2024

List of Tables

- Table 1: Qatar Infrastructure Sector Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Qatar Infrastructure Sector Industry Revenue Million Forecast, by Infrastructure segment 2019 & 2032

- Table 3: Qatar Infrastructure Sector Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Qatar Infrastructure Sector Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Qatar Infrastructure Sector Industry Revenue Million Forecast, by Infrastructure segment 2019 & 2032

- Table 6: Qatar Infrastructure Sector Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Qatar Infrastructure Sector Industry?

The projected CAGR is approximately > 7.00%.

2. Which companies are prominent players in the Qatar Infrastructure Sector Industry?

Key companies in the market include Qatari Diar Vinci Construction (QDVC) QSC, Qatar Construction Technique W L L **List Not Exhaustive, Al Bidda Group, Urbacon Trading & Contracting W L L, Redco Construction - Almana, Arabian Construction Engineering Company, ALEC, Al Jaber Engineering Co, United Construction Est W L L, Gulf Housing & Construction Co.

3. What are the main segments of the Qatar Infrastructure Sector Industry?

The market segments include Infrastructure segment.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Rapid Urabanization4.; Increasing government investments.

6. What are the notable trends driving market growth?

The Government's Focus on the Construction Industry Boosting the Market.

7. Are there any restraints impacting market growth?

4.; Increasing cost of raw materials affecting the construction industry4.; Slowdown in economic growth affecting the market.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Qatar Infrastructure Sector Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Qatar Infrastructure Sector Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Qatar Infrastructure Sector Industry?

To stay informed about further developments, trends, and reports in the Qatar Infrastructure Sector Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence