Key Insights

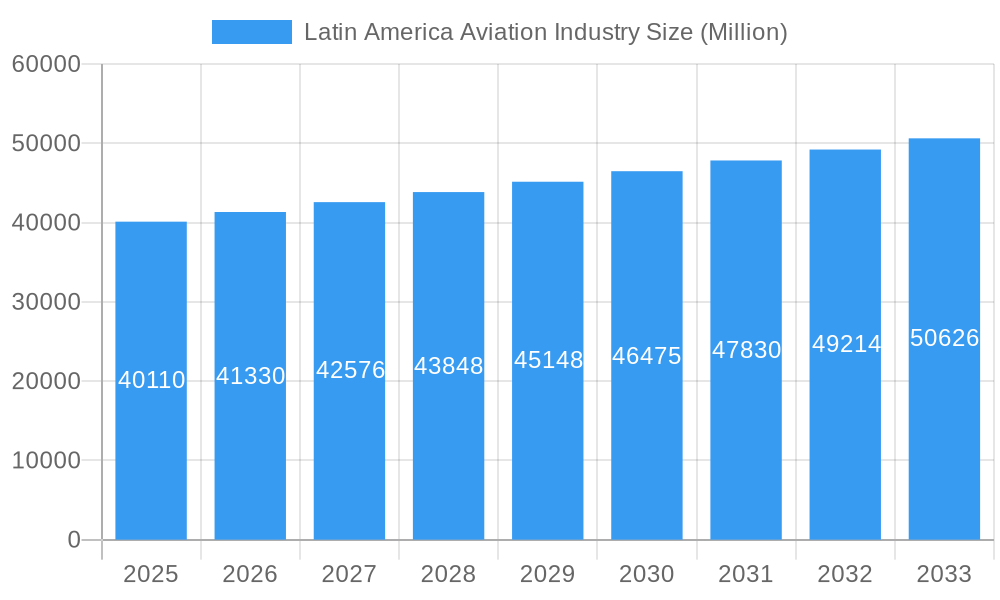

The Latin American aviation industry, valued at $40.11 billion in 2025, is projected to experience steady growth, exhibiting a Compound Annual Growth Rate (CAGR) of 3.03% from 2025 to 2033. This growth is fueled by several key factors. Firstly, increasing tourism and business travel within the region are driving demand for both commercial and general aviation services. The expansion of infrastructure, including airport upgrades and the development of new routes, further supports this expansion. Secondly, the modernization of existing fleets and the acquisition of new, fuel-efficient aircraft contribute to the industry's positive trajectory. Finally, government initiatives aimed at promoting air connectivity within Latin America are playing a crucial role in market stimulation. However, economic volatility in certain Latin American countries and potential fuel price fluctuations remain significant challenges.

Latin America Aviation Industry Market Size (In Billion)

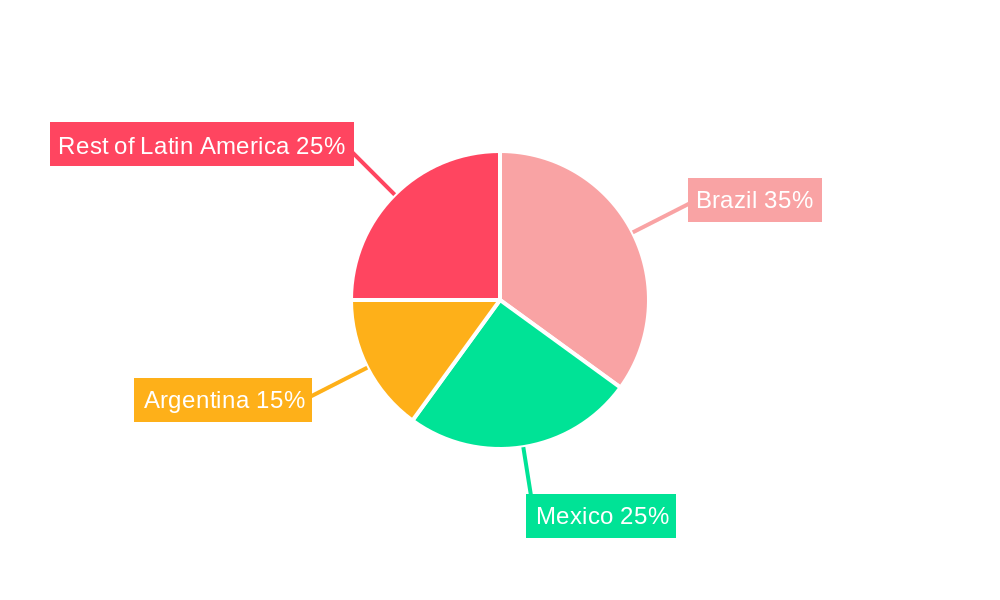

Despite these challenges, the segment breakdown indicates a robust outlook. Commercial aviation is expected to be the largest contributor, driven by the growth of low-cost carriers and the rising middle class with increased disposable income for air travel. Military aircraft procurement, while a smaller segment, is also anticipated to see modest growth, influenced by regional security concerns and modernization efforts. The general aviation segment, encompassing private and business jets, is expected to expand gradually, driven by demand from high-net-worth individuals and corporations. Brazil, Argentina, and Mexico are the largest markets within Latin America, owing to their developed economies and infrastructure. The growth in these key markets will serve as a primary driver of overall regional expansion, supported by strategic investments and the expansion of regional connectivity. The forecast period of 2025-2033 reflects a continuation of these trends, indicating a promising, although nuanced, growth outlook for the Latin American aviation market.

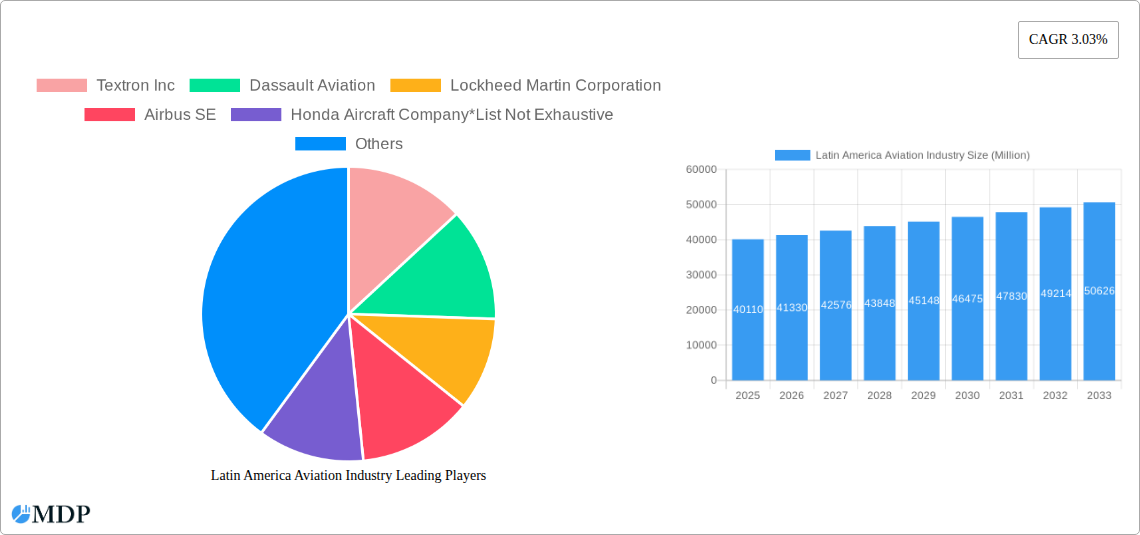

Latin America Aviation Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Latin America aviation industry, covering market dynamics, industry trends, leading players, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an essential resource for industry stakeholders, investors, and strategic decision-makers.

Latin America Aviation Industry Market Dynamics & Concentration

The Latin American aviation market is characterized by a complex interplay of factors influencing its growth and concentration. Market share is currently dominated by a few key players, with The Boeing Company, Embraer SA, and Airbus SE holding significant portions. However, the competitive landscape is dynamic, with smaller players and new entrants vying for market share. The market exhibits a moderate level of concentration, with a Herfindahl-Hirschman Index (HHI) estimated at xx in 2025. Innovation, driven by the need for fuel efficiency and technological advancements, is a major driver. Regulatory frameworks, varying across different Latin American countries, significantly impact operational costs and market access. The emergence of low-cost carriers is introducing a disruptive force, acting as a product substitute for traditional airlines. End-user trends, including increasing demand for air travel and the growth of e-commerce, are fuelling market growth. M&A activity has been relatively modest in recent years, with approximately xx deals recorded between 2019 and 2024, reflecting a cautious approach amidst economic uncertainties.

- Market Concentration (HHI 2025): xx

- M&A Deal Count (2019-2024): xx

- Top 3 Players Market Share (2025): xx%

Latin America Aviation Industry Industry Trends & Analysis

The Latin American aviation industry is experiencing robust growth, driven by several key factors. The Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is projected at xx%, reflecting a significant increase in air travel demand fueled by rising disposable incomes, expanding tourism, and robust economic growth in several key markets. Technological disruptions, such as the adoption of advanced aircraft technologies and digital solutions, are enhancing operational efficiency and customer experience. Consumer preferences are shifting towards more affordable and convenient travel options, creating opportunities for low-cost carriers and innovative service offerings. The competitive dynamics are intense, with established players competing fiercely for market share while also grappling with the challenges posed by new entrants and disruptive technologies. Market penetration of low-cost carriers is steadily increasing, with xx% market share estimated for 2025. This trend is further expected to increase to xx% by 2033. The industry is also experiencing increasing pressure to adopt sustainable practices, particularly in reducing carbon emissions, as environmental concerns gain prominence.

Leading Markets & Segments in Latin America Aviation Industry

Brazil and Mexico represent the dominant markets within Latin America's aviation sector, accounting for approximately xx% and xx% of the total market value respectively, in 2025. This dominance is attributed to factors such as larger population bases, robust economies, well-established infrastructure, and substantial tourism sectors. The commercial aircraft segment holds the largest market share (xx% in 2025), owing to the significant demand for passenger air travel. However, the general aviation segment is witnessing notable growth fueled by increasing private and business travel.

Key Drivers for Brazil and Mexico:

Latin America Aviation Industry Product Developments

Recent product innovations have focused on improving fuel efficiency, enhancing passenger comfort, and incorporating advanced technologies. This includes the introduction of new-generation aircraft with improved aerodynamics and lighter materials, as well as the integration of advanced avionics and in-flight entertainment systems. These advancements offer significant competitive advantages by reducing operating costs, improving safety, and enhancing the overall travel experience. The market is showing a strong preference for fuel-efficient aircraft designs and sustainable aviation fuels (SAFs) owing to rising fuel costs and growing environmental concerns.

Key Drivers of Latin America Aviation Industry Growth

The growth of the Latin American aviation industry is propelled by several key factors: the expansion of the middle class, fostering increased air travel demand; strong economic growth in several countries leading to higher disposable incomes; burgeoning tourism sectors attracting international and domestic travelers; significant infrastructure development enhancing airport capacity and connectivity; and supportive government policies encouraging investments in aviation. Technological advancements, like improved aircraft designs and digital solutions, boost efficiency and enhance the overall passenger experience.

Challenges in the Latin America Aviation Industry Market

The Latin American aviation industry faces challenges like inconsistent regulatory frameworks across different countries resulting in operational complexities; infrastructural limitations in certain regions leading to bottlenecks and delays; and volatile fuel prices influencing operating costs significantly. Furthermore, intense competition from both established and new entrants increases pressure on profitability. Supply chain disruptions also pose a risk to operations and growth, particularly regarding spare parts and maintenance. These factors collectively impact the overall financial health and sustainability of the industry.

Emerging Opportunities in Latin America Aviation Industry

Significant long-term growth opportunities are emerging due to the increasing adoption of digital technologies, leading to enhanced operational efficiency and improved customer experiences. Strategic partnerships between airlines and other stakeholders, such as tourism agencies and technology providers, offer pathways for market expansion and product diversification. The exploration of sustainable aviation fuels and eco-friendly technologies is not only crucial for compliance but also presents a significant opportunity to attract environmentally-conscious consumers and gain a competitive edge.

Leading Players in the Latin America Aviation Industry Sector

Key Milestones in Latin America Aviation Industry Industry

- October 2022: Air Canada Cargo expands its freighter network to the US (Dallas and Atlanta) and adds service to Bogota, Colombia. This signifies increased focus on Latin American markets and cargo operations.

- September 2022: Avianca and Boliviana de Aviación sign an interline agreement, enhancing connectivity within Latin America and expanding passenger reach to 24 countries. This highlights the importance of strategic partnerships and increased regional collaboration.

Strategic Outlook for Latin America Aviation Industry Market

The Latin American aviation industry is poised for continued growth, driven by expanding air travel demand, infrastructure improvements, and technological advancements. Strategic opportunities exist for airlines to capitalize on the rising middle class, increase regional connectivity, and embrace sustainable practices. By focusing on operational efficiency, customer experience, and strategic partnerships, players can achieve long-term success and capture a significant share of the burgeoning market potential. The implementation of robust digital strategies will also be key to optimizing operations and enhancing customer satisfaction.

Latin America Aviation Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Latin America Aviation Industry Segmentation By Geography

-

1. Latin America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Mexico

- 1.6. Peru

- 1.7. Venezuela

- 1.8. Ecuador

- 1.9. Bolivia

- 1.10. Paraguay

Latin America Aviation Industry Regional Market Share

Geographic Coverage of Latin America Aviation Industry

Latin America Aviation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.03% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Latin America

- 6. Latin America Aviation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Textron Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Dassault Aviation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Lockheed Martin Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Airbus SE

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Honda Aircraft Company*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Embraer SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Bombardier Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Saab AB

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Leonardo SPA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 The Boeing Company

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Textron Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Latin America Aviation Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Latin America Aviation Industry Share (%) by Company 2025

List of Tables

- Table 1: Latin America Aviation Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Latin America Aviation Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Latin America Aviation Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Latin America Aviation Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Latin America Aviation Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Latin America Aviation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Latin America Aviation Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Latin America Aviation Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Latin America Aviation Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Latin America Aviation Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Latin America Aviation Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Latin America Aviation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Brazil Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Chile Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Colombia Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Mexico Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Peru Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Venezuela Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Ecuador Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Bolivia Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Paraguay Latin America Aviation Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Aviation Industry?

The projected CAGR is approximately 3.03%.

2. Which companies are prominent players in the Latin America Aviation Industry?

Key companies in the market include Textron Inc, Dassault Aviation, Lockheed Martin Corporation, Airbus SE, Honda Aircraft Company*List Not Exhaustive, Embraer SA, Bombardier Inc, Saab AB, Leonardo SPA, The Boeing Company.

3. What are the main segments of the Latin America Aviation Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 40.11 Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Internet of Things (IoT) and Autonomous Systems; Rise in Demand for Military and Defense Satellite Communication Solutions.

6. What are the notable trends driving market growth?

Commercial Aircraft Market is Expected to Have the Largest Market Share During the Forecast Period.

7. Are there any restraints impacting market growth?

Cybersecurity Threats to Satellite Communication; Interference in Transmission of Data.

8. Can you provide examples of recent developments in the market?

In October 2022, Air Canada Cargo announced the expansion of its freighter network into the United States for the first time, with flights to Dallas and Atlanta. The company will also expand its presence in Latin America with service to Bogota, Colombia.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Aviation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Aviation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Aviation Industry?

To stay informed about further developments, trends, and reports in the Latin America Aviation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence